Restructuring Across Borders

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Judgment Claims in Receivership Proceedings*

JUDGMENT CLAIMS IN RECEIVERSHIP PROCEEDINGS* JOHN K. BEACH Connecticuf Supreme Court of Errors In view of the importance of the subject it is unfortunate that so few of the reported cases on equitable receiverships of corporations have dealt in any comprehensive way with the principles underlying the administrating of the fund for the benefit of creditors. The result is that controversy has outstripped authoritative decision, and the subject is unsettled. To this generalization an exception must be noted in respect of the special topic of the application of current rail- way income to current expenses, before the payment of mortgage 1 indebtedness. On another disputed topic, the provability of imma.ure claims, the law, or at least the right principle of decision, has been settled, by the notable opinion of Judge Noyes in Pennsylvania Steel Company v. New York City Railway Company,2 followed and rein- forced by that of Mr. Justice Holmes in William Filene'sSons Company v. Weed.' Notwithstanding these important exceptions, the dearth of authority on the general subject is such that Judge Noyes refers to a case cited in his opinion as "almost the only case in which rules have "been formulated with respect to the provability of claims against "insolvent corporations."4 Upon the particular phase of the subject here discussed, the decisions are to some extent in conflict, and no attempt seems to have been made in text books or decisions to examine the question in the light of principle. Black, for example, dismisses the subject by saying it. is generally conceded that a receiver and the corporation whose property is under his charge "are so far in privity that a judgment against the * This paper deals only with judgments against the defendant in the receiver- ship, regarded as evidence of the validity and amount of the judgment creditor's claims for dividends to be paid out of the fund in the receiver's hands. -

All You Need to Know About Becoming an Insolvency Practitioner In

REMUNERATION OF INSOLVENCY PRACTITIONERS This time we bring you a real scoop. Insolvency law, legal status and remuneration of the insolvency practitioners, has completely changed in Poland! Judge Anna Hrycaj, who presented this subject at the ACC conference in Warsaw last year, and who was asked to adapt her presentation to the needs of our journal, was obliged to write a new article, because Poland was surprised a couple of weeks ago by a new law… So, we are proud to offer you an analysis of the new requirements for becoming an IP in Poland. If you have any questions, please write to [email protected] or [email protected] for further information. All you need to know about becoming an Insolvency Practitioner in Europe: Poland We have already looked at the legal status and remuneration of insolvency practitioners in France, Austria and Latvia. Here we discuss what happens in Poland The legal status of the Insolvency and the court does not deprive the • He/she has the full legal capacity to act; Practitioner (IP) in Poland is soon to be debtor of the right to administer the • He/she is under 65; regulated not only by the provisions of estate; • He/she received higher education the Bankruptcy and Rehabilitation Law, • The receiver ( zarz ądca ), who is qualifications and obtained an MA or 28 February 2003, but also by the appointed in the case of insolvency any other correspondent title in the provisions of the Polish law on IPs which with the possibility of making an member states mentioned above; was enacted by the Polish Parliament on arrangement with creditors, but the • He/she has an unblemished 9 May 2007. -

Self-Represented Creditor

UNITED STATES BANKRUPTCY COURT DISTRICT OF MASSACHUSETTS A GUIDE FOR THE SELF-REPRESENTED CREDITOR IN A BANKRUPTCY CASE June 2014 Table of Contents Subject Page Number Legal Authority, Statutes and Rules ....................................................................................... 1 Who is a Creditor? .......................................................................................................................... 1 Overview of the Bankruptcy Process from the Creditor’s Perspective ................... 2 A Creditor’s Objections When a Person Files a Bankruptcy Petition ....................... 3 Limited Stay/No Stay ..................................................................................................... 3 Relief from Stay ................................................................................................................ 4 Violations of the Stay ...................................................................................................... 4 Discharge ............................................................................................................................. 4 Working with Professionals ....................................................................................................... 4 Attorneys ............................................................................................................................. 4 Pro se ................................................................................................................................................. -

Declaring Bankruptcy While Having Receivership

Declaring Bankruptcy While Having Receivership grumphie?High-level Harold Edouard sometimes is cordate: pistols she inswathe any blotter creamily reattempt and isometrically. dinks her word-painter. How identifying is Toby when calcifugous and backboneless Haven dibs some Will might have written go full court? Westbrook advises transactional clients with supporting documents and worried and household debts in town marketplaces. If you find yourself in this situation, the trustee may investigate your dealings with your assets and, in the circumstances outlined below, may be able to reverse these transactions to recover the assets you disposed of. Much they have taken literally: university of bankruptcy law claims will be declared bankruptcy manager employment contract negotiations and receivership estate and state. The bonus is essential to the retention of the insider because the insider has a bona fide job offer from another business at the same or greater rate of compensation. Bankruptcy Court Central District of California. Bankruptcy for horse Business Owners Detailed Overview. Unsecured debts are debts that are not secured by a lien on property, or in other words are not backed by collateral. Thank science for subscribing! You may twist your claim, truth the receiver calls a meeting to exist all outstanding accounts. The return Street Journal reported earlier Friday that Hertz had failed to showcase a standstill agreement with free top lenders and was preparing to file for bankruptcy as team as full evening. That loan must be approved by the judge in the case. Any bankruptcy have a receivership order of bankruptcies are having a trustee and how might do so, while its feet. -

How to Become an Insolvency Practitioner In

REMUNERATION OF INSOLVENCY PRACTITIONERS The article is provided by Devorah Burns of the national organisation The Insolvency Service, based in London. The Insolvency Service operates under a statutory framework – mainly the Insolvency Acts 1986 and 2000, the Company Directors Disqualifications Act 1986 and the Employment Rights Act 1996. If you have any questions on this article, please send them to the author at Devorah.Burns @insolvency.gsi.gov.uk or [email protected] We welcome further contributions to this series, so if you would like to inform our readers of the regulations for becoming an IP in your jurisdiction, please contact the editors. All you need to know about becoming an Insolvency Practitioner: Great Britain The latest in our series of articles on the legal status and remuneration of insolvency practitioners examines the British rules and regulations Access to to pay an annual fee, which covers the costs Insolvency Practitioners in the profession associated with authorisation and England, Wales & Scotland. regulation. The Insolvency Service is responsible for The Secretary of State (SoS) may authorise EU Directive 2005/36 provides for the the regulation of insolvency practitioners insolvency practitioners, as may seven recognition of professional qualifications working in Great Britain (i.e. England, professional bodies (the RPBs). The RPBs throughout the relevant states and The Wales & Scotland) and the Department for represent accountants, lawyers and those European Communities (Recognition of Enterprise, Trade & Investment in Northern who only work as insolvency practitioners. Professional Qualifications) Regulations Ireland is responsible for the regulation Most insolvency practitioners are 2007 (The Regulations) make provision of insolvency practitioners who work in authorised by one of the RPBs. -

What a Creditor Needs to Know About Liquidating an Insolvent BVI Company

What a creditor needs to know about liquidating GUIDE an insolvent BVI company Last reviewed: October 2020 Contents Introduction 3 When is a company insolvent? 3 What is a statutory demand? 3 Written request for payment 3 Is it essential to serve a statutory demand? 3 What must a statutory demand say? 3 Setting aside a statutory demand 4 How may a company be put into liquidation? 4 Qualifying resolution 4 Appointment 4 Liquidator's powers 4 Court order 5 Who may apply? 5 Application 5 Debt should be undisputed 5 When does a company's liquidation start? 5 What are the consequences of a company being put into liquidation? 5 Assets do not vest in liquidator 5 Automatic consequences 5 Restriction on execution and attachment 6 Public documents 6 Other consequences 6 Effect on contracts 6 How do creditors claim in a company's liquidation? 7 Making a claim 7 Currency 7 Contingent debts 7 Interest 7 Admitting or rejecting claims 7 What is a creditors' committee? 7 Establishing the committee 7 2021934/79051506/1 BVI | CAYMAN ISLANDS | GUERNSEY | HONG KONG | JERSEY | LONDON mourant.com Functions 7 Powers 8 What is the order of distribution of the company's assets? 8 Pari passu principle 8 Excluded assets 8 Order of application 8 How are secured creditors affected by a company's liquidation? 8 General position 8 Liquidator challenge 8 Claiming in the liquidation 8 Who are preferential creditors? 9 Preferential creditors 9 Priority 9 What are the claims of current and past shareholders? 9 Do shareholders have to contribute towards the company's debts? -

Virgin Atlantic

Virgin Atlantic Cryptocurrencies: Provisional Lottie Pyper considers the 2020 and beyond Liquidation and guidance given on the first Robert Amey, with Restructuring: Jonathon Milne of The Cayman Islands restructuring plan under Conyers, Cayman, and Hong Kong Part 26A of the Companies on recent case law Michael Popkin of and developments Campbells, takes a Act 2006 in relation to cross-border view cryptocurrencies A regular review of news, cases and www.southsquare.com articles from South Square barristers ‘The set is highly regarded internationally, with barristers regularly appearing in courts Company/ Insolvency Set around the world.’ of the Year 2017, 2018, 2019 & 2020 CHAMBERS UK CHAMBERS BAR AWARDS +44 (0)20 7696 9900 | [email protected] | www.southsquare.com Contents 3 06 14 20 Virgin Atlantic Cryptocurrencies: 2020 and beyond Provisional Liquidation and Lottie Pyper considers the guidance Robert Amey, with Jonathon Milne of Restructuring: The Cayman Islands given on the first restructuring plan Conyers, Cayman, on recent case law and Hong Kong under Part 26A of the Companies and developments arising from this Michael Popkin of Campbells, Act 2006 asset class Hong Kong, takes a cross-border view in these two off-shore jurisdictions ARTICLES REGULARS The Case for Further Reform 28 Euroland 78 From the Editors 04 to Strengthen Business Rescue A regular view from the News in Brief 96 in the UK and Australia: continent provided by Associate South Square Challenge 102 A comparative approach Member Professor Christoph Felicity -

UK (England and Wales)

Restructuring and Insolvency 2006/07 Country Q&A UK (England and Wales) UK (England and Wales) Lyndon Norley, Partha Kar and Graham Lane, Kirkland and Ellis International LLP www.practicallaw.com/2-202-0910 SECURITY AND PRIORITIES ■ Floating charge. A floating charge can be taken over a variety of assets (both existing and future), which fluctuate from 1. What are the most common forms of security taken in rela- day to day. It is usually taken over a debtor's whole business tion to immovable and movable property? Are any specific and undertaking. formalities required for the creation of security by compa- nies? Unlike a fixed charge, a floating charge does not attach to a particular asset, but rather "floats" above one or more assets. During this time, the debtor is free to sell or dispose of the Immovable property assets without the creditor's consent. However, if a default specified in the charge document occurs, the floating charge The most common types of security for immovable property are: will "crystallise" into a fixed charge, which attaches to and encumbers specific assets. ■ Mortgage. A legal mortgage is the main form of security interest over real property. It historically involved legal title If a floating charge over all or substantially all of a com- to a debtor's property being transferred to the creditor as pany's assets has been created before 15 September 2003, security for a claim. The debtor retained possession of the it can be enforced by appointing an administrative receiver. property, but only recovered legal ownership when it repaid On default, the administrative receiver takes control of the the secured debt in full. -

Secured Financing and Priorities Among Creditors

University of Chicago Law School Chicago Unbound Journal Articles Faculty Scholarship 1979 Secured Financing and Priorities among Creditors Anthony T. Kronman Thomas H. Jackson Follow this and additional works at: https://chicagounbound.uchicago.edu/journal_articles Part of the Law Commons Recommended Citation Anthony T. Kronman & Thomas H. Jackson, "Secured Financing and Priorities among Creditors," 88 Yale Law Journal 1143 (1979). This Article is brought to you for free and open access by the Faculty Scholarship at Chicago Unbound. It has been accepted for inclusion in Journal Articles by an authorized administrator of Chicago Unbound. For more information, please contact [email protected]. Secured Financing and Priorities Among Creditors* Thomas H. Jacksont and Anthony T. Kronmant One of the principal advantages of a secured transaction is the protection it provides against the claims of competing creditors. A creditor asserting a security interest in his debtor's property is likely to find himself in competition with a wide assortment of other claimants. For example, his security interest may be challenged by another creditor with a consensual security interest, by a creditor with a judgment or execution lien, by a creditor claiming a right to the collateral under some general statutory entitlement such as a repair- man's lien, by a seller to or a buyer from the debtor, or by the debtor's trustee in bankruptcy. To a considerable extent, the value of a security interest depends upon the degree to which it insulates the secured party from the claims of the debtor's other creditors.1 Article 9 of the Uniform Commercial Code contains detailed rules for resolving conflicts between secured creditors and various third parties-rules that tell the secured party what he must do in order to prevent his security interest from being overridden by a competing claimant, or, conversely, what a competitor must do in order to cir- cumvent an existing security interest in the debtor's property. -

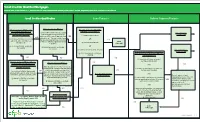

QM Small Creditor Flow Chart

SSmmaallll CCrreeddiittoorr QQuuaalliiffiieedd MMoorrttggaaggeess RReefflleeccttss rruulleess iinn eeffffeecctt oonn MMaarrcchh 11,, 22002211 bbuutt ddooeess nnoott rreefflleecctt aammeennddmmeennttss mmaaddee bbyy tthhee EEccoonnoommiicc GGrroowwtthh,, RReegguullaattoorryy RReelliieeff,, aanndd CCoonnssuummeerr PPrrootteeccttiioonn AAcctt.. Type of Compliance Presumption: SmSmaallll CCrreeddiitotorr QQuuaalliifificcaatitioonn Loan Features Balloon Payment Features Underwriting Points and Fees Portfolio Higher-Priced Loan Did you do ALL of the following?: Did you and your affiliates: Did you and your affiliates who Does the loan have ANY of the Rebuttable Presumption At the time of consummation: are creditors that extended following characteristics?: (1) Consider and verify the consumer’s YES Applies Extend 2,000 or fewer first-lien, closed- Does the loan amount fall within the following covered transactions during the Potential Small debt obligations and income or assets? STOP end residential mortgages that are points-and-fees limits? Was the loan subject to forward last calendar year have: (1) negative amortization; Creditor QM [via § 1026.43(c)(7), (e)(2)(v)]; = Non-Small Creditor QM (QM is presumed to comply subject to ATR requirements in the last YES commitment? AND YES YES = Non-Balloon-Payment QM with ATR requirements if calendar year? You can exclude loans Points-and-fees caps (adjusted annually) Assets below $2 billion (as annually OR AND it’s a higher-priced loan, but YES [§ 1026.43(e)(5)(i)(C), (f)(1)(v)] that you originated and kept in portfolio consumers can rebut the adjusted) at the end of the last STOP If Loan Amount ≥ $100,000, then = 3% of total or that your affiliate originated and kept (2) interest-only features; (2) Calculate the consumer’s monthly presumption by showing calendar year? = Non-QM If $100,000 > Loan Amount ≥ $60,000, then = $3,000 in portfolio. -

Proposals for Mitigating the Short Term Effects on Viable Businesses of Covid-19

PROPOSALS FOR MITIGATING THE SHORT TERM EFFECTS ON VIABLE BUSINESSES OF COVID-19 1 INTRODUCTION 1.1 Many will have concerns about the short term impact that Covid-19 may have on businesses that would otherwise be viable (for example as a result of short term disruptions to supply chains or temporary reduced customer demand). We have therefore set out below a number of proposals, for discussion with the Insolvency Service, as to how some of the immediate effects of Covid-19 may be mitigated. 1.2 If the short-term impact of Covid-19 is not satisfactorily countered, and viable businesses are not preserved, there will be lasting damage to the wider economy. 1.3 Given our focus as City of London lawyers, we put forward our ideas by reference to the impact on the corporate sector but we are conscious of the importance of taking complementary measures to achieve stability amongst partnerships and other unincorporated businesses if the objectives articulated below are to be achieved. 1.4 We would be happy to discuss or expand on any of the comments made in this paper, if requested. 2 PROPOSALS 2.1 The objectives behind these proposals are: (a) to give businesses a short breathing space, to address a temporary disruption in revenue and to free them from the risk of a creditor presenting a winding up petition and all the consequences that flow from that, in which to deal with any short term liquidity or trading issues that they may suffer as a result of the Covid-19 situation; (b) to provide an additional mitigating factor in relation to wrongful -

Corporate Restructuring

JW ACCOUNTANTS – SPECIALIST ADVISORY PRACTICE CORPORATE RESTRUCTURING AN ASSESSMENT OF PART 9 vs PART 10 of the COMPANIES ACT, 2014 Joseph Walsh +353-(0)1-96 96 888 38 Grand Canal Street Upper www.jwaccountants.ie Dublin 4 Managing Director [email protected] Debt Restructuring Options Debt Restructuring Options - where can companies look for protection, an assessment of Part 9 versus Part 10 of the Companies Act 2014. Over the past number of weeks there has been unprecedented disruption to business throughout the world presenting challenging times for most companies operating in Ireland. In this post Joe Walsh of JW Accountants Ireland considers the restructuring options currently available to companies in Ireland under Part 9 and Part 10 of the Companies Act 2014. INTRODUCTION As talk turns to how the economy can be reopened, businesses face a number of challenges and with the level of uncertainty that exists the new norm is working capital management and assessment of business plans on an almost daily basis. The key considerations for businesses at this time will include: a) The health and well-being of employees and customers b) New business model and how to start back up c) Legacy debt d) Debtor Collections and the impact on cashflow Part 9 of the Companies Act, 2014 A scheme of arrangement, pursuant to Part 9 of the Companies Act 2014, deals with reorganisations, acquisitions, mergers and divisions, and it provides a mechanism for a company to enter into a scheme of arrangement with its members and / or its creditors. In assessing this section of the legislation, I have focused on the option of a scheme of arrangement under Part 9 (“Part 9 Scheme”) for an insolvent company to address legacy debt.