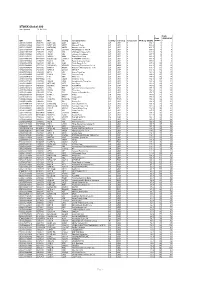

Mn Services Aandelenfonds Emerging Markets 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ANNUAL REPORT 2020 Important

stock code : 000063.SZ 763.HK ANNUAL REPORT 2020 Important The Board of Directors, Supervisory Committee and the Directors, Supervisors and senior management of the Company warrant that the contents of this report are true, accurate and complete without any false information, misleading statements or material omissions, and collectively and individually accept legal responsibility therefor. There are no Directors, Supervisors or senior management who do not warrant or who dispute the truthfulness, accuracy and completeness of the contents of this report. This report has been considered and approved at the Thirty-third Meeting of the Eighth Session of the Board of Directors of the Company. The respective financial statements of the Group for the year ended 31 December 2020 were prepared in accordance with PRC Accounting Standards for Business Enterprises and with Hong Kong Financial Reporting Standards respectively, and had been audited by Ernst & Young Hua Ming LLP and Ernst & Young, and an unqualified auditors’ report has been issued by each of them. During the year, there was no significant deficiency in internal control in relation to financial reporting of the Company, nor was any significant deficiency in internal control in relation to non-financial reporting identified. Mr. Li Zixue, Chairman of the Company, Ms. Li Ying, Chief Financial Officer of the Company and Mr. Xu Jianrui, Head of Finance Division of the Company, hereby declare that they warrant the truthfulness, accuracy and completeness of the financial reports contained in this report. In view of the state of affairs of the Company, the proposal for profit distribution for 2020 is as follows: distribution of RMB2 in cash (before tax) for every 10 shares to all shareholders based on the total share capital (including A shares and H shares) as at the record date for profit distribution and dividend payment. -

Fidelity® Emerging Markets Index Fund

Quarterly Holdings Report for Fidelity® Emerging Markets Index Fund January 31, 2021 EMX-QTLY-0321 1.929351.109 Schedule of Investments January 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 92.5% Shares Value Shares Value Argentina – 0.0% Lojas Americanas SA rights 2/4/21 (b) 4,427 $ 3,722 Telecom Argentina SA Class B sponsored ADR (a) 48,935 $ 317,099 Lojas Renner SA 444,459 3,368,738 YPF SA Class D sponsored ADR (b) 99,119 361,784 Magazine Luiza SA 1,634,124 7,547,303 Multiplan Empreendimentos Imobiliarios SA 156,958 608,164 TOTAL ARGENTINA 678,883 Natura & Co. Holding SA 499,390 4,477,844 Notre Dame Intermedica Participacoes SA 289,718 5,003,902 Bailiwick of Jersey – 0.1% Petrobras Distribuidora SA 421,700 1,792,730 Polymetal International PLC 131,532 2,850,845 Petroleo Brasileiro SA ‑ Petrobras (ON) 2,103,697 10,508,104 Raia Drogasil SA 602,000 2,741,865 Bermuda – 0.7% Rumo SA (b) 724,700 2,688,783 Alibaba Health Information Technology Ltd. (b) 2,256,000 7,070,686 Sul America SA unit 165,877 1,209,956 Alibaba Pictures Group Ltd. (b) 6,760,000 854,455 Suzano Papel e Celulose SA (b) 418,317 4,744,045 Beijing Enterprises Water Group Ltd. 2,816,000 1,147,720 Telefonica Brasil SA 250,600 2,070,242 Brilliance China Automotive Holdings Ltd. 1,692,000 1,331,209 TIM SA 475,200 1,155,127 China Gas Holdings Ltd. 1,461,000 5,163,177 Totvs SA 274,600 1,425,346 China Resource Gas Group Ltd. -

FTSE Korea 30/18 Capped

2 FTSE Russell Publications 19 August 2021 FTSE Korea 30/18 Capped Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) Alteogen 0.19 KOREA Hyundai Engineering & Construction 0.35 KOREA NH Investment & Securities 0.14 KOREA AmoreG 0.15 KOREA Hyundai Glovis 0.32 KOREA NHN 0.07 KOREA Amorepacific Corp 0.65 KOREA Hyundai Heavy Industries 0.29 KOREA Nong Shim 0.08 KOREA Amorepacific Pfd. 0.08 KOREA Hyundai Marine & Fire Insurance 0.13 KOREA OCI 0.17 KOREA BGF Retail 0.09 KOREA Hyundai Merchant Marine 1.02 KOREA Orion 0.21 KOREA BNK Financial Group 0.18 KOREA Hyundai Mipo Dockyard 0.15 KOREA Ottogi 0.06 KOREA Celltrion Healthcare 0.68 KOREA Hyundai Mobis 1.53 KOREA Paradise 0.07 KOREA Celltrion Inc 2.29 KOREA Hyundai Motor 2.74 KOREA Posco 1.85 KOREA Celltrion Pharm 0.24 KOREA Hyundai Motor 2nd Pfd. 0.33 KOREA Posco Chemical 0.32 KOREA Cheil Worldwide 0.14 KOREA Hyundai Motor Pfd. 0.21 KOREA Posco International 0.09 KOREA CJ Cheiljedang 0.3 KOREA Hyundai Steel 0.33 KOREA S1 Corporation 0.13 KOREA CJ CheilJedang Pfd. 0.02 KOREA Hyundai Wia 0.13 KOREA Samsung Biologics 0.92 KOREA CJ Corp 0.11 KOREA Industrial Bank of Korea 0.22 KOREA Samsung C&T 0.94 KOREA CJ ENM 0.15 KOREA Kakao 3.65 KOREA Samsung Card 0.08 KOREA CJ Logistics 0.12 KOREA Kangwon Land 0.23 KOREA Samsung Electro-Mechanics 0.81 KOREA Coway 0.36 KOREA KB Financial Group 1.78 KOREA Samsung Electronics 25.36 KOREA Daewoo Engineering & Construction 0.12 KOREA KCC Corp 0.12 KOREA Samsung Electronics Pfd. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Prohibited Agreements with Huawei, ZTE Corp, Hytera, Hangzhou Hikvision, Dahua and Their Subsidiaries and Affiliates

Prohibited Agreements with Huawei, ZTE Corp, Hytera, Hangzhou Hikvision, Dahua and their Subsidiaries and Affiliates. Code of Federal Regulations (CFR), 2 CFR 200.216, prohibits agreements for certain telecommunications and video surveillance services or equipment from the following companies as a substantial or essential component of any system or as critical technology as part of any system. • Huawei Technologies Company; • ZTE Corporation; • Hytera Communications Corporation; • Hangzhou Hikvision Digital Technology Company; • Dahua Technology company; or • their subsidiaries or affiliates, Entering into agreements with these companies, their subsidiaries or affiliates (listed below) for telecommunications equipment and/or services is prohibited, as doing so could place the university at risk of losing federal grants and contracts. Identified subsidiaries/affiliates of Huawei Technologies Company Source: Business databases, Huawei Investment & Holding Co., Ltd., 2017 Annual Report • Amartus, SDN Software Technology and Team • Beijing Huawei Digital Technologies, Co. Ltd. • Caliopa NV • Centre for Integrated Photonics Ltd. • Chinasoft International Technology Services Ltd. • FutureWei Technologies, Inc. • HexaTier Ltd. • HiSilicon Optoelectronics Co., Ltd. • Huawei Device Co., Ltd. • Huawei Device (Dongguan) Co., Ltd. • Huawei Device (Hong Kong) Co., Ltd. • Huawei Enterprise USA, Inc. • Huawei Global Finance (UK) Ltd. • Huawei International Co. Ltd. • Huawei Machine Co., Ltd. • Huawei Marine • Huawei North America • Huawei Software Technologies, Co., Ltd. • Huawei Symantec Technologies Co., Ltd. • Huawei Tech Investment Co., Ltd. • Huawei Technical Service Co. Ltd. • Huawei Technologies Cooperative U.A. • Huawei Technologies Germany GmbH • Huawei Technologies Japan K.K. • Huawei Technologies South Africa Pty Ltd. • Huawei Technologies (Thailand) Co. • iSoftStone Technology Service Co., Ltd. • JV “Broadband Solutions” LLC • M4S N.V. • Proven Honor Capital Limited • PT Huawei Tech Investment • Shanghai Huawei Technologies Co., Ltd. -

NVIDIA's New Ampere Data Center GPU in Full Production

NVIDIA’s New Ampere Data Center GPU in Full Production New NVIDIA A100 GPU Boosts AI Training and Inference up to 20x; NVIDIA’s First Elastic, Multi- Instance GPU Unifies Data Analytics, Training and Inference; Adopted by World’s Top Cloud Providers and Server Makers GTC 2020 -- NVIDIA today announced that the first GPU based on the NVIDIA® Ampere architecture, the NVIDIA A100, is in full production and shipping to customers worldwide. The A100 draws on design breakthroughs in the NVIDIA Ampere architecture — offering the company’s largest leap in performance to date within its eight generations of GPUs — to unify AI training and inference and boost performance by up to 20x over its predecessors. A universal workload accelerator, the A100 is also built for data analytics, scientific computing and cloud graphics. “The powerful trends of cloud computing and AI are driving a tectonic shift in data center designs so that what was once a sea of CPU-only servers is now GPU-accelerated computing,” said Jensen Huang, founder and CEO of NVIDIA. “NVIDIA A100 GPU is a 20x AI performance leap and an end-to-end machine learning accelerator — from data analytics to training to inference. For the first time, scale-up and scale-out workloads can be accelerated on one platform. NVIDIA A100 will simultaneously boost throughput and drive down the cost of data centers.” New elastic computing technologies built into A100 make it possible to bring right-sized computing power to every job. A multi-instance GPU capability allows each A100 GPU to be partitioned into as many as seven independent instances for inferencing tasks, while third-generation NVIDIA NVLink® interconnect technology allows multiple A100 GPUs to operate as one giant GPU for ever larger training tasks. -

Lessons of Korea's Financial Sector Policies

ADB INSTITUTE RESEARCH PAPER 47 Financial Repression, Liberalization, Crisis and Restructuring: Lessons of Korea’s Financial Sector Policies Yoon Je Cho November 2002 In the last 50 years, Korea’s financial sector has gone through heavy repression, rapid liberalization, deep crises and finally massive restructurings. However, there is no optimum financial sector policy to be applied at all times and system inertia often prevents the timely adjustment of policy to changed circumstances. Although no agreed international best practice has yet been found to guide successful and rapid economic expansion, financial sector reform should always be tuned to progress in the real sector and the capabilities of financial market infrastructure. adbi.org ADB Institute Research Paper Series No. 47 November 2002 Financial Repression, Liberalization, Crisis and Restructuring: Lessons of Korea’s Financial Sector Policies Yoon Je Cho I ADB INSTITUTE RESEARCH PAPER 47 ABOUT THE AUTHOR Yoon Je Cho is a Professor of Economics at the Graduate School of International Studies, Sogang University, Korea. He received his Ph.D. in economics from Stanford University and was the Vice President of the Korea Institute of Public Finance. Prof. Cho has also served for two terms as a senior counsellor to the Deputy Prime Minister and Minister of Finance and Economy of Korea. Additional copies of the paper are available free from the Asian Development Bank Institute, 8th Floor, Kasumigaseki Building, 3-2-5 Kasumigaseki, Chiyoda-ku, Tokyo 100-6008, Japan. Attention: Publications. Also online at www.adbi.org Copyright © 2002 Asian Development Bank Institute. All rights reserved. Produced by ADBI Publishing. The Research Paper Series primarily disseminates selected work in progress to facilitate an exchange of ideas within the Institute’s constituencies and the wider academic and policy communities. -

Fact Sheet:State Street Defensive Emerging Markets Equity Fund

State Street Defensive Emerging Markets Equity Fund - Class K Equity 30 June 2021 Fund Objective Total Return The State Street Defensive Emerging Markets Equity Fund seeks to provide MSCI Emerging maximum total return, primarily through capital appreciation, by investing Cumulative Fund at NAV Market Index primarily in securities of foreign issuers. QTD 5.52% 5.05% Process YTD 12.79 7.45 In seeking to identify stocks offering the potential for capital growth, the Annualized Adviser employs a proprietary quantitative process. The process evaluates 1 Year 37.80 40.90 the relative attractiveness of eligible securities based on the correlation 3 Year 8.25 11.27 of certain historical economic and financial factors (such as measures of 5 Year 8.45 13.03 growth potential, valuation, quality and investor sentiment) and based on other historical quantitative metrics. 10 Year 0.96 4.28 The Adviser also uses a quantitative analysis to determine the expected volatility of a stock's market price. Volatility is a statistical measurement of up and down fluctuations in the value of a security over time. Gross Expense Ratio 1.52% Through these quantitative processes of security selection and portfolio Net Expense Ratio^ 1.00% diversification, the Adviser expects that the portfolio will be subject to a 30 Day SEC Yield 1.41% relatively low level of absolute risk (as defined by statistical measures of 30 Day SEC Yield (Unsubsidized) 1.34% volatility, such as standard deviation of returns) and should exhibit relatively Maximum Sales Charge - low volatility compared with the Index over the long term. There can be no assurance that the Fund will in fact achieve any targeted level of volatility or experience lower volatility than the Index, nor can there be any assurance Performance quoted represents past performance, which is no guarantee of that the Fund will produce returns in excess of the Index. -

FTSE Publications

2 FTSE Russell Publications 01 October 2020 FTSE Value Stocks China A Share Indicative Index Weight Data as at Closing on 30 September 2020 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) Agricultural Bank of China (A) 4.01 CHINA Fuyao Glass Group Industries (A) 1.43 CHINA Seazen Holdings (A) 0.81 CHINA Aisino Corporation (A) 0.52 CHINA Gemdale (A) 1.37 CHINA Shanghai Fosun Pharmaceutical Group (A) 1.63 CHINA Anhui Conch Cement (A) 3.15 CHINA GoerTek (A) 2.12 CHINA Shenwan Hongyuan Group (A) 1.11 CHINA AVIC Investment Holdings (A) 0.61 CHINA Gree Electric Appliances Inc of Zhuhai (A) 7.48 CHINA Shenzhen Overseas Chinese Town Holdings 0.66 CHINA Bank of China (A) 2.23 CHINA Guangdong Haid Group (A) 1.24 CHINA (A) Bank Of Nanjing (A) 1.32 CHINA Guotai Junan Securities (A) 1.99 CHINA Sichuan Chuantou Energy (A) 0.71 CHINA Bank of Ningbo (A) 2 CHINA Hangzhou Hikvision Digital Technology (A) 3.56 CHINA Tbea (A) 0.86 CHINA Beijing Dabeinong Technology Group (A) 0.56 CHINA Henan Shuanghui Investment & Development 1.49 CHINA Tonghua Dongbao Medicines(A) 0.59 CHINA China Construction Bank (A) 1.83 CHINA (A) Weichai Power (A) 2.09 CHINA China Life Insurance (A) 2.14 CHINA Hengtong Optic-Electric (A) 0.59 CHINA Wuliangye Yibin (A) 9.84 CHINA China Merchants Shekou Industrial Zone 1.03 CHINA Industrial and Commercial Bank of China (A) 3.5 CHINA XCMG Construction Machinery (A) 0.73 CHINA Holdings (A) Inner Mongolia Yili Industrial(A) 6.32 CHINA Xinjiang Goldwind Science&Technology (A) 0.74 -

STOXX Global 200 Last Updated: 01.02.2018

STOXX Global 200 Last Updated: 01.02.2018 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) US0378331005 2046251 AAPL.OQ AAPL Apple Inc. US USD Y 694.2 1 1 US5949181045 2588173 MSFT.OQ MSFT Microsoft Corp. US USD Y 588.4 2 2 US0231351067 2000019 AMZN.OQ AMZN Amazon.com Inc. US USD Y 466.7 3 3 US30303M1027 B7TL820 FB.OQ US20PD FACEBOOK CLASS A US USD Y 355.6 4 4 US46625H1005 2190385 JPM.N CHL JPMorgan Chase & Co. US USD Y 329.9 5 5 US4781601046 2475833 JNJ.N JNJ Johnson & Johnson US USD Y 297.7 6 6 US30231G1022 2326618 XOM.N XON Exxon Mobil Corp. US USD Y 296.9 7 7 US02079K1079 BYY88Y7 GOOG.OQ US40C2 ALPHABET CLASS C US USD Y 289.1 8 8 US0605051046 2295677 BAC.N NB Bank of America Corp. US USD Y 250.0 9 9 US9497461015 2649100 WFC.N NOB Wells Fargo & Co. US USD Y 237.5 10 11 KR7005930003 6771720 005930.KS KR002D Samsung Electronics Co Ltd KR KRW Y 223.3 11 10 US0846707026 2073390 BRKb.N BRKB Berkshire Hathaway Inc. Cl B US USD Y 218.2 12 13 CH0038863350 7123870 NESN.S 461669 NESTLE CH CHF Y 216.1 13 12 US4370761029 2434209 HD.N HD Home Depot Inc. US USD Y 192.8 14 17 US1667641005 2838555 CVX.N CHV Chevron Corp. US USD Y 190.6 15 15 US00206R1023 2831811 T.N SBC AT&T Inc. US USD Y 184.6 16 14 US92826C8394 B2PZN04 V.N U0401 VISA Inc. -

Representative Legal Matters Mark W.C

Representative Legal Matters Mark W.C. Tu Represented KKR in relation to its proposed buyout of Yageo Corporation. Represented Advanced Semiconductor Engineering Inc. in its acquisition of 100 percent shares of PowerASE Technology by way of tender offer and merger. Represented Morgan Stanley, the financial advisor to Polaris Securities Corporation, in relation to its share swap with Yuanta Financial Holding Company. Represented MediaTek Inc. for acquisition of 100 percent of outstanding shares of Ralink Technology Corporation by way of a share swap. Represented Chimei Optoelectronics Corporation in relation to its merger with Innolux Corporation. Represented Morgan Stanley, the financial advisor to Taiwan International Securities Corporation (TISC), in relation to the sale of all issued and outstanding shares of TISC to Capital Securities Corporation by way of a tender offer followed by a merger. Represented E.Sun Commercial Bank in its general business and asset assumption from Chu Nan Co-operative Credit Association. Represented Prime View International Co., Ltd. in relation to its acquisition of E. Ink Corporation by way of a share exchange. Represented Morgan Stanley Private Equity in its acquisition of a stake in CTCI Corporation. Representing WIN Semiconductors Corporation in relation to its issuance of global depositary receipts. Represented E.Sun Financial Holding Company. in relation to its issuance of global depositary receipts. Represented Cathay Financial Holding Company in relation to its issuance of European convertible bonds. Represented Chunghwa Telecom Co., Ltd. in relation to its Form 20-F filing submitted to the U.S. Securities and Exchange Commission. Represented Pegatron Corporation in relation to its issuance of European convertible bonds. -

Japanese Companies' Links to Forced Labor in Xinjiang Uyghur

8 April 2021 [original Japanese text] 6 May 2021 [English translation] Japanese Companies’ Links to Forced Labor in Xinjiang Uyghur Autonomous Region and Corporate Responsibility1 Human Rights Now Japan Uyghur Association We are greatly concerned that Japanese companies have not yet taken sufficient measures to completely eliminate the possibility that they are involved through their supply chains in the Chinese government's mass detention, abuse, forced labor, and destruction of Muslim culture in Xinjiang Uyghur Autonomous Region. It has also been revealed that under the Chinese government's "Strike Hard Campaign against Violent Extremism," there are serious and widespread abuses and violations of basic human rights such as freedom of expression, association and privacy and freedom from torture and inhumane treatment, forced labor, unfair trial, discrimination, and violations of minority rights. In the report "Japanese Companies’ Links to Forced Labor in Xinjiang Uyghur Autonomous Region" dated 28 August 2020,2 we proposed that companies should fulfill their responsibilities in accordance with The UN Guiding Principles on Business and Human Rights ("Guiding Principles")3 in response to forced labor, which is a serious human rights violation, referred to in the report, “Uyghurs for sale: ‘Re-education’, forced labour and surveillance beyond Xinjiang” by the Australian Strategic Policy Institute (ASPI).4 Based on the Guiding Principles, Japanese companies are required to conduct human rights due diligence covering their supply chains and value chains, not only in cases where their business activities cause human rights violations, but also in cases where they may be involved in or contribute to human rights violations, or where their business, products or services directly link to business partners which violate human rights.