Metro Pacific Tollways Corporation and Subsidiaries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vol 14 No 10

www.punto.com.ph FOR COVID VAX P 10.00 Central V 14 P Gapan earmarks N 10 unto! M - S+ J, 4 - 9, 2021 PANANAW NG MALAYANG PILIPINO! Luzon initial P150-M B, A(%*); M. G GAPAN CITY - The city government has allo- cated an initial fund of P150 million for the procurement of vac- cine against the coro- navirus disease, Mayor Emerson Pascual said Thursday. Pascual said the funding for the vaccine was approved by the sangguniang panlung- sod on Wednesday. “Kung kakakapusin pa, magdadagdag pa po kami,” he added. Pascual In a video address, Pascual said the an- kasakit o mamamatay ti-Covid vaccination dahil sa Covid-19,” the program intends to mayor said. benefi t every resi- There was no im- dent of this city. mediate information “Bakit napagkaisah- as to the schedule of an po namin yan? Dahil procurement but Vice The Subic Freeport Expressway capacity expansion. C " ayaw po namin na may Mayor Dodong Bautis- taga-Gapan na magka- P*/& 6 3#&*5& MOTORISTS REJOICE AC allots P25-M 3 NLEX projects Seeks P50-M counterpart from DOH ANGELES CITY – idents of Angeles City With frontline medical especially those mem- near completion workers and those be- bers of vulnerable sec- longing to marginal- tor will receive free vac- ized sectors as priority, cine against the virus,” ITY OF SAN FERNANDO – Three major road projects – all aimed Mayor Carmelo “Pogi” Lazatin said in his let- Lazatin, Jr. has allotted ter to Health Secretary at improving the mobility and safety of motorists – are set to be P25 million for the pro- Francisco Duque. -

PS Rbs CPU Directory for Website February 2021.Xlsx

METRO MANILA PAYOUT CHANNELS PROVINCE CITY/MUNICIPALITY BRANCH NAME ADDRESS METRO MANILA MANILA H VILLARICA - BLUMENTRITT 1 1714 BLUMENTRITT ST. STA CRUZ MANILA METRO MANILA MANILA H VILLARICA - BLUMENTRITT 2 1601 COR. BLUEMNTRITT ST & RIZAL AVE BRGY 363,ZONE 037 STA CRUZ MANILA METRO MANILA MANILA H VILLARICA - BUSTILLOS 443 FIGUERAS ST. SAMPALOC MANILA METRO MANILA MANILA H VILLARICA - PACO 1 # 1122 PEDRO GIL ST., PACO MANILA METRO MANILA MANILA H VILLARICA - PADRE RADA 656 PADRE RADA ST TONDO MANILA METRO MANILA MANILA H VILLARICA - PRITIL 1 1835 NICOLAS ZAMORA ST TONDO BGY 86 MANILA METRO MANILA MANILA H VILLARICA - QUINTA 200 VILLALOBOS ST COR C PALANCA ST QUIAPO MANILA METRO MANILA MANILA H VILLARICA - SAMPALOC 1 1706 J. FAJARDO ST. SAMPALOC MANILA METRO MANILA MANILA HL VILLARICA - D JOSE 1574 D.JOSE ST STA. CRUZ NORTH,MANILA METRO MANILA MANILA HL VILLARICA - ESPAÑA 1664 ESPANA BLVD COR MA CRISTINA ST SAMPALOC EAST,MANILA METRO MANILA MANILA HL VILLARICA - LAON LAAN 1285 E. LAON LAAN ST., COR. MACEDA ST., SAMPALOC MANILA METRO MANILA MANILA HL VILLARICA - MACEDA 1758 RETIRO CORNER MACEDA ST. SAMPALOC MANILA METRO MANILA MANILA HL VILLARICA - PANDACAN 1922 J ZAMORA ST BRGY 851 ZONE 93 PANDACAN MANILA METRO MANILA MANILA HL VILLARICA - STA. ANA 1 3421-25 NEW PANADEROS ST. STA.ANA MANILA METRO MANILA MANILA HRV VILLARICA - ERMITA MANILA UYGUANGCO RD., BO. STO. NIÑO BRGY 187 TALA CALOOCAN METRO MANILA MANILA HRV VILLARICA - GAGALANGIN 2710 JUAN LUNA ST GAGALANGIN BRGY 185 ZONE 016 TONDO MANILA METRO MANILA MANILA HRV VILLARICA - HERMOSA 1157 B. HERMOSA ST. MANUGUIT TONDO MANILA METRO MANILA MANILA HRV VILLARICA - ILAYA MANILA #33 ARANETA ST. -

Assessment of Impediments to Urban-Rural Connectivity in Cdi Cities

ASSESSMENT OF IMPEDIMENTS TO URBAN-RURAL CONNECTIVITY IN CDI CITIES Strengthening Urban Resilience for Growth with Equity (SURGE) Project CONTRACT NO. AID-492-H-15-00001 JANUARY 27, 2017 This report is made possible by the support of the American people through the United States Agency for International Development (USAID). The contents of this report are the sole responsibility of the International City/County Management Association (ICMA) and do not necessarily reflect the view of USAID or the United States Agency for International Development USAID Strengthening Urban Resilience for Growth with Equity (SURGE) Project Page i Pre-Feasibility Study for the Upgrading of the Tagbilaran City Slaughterhouse ASSESSMENT OF IMPEDIMENTS TO URBAN-RURAL CONNECTIVITY IN CDI CITIES Strengthening Urban Resilience for Growth with Equity (SURGE) Project CONTRACT NO. AID-492-H-15-00001 Program Title: USAID/SURGE Sponsoring USAID Office: USAID/Philippines Contract Number: AID-492-H-15-00001 Contractor: International City/County Management Association (ICMA) Date of Publication: January 27, 2017 USAID Strengthening Urban Resilience for Growth with Equity (SURGE) Project Page ii Assessment of Impediments to Urban-Rural Connectivity in CDI Cities Contents I. Executive Summary 1 II. Introduction 7 II. Methodology 9 A. Research Methods 9 B. Diagnostic Tool to Assess Urban-Rural Connectivity 9 III. City Assessments and Recommendations 14 A. Batangas City 14 B. Puerto Princesa City 26 C. Iloilo City 40 D. Tagbilaran City 50 E. Cagayan de Oro City 66 F. Zamboanga City 79 Tables Table 1. Schedule of Assessments Conducted in CDI Cities 9 Table 2. Cargo Throughput at the Batangas Seaport, in metric tons (2015 data) 15 Table 3. -

Transportation History of the Philippines

Transportation history of the Philippines This article describes the various forms of transportation in the Philippines. Despite the physical barriers that can hamper overall transport development in the country, the Philippines has found ways to create and integrate an extensive transportation system that connects the over 7,000 islands that surround the archipelago, and it has shown that through the Filipinos' ingenuity and creativity, they have created several transport forms that are unique to the country. Contents • 1 Land transportation o 1.1 Road System 1.1.1 Main highways 1.1.2 Expressways o 1.2 Mass Transit 1.2.1 Bus Companies 1.2.2 Within Metro Manila 1.2.3 Provincial 1.2.4 Jeepney 1.2.5 Railways 1.2.6 Other Forms of Mass Transit • 2 Water transportation o 2.1 Ports and harbors o 2.2 River ferries o 2.3 Shipping companies • 3 Air transportation o 3.1 International gateways o 3.2 Local airlines • 4 History o 4.1 1940s 4.1.1 Vehicles 4.1.2 Railways 4.1.3 Roads • 5 See also • 6 References • 7 External links Land transportation Road System The Philippines has 199,950 kilometers (124,249 miles) of roads, of which 39,590 kilometers (24,601 miles) are paved. As of 2004, the total length of the non-toll road network was reported to be 202,860 km, with the following breakdown according to type: • National roads - 15% • Provincial roads - 13% • City and municipal roads - 12% • Barangay (barrio) roads - 60% Road classification is based primarily on administrative responsibilities (with the exception of barangays), i.e., which level of government built and funded the roads. -

Hub Identification of the Metro Manila Road Network Using Pagerank Paper Identification Number: AYRF15-015 Jacob CHAN1, Kardi TEKNOMO2

“Transportation for A Better Life: Harnessing Finance for Safety and Equity in AEC August 21, 2015, Bangkok, Thailand Hub Identification of the Metro Manila Road Network Using PageRank Paper Identification Number: AYRF15-015 Jacob CHAN1, Kardi TEKNOMO2 1Department of Information Systems and Computer Science, School of Science and Engineering Ateneo de Manila University, Loyola Heights, Quezon City, Philippines 1108 Telephone +632-426-6001, Fax. +632-4261214 E-mail: [email protected] 2Department of Information Systems and Computer Science, School of Science and Engineering Ateneo de Manila University, Loyola Heights, Quezon City, Philippines 1108 Telephone +632-426-6001, Fax. +632-4261214 E-mail: [email protected] Abstract We attempt to identify the different node hubs of a road network using PageRank for preparation for possible random terrorist attacks. The robustness of a road network against such attack is crucial to be studied because it may cripple its connectivity by simply shutting down these hubs. We show the important hubs in a road network based on network structure and propose a model for robustness analysis. By identifying important hubs in a road network, possible preparation schemes may be done earlier to mitigate random terrorist attacks, including defense reinforcement and transportation security. A case study of the Metro Manila road network is also presented. The case study shows that the most important hubs in the Metro Manila road network are near airports, piers, major highways and expressways. Keywords: PageRank, Terrorist Attack, Robustness 1. Introduction Table 1 Comparative analysis of different Roads are important access points because methodologies on network robustness indices connects different places like cities, districts, and Author Method Strength Weakness landmarks. -

Results Report 2014

Results Report 2014 Results Report 2014 26th February, 2015 Non Audited Figures 1 Results Report 2014 INDEX 1 Executive Summary 3 1.1 Main figures 3 1.2 Relevant facts 5 2 Consolidated Financial Statements 8 2.1 Income Statement 8 2.1.1 Sales and Backlog 8 2.1.2 Operating Results 10 2.1.3 Financial Results 11 2.1.4 Net Profit Attributable to the Parent Company 12 2.2 Consolidated Balance Sheet 13 2.2.1 Non-Current Assets 13 2.2.2 Assets held for sale 14 2.2.3 Working Capital 15 2.2.4 Net Debt 15 2.2.5 Net Worth 16 2.3 Net Cash Flows 17 2.3.1 Operating Activities 17 2.3.2 Investments 18 2.3.3 Other Cash Flows 18 3 Areas of Activity Evolution 19 3.1 Construction 19 3.2 Industrial Services 22 3.3 Environment 24 4 Relevant facts after the end of the period 26 5 Description of the main risks and opportunities 26 6 Corporate Social Responsibility 28 6.1 Ethics 28 6.2 Efficiency 28 6.3 Employees 30 7 Information on affiliates 30 8 Annexes 31 8.1 Main figures per area of activity 31 8.2 Financial Accounts per area of Activity 32 8.2.1 Income Statement 32 8.2.2 Balance Sheet 33 8.3 Infrastructure Concessions 34 8.4 Share data 35 8.5 Exchange rate effect 36 8.6 Main Awards of the Period 37 8.6.1 Construction 37 8.6.2 Industrial Services 40 8.6.3 Environment 41 Non Audited Figures 2 Results Report 2014 1 Executive Summary 1.1 Main figures Grupo ACS Key operating & financial figures Million Euro 2013 2014 Var. -

Comprehensive Land Use Plan 2016 - 2025

COMPREHENSIVE LAND USE PLAN 2016 - 2025 PART 3: SECTORAL PROFILE 3.1. INFRASTRUCTURE, FACILITIES AND UTILITIES 3.1.1. Flood Control Facilities 3.1.1.1. “Bombastik” Pumping Stations Being a narrow strip of land with a relatively flat terrain and with an aggregate shoreline of 12.5 kilometers that is affected by tidal fluctuations, flooding is a common problem in Navotas City. This is aggravated by pollution and siltation of the waterways, encroachment of waterways and drainage right-of-ways by legitimate and informal settlers, as well as improper waste disposal. The perennial city flooding inevitably became a part of everyday living. During a high tide with 1.2 meter elevation, some parts of Navotas experience flooding, especially the low-lying areas along the coast and riverways. As a mitigating measure, the city government - thru the Local Disaster Risk Reduction and Management Office - disseminates information about the heights of tides for a specific month. This results in an increased awareness among the residents on the time and date of occurrence of high tide. During rainy days, flooding reach higher levels. The residents have already adapted to this situation. Those who are well-off are able to install their own preventive measures, such as upgrading their floorings to a higher elevation. During the term of the then Mayor and now Congressman, Tobias M. Tiangco, he conceptualized a project that aims to end the perennial flooding in Navotas. Since Navotas is surrounded by water, he believed that enclosing the city to prevent the entry of water during high tide would solve the floods. -

Malolos-Clark Railway Project – Tranche 1 Volume I

Environmental Monitoring Report Semi-annual Environmental Monitoring Report No. 1 March 2020 PHI: Malolos-Clark Railway Project – Tranche 1 Volume I September 2019 – March 2020 Prepared by the Project Management Office (PMO) of the Department of Transportation (DOTr) for the Government of the Republic of the Philippines and the Asian Development Bank. CURRENCY EQUIVALENTS (as of 30 March 2020) Currency unit – Philippine Peso (PHP) PHP1.00 = $0.02 $1.00 = PHP50.96 ABBREVIATIONS ADB – Asian Development Bank BMB – Biodiversity Management Bureau Brgy – Barangay CCA – Climate Change Adaptation CCC – Climate Change Commission CDC – Clark Development Corporation CEMP – Contractor’s Environmental Management Plan CENRO – City/Community Environment and Natural Resources Office CIA – Clark International Airport CIAC – Clark International Airport Corporation CLLEx – Central Luzon Link Expressway CLUP – Comprehensive Land Use Plan CMR – Compliance Monitoring Report CMVR – Compliance Monitoring and Validation Report CNO – Certificate of No Objection CPDO – City Planning and Development Office DAO – DENR Administrative Order DD / DED – Detailed Design Stage / Detailed Engineering Design Stage DENR – Department of Environment and Natural Resources DepEd – Department of Education DIA – Direct Impact Area DILG – Department of Interior and Local Government DOH – Department of Health DOST – Department of Science and Technology DOTr – Department of Transportation DPWH – Department of Public Works and Highways DSWD – Department of Social Welfare and Development -

No. Area Municipality Address

NO. AREA MUNICIPALITY ADDRESS 1 MNM BULACAN KM 23 NLEX, MARILAO BULACAN 2 MNM BULACAN NORTH LUZON TOLLWAYS, SOUTHBOUND BOCAUE, BULACAN 3 MNM BULACAN BGY MALAMIG BUSTOS, BULACAN 4 MNM BULACAN 48 NORTHERN HILLS, MALHACAN, MEYCAUAYAN, BULACAN 5 MNM BULACAN KM 42 NLEX, NORTHBOUND LANE, PLARID BULACAN 6 MNM BULACAN MAHARLIKA HIGHWAY, GALA-MAASIM, SAN BULACAN 7 MNM BULACAN PUROK 1 MABINI STREET, SANTISSIMA T MALOLOS, BULACAN 8 MNM BULACAN KM 37 BGY CUTCUT, BULIHAN PLARIDEL, BULACAN 9 MNM BULACAN MAHARLIKA HIGHWAY BRGY. SAMPALOC SAN RAFAEL, BULACAN 10 MNM BULACAN VILLARAMA ST., POBLACION NORZAGARAY, BULACAN 11 MNM BULACAN BRGY. TAAL DRT HIGHWAY PULILAN BULACAN 12 MNM BULACAN GROTTO, SAN JOSE DEL MONTE BULACAN 13 MNM BULACAN 595 McARTHUR HIGHWAY, BO. TUKTUKAN GUIGUINTO, BULACAN 14 MNM BULACAN BO. TURO, BOCAUE BULACAN 15 MNM BULACAN DIVERSION ROAD (BY PASS), STA. CLAR STA. MARIA, BULACAN 16 MNM BULACAN DULONG BAYAN, STA. MARIA BULACAN 17 MNM BULACAN 101 MCARTHUR HIGHWAY BULACAN 18 NCR CALOOCAN C-3 ROAD, DAGAT-DAGATAN CALOOCAN CITY 19 NCR CALOOCAN B. SERRANO ST. COR 11TH AVE CALOOCAN CITY 20 NCR CALOOCAN GEN. LUIS CORNER P. DELA CRUZ STS. KALOOKAN CITY 21 NCR CALOOCAN ZABARTE ROAD, BRGY. CAMARIN, NORTH CALOOCAN, KALOOKAN CITY 22 NCR CALOOCAN TULLAHAN ROAD, ST. QUITERIA CALOOCAN CITY 23 NCR CALOOCAN 486 EDSA CORNER A DE JESUS ST., CALOOCAN 24 NCR LAS PINAS LOT 2A DAANG HARI CORNER DAANG REYN LAS PINAS 25 NCR LAS PINAS C5 EXT. COR. S. MARQUEZ ST. MANUYO TALON, LAS PINAS 26 NCR LAS PINAS 269 REAL ST. PAMPLONA LAS PINAS 27 NCR LAS PINAS C5 EXT. -

(CSHP) DOLE-Regional Office No. 3 April 2019

REGIONAL REPORT ON THE APPROVED/CONCURRED CONSTRUCTION SAFETY & HEALTH PROGRAM (CSHP) DOLE-Regional Office No. 3 April 2019 Date No. Company Name and Address Project Name Approved Sampaguita St., Doña KARPA BUILDERS AND 1 Francisca, Balanga City, Construction of Streetlights Barangay Bantan Munti, Pilar, Bataan 3/26/2019 TRADING Bataan BPQ CONSTRUCTION AND Doña Francisca, Balanga 2 Rehabilitation of Seawall Barangay Tortugas, Balanga City, Bataan 3/26/2019 TRADING City, Bataan Repair / Rehabilitation of Fourteen (14) Classroom School Building POLYMER-VIC Doña Francisca, Balanga 3 at A.G. Llamas Elementary School, Barangay Poblacion, Mariveles, 3/26/2019 CONSTRUCTION City, Bataan Bataan POLYMER-VIC Doña Francisca, Balanga Construction of Slope Protection Talimundoc-Doña Road Barangay 4 3/26/2019 CONSTRUCTION City, Bataan Talimundoc, Orani, Bataan PACKAGE 2 a.) Design & Build for the Construction of Two (2) Storey Four (4) Classroom School Bldg Sto. Niño Elem. School, Dinalupihan, Bataan; b.) Design & Building for the Construction of Two (2) Units Two (2) Storey Four (4) Classroom School Bldg San POLYMER-VIC Doña Francisca, Balanga 5 Ramon Elem. School, Dinalupihan, Bataan; c.) Design & Build for 3/26/2019 CONSTRUCTION City, Bataan the Construction of Two (2) Storey Four (4) Classroom School Building Colo Elem. School, Dinalupihan, Bataan; d.) Design & Build for the Construction of Two (2) Storey Four (4) Classroom School Bldg Pinulot Elem. School, Dinalupihan, Bataan Sunflower St., Doña E.R. VENZON Rehabilitation of Drainage System at Barangay Camacho, City of 6 Francisca, Balanga City, 3/26/2019 CONSTRUCTION Balanga, Bataan Bataan Construction of Concrete Revetment at Barangay Munting 7 RCS CONSTRUCTION #461 Yakal St., Panilao, Pilar 3/26/2019 Batangas, City of Balanga, Bataan Construction of Multi-Purpose Building at Barangay Pto. -

Project Implementation Plan

CHAPTER 5 PROJECT IMPLEMENTATION PLAN The Supplementary Survey on North South Commuter Rail Project (Phase II-A) in the Republic of the Philippines FINAL REPORT CHAPTER 5 PROJECT IMPLEMENTATION PLANNING 5.1 Examination of Preliminary Construction Plan The construction of NSCR will require careful planning and organization, given the magnitude of the works, time constraints and the location of the works on busy national and arterial roads within Metropolitan Manila and Bulacan Province. 5.1.1 Temporary Works 1) Temporary Access to Site It is necessary to apply countermeasures flooding during heavy rain season because of the low ground level between Malolos and Caloocan. There is no problem with an access road to the site along the main road in this area. However, it is necessary to consider to construct temporary access to site far from main roads. In swampy areas between Malolos and San Fernando along the PNR Route, it is necessary to construct a temporary steel stage for machinery or materials transportation during construction. It is necessary to install sheet piles to avoid an intrusion of ground water during construction of the substructure. 2) Sufficient Space for the Works There are some narrow ROW sections between Malolos and Caloocan along the PNR Route. During construction of elevated structures, it is necessary to have more than 15m width for access road to secure access of many trucks, truck mixers and other construction equipment transportation to the site. After construction, the temporary access shall be maintained more than 15m width as a service road for maintenance or emergency evacuation. Source: JICA Study Team Figure 5.1.1 Necessary ROW for Elevated Structures 5-1 5.1.2 Viaduct 5.1.2.1 Foundations Viaduct foundations comprise of conventional bored piles and pile caps. -

2011 Financial Statements

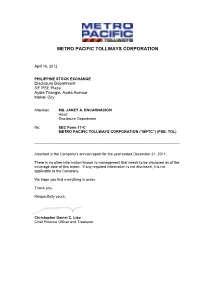

METRO PACIFIC TOLLWAYS CORPORATION April 16, 2012 PHILIPPINE STOCK EXCHANGE Disclosure Department 3/F PSE Plaza Ayala Triangle, Ayala Avenue Makati City Attention: MS. JANET A. ENCARNACION Head Disclosure Department Re: SEC Form 17-C METRO PACIFIC TOLLWAYS CORPORATION (“MPTC”) (PSE: TOL) Attached is the Company’s annual report for the year ended December 31, 2011. There is no other information known to management that needs to be disclosed as of the coverage date of this report. If any required information is not disclosed, it is not applicable to the Company. We hope you find everything in order. Thank you. Respectfully yours, Christopher Daniel C. Lizo Chief Finance Officer and Treasurer 4 0 5 9 0 SEC Registration Number M E T R O P A C I F I C T O L L W A Y S C O R P O R A T I O N ( F o r m e r l y F i r s t P h i l i p p i n e I n f r a s t r u c t u r e , I n c . ) A N D S U B S I D I A R I E S (Company’s Full Name) 1 0 t h F l o o r , M G O B u i l d i n g , L e g a s p i c o r . D e l a R o s a S t s . , M a k a t i C i t y (Business Address: No.