Fair Value Appraisal Of: Tivoli Village at Queensridge

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

10190 Covington Cross Drive, Las Vegas, NV Sublease Brochure 10-21-20 2020-10-22 17.37.08.Indd

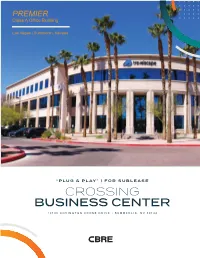

PREMIER Class A Offi ce Building Las Vegas | Summerlin, Nevada “PLUG & PLAY” | FOR SUBLEASE CROSSING BUSINESS CENTER 10190 COVINGTON CROSS DRIVE • SUMMERLIN, NV 89144 AVAILABLE SPACE Creative sublease opportunity! Best offi ce location in the heart of Summerlin, the Las Vegas valley’s strongest submarket! • Space Available – Entire building available totaling 75,588 RSF – Sublease premises of Suite 100A, Suite 120 and entirety of Floors 2 & 3 totaling 58,894 RSF – Entire building can be leased or the building can be devisable for full fl oor users • Rate $30.00/RSF, Modifi ed Gross per year or $2.50/RSF, Modifi ed Gross per month • Available Immediately • Term – Sublease Term Through October 31, 2022 – Longer term direct lease also available directly through the Landlord • Parking Ratio Above standard parking ratio up to approximately 7/1,000 USF; reserved covered parking available • Furniture High-end, modern furniture systems available • Amenities – Outdoor Employee Courtyard – Close proximity to restaurants, shopping, golf courses, hotels, City National Arena practice facility for the Vegas Golden Knights Hockey Team and Las Vegas Ballpark – home of the Las Vegas Aviators Triple A baseball team – Easy access to Summerlin Parkway, I-215 Beltway and US-95 FLOOR 1 FLOOR 2 FLOOR 3 “PLUG & PLAY” | FOR SUBLEASE CROSSING BUSINESS CENTER 10190 COVINGTON CROSS DRIVE • SUMMERLIN, NV 89144 LEASING CONTACTS BRAD PETERSON RANDY BROADHEAD CBRE, Inc. Senior Vice President Senior Vice President Broker Lic. 00409987 +1 702 369 4809 +1 702 369 4867 3993 Howard Hughes Pkwy, Suite 700 [email protected] [email protected] Las Vegas, NV 89169 Lic. -

At Las Vegas Boulevard

LOGISTICENTER AT LAS VEGAS BOULEVARD Available for Pre-Leasing | Delivery Q2 2019 ±109,200 SF Speculative Distribution Building 3475 N. Las Vegas Blvd, Las Vegas, NV 89115 Dermody.com Susan Borst , CCIM Dan Doherty Jerry Doty Senior Vice President Executive Vice President Associate Colliers | Las Vegas Colliers | Las Vegas Colliers | Las Vegas T +1 702 836 3719 T +1 702 836 3707 T +1 702 836 3735 [email protected] [email protected] [email protected] • Class A high image state-of-the- art construction • ±109,200 SF Speculative Distribution Building • Proximity to high quality, skilled labor pool LOGISTICENTER AT LAS VEGAS BOULEVARD • Available for Pre-Leasing | Delivery Q2 2019 • 3475 N. Las Vegas Boulevard, Las Vegas, NV 89115 SITE PLAN SITE DATA SUMMARY: APN: 140-07-701-018 (8.28 ACRES) JURISDICTION: CLARK COUNTY NEVADA ZONING: MD (DESIGN MANUFACTURING) OCCUPANCY: B, S1, F1 CONSTRUCTION TYPE: IIIB SETBACKS FRONT, SIDES AND REAR 20'. ADJUST FOR BLDG HEIGHT OVER 35', USE THE FOLLOWING FORMULA. (MAX. HEIGHT - 35') x 1/3 = "A" (ADDITIONAL SETBACK) EX B = EXISTING SETBACK I C= TOTAL SETBACK (A+B) ST D ING A "A" (BLDG. HT. 40') - 35' = (5' X 1/3) = 1.66' O BU "B" (EXISTING SET BACK) = 20' R IL "C" (TOTAL SETBACK) = "A" (1.66') + "B" (20') = 21.66'. USE 22'-0" T DI N G NU E TOTAL SITE ACREAGE: 8.2 ACRES XI AL ST IN FAR: 30.27% G W 3 0 ' D N. DETENTION R DOCK DOORS:: 12 DOORS +/ IV BASIN - 5 E 96 ' A - 0 IS DOCK DOORS WITH LEVELERS & SEALS: 6 DOORS " LE DRIVE-IN DOORS: 4 DOORS + " /- PARKING REQUIRED: 0 93 - ' ' -0 2 " WAREHOUSE: -

Appendix B. TRAFFIC OPERATIONS METHODOLOGY and ASSUMPTIONS

Appendix B. TRAFFIC OPERATIONS METHODOLOGY AND ASSUMPTIONS Traffic Operations Methodology and Assumptions Contents Page No. 1. Introduction and Background ................................................................................................................ 1 2. Project Goals and Objectives ................................................................................................................ 1 3. Project Study Limits ............................................................................................................................... 2 Mesoscopic Simulation Analysis ........................................................................................................... 2 Microscopic Simulation Analysis and Alternative Development ........................................................... 2 4. Analysis Years and Scenarios for Evaluation ...................................................................................... 6 US 95 .................................................................................................................................................... 6 CC 215 .................................................................................................................................................. 6 I-215 ...................................................................................................................................................... 6 I-15 ....................................................................................................................................................... -

Summerlin Brochure

10845 Griffith Peak Drive Suite 160 Las Vegas, NV 89135 BE PART OF SOMETHING BEAUTIFUL SUMMERLIN.COM 7.2020 SOME PLACES JUST Feel like Home It’s all right here. From the simple to the spectacular. From the silence of daybreak to the roar of the crowd. From the glow of The Strip to the awe of Red Rock Canyon. From quiet neighborhoods to buzzing blocks of fashion, dining, sports and entertainment. No matter where you turn, Summerlin presents inspiration in every direction, beckoning you to be part of something beautiful. Reverence Summerlin is 22,500 acres of master-planned perfection just waiting for life’s most beautiful moments. More than 150 miles of trails are carved into this desert oasis, meandering through hundreds of parks and More Planned the most diverse and stunning Perfection selection of homes in the city. for Years to Come. HIKE. BIKE. RUN. EXPLORE. GATHER. APPLAUD. PLAY. BREATHE. Vistas Pool SOME PLACES LET YOU Live out Loud. This is life lived out loud. Outside the box. Outside the lines, defined only by the outstanding backdrop of stunning Red Rock Canyon. With 300+ days of constant sunshine each year, life in Summerlin is as bold, beautiful and brilliant as it gets. Cottonwood Canyon Red Rock Loop SHOP. WORK. EAT. DRINK. Be. Fashionistas, foodies and fun seekers all gather on the bustling city blocks of Downtown Summerlin®, where residences, shops, sports, restaurants, bars and entertainment come together. When this stylish area is fully developed, the 400-acre walkable urban core will be home to even more excitement, as well as retail, office and luxe, high- density, urban-style residences. -

RRC Trnasportation Feasibility Study

Red Rock Canyon National Conservation Area Transportation Feasibility Study Final Report July 2012 Prepared by: John A. Volpe National Transportation Systems Center Research and Innovative Technologies Administration U.S. Department of Transportation Report Number: DOT-VNTSC-BLM-12-01 U.S. DOT Volpe Center RRCNCA Transportation Feasibility Study Table of Contents Executive Summary ................................................................................................................................................1 Overview and Goals ...................................................................................................................................1 Existing Conditions .....................................................................................................................................1 Definition of Alternatives ...........................................................................................................................2 Evaluation and Selection of Alternatives ...................................................................................................4 1 Introduction ........................................................................................................................................................5 1.1 Problem Definition .....................................................................................................................................5 1.1.1 Goals, Objectives, and Strategies .......................................................................................................6 -

Be Part of Something Beautiful

10845 Griffith Peak Drive Suite 160 Las Vegas, NV 89135 BE PART OF SOMETHING BEAUTIFUL SUMMERLIN.COM 7.2020 SOME PLACES JUST Feel like Home It’s all right here. From the simple to the spectacular. From the silence of daybreak to the roar of the crowd. From the glow of The Strip to the awe of Red Rock Canyon. From quiet neighborhoods to buzzing blocks of fashion, dining, sports and entertainment. No matter where you turn, Summerlin presents inspiration in every direction, beckoning you to be part of something beautiful. Reverence Summerlin is 22,500 acres of master-planned perfection just waiting for life’s most beautiful moments. More than 150 miles of trails are carved into this desert oasis, meandering through hundreds of parks and More Planned the most diverse and stunning Perfection selection of homes in the city. for Years to Come. HIKE. BIKE. RUN. EXPLORE. GATHER. APPLAUD. PLAY. BREATHE. Vistas Pool SOME PLACES LET YOU Live out Loud. This is life lived out loud. Outside the box. Outside the lines, defined only by the outstanding backdrop of stunning Red Rock Canyon. With 300+ days of constant sunshine each year, life in Summerlin is as bold, beautiful and brilliant as it gets. Cottonwood Canyon Red Rock Loop SHOP. WORK. EAT. DRINK. Be. Fashionistas, foodies and fun seekers all gather on the bustling city blocks of Downtown Summerlin®, where residences, shops, sports, restaurants, bars and entertainment come together. When this stylish area is fully developed, the 400-acre walkable urban core will be home to even more excitement, as well as retail, office and luxe, high- density, urban-style residences. -

Summerlin-Overview-101 Updated5

COMMUNITY BUILDER Since Summerlin® began development in the late 1980s, the community has become home to more than 100,000 Southern Nevadans who enjoy an unparalleled quality of life within one of the country’s most dynamic and exciting cities. As one of the nation’s best-selling master-planned communities for nearly two decades, Summerlin has set the standard both locally and nationally for award-winning master-planned development. Situated along the western rim of the Las Vegas Valley in the shadow of the Spring Mountain Range and Red Rock Canyon National Conservation Area, Summerlin is unfolding on 35 square miles of desert land acquired by Howard Hughes in the 1950s. It is one of the nation’s largest contiguous properties under single ownership adjacent to a major metropolitan area. The Howard Hughes Corporation spent more than three years developing a community master plan that set the standard for master-planned communities nationwide. The result is the stunning and vibrant community of Summerlin – a place where residents learn and live in harmony with the environment, their neighbors and their families. A multi-generational community, Summerlin abounds with parks, trails, sports fields, golf courses, natural open areas and its own live, work, play urban core in the heart of the community. The community boasts more educational choices than any other in Las Vegas with more than two dozen schools, including the city’s finest private schools and top-ranked public schools. Summerlin is also home to a growing number of national and local businesses that choose to make it a place to work as well as live. -

Southern Nevada HOV Plan Update

This page intentionally left blank Southern Nevada HOV Plan Update Prepared for: Nevada Department of Transportation Prepared by: April 2015 This page intentionally left blank Southern Nevada HOV Plan Update Table of Contents Executive Summary ................................................................................................ ES-1 ES.1. HOV System Evaluation .............................................................................................. ES-1 ES.2. HOV System Recommendations ................................................................................ ES-3 ES.3. HOV System Implementation Phasing Plan ................................................................ ES-7 ES.4. HOV Direct-Access Ramp Implementation Cost Estimates ........................................ ES-9 ES.5. HOV System Operational Plan .................................................................................. ES-10 ES.6. Next Steps ................................................................................................................. ES-12 1. Introduction ......................................................................................................... 1 1.1. Need for HOV Lanes ......................................................................................................... 1 1.2. Existing Managed Lanes in Southern Nevada .................................................................. 3 1.3. Planned HOV Lanes ........................................................................................................ -

TRAC-301 Comm Guide

A GUIDE TO THE SERVICES AVAILABLE NEAR YOUR NEW HOME Traccia COMMUNITY GUIDE Copyright 2004 Toll Brothers, Inc. All rights reserved. These resources are provided for informational purposes only, and represent just a sample of the services available for each community. Toll Brothers in no way endorses or recommends any of the resources presented herein. CONTENTS COMMUNITY PROFILE . .1 SCHOOLS . .2 CHILD CARE/PRE-SCHOOL . .2 SHOPPING . .3-4 MEDICAL FACILITIES . .4 PUBLIC UTILITIES/GENERAL INFORMATION . .5 WORSHIP . .6 TRANSPORTATION . .7 RECREATIONAL FACILITIES – LOCAL . .8-9 RECREATIONAL FACILITIES – REGIONAL . .10-11 RESTAURANTS . .12-13 LIBRARIES . .14 COLLEGES . .14 SOCIAL SERVICE ORGANIZATIONS . .15 GOVERNMENT . .15 SENIOR CITIZEN CENTERS . .16 ASSISTED LIVING . .16 EMERGENCY NUMBERS . .16 LEARN ABOUT THE SERVICES YOUR COMMUNITY HAS TO OFFER PROFILE In Traccia, you will enjoy the relaxed atmosphere of gracious living with good schools, excellent shopping, and a wide choice of cultural events close to home. Traccia, offering you both an exclusive neighborhood and a classic lifestyle, is an ideal place for you and your family to make new friends. It is a tranquil place to live with almost every type of recreational activity close at hand. The challenging 18-hole public golf courses of Angel Park and TPC Canyons are within ten minutes. Red Rock Canyon National Conservation Area, located within five minutes, has a 13-mile scenic loop, a natural history museum, and a visitor’s center, exhibiting native plant, animal and desert life. Other parks, including Spring Mountain Ranch and Toiyabe National Forest, are within 40 minutes of Traccia. At these parks, you and your family can enjoy hiking, picnicking, fishing, volleyball, horseback riding, and outdoor concerts. -

The Suites at Marketwalk Brochure Refresh 6

1985, 2025, 2115, 2120 FESTIVAL PLAZA DRIVE, LAS VEGAS, NEVADA 89135 SUMMERLIN Fashionistas, foodies, sports fans, fi tness junkies and funseekers all gather on the bustling city blocks of Downtown Summerlin®. Here, the lines between work and play are beautifully blurred. The Downtown Summerlin area is home to three Class A towers, nearly 400 luxury rental residences at Constellation and Tanager, Red Rock Casino Resort & Spa, City National Arena– practice facility for the National Hockey League’s Vegas Golden Knights and Las Vegas Ballpark®– a 10,000-capacity Triple-A baseball Stadium home to the Las Vegas Aviators which hosts more than 100 events annually. OFFICE ABOVE RETAIL SPACE consisting of approximately 33,734 SF UNIQUE 3.5:1000 PARKING RATIO, reserved parking available in a covered, multi-level parking structure along with abundant surface and customer parking RETAIL SPACE LEASING RATE Downtown Summerlin is part of a $2.60/RSF/MONTH/FSG planned urban center, serving the entire Las Vegas Valley. It includes retail, entertainment, offi ce, hotel, and multifamily residential elements, all designed to create a vibrant, walkable A WIDE ARRAY OF urban core within the award winning ENTERTAINMENT OPTIONS and unique dining destinations 22,500-acre Summerlin master- planned community. Downtown Summerlin totals nearly 400 acres and features more than 125 stores and restaurants in the streetscape- shopping environment with pedestrian thoroughfares and dynamic storefronts. CONVENIENT ACCESS to the I-215 Beltway via W. Charleston Blvd. and W. Sahara Blvd. THE POWER OF CONNECTIVITY 400 ACRE 30+ EATERIES 100+ WALKABLE URBAN CORE AND NUMEROUS OUTDOOR DINING OPTIONS NATIONAL AND LOCAL BRANDS • HOME TO LIFETIME FITNESS, TRUFUSION, PURE BARRE AND UNLIMITED OUTDOOR FITNESS OPPORTUNITIES • EASE OF ACCESS TO ENDLESS SERVICES SUCH AS BANKS, SALONS TO DOCTORS, SPAS AND SO MUCH MORE 2 15 Summerlin Parkway 95 ALL ROADS LEAD HERE. -

1050 INDIGO DRIVE Las Vegas, NV 89145 RARE SUMMERLIN INVESTMENT OPPORTUNITY SELLER MAY CONSIDER a CARRY BACK

1050 INDIGO DRIVE Las Vegas, NV 89145 RARE SUMMERLIN INVESTMENT OPPORTUNITY SELLER MAY CONSIDER A CARRY BACK Offered by: Service You Deserve. People You Trust. Jarrad Katz, SIOR, CCIM Galit Kimerling 5960 South Jones Boulevard Executive Vice President I Principal Vice President Las Vegas, Nevada 89118 Lic#: BS.0145888 Lic#: S.0065773 T 702.388.1800 | F 702.388.1010 702.610.1002 323.244.1628 www.mdlgroup.com [email protected] [email protected] HIGHLIGHTS INVESTMENT OVERVIEW ACQUISITION NARRATIVE LOCATION 1050 Indigo Drive, Las Vegas, NV 89145 This offering is a rare opportunity to acquire a quality office PARCEL NUMBER 137-368-110-17 asset in an A+ location. The property is fully occupied with sig- nificant upside going forward. Current rents are ±40% below INTERSECTION Indigo Drive & Charleston Boulevard market rents of like kind office properties within the immediate area. It would be incredibly difficult to replace this asset, due SQUARE FOOTAGE ±20,774 to an absence of available land for commercial development in The JGS Group, Douglas M. Edwards, P.C, Michael J. Mona, the sub-market. TENANTS Jr., Wiley Law LLC, Naylor & Braster, Envision PURCHASE PRICE $5,500,000 ($264.75 PSF) ACTUAL CAP RATE 6.14% PROFORMA CAP RATE 9.99% NOI $348,116.46 LEASE TYPE Full service gross on most leases RENTAL ESCALATIONS 3% on average YEAR BUILT 2004 LOT SIZE ±1.5 Acres HIGHLIGHTS AREA DESCRIPTION In 1952 Howard Hughes purchased a ±25,000 acre parcel in Southern Nevada to possibly relocate his California based airline operation. Hughes ended up not relocating after all. -

The Center at Spring Mountain

THE CENTER AT STEVE NEIGER, CCIM SPRING MOUNTAIN +1 702 592 7187 [email protected] 3893 SPRING MOUNTAIN ROAD, LAS VEGAS, NV 89102 License # NV-S.0078706.LLC JOIN THE FOLLOWING TENANTS AND MORE: THE CENTER AT SPRING MOUNTAIN 3893 SPRING MOUNTAIN ROAD, LAS VEGAS, NV 89102 A T 5 MB BLVD ALTA MIRA CRAIG ROAD 573 World renowned as Las Vegas’ very own China Town, this OAD 93 PECOS ROAD N RAINBOW BLVD RAINBOW N BUFFALO DRIVE BUFFALO NORTH D 599 GAS BLV LAS VEGAS M area, just one very quick mile west of the Fashion Show A VE ANGO RTIN LUTHER KING JR BLVD N LAS HILLS W CHEYENNE AVENUE 574 Mall, Wynn & Encore Resorts, and The Strip, has become M DESERT E Evans Ave SHORES NORTH LAS VEGAS EY AIRPORT SMOKE RANCH ROAD E Carey Ave Belmont St a destination for both locals and tourists alike. 95 147 W LAKE MEAD BLVD N RANCHO DR 147 N N BRUCE S BRUCE VEGAS DRIVE N E AT T LAS VEGAS 15 ASTERN AVE RLIN W WASHINGTON DRIVE MUNICIPAL With uniquely themed properties that include some of the most famous and well SUMMERLIN PARKWAY RAMPART WESTCLIFF DRIVE 95 known restaurants in the Las Vegas valley, the China Town corridor is visited at ANGEL LAS VEGAS N J PARK ONES DESERT PINES ALTA DRIVE 515 93 BL all times day and night, with some hot spots open with 60-minute waits as late VD W CHARLESTON BLVD 159 FREMON (or early) as 3:00 AM. There’s no place off the Las Vegas Strip quite like it! T ST YON 607 595 E ST LOUIS AVE ATE W SAHARA AVE 589 VALLEY VIEW ROAD BUFFALO E SAHARA AVE IP R ST D LAS VEGAS D E A 612 TH RIVE CC PROPERTY DETAILS E DESERT INN ROAD INN