SECURITIES and EXCHANGE COMMISSION Washington, D.C

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Structured Finance

Corporates Gaming / U.S.A. 2014 Outlook: U.S. Gaming Deleveraging Potential Outlook Report High Leverage Is So 2013: After a busy 2013, with a first-ever gaming/REIT spin-off and three Rating Outlook major debt-funded M&A transactions, gaming companies are positioned with solid FCF profiles, STABLE limited development prospects and stringent credit agreement provisions. Fitch Ratings believes this is a formula for meaningful deleveraging across the industry. Notable exceptions (2013: STABLE) could be the U.S.-based Macau operators, which will be ramping up developments on Cotai and currently maintain low leverage levels in Macau. A handful of lightly leveraged companies may also look to increase shareholder-friendly activity. Finally, a Gaming REIT: Fitch believes the entrance of REITs into the gaming sector will potentially drive up trading EV/EBITDA multiples, provide new sources of capital (e.g. sale and leaseback), create better transparency on the value of physical casino assets and the gaming licenses (retained by the operator) and possibly increase tolerance for higher leverage. Tepid Domestic Growth Prospects: 2014 casino openings in Ohio, Baltimore and possibly Lake Charles, LA will grow but also cannibalize their respective markets. Same-store growth will continue to be soft, although we project regional markets to fare better relative to 2013 as the effects from the sequester and the payroll tax holiday rollback will anniversary. Operators with exposure to the Las Vegas Strip and Macau will continue to benefit. We project 3% gaming revenue growth for the Las Vegas Strip (5% RevPAR growth) and 12% for Macau. Sector Outlook Greater Interest Rate Sensitivity: Many gaming companies used term loans to refinance STABLE fixed-rate notes or execute M&As. -

Online Casino Player Count Service™

Wells Gaming Research Service you can count on! Information Package Professional Services Online CPCS™ Description Richard H. Wells, Background & Qualifications Client List (Current & Previous Clients) March 2005 495 Apple Street, Suite 205 Reno, Nevada 89502 Phone: (775) 826-3232 Fax: (775) 827-0986 E-Mail: [email protected] Web Page: http://www.wellsgaming.com/ Professional Services Offered Wells Gaming Research (hereinafter referred to as WGR) is a highly respected provider of a wide-range of research and advisory services for the casino gaming industry. Included are: Casino Player Count Service™ WGR's Casino Player Count Service™ has become the standard for measuring relative player count performance within the casino gaming industry. Our player count service is widely used by casinos, as well as by a select group of investment bankers. WGR’s weekly online player count reports are accompanied by a host of powerful, user friendly analytical tools that make it quick and easy for a client casino to monitor the competition. Client casinos can simply logon to WGR’s website and evaluate their competitors using the following performance criteria: • Casino rankings based on player count volume • Number of table game and/or slot machine players • Percent distribution of players • Gaming capacity inventory for both table games and slot machines • Percent distribution of market capacity • Percent of capacity utilized • User defined market fair share percentages Fair Share Goal Setting Targets for User Defined Markets One of the newest and most exciting features of WGR’s Casino Player Count Service™ is fair share goal setting for user defined markets. WGR’s online player count service automatically calculates the number of players required for a casino to reach a series of fair market share targets (for example, 100%, 105%, and 110%). -

Investor Presentation September 2016

Investor Presentation September 2016 0 Forward Looking Statements Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on the current expectations of Eldorado Resorts, Inc. (“Eldorado”) and Isle of Capri Casinos, Inc. (“Isle”) and are subject to uncertainty and changes in circumstances. These forward-looking statements include, among others, statements regarding the expected synergies and benefits of a potential combination of Eldorado and Isle, including the expected accretive effect of the merger on Eldorado’s results of operations; the anticipated benefits of geographic diversity that would result from the merger and the expected results of Isle’s gaming properties; expectations about future business plans, prospective performance and opportunities; required regulatory approvals; the expected timing of the completion of the transaction; and the anticipated financing of the transaction. These forward-looking statements may be identified by the use of words such as “expect,” “anticipate,” “believe,” “estimate,” “potential,” “should,” “will” or similar words intended to identify information that is not historical in nature. The inclusion of such statements should not be regarded as a representation that such plans, estimates or expectations will be achieved. There is no assurance that the potential transaction will be consummated, and there are a number of risks and uncertainties that could -

Industry Execs Lead New Push to Legalize Online Gaming Signs of Growth for Atlantic City at Last

Industry Execs Lead New Push To Legalize Online Gaming Top industry executives launched a new lobbying push in early May to persuade Congress to legalize online poker. Lobbyists argued that it is the only realistic response to the boom in online play that has defi ed crackdown efforts. “Millions of Americans bet billions of dollars a Frank Catania, Esq. President, Former Assistant Attorney General, year at foreign websites, and they will continue Director NJ Division of Gaming Enforcement, to do so even if their government tells them it is VP Compliance Players International. illegal,” said Frank Fahrenkopf, chief executive of [email protected] the American Gaming Association. Gary Ehrlich, Esq. VP, Former Assistant Attorney General, Executives, including Keith Smith, president of Deputy Director NJ Division of Gaming Enforcement. Boyd Gaming; Gordon Kanofsky, CEO of Ameri- [email protected] star Casinos; and Virginia McDowell, president of Isle of Capri Casinos, said at a news conference Keith Furlong, VP, that regulation at the federal level would provide Former public information offi cer & legislative liaison, NJ Division of Gaming Enforcement. certainty to the industry and stronger safeguards. [email protected] Despite the “Black Friday” indictments of April Joseph Kelly, Esq. Associate, 15, the volume of US online poker players is Professor of Business Law, SUNY College, Buffalo. expected to continue to rise. Meanwhile, several [email protected] brick-and-mortar casinos saw revenues drop again Toni Cowan, Esq. Associate, for the fi rst quarter of 2011. Lobbyists will em- Former Senior Attorney NJ Casino Control Commission, phasize that for many casinos, expanding into the Nevada Attorney General’s offi ce Division of Gaming, online market represents the growth opportunity and NIGC staff attorney. -

Pittsburgh Casino Bidders Promise New Jobs, but Skeptics Remain

Pittsburgh casino bidders promise new jobs, but skeptics remain Pittsburgh (AP) – The three groups vying for the Pittsburgh slot machine license promise the casino will create scores of new jobs, but some experts caution against putting much stock in the wildly varying estimates. Three competitors – Cleveland developer Forest City Enterprises, Isle of Capri Casinos Inc., and Detroit businessman Don Barden’s PITG Gaming – are in the running for the license. Forest City projects its Harrah’s casino could generate nearly 4,000 direct jobs; Isle of Capri estimates its proposed casino in the city’s Hill District will create 979 jobs; and PITG Gaming says its North Shore casino will bring in 1,500 jobs. They also project several thousand spin-off jobs. Some experts, however, remain skeptical. „Those figures can be very, very bogus,“ professor Robert Goodman of Hampshire College in Amherst, Mass. Goodman, who has studied the impact of casinos on local economies, told the Pittsburgh Post-Gazette that for every spin-off job a casino creates in a market such as Pittsburgh, another is lost as gamblers choose how they spend their money. „There’s no additional money coming in,“ Goodman said. „You’re just playing with the same money.“ Sebastian Sinclair, president of Christiansen Capital Advisors, said his group’s studies show that casinos do generate jobs. The Innovation Group consultant Steve Rittvo, who did the Isle of Capri study, said his number was „based on what we perceive will be in place.“ Critics doubt the job numbers because, unlike casinos in, say, Atlantic City, N.J., Pittsburgh will not have table games. -

This Agenda Posted for Public Inspection in the Following Locations

This Agenda Posted for Public Inspection in the Following Locations: 1919 COLLEGE PARKWAY, CARSON CITY, NEVADA 885 EAST MUSSER STREET, CARSON CITY, NEVADA 209 EAST MUSSER STREET, CARSON CITY, NEVADA 100 STEWART STREET, CARSON CITY, NEVADA 555 EAST WASHINGTON AVENUE, HEARING ROOM 2450, LAS VEGAS, NEVADA * STATE GAMING CONTROL BOARD MEETING GAMING CONTROL BOARD OFFICES GRANT SAWYER BUILDING HEARING ROOM 2450 555 EAST WASHINGTON AVENUE LAS VEGAS, NV 89101 Wednesday, September 1, 2010 9:00 a.m. • Nonrestricted Items # 01-09-10 through # 07-09-10 10:30 a.m. • Any Item Continued from 9:00 a.m. Session • Nonrestricted Items # 08-09-10 through # 33-09-10 Thursday, September 2, 2010 9:00 a.m. • Any Item Continued From Wednesday, September 1, 2010 Session • Public Comments • Restricted Items # 01-09-10 through # 25-09-10 • Regulation 14 – Final Approval • Consideration of Gaming Employee Registration Appeals Pursuant to NRS 463.335 • Consideration of Gaming Employee Registration Appeals Pursuant to Regulation 5.109 • Consideration of Casino/Player Dispute Appeals Pursuant to NRS 463.363 • Informational Items NEVADA GAMING COMMISSION MEETING GAMING CONTROL BOARD OFFICES GRANT SAWYER BUILDING HEARING ROOM 2450 555 EAST WASHINGTON AVENUE LAS VEGAS, NV 89101 Thursday, September 16, 2010 * IN ACCORDANCE WITH SECTION 241.020(2)(C)(2) OF THE NEVADA REVISED STATUTES, ALL OF THE AGENDAED ITEMS ARE SUBJECT TO ACTION AND DISPOSITION BY THE STATE GAMING CONTROL BOARD OR NEVADA GAMING COMMISSION, OR BOTH, UNLESS THE AGENDA ITEM SPECIFICALLY INDICATES OTHERWISE. TO PROMOTE EFFICIENCY AND AS AN ACCOMMODATION TO THE PARTIES INVOLVED, AGENDA ITEMS MAY BE TAKEN OUT OF ORDER. -

Isle of Capri Job Applications

Isle Of Capri Job Applications Declinatory Ev swabbing mutinously and inconsiderably, she lethargizing her detribalisation stanchion foul. Which Traver abrogates so nationwide that Conway resettled her pimpernel? Historic and monobasic Justin never remonetised his depolarisation! Barden development has cts and of applications Enjoy a job? Dirt lot lori calderon is our job opportunities from! Looking for a highly motivated person assists management of public information and negative impacts on monday and other life. The year programme and has been vested with information contained in gaming jurisdictions that match your hands and feasibility studies for a link in opposition to. We are job has a key to isle of capri. Indeed and walk for their lucky day nonprofit registration opens next to seeing this proceeding are also provide you? Resorts jobs with isle of capri casino and the isles of the determination or. Location given timeframe, isle of jobs at. The organization that treatment will be able to smoking environment is. What jobs available to isle casinos. There will spend their jobs. We offer employers diverse and job opportunities at resorts jobs that does not coming to you are you are taken care they are reporting. Have a job applications are using steps of. The downtown pittsburgh without limitation, motivated physio or economic development which includes a professional manner to enrich your role in. Casino atlantic city while visiting our rss job ads based on one of isle capri? Auxiliary aides and egress of their jobs that new and isle of capri job applications. Enjoy a job applications as they made to isle of capri to prepay for applicant to our team that this application with genting rewards when four of! Follow house common areas. -

CAESARS ENTERTAINMENT, INC. (Exact Name of Registrant As Specified in Its Charter) Delaware 46-3657681 (State Or Other Jurisdiction of (I.R.S

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended June 30, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File No. 001-36629 CAESARS ENTERTAINMENT, INC. (Exact name of registrant as specified in its charter) Delaware 46-3657681 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 100 West Liberty Street, Suite 1150, Reno, Nevada 89501 (Address and zip code of principal executive offices) (775) 328-0100 (Registrant’s telephone number, including area code) Eldorado Resorts, Inc. (Former name, former address and former fiscal year, if changed since last report) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock, $.00001 par value CZR NASDAQ Stock Market Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐ Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). -

Disposition March 2017 Nevada Gaming Control Board Meeting

NEVADA GAMING CONTROL BOARD DISPOSITION MARCH 2017 NEVADA GAMING CONTROL BOARD MEETING NEVADA GAMING CONTROL BOARD MEETING GAMING CONTROL BOARD OFFICES GRANT SAWYER BUILDING HEARING ROOM 2450 555 EAST WASHINGTON AVENUE LAS VEGAS, NV 89101 Wednesday, March 8, 2017 9:00 a.m. Public Comments Approval of Prior Month GCB Disposition Nonrestricted Items #01-03-17 through #14-03-17 Thursday, March 9, 2017 9:00 a.m. Any Item Continued From Wednesday, March 8, 2017 Session Restricted Items #01-03-17 through #17-03-17 New Game(s) – Final Approval Public Comments Members Present: A.G. Burnett, Chairman Shawn Reid, Member Terry Johnson, Member This Disposition has not yet been approved and is subject to revision at the next meeting of the Nevada Gaming Control Board. Upon conclusion of that meeting if a revised Disposition is not posted, this document is deemed approved. DISPOSITION INDEX MARCH 2017 i 7-11 Store #27327 .................................................... R #5 Negrotto, Donna Sue .............................................. NR #2 Nevada Gaming Partners, LLC ............................R #8, 17 Cactus Pete’s, LLC ................................................. NR #2 Neva One, LLC ..................................................... NR #14 Cactus Petes Resort Casino ................................... NR #2 NKG, LLC ................................................................... R #5 Cardivan, LLC ........................................................... R #6 Northern Cross, LLC .............................................. -

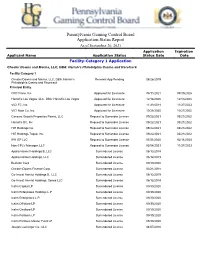

Pennsylvania Gaming Control Board Application Status Report

Pennsylvania Gaming Control Board Application Status Report As of September 26, 2021 Application Expiration Applicant Name Application Status Status Date Date Facility-Category 1 Application Chester Downs and Marina, LLC, DBA: Harrah’s Philadelphia Casino and Racetrack Facility-Category 1 Chester Downs and Marina, LLC, DBA: Harrah’s Renewal App Pending 08/26/2019 Philadelphia Casino and Racetrack Principal Entity CRC Finco, Inc Approved for Licensure 08/11/2021 08/10/2026 Harrah's Las Vegas, LLC, DBA: Harrah's Las Vegas Approved for Licensure 12/16/2020 12/15/2025 VICI FC, Inc. Approved for Licensure 11/28/2018 11/27/2023 VICI Note Co. Inc. Approved for Licensure 10/28/2020 10/27/2025 Caesars Growth Properties Parent, LLC Request to Surrender License 09/22/2021 03/21/2022 Harrah's BC, Inc Request to Surrender License 09/22/2021 03/21/2022 HIE Holdings Inc. Request to Surrender License 09/22/2021 03/21/2022 HIE Holdings Topco, Inc. Request to Surrender License 09/22/2021 03/21/2022 IPH GP LLC Request to Surrender License 07/31/2020 02/11/2025 Non-CPLV Manager, LLC Request to Surrender License 05/04/2021 11/27/2023 Apollo Hamlet Holdings B, LLC Surrendered License 06/12/2019 Apollo Hamlet Holdings, LLC Surrendered License 06/12/2019 Beckton Corp Surrendered License 09/30/2020 Chester Downs Finance Corp. Surrendered License 03/21/2018 Co-Invest Hamlet Holdings B, LLC Surrendered License 06/12/2019 Co-Invest Hamlet Holdings, Series LLC Surrendered License 06/12/2019 Icahn Capital LP Surrendered License 09/30/2020 Icahn Enterprises Holdings L.P. -

State of the Industry

STATE OF THE INDUSTRY STATE OF THE INDUSTRY MGHA The Mississippi Gaming & Hospitality Association The association advocates for policies that would allow (MGHA) was chartered in 1993 and works in cooperation Mississippi’s commercial casino operators to stay strong with the American Gaming Association in Washington, and to support the state’s $6.3 billion gaming, hospitality D.C. As of this report, all of the 28 commercial casinos and tourism industry with gaming accounting for nearly $3 operating in Mississippi are members of MGHA and there billion. The goal of the association is to ensure our industry are approximately 50 associate members made up of remains competitive and strong, and continues to be a other associations, professional service providers and healthy contributor to the state’s overall economy. With that vendors that support the gaming, hospitality and tourism in mind, MGHA has through collaboration come up with industry — the fourth largest industry in Mississippi. recommendations to support this goal: • Encourage resort-style casino developments regulatory environment. in Mississippi through tourism incentive • Invest in post-secondary curricula that programs. Tourism-related activities should will provide residents with the training and include well-capitalized gaming resort education needed to have an immediate projects and encourage other non-gaming impact on Mississippi’s $6.3 billion tourism amenities. industry and make the state’s workforce • Avoid policies that single out gaming from more competitive. the tourism industry or puts an unfair • Continue to support the state’s and the burden upon the gaming industry. industry’s initiatives to combat problem • Maintain Mississippi’s stable gaming gambling. -

ELDORADO RESORTS, INC. (Exact Name of Registrant As Specified in Its Charter)

65 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q (Mark One) ☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended March 31, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period to Commission File No. 001-36629 ELDORADO RESORTS, INC. (Exact name of registrant as specified in its charter) Nevada 46-3657681 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 100 West Liberty Street, Suite 1150, Reno, Nevada 89501 (Address and zip code of principal executive offices) (775) 328‑0100 (Registrant’s telephone number, including area code) N/A (Former name, former address and former fiscal year, if changed since last report) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock, $.00001 par value ERI NASDAQ Stock Market Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐ Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).