The Greater Pittsburgh Region: Working Together to Compete Globally

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Fit City Challenge Series Is Coming, Get Ready Akron, Cincinnati, Cleveland, Columbus, and Pittsburgh!

THE FIT CITY CHALLENGE SERIES IS COMING, GET READY AKRON, CINCINNATI, CLEVELAND, COLUMBUS, AND PITTSBURGH! We’re excited to announce the FREE 2020 FIT CITY CHALLENGE! This is an ongoing social impact campaign with engaging programs throughout the year with 3 primary benefits for participation: ● Fitness & Health ● Leadership Development ● Community Engagement Participating is a great way to add new engagement tools to improve the health and fitness of your employees, while coming together as a city! Our Sign Up Challenge is to see which city can sign up 100 companies first! That sets the stage to make this an historic challenge that could help your company and make your city benefit from this friendly competition. The actual challenge runs from September 1 - October 15, 2020. This is the start of our platform being “always on” -- meaning there will always be programs available to help your company, including an annual calendar of events and challenges. We’re turning up our commitment to bring together great programs and partners to help your company. Why YOU and YOUR COMPANY should participate: ● Enhances your company wellness program and engages your employees in healthy competition ● It’s FREE, fun, and easy, with opportunities to win prizes and recognition ● Companies in the “Winner’s Circle” will be featured in broadcast television spots The 2020 FIT CITY CHALLENGE Details: ● Individual account activation starts on August 1st, 2020, but company registration is OPEN! ● Challenge officially kicks off on September 1 and runs through October -

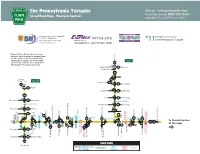

Simple Maps of the Pennsylvania Turnpike System

The Pennsylvania Turnpike Website: www.paturnpike.com Customer Service: 800.331.3414 (Outside U.S., call 717.831.7601) Travel Information: Dial 511 within PA Emergency Assistance or 1-877-511-PENN(7366) (877.736 .6727) when calling from outside of PA, Customer Service *11on the Pennsylvania Turnpike or visit www.511pa.com (Outside U.S., call 717-561-1522) *Gateway Toll Plaza (#2) near Ohio is a one-way toll facility. No toll is charged for westbound travel into Ohio, but there is an eastbound toll to enter Delmont Greensburg Pennsylvania via Gateway. The one-way tolling Bypass conversion was required to ease congestion and 66 allow installation of Express E-ZPass lanes. 14 Murrysville 22 Blairsville Sheffield D r. 66 12 BUS Sharon, Beaver Valley 66 Youngstown Expressway Harrison City 993 9 BUS Greensburg 376 15 66 422 Butler 8 Jeannette 130 Greensburg 376 6 Irwin 30 Greensburg 17 Mt. Jackson 108 New Castle Mainline Toll Zone 4 Mainline Toll Zone West Newton 136 Greensburg 20 New Galilee 168 Moravia 1 Erie Arona Rd. 351 Butler Ligonier Murrysville New Kensington Johnstown Greensburg 119 19 0 26 Elwood City ALLEGHENY 28 PITTSBURGH IRWIN DONEGAL 711 SOMERSET VALLEY 22 57 30 NEW STANTON 601 48 67 New Stanton Service Plaza 91 110 N.Somerset Service Plaza Allegheny Tunnel Warrendale Toll Plaza Allegheny River Allegheny Gateway Toll Plaza (Eastbound Only)* 75 Beaver River Beaver 49 To Central Section 76 70 76 Ohio 2 30 78 NEW BEAVER CRANBERRY BUTLER 112 of the map CASTLE 18 VALLEY 28 VALLEY 70 119 31 10 13 8 39 29 79 376 Darlington 551 Beaver -

Cleveland/Detroit Study Team Final Report

Federal Aviation Administration Cleveland/Detroit Metroplex Optimization of Airspace and Procedures Study Team Final Report May 2014 By Cleveland/Detroit Metroplex Study Team Table of Contents 1 Background 1 2 Purpose of the Metroplex Study Team 2 3 Cleveland/Detroit Metroplex Study Team Analysis Process 3 3.1 Five Step Process 3 3.2 Cleveland/Detroit Study Area Scope 5 3.3 Assumptions and Constraints 6 3.4 Assessment Methodology 6 3.4.1 Track Data Selected for Analyses 7 3.4.2 Analysis and Design Tools 9 3.4.3 Determining the Number of Operations and Modeled Fleet Mix 10 3.4.4 Determining Percent of RNAV Capable Operations by Airport 12 3.4.5 Profile Analyses 13 3.4.6 Cost to Carry (CTC) 13 3.4.7 Benefits Metrics 13 3.5 Key Considerations for Evaluation of Impacts and Risks 15 4 Identified Issues and Proposed Solutions 16 4.1 Design Concepts 16 4.2 CLE Procedures 19 4.2.1 CLE Arrivals 20 4.2.2 CLE Departures 34 4.2.3 CLE SAT Departures Issues 43 4.2.4 Summary of Potential Benefits for CLE 44 4.3 DTW Procedures 45 4.3.1 DTW Arrivals 45 4.3.2 DTW Departures 72 4.3.3 Summary of Potential Benefits for DTW 85 4.4 D21 Airspace Issues 86 4.5 T-Route Notional Designs 87 4.6 Military Issues 88 4.6.1 180th FW Issues 88 4.6.2 KMTC Issues 89 4.7 Industry Issues 90 4.8 Out of Scope Issues 90 4.9 Additional D&I Considerations 91 5 Summary of Benefits 92 5.1 Qualitative Benefits 92 5.1.1 Near-Term Impacts 92 i 5.1.2 Long-Term Impacts to Industry 93 5.2 Quantitative Benefits 93 Appendix A Acronyms 95 Appendix B PBN Toolbox 99 ii List of Figures Figure 1. -

Cincinnati, Oh Laboratory--Us Epa Office of Research

CINCINNATI, OH LABORATORY US EPA OFFICE OF RESEARCH AND DEVELOPMENT At a Glance The EPA laboratory in Cincinnati, OH is a major federal facility that includes a large Office of Research and Development (ORD) presence. Scientists in Cincinnati con- duct a wide range of environmental and public health research. ORD activities have significant impacts on the Greater Cincinnati region—which includes south- west Ohio, northern Kentucky and southeastern Indiana—by advancing science, positively impacting the economy, and contributing to the local community. Science: ORD is a world-class research organization, and the research conducted by scientists in Cincinnati has broad impacts at local, regional, and national levels. Among many different areas of study, ORD scientists develop methods, models, and tools that help states and communities assess environmental risks and, ultimate- ly, make decisions to manage chemical risks, clean up hazardous waste sites, and safeguard water quality, public water systems, and public health. Community Engagement: ORD scientists are developing water quality monitoring, modeling and management practices in partnership with the East Fork Watershed Cooperative, a multi-agency group focused on improving water quality in this lo- cal, mixed-use watershed. EPA is also a technical anchor for Confluence, the Water Technology Innovation Cluster for the Ohio River Valley Region, which helps draw companies to the region to collaborate on water technology. Cincinnati Laboratory Impacts by the Numbers Economic Impacts: The EPA Cincinnati facility has a total federal payroll of over $58 mil- lion. The 980 people working there provide a total of $88.6 million dollars that are inject- Greater Cincinnati, OH Area ed into the local economy where workers buy goods and services in the community, 980 $88.6 million 537 supporting additional jobs and spending and increasing overall economic output for the community. -

The Syrian Community in New Castle and Its Unique Alawi Component, 1900-1940 Anthony B

The Syrian Community in New Castle and Its Unique Alawi Component, 1900-1940 Anthony B. Toth L Introduction and immigration are two important and intertwined phenomena in Pennsylvania's history from 1870 to INDUSTRIALIZATIONWorld War II.The rapid growth of mining, iron and steel pro- duction, manufacturing, and railroads during this period drew millions of immigrants. In turn, the immigrants had a significant effect on their towns and cities. The largest non-English-speaking— groups to jointhe industrial work force — the Italians and Poles have been the sub- jects of considerable scholarly attention. 1 Relatively little, however, has been published about many of the smaller but still significant groups that took part in the "new immigration/' New Castle's Syrian community is one such smaller group. 2 In a general sense, it is typical of other Arabic-speaking immigrant com- munities which settled inAmerican industrial centers around the turn of the century — Lawrence, Fall River, and Springfield, Mass.; Provi- Writer and editor Anthony B. Toth earned his master's degree in Middle East history from Georgetown University. He performed the research for this article while senior writer for the American-Arab Anti-Discrimination Committee Re- search Institute. He has also written articles on the Arab-American communities in Jacksonville, Florida, and Worcester, Massachusetts. —Editor 1 Anyone researching the history of immigrants and Pennsylvania industry cannot escape the enlightening works of John E.Bodnar, who focuses main- ly on the Polish and Italian experiences. In particular, see his Workers' World: Kinship, Community and Protest in an Industrial Society, 1900- 1940 (Baltimore, 1982); Immigration and Industrialization: Ethnicity in an American MillTown, 1870-1940 (Pittsburgh, —1977); and, with Roger Simon and Michael P. -

Mercy Healthcare - Network Plan

Mercy Healthcare - Network Plan 1. Goals and objectives of the proposed network Mercy Health (formerly Catholic Health Partners) is a not-for-profit health care system headquartered in Cincinnati, Ohio. It is the largest health system in Ohio and one of the largest nonprofit health systems in the United States. Mercy Health employs more than 32,000 employees in more than 450 health facilities, including 23 hospitals in Ohio and Kentucky. It is the 4th largest Employer in Ohio. Mercy Health serves seven markets: Cincinnati, Toledo, Youngstown, Lima, Lorain and Springfield in Ohio and Paducah in Kentucky. The major markets are Cincinnati and Toledo. Mercy Health began serving Cincinnati neighborhoods for more than 160 years ago and has expanded to multiple award-winning hospitals that provide access to leading physicians, advanced technology, experienced and compassionate caregivers, and a wide range of care. Services include care for all aspects of life from maternity to senior care, primary and specialty care physician practices, outpatient centers, social service agencies and fitness centers to a variety of outreach programs. The Main Hospitals in the Cincinnati area are: Jewish Hospital Mercy Hospital Anderson Mercy Hospital Fairfield Mercy Clermont Mercy West Hospital Mercy Health was named one of the Top 15 Health Systems in the Nation by Truven Health Analytics (2013 and 2014). Anderson Hospital and Fairfield Hospital are rated among the 100 Top Hospitals in the nation by Truven Health Analytics (2014). Fairfield Hospital is rated nationally among the Top 50 Hospitals for Cardiovascular Care by Thomson Reuters (2011). Toledo is the other major area served by Mercy with a seven hospital system and a preferred provider of healthcare services for the 20-county area in Northwest Ohio and Southeast Michigan. -

Community Residential Centers?

COMMUNITY RESIDENTIAL CENTER TRANSITIONAL HOUSING DIRECTORY Cynthia Mausser Acting Managing Director Department of Rehabilitation and Correction Christopher Galli Chief Bureau of Community Sanctions Matthew Morris Assistant Chief Bureau of Community Sanctions Jennifer Gentry Assistant Chief Bureau of Community Sanctions REVISION DATE: DECEMBER 2019 What are Community Residential Centers? • A transitional housing initiative, formerly identified as independent housing, launched by the Department of Rehabilitation and Correction in January 2004. • The Bureau of Community Sanctions (BCS) has licensed contractors in the following cities: Akron, Canton, Chillicothe, Cincinnati, Cleveland, Columbus, Dayton, Greenville, Hamilton, Lima, Mansfield, Sidney and Toledo. The facilities provide temporary, transitional housing and some limited case management for offenders under Adult Parole Authority and Common Pleas Court supervision. • The Department will pay for residence in these facilities for up to 90 days for eligible offenders o If the agency and parole/probation officer request an extension of the 90-days due to extenuating circumstances, i.e. applying for SSI, etc. the BCS Assistant Chief or designee will review that request and may grant an extension as appropriate. Which offenders are eligible for Community Residential Centers? • TC offenders eligible for step-down to electronic monitoring and Adult Parole Authority and Common Pleas Court supervised offenders with no viable home placement that are at risk of being homeless. This includes offenders residing in homeless shelters. • Moderate to low risk/lower need offenders with little or no programming needs other than housing. • Higher risk/higher need offenders who have successfully completed adequate programming in prison, a halfway house, or through a community agency (or are currently involved in programming in the community) and are stabilized, but would still benefit from housing assistance due to not having a home placement. -

Chicago-South Bend-Toledo-Cleveland-Erie-Buffalo-Albany-New York Frequency Expansion Report – Discussion Draft 2 1

Chicago-South Bend-Toledo-Cleveland-Erie-Buffalo- Albany-New York Frequency Expansion Report DISCUSSION DRAFT (Quantified Model Data Subject to Refinement) Table of Contents 1. Project Background: ................................................................................................................................ 3 2. Early Study Efforts and Initial Findings: ................................................................................................ 5 3. Background Data Collection Interviews: ................................................................................................ 6 4. Fixed-Facility Capital Cost Estimate Range Based on Existing Studies: ............................................... 7 5. Selection of Single Route for Refined Analysis and Potential “Proxy” for Other Routes: ................ 9 6. Legal Opinion on Relevant Amtrak Enabling Legislation: ................................................................... 10 7. Sample “Timetable-Format” Schedules of Four Frequency New York-Chicago Service: .............. 12 8. Order-of-Magnitude Capital Cost Estimates for Platform-Related Improvements: ............................ 14 9. Ballpark Station-by-Station Ridership Estimates: ................................................................................... 16 10. Scoping-Level Four Frequency Operating Cost and Revenue Model: .................................................. 18 11. Study Findings and Conclusions: ......................................................................................................... -

Western Pennsylvania History Magazine

A snapshot of Pittsburgh LOOKING BACK at 1816 from 19 16 By Aaron O’Data and Carrie Hadley Learn More Online 44 WESTERN PENNSYLVANIA HISTORY SUMMER 2016 | The 200th anniversary of Pittsburgh’s incorporation explained “This morning about sunrise, we left Pittsburgh with all the joy of a bird which escapes from its cage. ‘From the tumult, and smoke of the city set free,’ we were ferried over the Monongahela, with elated spirits.” “[John Byrne] at his Umbrella Manufactory, Fourth, Between Market and Ferry Streets. Just received and for sale at his Oyster House, a few kegs of the most excellent Spiced Oysters [but] continues to make and repair Umbrellas and Parasols in the newest manner.” ~ both from Pittsburgh in 1816, published 1916 1 These two spirited, offbeat quotes are a tiny but entertaining window into the world of Pittsburgh in 1816, the year of its official incorporation as a city. In 1916, Pittsburghers saw fit to mark the centennial of the incorporation by gathering small sketches about the city for a book, Pittsburgh in 1816. The slim volume was compiled by unknown authors from the Carnegie Library of Pittsburgh, and is structured like a written photo album, with snapshots of information to “interest the Pittsburgher of 1916 chiefly because the parts and pieces of which it is made were written by men who were living here or passed this way in 1816.”2 To mark the bicentennial of the incorporation of Pittsburgh, it is fitting to look back on both the city’s founding and its centennial year. Cover of Pittsburgh in 1816. -

Trauma Centers

Updated: 5/5/2021 TRAUMA CENTERS Location Level EMS Adult Pediatric HOSPITAL CITY COUNTY Status Expires Visit Date Region Level Level Akron Children's Hospital Akron Summit 5 ACS 9/10/2022 2 Atrium Medical Center Franklin Butler 6 ACS 11/6/2022 3 Aultman Hospital Canton Stark 5 ACS 10/24/2021 6/4/2021 V 2 Bethesda North Cincinnati Hamilton 6 ACS 6/9/2022 3 Blanchard Valley Hospital Findlay Hancock 1 ACS 1/15/2024 3 Cincinnati Children's Hospital Medical Center Cincinnati Hamilton 6 ACS 1/23/2022 1 Cleveland Clinic Akron General Akron Summit 5 ACS 4/17/2022 1 Cleveland Clinic Fairview Hospital Cleveland Cuyahoga 2 ACS 3/9/2022 2 Cleveland Clinic Hillcrest Hospital Mayfield Heights Cuyahoga 2 ACS 12/9/2021 2 Dayton Children's Hospital Dayton Montgomery 3 ACS 2/12/2024 1 Firelands Regional Medical Center Sandusky Erie 1 ACS 2/23/2023 3 Fisher-Titus Medical Center Norwalk Huron 1 ACS 11/23/2022 3 Genesis HealthCare System Zanesville Muskingum 8 ACS 10/6/2024 3 Grandview Medical Center Dayton Montgomery 3 ACS 10/26/2022 3 Kettering Health Network Fort Hamilton Hospital Hamilton Butler 6 Ohio-18 8/24/2022 *3* Kettering Health Network Soin Medical Center Beavercreek Greene 3 ACS 11/13/2023 3 Kettering Medical Center Kettering Montgomery 3 ACS 1/11/2023 2 Lima Memorial Hospital Lima Allen 1 ACS 5/13/2021 5/4-5/2021 V 2 Marietta Memorial Hospital Marietta Washington 8 ACS 11/20/2022 3 Mercy Health St. Charles Hospital Toledo Lucas 1 ACS 12/8/2022 3 Mercy Health St. -

August 12, 2020 Allentown City Council 435

August 12, 2020 Allentown City Council 435 Hamilton Street Allentown, PA 18101 Eastern Region Office (610) 437-7555 PO Box 60173 By fax to (610) 437-7554 Philadelphia, PA 19102 By email to 215-592-1513 T 215-592-1343 F [email protected] [email protected] [email protected] Central Region Office PO Box 11761 [email protected] Harrisburg, PA 17108 [email protected] 717-238-2258 T [email protected] 717-236-6895 F [email protected] Western Region Office PO Box 23058 Re: Resolution 86 and District Attorney Martin’s Memorandum Pittsburgh, PA 15222 in Response 412-681-7736 T 412-681-8707 F To Council President Hendricks, Council Vice-President Guridy, and Council Members Affa, Gerlach, Mota, Siegel and Zucal: The American Civil Liberties Union of Pennsylvania has been made aware of the memorandum written by District Attorney Martin in opposition to proposed Resolution No. 86, which details Community Strategies for Police Oversight Review and Recommendations. Unfortunately, in raising his concerns, District Attorney Martin seems to have misinterpreted Pennsylvania law and its applicability. Based on growing community demands for police reform, Resolution No. 86 proposes to begin a dialogue on various police reform proposals. Several of these reforms originate from the Eight Can’t Wait agenda, which have been adopted by municipalities and police professionals from across the country, including by other officials in Pennsylvania. The Resolution does not mandate the adoption of any specific proposal at this time, but would only commit the City Council to make recommendations based on these discussions within three months—with the aim to produce legislation on any accepted recommendations. -

Pittsburgh, Philadelphia, and the Elusive Quest for a New Deal Majority in the Keystone State

A Tale of Two Cities: Pittsburgh, Philadelphia, and the Elusive Quest for a New Deal Majority in the Keystone State The Needs of the Many . N RETROSPECT, the formation of a Democratic electoral majority in the 1930s—one that ruled American politics for two generations— Iseems almost to have been inevitable. The Great Depression, and then a world war, enabled Franklin D. Roosevelt to lay the foundations of the modern welfare state, drive much of the public policy debate, and unite Americans in war—and to some extent in peace. But a careful study of the national scene, as well as sensitivity to the nuances of community and state politics in Pennsylvania, paints a different picture. The New Deal coalition was comprised of various interests with little in common beyond shared poverty and a profound admiration for President Roosevelt. Segregationist white southerners, northern blacks, Jews, Catholics, and unskilled workers who enlisted in the affiliates of the Congress of Industrial Organizations (CIO) maintained a tenuous alliance brokered by Roosevelt. On more than a few occasions, the New Deal coalition faltered, leading to both local and national Republican vic- tories. Due to effective organization, cultural preferences, and political habit, among other factors, Republicans remained viable, and even strong, in states such as Pennsylvania. Essential to Democratic victory were the children of southern and eastern European Roman Catholic and Jewish immigrants who clustered in the urban industrial centers of the North. With the advent of federal immigration-restriction legislation in 1921 (and again in 1924), ethnic urban wards largely ceased to be centers of transient male workers who had little desire to follow the moral exhortations of clergy, join labor THE PENNSYLVANIA MAGAZINE OF HISTORY AND BIOGRAPHY Vol.