Getting Things Done

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Quarterly Investment Update Antares High Growth Shares Fund – June 2021

Quarterly Investment Update Antares High Growth Shares Fund – June 2021 For adviser use only Highlights for the quarter Performance: The Fund returned 9.6% (net of fees) for the June quarter, outperforming its benchmark by 1.3%. Contributors to performance: Positive contributors – Aristocrat Leisure, Telix Pharmaceuticals, Megaport, Boral, Woodside (not owned); Negative contributors – Incitec Pivot, Qantas, ANZ, Resmed (not owned) and Altium (not owned). Stock activity: Buys/additions – Ansell, Downer and TPG Telecom ; Sells/reductions – BlueScope Steel, Boral, Endeavour Group and Worley Fund snapshot Inception date 7 December 1999 Benchmark S&P/ASX 200 Total Return Index To outperform the benchmark (after fees) over rolling Investment objective 5-year periods Investment returns as at 30 June 20211 Period 3 months 1 year 3 years pa 5 years pa 10 years pa Since inception pa Net return2 % 9.6 39.9 9.2 12.6 10.0 11.0 Gross return3 % 9.9 41.9 10.5 13.9 11.2 12.5 Benchmark return % 8.3 27.8 9.6 11.2 9.3 8.5 Net excess return % 1.3 12.1 -0.4 1.4 0.7 2.5 Gross excess return % 1.6 14.1 0.9 2.7 1.9 4.0 1 Past performance is not a reliable indicator of future performance. Returns are not guaranteed and actual returns may vary from any target returns described in this document. 2 Investment returns are based on exit prices, and are net of management fees and assume reinvestment of all distributions. Contributors to performance Pleasingly the Fund enjoyed another strong quarter, returning 9.6% (net of fees) vs the benchmark return of 8.3%. -

Business Leadership: the Catalyst for Accelerating Change

BUSINESS LEADERSHIP: THE CATALYST FOR ACCELERATING CHANGE Follow us on twitter @30pctAustralia OUR OBJECTIVE is to achieve 30% of ASX 200 seats held by women by end 2018. Gender balance on boards does achieve better outcomes. GREATER DIVERSITY ON BOARDS IS VITAL TO THE GOOD GOVERNANCE OF AUSTRALIAN BUSINESSES. FROM THE PERSPECTIVE OF PERFORMANCE AS WELL AS EQUITY THE CASE IS CLEAR. AUSTRALIA HAS MORE THAN ENOUGH CAPABLE WOMEN TO EXCEED THE 30% TARGET. IF YOUR BOARD IS NOT INVESTING IN THE CAPABILITY THAT DIVERSITY BRINGS, IT’S NOW A MARKED DEPARTURE FROM THE WHAT THE INVESTOR AND BROADER COMMUNITY EXPECT. Angus Armour FAICD, Managing Director & Chief Executive Officer, Australian Institute of Company Directors BY BRINGING TOGETHER INFLUENTIAL COMPANY CHAIRS, DIRECTORS, INVESTORS, HEAD HUNTERS AND CEOs, WE WANT TO DRIVE A BUSINESS-LED APPROACH TO INCREASING GENDER BALANCE THAT CHANGES THE WAY “COMPANIES APPROACH DIVERSITY ISSUES. Patricia Cross, Australian Chair 30% Club WHO WE ARE LEADERS LEADING BY EXAMPLE We are a group of chairs, directors and business leaders taking action to increase gender diversity on Australian boards. The Australian chapter launched in May 2015 with a goal of achieving 30% women on ASX 200 boards by the end of 2018. AUSTRALIAN 30% CLUB MEMBERS Andrew Forrest Fortescue Metals Douglas McTaggart Spark Group Ltd Infrastructure Trust Samuel Weiss Altium Ltd Kenneth MacKenzie BHP Billiton Ltd John Mulcahy Mirvac Ltd Stephen Johns Brambles Ltd Mark Johnson G8 Education Ltd John Shine CSL Ltd Paul Brasher Incitec Pivot -

Tea Tree Gully Gem & Mineral Club News

Tea Tree Gully Gem & Mineral Club Inc. (TTGGMC) November Clubrooms: Old Tea Tree Gully School, Dowding Terrace, Tea Tree Gully, SA 5091. Postal Address: Po Box 40, St Agnes, SA 5097. Edition President: Ian Everard. 0417 859 443 Email: [email protected] 2019 Secretary: Claudia Gill. 0419 841 473 Email: [email protected] Treasurer: Russell Fischer. Email: [email protected] Membership Officer: Augie Gray: 0433 571 887 Email: [email protected] Newsletter/Web Site: Mel Jones. 0428 395 179 Email: [email protected] Web Address: https://teatreegullygemandmineralclub.com "Rockzette" Tea Tree Gully Gem & Mineral Club News President’s Report General Interest Club Activities / Fees Pages 3 to 5: Meetings Hi All, Augie’s November Agate and Mineral Selections… Club meetings are held on the 1st Thursday of each As you all know this month’s meeting is AGM month except January. time. I would like to see you all there. Committee meetings start at 7 pm. General meetings - arrive at 7.30 pm for Get well Mal Knott. 8 pm start. Please check all notices on pages 1, 2 and 20. Library Librarian - Augie Gray Cheers, Pages 6 to 8: Augie’s November Mineral Matters – Fordite… There is a 2-month limit on borrowed items. Ian. When borrowing from the lending library, fill out the card at the back of the item, then place the card in Diary Dates / Notices the box on the shelf. When returning items, fill in the return date on the card, then place the card at the back of the item. See Notices on Page 2 Pages 9 & 10: Tuesday Faceting/Cabbing Ian’s 2019 Agate Creek Finds Part 2… Tuesdays - 10 am to 2 pm. -

Dow Jones Sustainability Australia Index

Effective as of 23 November 2020 Dow Jones Sustainability Australia Index Company Country Industry Group Comment Australia and New Zealand Banking Group Limited Australia Banks National Australia Bank Limited Australia Banks Westpac Banking Corporation Australia Banks CIMIC Group Limited Australia Capital Goods Brambles Limited Australia Commercial & Professional Services Downer EDI Limited Australia Commercial & Professional Services Tabcorp Holdings Limited Australia Consumer Services The Star Entertainment Group Limited Australia Consumer Services Janus Henderson Group plc United Kingdom Diversified Financials Oil Search Limited Papua New Guinea Energy Woodside Petroleum Ltd Australia Energy Coles Group Limited Australia Food & Staples Retailing Fisher & Paykel Healthcare Corporation Limited New Zealand Health Care Equipment & Services Asaleo Care Limited Australia Household & Personal Products Insurance Australia Group Limited Australia Insurance QBE Insurance Group Limited Australia Insurance Suncorp Group Limited Australia Insurance Addition Amcor plc Switzerland Materials Addition BHP Group Australia Materials Boral Limited Australia Materials Evolution Mining Limited Australia Materials Fletcher Building Limited New Zealand Materials Fortescue Metals Group Limited Australia Materials IGO Limited Australia Materials Iluka Resources Limited Australia Materials Incitec Pivot Limited Australia Materials Newcrest Mining Limited Australia Materials Orocobre Limited Australia Materials Rio Tinto Ltd Australia Materials South32 Limited -

Stoxx® Australia 150 Index

STOXX® AUSTRALIA 150 INDEX Components1 Company Supersector Country Weight (%) Commonwealth Bank of Australia Banks Australia 8.37 CSL Ltd. Health Care Australia 7.46 BHP GROUP LTD. Basic Resources Australia 7.23 National Australia Bank Ltd. Banks Australia 4.37 Westpac Banking Corp. Banks Australia 4.09 Australia & New Zealand Bankin Banks Australia 3.75 Wesfarmers Ltd. Retail Australia 3.30 WOOLWORTHS GROUP Personal Care, Drug & Grocery Australia 2.87 Macquarie Group Ltd. Financial Services Australia 2.84 Rio Tinto Ltd. Basic Resources Australia 2.48 Fortescue Metals Group Ltd. Basic Resources Australia 2.27 Transurban Group Industrial Goods & Services Australia 2.20 Telstra Corp. Ltd. Telecommunications Australia 2.05 Goodman Group Real Estate Australia 1.77 AFTERPAY Industrial Goods & Services Australia 1.54 Coles Group Personal Care, Drug & Grocery Australia 1.39 Woodside Petroleum Ltd. Energy Australia 1.28 Newcrest Mining Ltd. Basic Resources Australia 1.27 Aristocrat Leisure Ltd. Travel & Leisure Australia 1.11 XERO Technology Australia 1.00 SYDNEY AIRPORT Industrial Goods & Services Australia 0.93 Brambles Ltd. Industrial Goods & Services Australia 0.91 Sonic Healthcare Ltd. Health Care Australia 0.90 ASX Ltd. Financial Services Australia 0.82 SCENTRE GROUP Real Estate Australia 0.80 Cochlear Ltd. Health Care Australia 0.74 QBE Insurance Group Ltd. Insurance Australia 0.73 SUNCORP GROUP LTD. Insurance Australia 0.71 South32 Australia Basic Resources Australia 0.71 Santos Ltd. Energy Australia 0.68 Ramsay Health Care Ltd. Health Care Australia 0.66 Insurance Australia Group Ltd. Insurance Australia 0.65 Mirvac Group Real Estate Australia 0.60 DEXUS Real Estate Australia 0.59 SEEK Ltd. -

Australian Listed Equities: Weekly Share Market Wrap

Australian Listed Equities: Weekly Share Market Wrap Total Shareholder Returns as at 04 December 2020 Price 1 week 1 month 6 months 1 year 2 years 3 years 5 years 10 years 10 years Ticker Stock Name $ % % % % % p.a. % p.a. % p.a. % p.a. ranking A2M The A2 Milk Company 13.48 -3.02 2.04 -24.57 -5.73 13.14 21.69 66.61 - - ABC Adelaide Brighton 3.23 2.22 3.19 -2.46 -0.08 -18.14 -17.52 -1.18 4.55 98 ABP Abacus Property Grp 3.15 -0.63 6.42 21.82 -10.83 4.23 -3.52 6.74 8.37 69 AFI Australian Foundat 7.22 -0.82 8.41 17.95 9.38 13.38 9.55 8.04 7.01 75 AGL AGL Energy Limited 13.52 -1.46 5.54 -20.24 -27.72 -9.15 -12.47 1.87 3.88 102 AIA Auckland Internation 7.32 -0.41 8.77 11.76 -12.65 5.08 9.74 10.98 18.12 22 ALD Ampol Limited 30.77 0.46 21.00 9.73 -8.08 8.66 -1.78 0.93 10.77 56 ALL Aristocrat Leisure 31.84 -3.74 3.67 17.51 -3.91 17.25 14.09 28.04 29.23 7 ALQ ALS Limited 9.52 -2.36 -0.98 31.69 7.40 14.26 14.25 21.73 5.54 90 ALU Altium Limited 35.72 2.09 -5.53 -1.48 2.44 24.33 41.36 50.26 71.58 1 ALX Atlas Arteria 6.48 -1.22 8.91 -2.66 -11.90 3.02 5.85 12.80 18.17 21 AMC Amcor PLC 15.34 -0.84 0.16 3.68 8.49 11.97 3.36 6.80 13.24 39 AMP AMP Limited 1.72 -1.15 3.30 2.84 0.04 -12.32 -25.31 -14.07 -2.03 121 ANN Ansell Limited 35.68 -5.06 -14.07 0.81 26.57 27.11 14.59 12.75 11.78 48 ANZ ANZ Banking Grp Ltd 23.30 0.91 22.54 24.41 -1.20 -1.64 -1.47 2.25 5.11 94 APA APA Group 10.18 -3.69 -6.86 -9.84 -0.47 13.21 7.59 8.16 14.00 36 APE AP Eagers Limited 13.25 -0.53 14.13 81.51 37.33 41.67 21.54 5.80 20.09 20 APT Afterpay Touch 94.50 -0.21 -6.20 81.03 224.97 -

Single Sector Funds Portfolio Holdings

! Mercer Funds Single Sector Funds Portfolio Holdings December 2020 welcome to brighter Mercer Australian Shares Fund Asset Name 4D MEDICAL LTD ECLIPX GROUP LIMITED OOH MEDIA LIMITED A2 MILK COMPANY ELDERS LTD OPTHEA LIMITED ABACUS PROPERTY GROUP ELECTRO OPTIC SYSTEMS HOLDINGS LTD ORICA LTD ACCENT GROUP LTD ELMO SOFTWARE LIMITED ORIGIN ENERGY LTD ADBRI LTD EMECO HOLDINGS LTD OROCOBRE LTD ADORE BEAUTY GROUP LTD EML PAYMENTS LTD ORORA LTD AFTERPAY LTD ESTIA HEALTH LIMITED OZ MINERALS LTD AGL ENERGY LTD EVENT HOSPITALITY AND ENTERTAINMENT PACT GROUP HOLDINGS LTD ALKANE RESOURCES LTD EVOLUTION MINING LTD PARADIGM BIOPHARMACEUTICALS LTD ALS LIMITED FISHER & PAYKEL HEALTHCARE CORP LTD PENDAL GROUP LTD ALTIUM LTD FLETCHER BUILDING LTD PERENTI GLOBAL LTD ALUMINA LTD FLIGHT CENTRE TRAVEL GROUP LTD PERPETUAL LTD AMA GROUP LTD FORTESCUE METALS GROUP LTD PERSEUS MINING LTD AMCOR PLC FREEDOM FOODS GROUP LIMITED PHOSLOCK ENVIRONMENTAL TECHNOLOGIES AMP LTD G8 EDUCATION LTD PILBARA MINERALS LTD AMPOL LTD GALAXY RESOURCES LTD PINNACLE INVESTMENT MANAGEMENT GRP LTD ANSELL LTD GDI PROPERTY GROUP PLATINUM INVESTMENT MANAGEMENT LTD APA GROUP GENWORTH MORTGAGE INSRNC AUSTRALIA LTD POINTSBET HOLDINGS LTD APPEN LIMITED GOLD ROAD RESOURCES LTD POLYNOVO LIMITED ARB CORPORATION GOODMAN GROUP PTY LTD PREMIER INVESTMENTS LTD ARDENT LEISURE GROUP GPT GROUP PRO MEDICUS LTD ARENA REIT GRAINCORP LTD QANTAS AIRWAYS LTD ARISTOCRAT LEISURE LTD GROWTHPOINT PROPERTIES AUSTRALIA LTD QBE INSURANCE GROUP LTD ASALEO CARE LIMITED GUD HOLDINGS LTD QUBE HOLDINGS LIMITED ASX LTD -

View Annual Report

Nufarm Limited Annual Report 2015 ANNUAL REPORT 2015 Building a better Nufarm The company is making changes and improvements that will help Nufarm become a better, more successful business. While we have continued to grow in recent years, we must ensure that we are generating the level of profitability that we need to fund future growth opportunities and reward our shareholders with a suitable return on their investment. We are lowering our cost base and putting systems and processes in place that help us become more efficient and more competitive. And we’ve set some ambitious targets to achieve over the next three years, with the aim of generating significant cost savings and a return on funds employed (ROFE) of 16 per cent by the end of our 2018 financial year. Nufarm has a strong global distribution platform; a broad product portfolio; a respected brand; and talented, committed employees who will continue to contribute to the success of the company. It’s a challenging, but exciting time to be part of a business where things are changing for the better. CONTENTS 01 About Nufarm 02 Key events 03 Facts in brief 04 Managing director’s review ER AND M 10 Business review M AR TO K S E U T 14 Sustainability C We understand our 16 Board of directors customers and markets. V E Our people, systems and A 18 Executive management R processes make us easy L U to deal with. U 20 Information on the company T L E 22 Corporate governance S U 36 Financial report C WE BUILD 37 Directors’ report VALUE FOR CUSTOMERS 57 Lead auditor’s independence declaration We safely AND NUFARM manufacture high We create unique E P quality products 58 Income statement C O value propositions and we deliver N R for our customers 59 Statement of comprehensive income those products in E T across our range L F full and on time O of high quality L 60 Balance sheet at the lowest E L products. -

Australian Capital Territory Listed Company Shareholdings As at 31 March 2021

? i Australian Capital Territory Listed Company Shareholdings at 31 March 2021 Publication Date: April 2021 Page | 1 10X Genomics Inc Airbus SE 3i Group PLC Aisin Corp 3M Co Ajinomoto Co Inc A O Smith Corp Akamai Technologies Inc a2 Milk Co Ltd/The Akzo Nobel NV ABB Ltd Albemarle Corp Abbott Laboratories Alcon Inc AbbVie Inc Alexandria Real Estate Equities Inc ABC-Mart Inc Alexion Pharmaceuticals Inc ABIOMED Inc Alfa Laval AB Accent Group Ltd Algonquin Power & Utilities Corp Accenture PLC Align Technology Inc Accor SA Alimentation Couche-Tard Inc Acom Co Ltd Alkane Resources Ltd ACS Actividades de Construccion y Servic Alleghany Corp Activision Blizzard Inc Allegion plc Adbri Ltd Allianz SE Adecco Group AG Allstate Corp/The adidas AG Ally Financial Inc Admiral Group PLC Alnylam Pharmaceuticals Inc Adobe Inc Alphabet Inc Advance Auto Parts Inc ALS Ltd Advanced Micro Devices Inc Alstom SA Advantest Corp AltaGas Ltd Adyen NV Altice USA Inc Aegon NV Altium Ltd Aeon Co Ltd Alumina Ltd Aflac Inc Amada Co Ltd Afterpay Ltd Amadeus IT Group SA AGC Inc Amazon.com Inc Ageas SA/NV Ambu A/S Agilent Technologies Inc Amcor PLC Agnaten SE AMERCO AGNC Investment Corp American Express Co Agnico Eagle Mines Ltd American Financial Group Inc/OH AIA Group Ltd American International Group Inc Air Canada American Tower Corp Air Liquide SA American Water Works Co Inc Air Products and Chemicals Inc Ameriprise Financial Inc Air Water Inc AmerisourceBergen Corp Airbnb Inc AMETEK Inc Page | 2 Amgen Inc Assicurazioni Generali SpA AMP Ltd Assurant Inc Amphenol Corp -

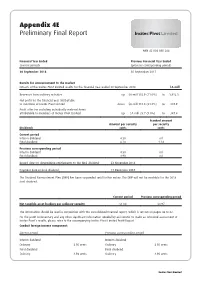

Appendix 4E Preliminary Final Report

Appendix 4E Preliminary Final Report ABN 42 004 080 264 Financial Year Ended Previous Financial Year Ended (current period) (previous corresponding period) 30 September 2018 30 September 2017 Results for announcement to the market Extracts of the Incitec Pivot Limited results for the financial year ended 30 September 2018 $A mill Revenues from ordinary activities up $A mill 382.9 (11.0%) to 3,856.3 Net profit for the financial year attributable to members of Incitec Pivot Limited down $A mill 110.8 (34.8%) to 207.9 Profit after tax excluding individually material items attributable to members of Incitec Pivot Limited up $A mill 28.7 (9.0%) to 347.4 Franked amount Amount per security per security Dividends cents cents Current period Interim dividend 4.50 nil Final dividend 6.20 1.24 Previous corresponding period Interim dividend 4.50 nil Final dividend 4.90 nil Record date for determining entitlements to the final dividend: 23 November 2018 Payment date of final dividend: 17 December 2018 The Dividend Reinvestment Plan (DRP) has been suspended until further notice. The DRP will not be available for the 2018 final dividend. Current period Previous corresponding period Net tangible asset backing per ordinary security $1.04 $0.97 The information should be read in conjunction with the consolidated financial report, which is set out on pages 46 to 82. For the profit commentary and any other significant information needed by an investor to make an informed assessment of Incitec Pivot’s results, please refer to the accompanying Incitec Pivot Limited Profit Report. -

Wesley Mission - Green Conscience Wesley Mission - Green Conscience

Wesley Mission - Green Conscience Wesley Mission - Green Conscience Contents Introduction Acknowledgments 1. Birdwood Park 2. Trees in Newcastle 3. Shortland Wetlands 4. Northern Parks & Playgrounds 5. Throsby Creek http://www.wesleymission.org.au/publications/green_c/default.asp (1 of 2) [6/06/2003 3:46:05 PM] Wesley Mission - Green Conscience 6. Hunter Botanic Gardens 1990-2001 7. The Ecohome & Eco-Village 8. Green Point 9. Koala Preservation Society 10. Friends of the Earth 11. Green Corps & Green Reserve 12. Glenrock State Recreation Area 13. Citizens Against Kooragang airport 14. Flora and Fauna Protection Society 15. Smoke Abatement 16. Cleaner beaches 17. Surfrider 18. No Lead Campaign at Boolaroo 19. Australia Native Plant Society 20. Wilderness Society 21. Animal Watch 22. The Green Movement Conclusion Bibliography http://www.wesleymission.org.au/publications/green_c/default.asp (2 of 2) [6/06/2003 3:46:05 PM] Introduction INTRODUCTION We live in a society where conspicuous consumption is often applauded, or envied, rather than deplored. In a society where most of the people live in poverty, the principle that 'more is better' applies. However, when a society becomes affluent this is no longer the case. Many of our problems originate in the fact that some people have not yet grasped this simple truth. One of the problems emanating from this state of affairs is the depletion of natural resources and the pollution of our land, air and water. This book gives a brief account of some of the groups who have attempted to restore a balance, or sanity, into the debate about where we, as a society, are heading. -

Pasminco Cockle Creek Smelter Pty Ltd Remediation Project

MAJOR PROJECT ASSESSMENT: Pasminco Cockle Creek Smelter Pty Ltd Remediation Project Director-General’s Environmental Assessment Report Section 75I of the Environmental Planning and Assessment Act 1979 February 2007 © Crown copyright 2007 Published February 2007 NSW Department of Planning www.planning.nsw.gov.au Disclaimer: While every reasonable effort has been made to ensure that this document is correct at the time of publication, the State of New South Wales, its agents and employees, disclaim any and all liability to any person in respect of anything or the consequences of anything done or omitted to be done in reliance upon the whole or any part of this document. ©NSW Government February 2007 Pasminco Cockle Creek Smelter Site – Remediation Project Director-General’s Environmental Assessment Report EXECUTIVE SUMMARY Pasminco Cockle Creek Smelter Pty Ltd (the Proponent) (Subject to Deed of Company Arrangement) proposes to remediate land associated with its former lead smelting operations at Boolaroo, near Newcastle. The land proposed to be remediated includes Lot 201 DP 805914, Lot 21 DP 253122, Lot 1 DP 523781 and Lot 23 DP 251322. The main site of the PCCS land (Lot 201 DP805914) is currently subject to a Remediation Order issued by the Department of Environment and Conservation (DEC) on 1 July 2003 under the Contaminated Land Management Act, 1997. In issuing the Remediation Order, the DEC considered that the dust, surface water and groundwater leaving the main site posed a Significant Risk of Harm to human health and the environment. The Proponent closed the smelter on 12 September 2003 and since that time has undertaken actions to address the Remediation Order.