Investor Presentation April 2019 SAFE HARBOR

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Official Form 309F (For Corporations Or Partnerships)

17-22445-rdd Doc 9 Filed 03/28/17 Entered 03/28/17 11:28:37 Ch 11 First Mtg Corp/Part Pg 1 of 3 Information to identify the case: Debtor Metro Newspaper Advertising Services, Inc. EIN 13−1038730 Name United States Bankruptcy Court Southern District of New York Date case filed for chapter 11 3/27/17 Case number: 17−22445−rdd Official Form 309F (For Corporations or Partnerships) Notice of Chapter 11 Bankruptcy Case 12/15 For the debtor listed above, a case has been filed under chapter 11 of the Bankruptcy Code. An order for relief has been entered. This notice has important information about the case for creditors, debtors, and trustees, including information about the meeting of creditors and deadlines. Read both pages carefully. The filing of the case imposed an automatic stay against most collection activities. This means that creditors generally may not take action to collect debts from the debtor or the debtor's property. For example, while the stay is in effect, creditors cannot sue, assert a deficiency, repossess property, or otherwise try to collect from the debtor. Creditors cannot demand repayment from the debtor by mail, phone, or otherwise. Creditors who violate the stay can be required to pay actual and punitive damages and attorney's fees. Confirmation of a chapter 11 plan may result in a discharge of debt. A creditor who wants to have a particular debt excepted from discharge may be required to file a complaint in the bankruptcy clerk's office within the deadline specified in this notice. -

Minority Percentages at Participating Newspapers

Minority Percentages at Participating Newspapers Asian Native Asian Native Am. Black Hisp Am. Total Am. Black Hisp Am. Total ALABAMA The Anniston Star........................................................3.0 3.0 0.0 0.0 6.1 Free Lance, Hollister ...................................................0.0 0.0 12.5 0.0 12.5 The News-Courier, Athens...........................................0.0 0.0 0.0 0.0 0.0 Lake County Record-Bee, Lakeport...............................0.0 0.0 0.0 0.0 0.0 The Birmingham News................................................0.7 16.7 0.7 0.0 18.1 The Lompoc Record..................................................20.0 0.0 0.0 0.0 20.0 The Decatur Daily........................................................0.0 8.6 0.0 0.0 8.6 Press-Telegram, Long Beach .......................................7.0 4.2 16.9 0.0 28.2 Dothan Eagle..............................................................0.0 4.3 0.0 0.0 4.3 Los Angeles Times......................................................8.5 3.4 6.4 0.2 18.6 Enterprise Ledger........................................................0.0 20.0 0.0 0.0 20.0 Madera Tribune...........................................................0.0 0.0 37.5 0.0 37.5 TimesDaily, Florence...................................................0.0 3.4 0.0 0.0 3.4 Appeal-Democrat, Marysville.......................................4.2 0.0 8.3 0.0 12.5 The Gadsden Times.....................................................0.0 0.0 0.0 0.0 0.0 Merced Sun-Star.........................................................5.0 -

Kennedy Assassination Newspaper Collection : a Finding Aid

University of South Florida Scholar Commons Special Collections and University Archives Finding Aids and Research Guides for Finding Aids: All Items Manuscript and Special Collections 5-1-1994 Kennedy Assassination Newspaper Collection : A Finding Aid Nelson Poynter Memorial Library. Special Collections and University Archives. James Anthony Schnur Hugh W. Cunningham Follow this and additional works at: https://scholarcommons.usf.edu/scua_finding_aid_all Part of the Archival Science Commons Scholar Commons Citation Nelson Poynter Memorial Library. Special Collections and University Archives.; Schnur, James Anthony; and Cunningham, Hugh W., "Kennedy Assassination Newspaper Collection : A Finding Aid" (1994). Special Collections and University Archives Finding Aids: All Items. 19. https://scholarcommons.usf.edu/scua_finding_aid_all/19 This Other is brought to you for free and open access by the Finding Aids and Research Guides for Manuscript and Special Collections at Scholar Commons. It has been accepted for inclusion in Special Collections and University Archives Finding Aids: All Items by an authorized administrator of Scholar Commons. For more information, please contact [email protected]. Kennedy Assassination Newspaper Collection A Finding Aid by Jim Schnur May 1994 Special Collections Nelson Poynter Memorial Library University of South Florida St. Petersburg 1. Introduction and Provenance In December 1993, Dr. Hugh W. Cunningham, a former professor of journalism at the University of Florida, donated two distinct newspaper collections to the Special Collections room of the USF St. Petersburg library. The bulk of the newspapers document events following the November 1963 assassination of John F. Kennedy. A second component of the newspapers examine the reaction to Richard M. Nixon's resignation in August 1974. -

Minority Percentages at Participating Newspapers

2012 Minority Percentages at Participating Newspapers American Asian Indian American Black Hispanic Multi-racial Total American Asian The News-Times, El Dorado 0.0 0.0 11.8 0.0 0.0 11.8 Indian American Black Hispanic Multi-racial Total Times Record, Fort Smith 0.0 0.0 0.0 0.0 3.3 3.3 ALABAMA Harrison Daily Times 0.0 0.0 0.0 0.0 0.0 0.0 The Alexander City Outlook 0.0 0.0 0.0 0.0 0.0 0.0 The Daily World, Helena 0.0 0.0 0.0 0.0 0.0 0.0 The Andalusia Star-News 0.0 0.0 0.0 0.0 0.0 0.0 The Sentinel-Record, Hot Springs National Park 0.0 0.0 0.0 0.0 0.0 0.0 The News-Courier, Athens 0.0 0.0 0.0 0.0 0.0 0.0 The Jonesboro Sun 0.0 0.0 0.0 0.0 0.0 0.0 The Birmingham News 0.0 0.0 20.2 0.0 0.0 20.2 Banner-News, Magnolia 0.0 0.0 15.4 0.0 0.0 15.4 The Cullman Times 0.0 0.0 0.0 0.0 0.0 0.0 Malvern Daily Record 0.0 0.0 0.0 0.0 0.0 0.0 The Decatur Daily 0.0 0.0 13.9 11.1 0.0 25.0 Paragould Daily Press 0.0 0.0 0.0 0.0 0.0 0.0 Enterprise Ledger 0.0 0.0 0.0 0.0 0.0 0.0 Pine Bluff Commercial 0.0 0.0 25.0 0.0 0.0 25.0 TimesDaily, Florence 0.0 0.0 4.8 0.0 0.0 4.8 The Daily Citizen, Searcy 0.0 0.0 0.0 0.0 0.0 0.0 Fort Payne Times-Journal 0.0 0.0 0.0 0.0 0.0 0.0 Stuttgart Daily Leader 0.0 0.0 0.0 0.0 0.0 0.0 Valley Times-News, Lanett 0.0 0.0 0.0 0.0 0.0 0.0 Evening Times, West Memphis 0.0 0.0 0.0 0.0 0.0 0.0 Press-Register, Mobile 0.0 0.0 8.7 0.0 1.4 10.1 CALIFORNIA Montgomery Advertiser 0.0 0.0 17.5 0.0 0.0 17.5 The Bakersfield Californian 0.0 2.4 2.4 16.7 0.0 21.4 The Selma Times-Journal 0.0 0.0 50.0 0.0 0.0 50.0 Desert Dispatch, Barstow 0.0 0.0 0.0 0.0 0.0 0.0 -

Infographic Placements

MEDIA OUTLET NAME CITY STATE READERSHIP Your Alaska Link Anchorage AK 8,989 Kodiak Daily Mirror Kodiak AK 6,484 Seward Journal Delta Junction AK 5,001 Delta Wind Delta Junction AK 1,200 Fairbanks Daily News-Miner Fairbanks AK 434,431 Gadsden Times Gadsden AL 71,778 Alex City Outlook Alexander City AL 50,933 Wetumpka Herald Wetumpka AL 37,608 Courier Journal Florence AL 24,563 Arab Tribune Arab AL 13,952 Elba Clipper Elba AL 10,969 Randolph Leader Roanoke AL 6,449 Cutoff News Bessemer AL 5,963 Montgomery Independent Montgomery AL 4,632 Tallassee Tribune Alexander City AL 4,500 Southeast Sun Enterprise AL 4,337 Tuskegee News Tuskegee AL 3,294 Moulton Advertiser Moulton AL 3,073 Opelika Observer Online Opelika AL 3,000 WHEP 1310 Foley AL 613 Times Daily's TN Valley Search Decatur AL 5,700 Times Daily's TN Valley Brides Decatur AL 5,968 Northwest Arkansas Democrat-Gazette Online Fayetteville AR 159,356 Log Cabin Democrat Conway AR 67,156 Courier News Russellville AR 47,028 River Valley Now Russellville AR 15,000 El Dorado News-Times Online El Dorado AR 8,601 ASU Herald State University AR 6,698 Saline Courier Benton AR 5,511 Waldron News Waldron AR 3,158 De Queen Bee De Queen AR 2,204 Newton County Times Jasper AR 1,665 Radio Works Camden AR 1,500 Madison County Record Huntsville AR 1,221 Bray Online Magnolia AR 1,000 Dewitt Era Enterprise Online Dewitt AR 1,000 Southern Progressive Online Horseshoe Bend AR 300 Harrison Daily Times Harrison AR 53,294 Ashley County Ledger Hamburg AR 8,974 Ashley News Observer Crossett AR 1,001 The Seward Journal -

BMJ in the News Is a Weekly Digest of BMJ Stories, Plus Any Other News

BMJ in the News is a weekly digest of BMJ stories, plus any other news about the company that has appeared in the national and a selection of English-speaking international media. This week’s (8-14 May) highlights: ● A study in The BMJ reporting heightened risk of heart attacks with common painkillers generated global news headlines, including BBC, CNN and Voice of America ● A rapid recommendations article in The BMJ, advising against surgery for most patients with knee arthritis also made global headlines, including CBS and National Public Radio (NPR) in the US ● A warning by doctors in BMJ Case Reports of parasites in raw and undercooked fish generated global headlines, including BBC, Newsweek, CNN and Hindustan Times ● Dr Krishna Chinthapalli was interviewed on Channel 4 News, Sky News, and BBC about this weekend’s cyberattack after warning in The BMJ that hospitals must be better prepared The BMJ Awards Birch's life-saver wins a top award [print only] - Leicester Mercury, 10/05/2017 The BMJ Analysis: Medicalising unhappiness: new classification of depression risks more patients being put on drug treatment from which they will not benefit Fluctuating emotions are part of sport, they must not cloud mental health debate - The Times + The Times Scotland [The Game] 08/05/2017 Trump, the doctor and the vaccine scandal [mentions The BMJ’s articles accusing Andrew Wakefield of fraud] - Channel 4 Dispatches 08/05/2017 Why on earth are so many broken bones not spotted in casualty? - Daily Mail -

Newspaper Distribution List

Newspaper Distribution List The following is a list of the key newspaper distribution points covering our Integrated Media Pro and Mass Media Visibility distribution package. Abbeville Herald Little Elm Journal Abbeville Meridional Little Falls Evening Times Aberdeen Times Littleton Courier Abilene Reflector Chronicle Littleton Observer Abilene Reporter News Livermore Independent Abingdon Argus-Sentinel Livingston County Daily Press & Argus Abington Mariner Livingston Parish News Ackley World Journal Livonia Observer Action Detroit Llano County Journal Acton Beacon Llano News Ada Herald Lock Haven Express Adair News Locust Weekly Post Adair Progress Lodi News Sentinel Adams County Free Press Logan Banner Adams County Record Logan Daily News Addison County Independent Logan Herald Journal Adelante Valle Logan Herald-Observer Adirondack Daily Enterprise Logan Republican Adrian Daily Telegram London Sentinel Echo Adrian Journal Lone Peak Lookout Advance of Bucks County Lone Tree Reporter Advance Yeoman Long Island Business News Advertiser News Long Island Press African American News and Issues Long Prairie Leader Afton Star Enterprise Longmont Daily Times Call Ahora News Reno Longview News Journal Ahwatukee Foothills News Lonoke Democrat Aiken Standard Loomis News Aim Jefferson Lorain Morning Journal Aim Sussex County Los Alamos Monitor Ajo Copper News Los Altos Town Crier Akron Beacon Journal Los Angeles Business Journal Akron Bugle Los Angeles Downtown News Akron News Reporter Los Angeles Loyolan Page | 1 Al Dia de Dallas Los Angeles Times -

Minority Percentages at Participating News Organizations

Minority Percentages at Participating News Organizations Asian Native Asian Native American Black Hispanic American Total American Black Hispanic American Total ALABAMA Paragould Daily Press 0.0 0.0 0.0 0.0 0.0 The Anniston Star 0.0 7.7 0.0 0.0 7.7 Pine Bluff Commercial 0.0 13.3 0.0 0.0 13.3 The Birmingham News 0.8 18.3 0.0 0.0 19.2 The Courier, Russellville 0.0 0.0 0.0 0.0 0.0 The Decatur Daily 0.0 7.1 3.6 0.0 10.7 Northwest Arkansas Newspapers LLC, Springdale 0.0 1.5 1.5 0.0 3.0 Enterprise Ledger 0.0 0.0 0.0 0.0 0.0 Stuttgart Daily Leader 0.0 0.0 20.0 0.0 20.0 TimesDaily, Florence 0.0 2.9 0.0 0.0 2.9 Evening Times, West Memphis 0.0 25.0 0.0 0.0 25.0 The Gadsden Times 0.0 5.6 0.0 0.0 5.6 CALIFORNIA The Daily Mountain Eagle, Jasper 0.0 0.0 0.0 0.0 0.0 Desert Dispatch, Barstow 14.3 0.0 0.0 0.0 14.3 Valley Times-News, Lanett 0.0 0.0 0.0 0.0 0.0 Center for Investigative Reporting, Berkeley 7.1 14.3 14.3 0.0 35.7 Press-Register, Mobile 0.0 10.5 0.0 0.0 10.5 Ventura County Star, Camarillo 1.6 3.3 16.4 0.0 21.3 Montgomery Advertiser 0.0 19.5 2.4 0.0 22.0 Chico Enterprise-Record 3.6 0.0 0.0 0.0 3.6 The Daily Sentinel, Scottsboro 0.0 0.0 0.0 0.0 0.0 The Daily Triplicate, Crescent City 11.1 0.0 0.0 0.0 11.1 The Tuscaloosa News 5.1 2.6 0.0 0.0 7.7 The Davis Enterprise 7.1 0.0 7.1 0.0 14.3 ALASKA Imperial Valley Press, El Centro 17.6 0.0 41.2 0.0 58.8 Fairbanks Daily News-Miner 0.0 0.0 0.0 0.0 0.0 North County Times, Escondido 1.3 0.0 5.2 0.0 6.5 Peninsula Clarion, Kenai 0.0 10.0 0.0 0.0 10.0 The Fresno Bee 6.4 1.3 16.7 0.0 24.4 The Daily News, Ketchikan -

2008 Annual Report Dow Jones Newspaper Fund, Inc. on the Cover Karl Grubaugh, 2008 National High School Journalism Teacher of the Year; S

2008 Annual Report Dow Jones Newspaper Fund, Inc. On the Cover Karl Grubaugh, 2008 National High School Journalism Teacher of the Year; S. Griffin Singer teaching interns at the University of Texas at Austin; Tony Ortega of The Village Voice with students from the New York University Urban Journalism Workshop. Table of Contents From the President 2 From the Executive Director 3 Programs At-A-Glance 4 2008 Financial Report 5 Programs College Programs Multimedia Internships 6 News Editing Internships 7 Sports Editing Internships 8 Business Reporting Internships 9 High School Programs Summer High School Journalism Workshops 10 High School Newspaper Project 14 Teacher Programs National High School Journalism Teacher of the Year 15 Publications 18 Board of Directors 19 Guidelines 20 The Dow Jones Newspaper Fund is a nonprofit foundation established in 1958 and supported by the Dow Jones Foundation and media companies. Its purpose is to promote careers in print and online journalism. The Dow Jones Newspaper Fund, Inc. P.O. Box 300 Princeton, New Jersey 08543-0300 Phone: (609) 452-2820 FAX: (609) 520-5804 Web: https://www.newspaperfund.org Email: [email protected] © 2009 Copyright Dow Jones Newspaper Fund, Inc. From the President/Richard J. Levine Dealing with Reality “It was the best of times, it was the worst of times.” The famous opening line of Charles Dickens’ “A Tale of Two Cities” strikes me as an apt description of the year 2008 in the newspaper industry, which for the past half-century has been the key partner of the Dow Jones Newspaper Fund in developing young journalists. -

Table 6: Details of Race and Ethnicity in Newspaper

Table 6 Details of race and ethnicity in newspaper circulation areas All daily newspapers, by state and city Source: Report to the Knight Foundation, June 2005, by Bill Dedman and Stephen K. Doig The full report is at http://www.asu.edu/cronkite/asne (The Diversity Index is the newsroom non-white percentage divided by the circulation area's non-white percentage.) (DNR = Did not report) State Newspaper Newsroom Staff non-Non-white Hispanic % Black % in Native Asian % in Other % in Multirace White % in Diversity white % % in in circulation American circulation circulation % in circulation Index circulation circulation area % in area area circulation area (100=parity) area area circulation area area Alabama The Alexander City Outlook N/A DNR 26.8 0.6 25.3 0.3 0.2 0.0 0.5 73.2 Alabama The Andalusia Star-News 175 25.0 14.3 0.8 12.3 0.5 0.2 0.0 0.6 85.7 Alabama The Anniston Star N/A DNR 20.7 1.4 17.6 0.3 0.5 0.1 0.8 79.3 Alabama The News-Courier, Athens 0 0.0 15.7 2.8 11.1 0.5 0.4 0.0 0.9 84.3 Alabama Birmingham Post-Herald 29 11.1 38.5 3.6 33.0 0.2 1.0 0.1 0.7 61.5 Alabama The Birmingham News 56 17.6 31.6 1.8 28.1 0.3 0.8 0.1 0.7 68.4 Alabama The Clanton Advertiser 174 25.0 14.4 2.9 10.4 0.3 0.2 0.0 0.6 85.6 Alabama The Cullman Times N/A DNR 4.5 2.1 0.9 0.4 0.2 0.0 0.9 95.5 Alabama The Decatur Daily 44 8.6 19.7 3.1 13.2 1.6 0.4 0.0 1.4 80.3 Alabama The Dothan Eagle 15 4.0 27.3 1.9 23.1 0.5 0.6 0.1 1.0 72.8 Alabama Enterprise Ledger 68 16.7 24.4 2.7 18.2 0.9 1.0 0.1 1.4 75.6 Alabama TimesDaily, Florence 89 12.1 13.7 2.1 10.2 0.3 0.3 0.0 0.7 -

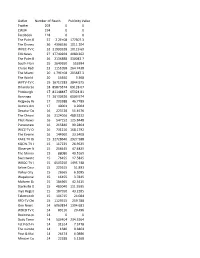

Number of Articles and Outlets.Pdf

Outlet Number of ClipsReach Publicity Value Twitter 203 0 0 CW34 194 0 0 Facebook 118 0 0 The Palm Beach Post57 Online2.2E+08 177307.3 The Disney Cruise Line36 Blog4396536 1011.204 WPEC-TV Online 32 21999328 10119.69 EIN News 27 17740269 4080.262 The Palm Beach Post26 2136888 330043.7 South Florida Sun Sentinel25 2649650 553994 Cruise Radio 23 1151058 264.7438 The Miami Herald Online20 1.79E+08 205687.3 The World News 20 14640 3.368 WPTV-TV Online 19 16717283 3844.975 Orlando Sentinel Online18 85873374 69128.07 Pittsburgh Post-Gazette17 81148837 Online 65324.81 Benzinga 17 26130326 6009.974 Ridgway Record 17 203388 46.7789 Antlers American Online17 40001 9.2004 Decatur Daily Democrat16 Online223728 51.4576 The Chronicle-Journal16 Online2124016 488.5232 Pilot-News Online 16 547152 125.8448 Punxsutawney Spirit16 215840 99.2864 WICZ-TV ONLINE 16 731216 168.1792 The Evening Leader 16Online144960 33.3408 KAKE TV Online 15 12728640 2927.588 KQCW-TV Online 15 117225 26.9625 Observer News Enterprise15 206445 - Online 47.4825 The Morning News 15 88080 40.5165 Sweetwater Reporter15 - Online76455 17.5845 WBOC-TV Online 15 6503250 1495.748 Saline Courier Online15 225615 51.891 Valley City Times-Record15 Online26565 6.1095 Wapakoneta Daily News15 Online16455 3.7845 Malvern Daily Record15 184965 42.5415 Starkville Daily News15 Online485040 111.5595 Inyo Register - Online15 187950 43.2285 Telemundo Lubbock15 104715 24.084 RFD-TV Online 15 1129515 259.788 One News Page 14 6063834 1394.681 WBCB TV Online 14 89110 20.496 Business.poteaudailynews14 0 0 Daily -

9 Average Units(1) Newspaper Primary Website Location Daily (2

Average Units (1) Newspaper Primary Website Location Daily (2) Sunday Magic Valley Group The Times-News magicvalley.com Twin Falls, ID 14,455 12,797 Elko Daily Free Press elkodaily.com Elko, NV 3,218 — Globe Gazette globegazette.com Mason City, IA 9,668 11,995 Santa Maria Times (3) santamariatimes.com Santa Maria, CA 7,784 11,971 The Daily News tdn.com Longview, WA 13,498 11,194 Napa Valley Register (3) napavalleyregister.com Napa, CA 8,519 8,881 Arizona Daily Sun (3) azdailysun.com Flagstaff, AZ 6,411 (6) 7,687 The Citizen auburnpub.com Auburn, NY 5,620 7,148 The Times and Democrat thetandd.com Orangeburg, SC 6,460 6,995 The Sentinel cumberlink.com Carlisle, PA 6,780 (6) — The World (3) theworldlink.com Coos Bay, OR 4,473 — The Sentinel (3) hanfordsentinel.com Hanford, CA 4,575 — The Ledger Independent maysville-online.com Maysville, KY 3,773 — Daily Journal (3) dailyjournalonline.com Park Hills, MO 3,654 (6) — 787,655 1,129,677 (1) Source: AAM: September 2017 Quarterly Executive Summary Data Report, unless otherwise noted. (2) Not all newspapers are published Monday through Saturday (3) Owned by Pulitzer, Inc. (4) Owned by MNI. (5) Owned by Star Publishing and published through TNI. (6) Source: Company statistics. NEWSPRINT The raw material of newspapers, and our other print publications, is newsprint. We purchase newsprint from U.S. and Canadian producers. We believe we will continue to receive a supply of newsprint adequate for our needs and consider our relationships with newsprint producers to be good.