Tampa Bay Office Market Report First Quarter 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Outside Counsel Firm/Attorney/Consultant Address

Outside Counsel Firm/Attorney/Consultant Address City State Zip IES Company Name Role Type of Case Akin Gump Strauss 1111 Louisana Street, 44th Floor Houston TX 77002 Ron's Electric, Inc., dba IES - North Plains Defendant Employment Agreement Dispute Allen & Gooch 1015 St. John Street Lafayette LA 70501 IES New Iberia, Inc./ Ernest P. Breaux Defendant Wrongful Termination Allen and Gooch 1015 St. John Street/PO Drawer 3768 Lafayette LA 70502 IES New Iberia, Inc./ Ernest P. Breaux Defendant Property Damage Allen Martin & Blue 121 Majorca Ave., Suite 300 Coral Gables FL 33134 Daniel Electrical Contractors, Inc. Both Employment Agreement Dispute * Baker & McKenzie 2300 Trammell Crow Center Dallas TX 75201 Bryant Electric Comm. Dispute Bracewell & Patterson, LLP 711 Louisiana Street, Suite 2900 Houston TX 77002 Galbraith Electric Co., Inc. Defendant Property Damage Brazeale Sachese & Wilson LLP PO Box 3197 Baton Rouge LA 70821 Cypress Electrical Contractors, Inc. Plaintiff Collection Bugg & Wolf P. O. Box 2917 Durham NC 27715 Bryant Electric Both Comm. Dispute Burns Day & Presnell 2626 Glenwood Ave., Suite 560 Raleigh NC 27608 Houston-Stafford Electric Holdings III, Inc. Plaintiff Collection Canterbury Stuber Elder 5005 LBJ Freeway, Suite 1000 Dallas TX 75244 Pollock Summit Electric LP Defendant NLRB Carter & Ansley 191 Peachtree Tower Atlanta GA 30303 Mark Henderson, Incorporated Defendant Personal Injury * Chamberlain Hrdlicka 191 Peachtree Street North East, 9th Fl Atlanta GA 30303 Bryant Electric Company, Inc. Both Commercial Dispute Cheifetz, Iannitelli, Marcolini, PC 1850 N. Central Avenue Phoenix AZ 85004 Hatfield Reynolds Electric Company Both Collection Chrissinger & Baumberger Three Milll Road, Suite 301 Wilmington DE 19806 Primo Electric Company Defendant Property Damage DeCaro Doran Siciliano 4601 Forbes Blvd., Suite 200 Lanham MD 20703 ARC Electric, Incorporated Defendant Personal Injury, Property Damage Bryant Electric Company, Inc. -

Recommended By: __ Z

Agenda Item #: 3A-2 PALM BEACH COUNTY BOARD OF COUNTY COMMISSIONERS AGENDA ITEM SUMMARY Meeting Date: January 13, 2015 [x] Consent [ ] Regular [] Ordinance [] Public Hearing Department: Administration Submitted By: Legislative Affairs Submitted For: Legislative Affairs --------------------------------------------------------------------------- I. EXECUTIVE BRIEF Motion and Title: Staff recommends motion to approve: Five (5) consulting/professional service contracts for state lobbying services on behalf of Palm Beach County and in response to RFP No. 15-008/SC for the term of twelve months from January 13, 2015 to January 12, 2016 for a total amount of $175,000 as follows: A. A contract with Ericks Consultants, Inc. in the amount of $35,000; B. A contract with Foley and Lardner, LLP in amountthe of $35,000. C. A contract with Ron L. Book, P.A. in the amount of $35,000; D. A contract with Corcoran & Associates, Inc. dba Corcoran & Johnson in the amount of $35,000; E. A contract with The Moya Group, Inc. in the amount of $35,000; Summary: In December 2014, the State Lobbyist Services Selection Committee met to review nine proposals to RFP No. 15-008/SC, State Lobbying Services. The selection committee met on two occasions to rank and recommend to the Board of County Commissioners an award of contract of to up to six firms for state lobbying services. The committee recommended the five firms listed above for approval of individual lobbying contracts of $35,000 for a total of $175,000. No SBE firms submitted and the committee recommended continuing to seek participation of such firms in county lobbying services. -

Tampa CBD Commercial Office Real Estate Update

Tampa CBD Office Market Presented by Larry Richey HOW DO WE COMPARE? Tampa CBD vs Other Southeast CBD’s CBD Class A NASHVILLE CHARLOTTE Average $33.23 $32.25 Asking DALLAS / FORT WORTH $31.90 Rates ATLANTA $31.61 JACKSONVILLE $21.39 $54.52 ORLANDO AUSTIN TAMPA $26.55 $29.87 MIAMI $50.90 Cushman & Wakefield SO, WHERE IS THERE SPACE? Tampa Bay Snapshot Total Overall Inventory No. Overall Vacancy Direct Wtd. Average 43,677,108 SF Bldgs. Inventory Rate Rental Rates (psf) Tampa CBD 26 6,032,822 13.7% $26.93 Westshore 115 12,761,174 9.0% $27.57 Total Direct Weighted Northwest 87 4,339,742 11.8% $22.28 Average Rental Rate I-75 Corridor 85 7,515,700 15.1% $21.69 Southwest 10 360,126 18.8% $18.86 $23.82 Hyde Park 10 363,994 1.3% $23.77 Ybor City 5 207,399 6.0% $0.00 Class A Total Direct St. Petersburg CBD 21 2,054,997 13.1% $27.79 Gateway/Mid-Pinellas 76 4,537,299 15.2% $21.10 Weighted Average Bayside 21 1,454,626 10.2% $21.52 Rental Rate Countryside 22 1,204,976 14.0% $19.70 $26.35 North Pinellas 19 1,262,147 7.8% $19.59 Clearwater Downtown 12 702,597 15.3% $17.97 South St. Petersburg 19 879,509 12.1% $21.15 2 Cushman & Wakefield Tampa CBD Snapshot CLASS A OFFICE PROPOSED DEVELOPMENT SunTrust Financial Center The Heights 100 North Tampa Riverwalk Tower Bank of America Plaza Water Street Tampa City Center Rivergate Tower Wells Fargo Center One Harbour Place Two Harbour Place CLASS B OFFICE Park Tower Fifth Third Center 501 East Kennedy The Times Building Cushman & Wakefield Class A Properties SunTrust Bank of 100 Tampa Financial America North City -

Bankruptcy Forms

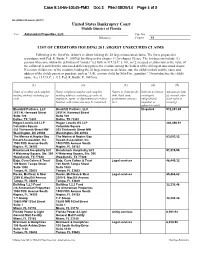

Case 9:14-bk-10145-FMD Doc 13 Filed 08/29/14 Page 41 of 92 B4 (Official Form 4) (12/07) United States Bankruptcy Court Middle District of Florida In re Antaramian Properties, LLC. Case No. Debtor(s) Chapter 11 LIST OF CREDITORS HOLDING 20 LARGEST UNSECURED CLAIMS Following is the list of the debtor's creditors holding the 20 largest unsecured claims. The list is prepared in accordance with Fed. R. Bankr. P. 1007(d) for filing in this chapter 11 [or chapter 9] case. The list does not include (1) persons who come within the definition of "insider" set forth in 11 U.S.C. § 101, or (2) secured creditors unless the value of the collateral is such that the unsecured deficiency places the creditor among the holders of the 20 largest unsecured claims. If a minor child is one of the creditors holding the 20 largest unsecured claims, state the child's initials and the name and address of the child's parent or guardian, such as "A.B., a minor child, by John Doe, guardian." Do not disclose the child's name. See 11 U.S.C. § 112; Fed. R. Bankr. P. 1007(m). (1) (2) (3) (4) (5) Name of creditor and complete Name, telephone number and complete Nature of claim (trade Indicate if claim is Amount of claim mailing address including zip mailing address, including zip code, of debt, bank loan, contingent, [if secured, also code employee, agent, or department of creditor government contract, unliquidated, state value of familiar with claim who may be contacted etc.) disputed, or security] subject to setoff Blackhill Partners, LLC Blackhill Partners, LLC Disputed 512,291.45 2651 N. -

LGTW ECO Contributions

Date Contributor Name Address City State Zip Occupation Amount 6/24/2010 F. ANNETTE SCOTT REVOCABLE TRUST ACCOUNT 1400 GULF SHORE BLVD STE 148 NAPLES, FL 34102 SELF EMPLOYED $ 2,000,000.00 6/28/2010 GOTTSEGER PETER M. 136 BEDFORD ROAD POUND RIDGE, NY 10576 INVESTOR $ 2,500.00 6/28/2010 DANIELS L.B. 100 EVERGLADES AVENUE PALM BEACH, FL 33480 INVESTOR $ 25,000.00 6/28/2010 SCHMEELK RICHARD J. 160 VIA DEL LAGO PALM BEACH, FL 33480 FINANCIAL ADVISOR $ 2,500.00 6/28/2010 PALM BEACH HEALTH ASSOCIATES INC. 1590 SOUTH CONGRESS AVENUE WEST PALM BEACH, FL 33406 HEALTH CARE $ 10,000.00 6/28/2010 SALAZAR BARBARA C. 5790 SW 97TH STREET PINECREST, FL 33156 CONSULTANT $ 20,000.00 6/28/2010 ATLANTIS PHYSICIAN GROUP 4960 SW 72ND AVENUE STE 406 MIAMI, FL 33155 HEALTH CARE $ 10,000.00 6/28/2010 PRIMARY CARE SPECIALISTS OF THE PALM BEACHES 6701 SOUTH DIXIE HIGHWAY WEST PALM BEACH, FL 32405 HEALTH CARE $ 10,000.00 6/28/2010 JV-CAM LLC 3191 CORAL WAY STE 303 MIAMI, FL 33155 SOFTWARE DEVELOPER $ 1,500.00 6/28/2010 PHYSICIAN CONSORTIUM SERVICES LLC 3191 CORAL WAY STE 303 MIAMI, FL 33145 HEALTH CARE $ 2,000.00 6/28/2010 MCCI GROUP HOLDINGS LLC 4960 SW 72ND AVENUE STE 406 MIAMI, FL 33155 SOFTWARE DEVELOPER $ 10,000.00 6/28/2010 TEAL BRUCE 112 HIDDEN POINT HENDERSONVILLE, TN 37075 HEALTH CARE EXECUTIV $ 300.00 7/2/2010 F. ANNETTE SCOTT REVOCABLE TRUST ACCOUNT 1400 GULF SHORE BLVD STE 148 NAPLES, FL 34102 SELF EMPLOYED $ 3,000,000.00 7/16/2010 F. -

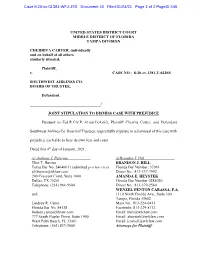

Joint Stipulation to Dismiss Case with Prejudice

Case 8:20-cv-01381-WFJ-JSS Document 46 Filed 01/04/21 Page 1 of 2 PageID 449 UNITED STATES DISTRICT COURT MIDDLE DISTRICT OF FLORIDA TAMPA DIVISION CHERRITA CARTER, individually and on behalf of all others similarly situated, Plaintiff, v. CASE NO.: 8:20-cv-1381-T-02JSS SOUTHWEST AIRLINES CO. BOARD OF TRUSTEE, Defendant. ____________________________________/ JOINT STIPULATION TO DISMISS CASE WITH PREJUDICE Pursuant to Fed.R.Civ.P. 41(a)(1)(A)(ii), Plaintiff Cherrita Carter, and Defendant Southwest Airlines Co. Board of Trustees, respectfully stipulate to a dismissal of this case with prejudice, each side to bear its own fees and costs. Dated this 4th day of January, 2021. /s/ Anthony J. Palermo /s/Brandon J. Hill Eliot T. Burriss BRANDON J. HILL Texas Bar No. 24040611 (admitted pro hac vice) Florida Bar Number: 37061 [email protected] Direct No.: 813-337-7992 200 Crescent Court, Suite 1600 AMANDA E. HEYSTEK Dallas, TX 75201 Florida Bar Number 0285020 Telephone: (214) 964-9500 Direct No.: 813-379-2560 WENZEL FENTON CABASSA, P.A. and 1110 North Florida Ave., Suite 300 Tampa, Florida 33602 Lindsey R. Camp Main No.: 813-224-0431 Florida Bar No. 84138 Facsimile: 813-229-8712 [email protected] Email: [email protected] 777 South Flagler Drive, Suite 1900 Email: [email protected] West Palm Beach, FL 33401 Email: [email protected] Telephone: (561) 833-2000 Attorneys for Plaintiff Case 8:20-cv-01381-WFJ-JSS Document 46 Filed 01/04/21 Page 2 of 2 PageID 450 and Anthony J. Palermo Florida Bar No. -

United States Bankruptcy Court Middle District of Florida Fort Myers Division

UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA FORT MYERS DIVISION In re: Chapter 11 VICTOR G. MELLOR, Case No. 9:10-bk-20398-DHA COLONIAL CONSTRUCTION Case No. 9:10-bk-28157-DHA COMPANY, INC., COLONIAL READY MIX, LLC, Case No. 9:10-bk-28160-DHA CCC TRUCKING, LLC, Case No. 9:10-bk-28161-DHA Debtors. (Jointly Administered under / Case No. 9:10-bk-20398-DHA) Emergency Hearing Requested for December 16, 2010 at 10:30 a.m. EMERGENCY MOTION OF COLONIAL CONSTRUCTION COMPANY, INC., COLONIAL READY MIX, LLC, AND CCC TRUCKING, LLC FOR ENTRY OF AN ORDER (A) AUTHORIZING THE SALE OF SUBSTANTIALLY ALL OF THE ASSETS OWNED BY DEBTORS COLONIAL CONSTRUCTION COMPANY, INC., COLONIAL READY MIX, LLC, AND CCC TRUCKING, LLC, FREE AND CLEAR OF LIENS, CLAIMS AND ENCUMBRANCES PURSUANT TO 11 U.S.C. § 363; (B) ESTABLISHING BID PROCEDURES AND SALE PROCESS; (C) APPROVING ASSET PURCHASE AGREEMENT; (D) APPROVING FORM AND MANNER OF NOTICES; (E) SCHEDULING AUCTION AND FINAL SALE APPROVAL HEARING; (F) AUTHORIZING THE REJECTION OF CERTAIN EXECUTORY CONTRACTS AT THE SALE HEARING AND AUTHORIZING THE ASSUMPTION AND ASSIGNMENT OF OTHERS; AND (G) GRANTING RELATED RELIEF Colonial Construction Company, Inc. (“Colonial”), Colonial Ready Mix, LLC (“Ready Mix”), and CCC Trucking, LLC (“CCC Trucking”, collectively with Colonial and Ready Mix, the “Debtors” or “Corporate Debtors”), by and through their undersigned counsel, and pursuant to 11 U.S.C. §§ 105, 363 and 365, Fed. R. Bank. P. 2002, 6004, 6006, and 9014 and Local Rules 2002-1, 6004-1, and 9014-1, move the Court for entry of an order: A. -

Hillsborough County Follow the Leaders

( Community Portrait ) Tampa Hillsborough County Follow the Leaders. Follow Florida Trend. Follow the 250,000 business, government and civic leaders who rely on Florida Trend each month to deliver the latest news items and developing trends in Florida business. Why not join them at a special introductory subscription rate? www.FloridaTrend.com/subscribe ( Tampa/Hillsborough County ) T rend Florida www.FloridaTrend.com A Word from the Publisher Publisher Andrew P. Corty Executive Editor Mark R. Howard Welcome to Florida Trend’s special Deputy Publisher David G. Denor report on Tampa and Hillsborough County. In this e-zine format, you’ll see the full EDITORIAL Managing Editor John Annunziata Community Portrait that was featured in South Florida Editor Mike Vogel our November 2017 issue. Associate Editors Jason Garcia, The Tampa region is a vital segment of Art Levy, Amy Martinez the Florida economy — population here Restaurant Editor Chris Sherman Contributors Mark Basch, totals more than 1. 3 million, the fourth Rochelle Broder-Singer, Carlton Proctor most populous in Florida. Hillsborough ART is proudly diverse with more than half Art Director Gary Bernloehr defining themselves as Caucasian and Associate Art Director Jason Morton the remainder divided among those with N aturally, Tampa has major league sports ADMINISTRATION African, Asian or Hispanic origin. — football’s Buccaneers play here as do the Business Manager Barbara Goodman Hillsborough is the home of major Staff Accountant Jenny Shea Lightning of the National Hockey League. companies like Bloomin’ Brands (Outback And many Tampa-area residents attend the CIRCULATION and other familiar restaurants), Mosaic Director of Audience Development Karen Tyson Rays or the Rowdies just across Tampa Bay. -

STEIN MART, INC., § CASE NO.: 3:20-Bk-02387 § DEBTOR

Case 3:20-bk-02387-JAF Doc 943 Filed 03/05/21 Page 1 of 8 IN THE UNITED STATES BANKRUPTCY COURT FOR THE MIDDLE DISTRICT OF FLORIDA JACKSONVILLE DIVISION In Re: § § STEIN MART, INC., § CASE NO.: 3:20-bk-02387 § DEBTOR. § CHAPTER 11 § AMENDED MOTION FOR RELIEF FROM THE AUTOMATIC STAY TO PERMIT CIVIL LITIGATION TO PROCEED John Pennell, (“Movant” or “Pennell”) by and through his attorneys, hereby seeks relief from the automatic stay pursuant to 11 U. S. C. § 362(d)(1) and 28 U.S.C. §1334(c) to permit him to continue litigating his claims against Debtor, Stein Mart, Inc. (“Debtor” or “Stein Mart”), in Case No. 16-2013-CA-001253-XXXX-MA (the “State Court Action”) pending in the Circuit Court Of The Fourth Judicial Circuit In And For Duval County, Florida in order to liquidate his claim and to collect insurance proceeds. In support of his motion, Pennell would show the Court as follows: INTRODUCTION 1. Pennell was employed by Debtor in March 2001 and from October 2006 until January 27, 2011 served as Debtor’s Senior Vice President and General Merchandise Manager. 2. On February 1, 2013 Pennell filed his State Court Action alleging, causes of action for age discrimination prohibited by the Florida Civil Rights Act of 1992, Florida Statues 760.01 et seq., and breach of contract, fraud, and defamation. A copy of the Complaint in the State Court Action is attached hereto as Exhibit A. 3. As described below, Debtor has insurance that covers Pennell’s wrongful employment practices claims. -

United States Bankruptcy Court Middle District of Florida Jacksonville Division

Case 3:20-bk-02387-JAF Doc 426 Filed 09/22/20 Page 1 of 4 UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA JACKSONVILLE DIVISION IN RE: CHAPTER 11 Stein Mart, Inc. Case No. 3:20-bk-2387 Jointly Administered with Stein Mart Buying Corp., Case No. 3:20-bk-02388 Stein Mart Holding Corp., Case No. 3:20-bk-02389 Debtors.1 NOTICE OF APPEARANCE OF COUNSEL AND REQUEST FOR SERVICE OF PAPERS PLEASE TAKE NOTICE that, pursuant to Rules 2002 and 9010(b) of the Federal Rules of Bankruptcy Procedure, the undersigned attorney hereby gives notice of appearance as counsel for PREMIER CENTRE, LLC, a creditor and party in interest in this matter, and requests that all notices, pleadings and correspondence which are required to be given in this case and all papers served or required to be served in this case be given to and served upon the undersigned at the addresses and electronic mail addresses set forth below. PLEASE TAKE FURTHER NOTICE that neither this Notice of Appearance of Counsel and Request for Service of Papers (the "Notice") nor any later appearance, pleading, proof of claim, claim, or suit shall constitute a waiver of (i) the right to have final orders in noncore matters entered only after de novo review by a District Court judge, (ii) the right to trial by jury in any proceeding triable in these cases 1 The tax identification numbers of the Debtors are as follows: Stein Mart, Inc. 6198; Stein Mart Buying Corp. 1114; and Stein Mart Holding Corp. 0492. -

Efore the Florida Judicial Qualifications Commission

BEFORE THE FLORIDA JUDICIAL QUALIFICATIONS COMMISSION INQUIRY CONCERNING A JUDGE, NO. 01-244 Case No. SC01-2670 (Judge Charles W. Cope) / SPECIAL COUNSEL NOTICE OF CHANGE OF ADDRESS AND FIRM AFFILIATION The undersigned Special Counsel hereby gives notice that he has formed a new law firm with a new address. All future papers and correspondence should be sent to the following address: John S. Mills The Mills Firm 200 North Laura Street, Suite 1150 Jacksonville, Florida 32202 (904) 350-0075 telephone (904) 350-0086 facsimile HeatherAnn Solanka of Foley & Lardner, the undersigned’s former law firm, will continue to serve as co-counsel to the Special Counsel. It is requested that in addition to being served on the undersigned, all papers filed in this matter also be served on Ms. Solanka at the following address: HeatherAnn Solanka Foley & Lardner 200 North Laura Street Jacksonville, Florida 32202 (904) 359-2000 telephone (904) 359-8719 facsimile CERTIFICATE OF SERVICE I HEREBY CERTIFY that a true and correct copy of the foregoing has been furnished by facsimile and regular U.S. mail to: Robert W. Merkle, Jr., Esq., Co-Counsel for Respondent, 5510 W. La Salle Street, #300, Tampa, Florida 33607-1713; Judge James R. Jorgenson, Chair of the Judicial Qualifications Commission Hearing Panel, 3rd District Court of Appeal, 2001 S.W. 117th Ave., Miami, Florida 33175-1716; John Beranek, Esq., Counsel to the Hearing Panel of the Judicial Qualifications Commission, P.O. Box 391, Tallahassee, Florida 32301; Brooke S. Kennerly, Executive Director of the Florida Judicial Qualifications Commission, 1110 Thomasville Road, Tallahassee, Florida 32303; Thomas C. -

United States Bankruptcy Court Middle District of Florida Jacksonville Division

Case 3:20-bk-02387-JAF Doc 1045 Filed 05/19/21 Page 1 of 2 UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF FLORIDA JACKSONVILLE DIVISION In re: Chapter 11 STEIN MART, INC.1 Case No. 3:20-bk-2387 Jointly Administered with STEIN MART BUYING CORP. Case No. 3:20-bk-2388 STEIN MART HOLDING CORP., Case No. 3:20-bk-2389 Debtors. PROOF OF SERVICE I HEREBY CERTIFY that a true and correct copy of the AGREED ORDER FOR RELIEF FROM AUTOMATIC STAY [Docket No. 10402] was served via United States Mail on May 19th, 2021 to the parties on the accompanying Service List. Dated: Jacksonville, Florida May 19, 2021 Respectfully submitted, s/ Christopher M. Hodge By: Christopher M. Hodge Florida Bar No. 72699 HODGE LAW FIRM, P.A 245 Riverside Ave., Suite 300 Jacksonville, FL 32202 904-425-1789 (Tel.) 904-240-4506 (Fax) [email protected] /s/ Carol Nelkin By: Carol Nelkin Texas State Bar No.14883500 Admitted Pro Hac Vice NELKIN & NELKIN, P.C. 7702 Portal Drive 1 The tax identification numbers of the Debtors are as follows: Stein Mart, Inc. 6198; Stein Mart Buying Corp. 1114; and Stein Mart Holding Corp. 0492. The address of Debtors’ office for wind-down activities is 8936 Western Way, Building 6, Ste. 9, Jacksonville, FL 32256. 2 Docket numbers referenced herein reflect the docket number filed in the lead case, Stein Mart, Inc., Case No. 3:20- bk-02387 Case 3:20-bk-02387-JAF Doc 1045 Filed 05/19/21 Page 2 of 2 Houston, TX 77071 713-526-4500 (Tel) [email protected] ATTORNEYS FOR CREDITOR JOHN PENNELL SERVICE LIST Debtors: Ronald E.