June 30, 2021 Ms. Lisa Felice Executive Secretary Michigan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Excesss Karaoke Master by Artist

XS Master by ARTIST Artist Song Title Artist Song Title (hed) Planet Earth Bartender TOOTIMETOOTIMETOOTIM ? & The Mysterians 96 Tears E 10 Years Beautiful UGH! Wasteland 1999 Man United Squad Lift It High (All About 10,000 Maniacs Candy Everybody Wants Belief) More Than This 2 Chainz Bigger Than You (feat. Drake & Quavo) [clean] Trouble Me I'm Different 100 Proof Aged In Soul Somebody's Been Sleeping I'm Different (explicit) 10cc Donna 2 Chainz & Chris Brown Countdown Dreadlock Holiday 2 Chainz & Kendrick Fuckin' Problems I'm Mandy Fly Me Lamar I'm Not In Love 2 Chainz & Pharrell Feds Watching (explicit) Rubber Bullets 2 Chainz feat Drake No Lie (explicit) Things We Do For Love, 2 Chainz feat Kanye West Birthday Song (explicit) The 2 Evisa Oh La La La Wall Street Shuffle 2 Live Crew Do Wah Diddy Diddy 112 Dance With Me Me So Horny It's Over Now We Want Some Pussy Peaches & Cream 2 Pac California Love U Already Know Changes 112 feat Mase Puff Daddy Only You & Notorious B.I.G. Dear Mama 12 Gauge Dunkie Butt I Get Around 12 Stones We Are One Thugz Mansion 1910 Fruitgum Co. Simon Says Until The End Of Time 1975, The Chocolate 2 Pistols & Ray J You Know Me City, The 2 Pistols & T-Pain & Tay She Got It Dizm Girls (clean) 2 Unlimited No Limits If You're Too Shy (Let Me Know) 20 Fingers Short Dick Man If You're Too Shy (Let Me 21 Savage & Offset &Metro Ghostface Killers Know) Boomin & Travis Scott It's Not Living (If It's Not 21st Century Girls 21st Century Girls With You 2am Club Too Fucked Up To Call It's Not Living (If It's Not 2AM Club Not -

Songs by Artist

Sunfly (All) Songs by Artist Karaoke Shack Song Books Title DiscID Title DiscID (Comic Relief) Vanessa Jenkins & Bryn West & Sir Tom Jones & 3OH!3 Robin Gibb Don't Trust Me SFKK033-10 (Barry) Islands In The Stream SF278-16 3OH!3 & Katy Perry £1 Fish Man Starstrukk SF286-11 One Pound Fish SF12476 Starstrukk SFKK038-10 10cc 3OH!3 & Kesha Dreadlock Holiday SF023-12 My First Kiss SFKK046-03 Dreadlock Holiday SFHT004-12 3SL I'm Mandy SF079-03 Take It Easy SF191-09 I'm Not In Love SF001-09 3T I'm Not In Love SFD701-6-05 Anything FLY032-07 Rubber Bullets SF071-01 Anything SF049-02 Things We Do For Love, The SFMW832-11 3T & Michael Jackson Wall Street Shuffle SFMW814-01 Why SF080-11 1910 Fruitgum Company 3T (Wvocal) Simon Says SF028-10 Anything FLY032-15 Simon Says SFG047-10 4 Non Blondes 1927 What's Up SF005-08 Compulsory Hero SFDU03-03 What's Up SFD901-3-14 Compulsory Hero SFHH02-05-10 What's Up SFHH02-09-15 If I Could SFDU09-11 What's Up SFHT006-04 That's When I Think Of You SFID009-04 411, The 1975, The Dumb SF221-12 Chocolate SF326-13 On My Knees SF219-04 City, The SF329-16 Teardrops SF225-06 Love Me SF358-13 5 Seconds Of Summer Robbers SF341-12 Amnesia SF342-12 Somebody Else SF367-13 Don't Stop SF340-17 Sound, The SF361-08 Girls Talk Boys SF366-16 TOOTIMETOOTIMETOOTIME SF390-09 Good Girls SF345-07 UGH SF360-09 She Looks So Perfect SF338-05 2 Eivissa She's Kinda Hot SF355-04 Oh La La La SF114-10 Youngblood SF388-08 2 Unlimited 50 Cent No Limit FLY027-05 Candy Shop SF230-10 No Limit SF006-05 Candy Shop SFKK002-09 No Limit SFD901-3-11 In Da -

The Effects of Digital Music Distribution" (2012)

Southern Illinois University Carbondale OpenSIUC Research Papers Graduate School Spring 4-5-2012 The ffecE ts of Digital Music Distribution Rama A. Dechsakda [email protected] Follow this and additional works at: http://opensiuc.lib.siu.edu/gs_rp The er search paper was a study of how digital music distribution has affected the music industry by researching different views and aspects. I believe this topic was vital to research because it give us insight on were the music industry is headed in the future. Two main research questions proposed were; “How is digital music distribution affecting the music industry?” and “In what way does the piracy industry affect the digital music industry?” The methodology used for this research was performing case studies, researching prospective and retrospective data, and analyzing sales figures and graphs. Case studies were performed on one independent artist and two major artists whom changed the digital music industry in different ways. Another pair of case studies were performed on an independent label and a major label on how changes of the digital music industry effected their business model and how piracy effected those new business models as well. I analyzed sales figures and graphs of digital music sales and physical sales to show the differences in the formats. I researched prospective data on how consumers adjusted to the digital music advancements and how piracy industry has affected them. Last I concluded all the data found during this research to show that digital music distribution is growing and could possibly be the dominant format for obtaining music, and the battle with piracy will be an ongoing process that will be hard to end anytime soon. -

Consumers Energy

Table of Contents CMS ENERGY CONSUMERS ENERGY 2020 COMBINED PROXY STATEMENT Table of Contents CMS ENERGY CORPORATION CONSUMERS ENERGY COMPANY NOTICE OF ANNUAL MEETINGS OF SHAREHOLDERS To Shareholders of CMS Energy Corporation and Consumers Energy Company: The CMS Energy Corporation (‘‘CMS’’) Annual Meeting of Shareholders and the Consumers Energy Company (‘‘Consumers’’) Annual Meeting of Shareholders (collectively ‘‘Annual Meeting’’) will be held concurrently on Friday, May 1, 2020, at 10:00 a.m., Eastern Daylight Saving Time, at the corporate headquarters, One Energy Plaza, Jackson, Michigan 49201 for the purpose of considering the following matters: Board of Directors For Both CMS and Consumers Shareholders: Recommendation Elect the Director Nominees Named in this Proxy Statement to the Board of FOR EACH Directors Approve, on an Advisory Basis, Executive Compensation FOR Ratify the Appointment of Independent Registered Public Accounting Firm FOR Approve the 2020 Performance Incentive Stock Plan FOR Transact such other business as may properly come before the Annual Meeting and any adjournment or postponement Board of Directors For CMS Shareholders Only: Recommendation Vote on a Shareholder Proposal Relating to Political Contributions AGAINST Disclosure, if Properly Presented All shareholders of record at the close of business on March 3, 2020, are entitled to receive notice of and vote at the Annual Meeting. Whether or not you plan to attend the Annual Meeting, you can vote prior to the meeting by telephone, Internet, proxy card or voting instruction form. We encourage you to exercise your right to vote. All shares of Consumers common stock held by CMS (99.6% of the voting shares of Consumers) will be voted for the proposed Director nominees, thus assuring their election as Directors of Consumers, as well as for the other recommendations of the Consumers’ Board of Directors. -

Download Corporate Announcements

Facility Announcement Date Company Headline Activity Type Job Impact Square Feet Description News source Type 6/23/2021 Quiet 3PF Massachusetts logistics company opens 1st TX Industrial New Facility / 400 550,000 Quiet 3PF, leading logistics provider for premium lifestyle brands, has occupied over 550,000-sf in northwest Dallas for new Dallas Business Journal fulfillment center in Dallas Operation fulfillment center. Plans to bring 400 new jobs. 6/17/2021 Youtech & Associates Digital marketing agency opens DFW office Office New Facility / 50 1,000 Youtech, digital marketing agency based in Chicago, opens Plano office with plans to hire 50 workers. The Business Journals / NTX INNO Inc. with plans to hire around 50 workers Operation 6/16/2021 Theragun, Inc Theragun Maker Picks Dallas For Second U.S. Office New Facility / 50 Therabody, Los Angeles tech-wellness company and creator of the Theragun, will set up its 2nd U.S. HQ in Dallas at 2200 D Magazine Headquarters Operation Main in the East Quarter of downtown Dallas. It expects to bring 50 jobs. 6/16/2021 CarParts.com CarParts.com creates 125 jobs with 156,000-sf Industrial Expansion / 125 156,000 CarParts.com, California-based automobile parts company, is expanding its Grand Prairie distribution center by adding 125 Dallas Morning News expansion in Grand Prairie Consolidation jobs and 156,000-sf to its existing building. 6/10/2021 Siteone Landscape Public wholesaler expands into Texas with Industrial New Facility / 337,913 Georgia-based SiteOne Landscape Supply has opened its largest distribution center in South Dallas County. The wholesaler Dallas Business Journal Supply, Inc. -

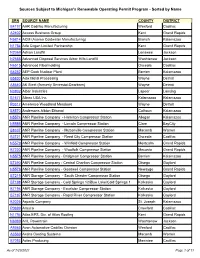

Sources Subject to Michigan's Renewable Operating Permit Program - Sorted by Name

Sources Subject to Michigan's Renewable Operating Permit Program - Sorted by Name SRN SOURCE NAME COUNTY DISTRICT B4197 AAR Cadillac Manufacturing Wexford Cadillac A2402 Access Business Group Kent Grand Rapids N5814 ACM (Asama Coldwater Manufacturing) Branch Kalamazoo N1784 Ada Cogen Limited Partnership Kent Grand Rapids N2369 Adrian Landfill Lenawee Jackson N2688 Advanced Disposal Services Arbor Hills Landfill Washtenaw Jackson N6515 Advanced Fibermolding Osceola Cadillac B4252 AEP Cook Nuclear Plant Berrien Kalamazoo B5830 Ajax Metal Processing Wayne Detroit A8640 AK Steel (formerly Severstal-Dearborn) Wayne Detroit N0802 Albar Industries Lapeer Lansing B1677 Allnex USA Inc. Kalamazoo Kalamazoo P0317 Ameresco Woodland Meadows Wayne Detroit B8570 Andersons Albion Ethanol Calhoun Kalamazoo N5574 ANR Pipeline Company - Hamilton Compressor Station Allegan Kalamazoo N5586 ANR Pipeline Company - Lincoln Compressor Station Clare BayCity B8337 ANR Pipeline Company - Muttonville Compressor Station Macomb Warren B3721 ANR Pipeline Company - Reed City Compressor Station Osceola Cadillac N5578 ANR Pipeline Company - Winfield Compressor Station Montcalm Grand Rapids B7220 ANR Pipeline Company - Woolfolk Compressor Station Mecosta Grand Rapids N5575 ANR Pipeline Company - Bridgman Compressor Station Berrien Kalamazoo B7390 ANR Pipeline Company - Central Charlton Compressor Station Otsego Gaylord N5576 ANR Pipeline Company - Goodwell Compressor Station Newaygo Grand Rapids B7219 ANR Storage Company - South Chester Compressor Station Otsego Gaylord -

My Bloody Valentine's Loveless David R

Florida State University Libraries Electronic Theses, Treatises and Dissertations The Graduate School 2006 My Bloody Valentine's Loveless David R. Fisher Follow this and additional works at the FSU Digital Library. For more information, please contact [email protected] THE FLORIDA STATE UNIVERSITY COLLEGE OF MUSIC MY BLOODY VALENTINE’S LOVELESS By David R. Fisher A thesis submitted to the College of Music In partial fulfillment of the requirements for the degree of Master of Music Degree Awarded: Spring Semester, 2006 The members of the Committee approve the thesis of David Fisher on March 29, 2006. ______________________________ Charles E. Brewer Professor Directing Thesis ______________________________ Frank Gunderson Committee Member ______________________________ Evan Jones Outside Committee M ember The Office of Graduate Studies has verified and approved the above named committee members. ii TABLE OF CONTENTS List of Tables......................................................................................................................iv Abstract................................................................................................................................v 1. THE ORIGINS OF THE SHOEGAZER.........................................................................1 2. A BIOGRAPHICAL ACCOUNT OF MY BLOODY VALENTINE.………..………17 3. AN ANALYSIS OF MY BLOODY VALENTINE’S LOVELESS...............................28 4. LOVELESS AND ITS LEGACY...................................................................................50 BIBLIOGRAPHY..............................................................................................................63 -

By Student Congresswoman by Sonja Martin Are Not Known

Volume 44 Number 10 December 3,1992 STOCKTON STATE COLLEGE POMONA, NEW J ERSE Y 08240 Officer "assaulted" by student Congresswoman by Sonja Martin are not known. Skipper, Monfiston's roommate. In the morning of December 2, Monfiston has been charged with Skipper was asleep and awoke to 1992, an altercation occurred in Hous- aggravated assault of a police officer, find Monfiston against the wall and ing I resulting in an arrest of a student resisting arrest, and disorderly person Lentz "in his face." Monfiston was due to an alleged assault of Sergeant according to campus police. He is held apparently saying that all he was doing and harmony William Lentz of Stockton Campus in the Atlantic County Corrections was walking up to his apartment. Police. Officers were responding to a Skipper tried to break up the physi- E.C. O'Hanlon report of gunshots fired and a female cal confrontation between Lentz and "We must recognize we are fellow travelers on this screaming in H-court at approximately Monfiston but Officer Forte, the other Earth Ship, the small planet called Earth. All our actions 4:00AM. Officers responded and ques- officer present, held him back. Ac- should reflect and acknowledge this," commented Shirley tioned Dominique Monfiston as to if cording to Skipper, Lentz pushed Chisholm recently. he had any information on what oc- Monfiston into the living room lamp The Stockton International Student Organization curred. and Monfiston pushed him back. Skip- brought Ms. Chisholm, former United States Congress- "For some reason, the suspect be- per again tried to break this up. -

Annual Report

Table of Contents CMS ENERGY & C ONSUME RS ENERGY ANNUAL REPORT 2019 Table of Contents Dear Shareowners: I’m proud to report that we delivered another year of strong financial performance in 2019, marking 17 years of meeting our adjusted earnings guidance. As we reflect on a successful year of world class performance delivering hometown service, I’m proud to share our top achievements with you, as measured by our triple bottom line of People, Planet and Profit. PEOPLE ─ Serving our customers, communities and co-workers. Highlights include: • Achieved 1st Quartile Employee Engagement • Named the #1 Michigan Company for Diversity 2019 by Forbes® Magazine for the third year in a row • Ranked 2nd in the state (40th of 113 companies globally) in the Military Times Best for Vets: Employers 2019 • Ranked in the Top 50 Best Employers for Diversity 2020 by Forbes® Magazine • Won the Association for Talent Development (ATD) 2019 BEST Award (# 3 in the world) • Received the 2019 Women’s Resource Network’s Pillar Award • Ranked #1 overall in the Midwest Large Segment for the 2019 Gas Residential Customer Satisfaction Study, JD Power & Associates • Partnered with Project Search and Jackson Intermediate School District to launch our 2nd cohort of interns to provide meaningful work experiences to young adults with disabilities PLANET ─ Going above and beyond environmental regulations to leave our planet better than we found it. Highlights include: • Settled our 20-year Clean Energy Plan with broad coalition of support • Cross Winds® Energy Park Phase -

8123 Songs, 21 Days, 63.83 GB

Page 1 of 247 Music 8123 songs, 21 days, 63.83 GB Name Artist The A Team Ed Sheeran A-List (Radio Edit) XMIXR Sisqo feat. Waka Flocka Flame A.D.I.D.A.S. (Clean Edit) Killer Mike ft Big Boi Aaroma (Bonus Version) Pru About A Girl The Academy Is... About The Money (Radio Edit) XMIXR T.I. feat. Young Thug About The Money (Remix) (Radio Edit) XMIXR T.I. feat. Young Thug, Lil Wayne & Jeezy About Us [Pop Edit] Brooke Hogan ft. Paul Wall Absolute Zero (Radio Edit) XMIXR Stone Sour Absolutely (Story Of A Girl) Ninedays Absolution Calling (Radio Edit) XMIXR Incubus Acapella Karmin Acapella Kelis Acapella (Radio Edit) XMIXR Karmin Accidentally in Love Counting Crows According To You (Top 40 Edit) Orianthi Act Right (Promo Only Clean Edit) Yo Gotti Feat. Young Jeezy & YG Act Right (Radio Edit) XMIXR Yo Gotti ft Jeezy & YG Actin Crazy (Radio Edit) XMIXR Action Bronson Actin' Up (Clean) Wale & Meek Mill f./French Montana Actin' Up (Radio Edit) XMIXR Wale & Meek Mill ft French Montana Action Man Hafdís Huld Addicted Ace Young Addicted Enrique Iglsias Addicted Saving abel Addicted Simple Plan Addicted To Bass Puretone Addicted To Pain (Radio Edit) XMIXR Alter Bridge Addicted To You (Radio Edit) XMIXR Avicii Addiction Ryan Leslie Feat. Cassie & Fabolous Music Page 2 of 247 Name Artist Addresses (Radio Edit) XMIXR T.I. Adore You (Radio Edit) XMIXR Miley Cyrus Adorn Miguel Adorn Miguel Adorn (Radio Edit) XMIXR Miguel Adorn (Remix) Miguel f./Wiz Khalifa Adorn (Remix) (Radio Edit) XMIXR Miguel ft Wiz Khalifa Adrenaline (Radio Edit) XMIXR Shinedown Adrienne Calling, The Adult Swim (Radio Edit) XMIXR DJ Spinking feat. -

Rate Book for Natural Gas Service

M.P.S.C. No. 3 - Gas Original Sheet No. A-1.00 Consumers Energy Company (To reformat Rate Book) CONSUMERS ENERGY COMPANY RATE BOOK FOR NATURAL GAS SERVICE These Standard Rules and Regulations and Rate Schedules contained herein have been adopted by the Company to govern its relations with customers and have been approved by the Michigan Public Service Commission as an integral part of its Rate Book for Natural Gas Service. Copies of the Company's Rate Book for Natural Gas Service are available on Consumers Energy Company's website at the following website address, https://www.consumersenergy.com/-/media/CE/Documents/rates/gas-rate-book.ashx or at the Michigan Public Service Commission's website at the following website address, https://www.michigan.gov/documents/mpsc/consumers2cur_575658_7.pdf. Territory This Rate Book for Natural Gas Service applies to the entire territory served with Natural Gas by the Company. THIS RATE BOOK SUPERSEDES AND CANCELS RATE BOOK M.P.S.C. No. 2 - Gas Issued December 13, 2019 by Patti Poppe, President and Chief Executive Officer, Jackson, Michigan M.P.S.C. No. 3 – Gas Second Revised Sheet No. A-2.00 Consumers Energy Company Cancels First Revised Sheet No. A-2.00 (To update links) INDEX SECTION A Sheet No. Title Page A-1.00 Index A-2.00 Table of Contents - Checklist A-7.00 Gas Service or Franchise Area A-11.00 Territory Served A-12.00 Technical Terms and Abbreviations A-24.00 Supplemental Utility Service Charges A-26.00 SECTION B ADMINISTRATIVE RULES INDEX https://www.michigan.gov/mpsc/0,9535,7-395-93309_93437_93467---,00.html B1. -

Policies to Overcome Barriers for Renewable Energy Distributed Generation: a Case Study of Utility Structure and Regulatory Regimes in Michigan

Michigan Technological University Digital Commons @ Michigan Tech Department of Social Sciences Publications Department of Social Sciences 2-20-2019 Policies to overcome barriers for renewable energy distributed generation: A Case study of utility structure and regulatory regimes in Michigan Emily Prehoda Michigan Technological University Joshua M. Pearce Michigan Technological University Chelsea Schelly Michigan Technological University Follow this and additional works at: https://digitalcommons.mtu.edu/social-sciences-fp Part of the Energy Policy Commons, and the Environmental Policy Commons Recommended Citation Prehoda, E., Pearce, J. M., & Schelly, C. (2019). Policies to overcome barriers for renewable energy distributed generation: A Case study of utility structure and regulatory regimes in Michigan. Energies, 12(4). http://dx.doi.org/10.3390/en12040674 Retrieved from: https://digitalcommons.mtu.edu/social-sciences-fp/164 Follow this and additional works at: https://digitalcommons.mtu.edu/social-sciences-fp Part of the Energy Policy Commons, and the Environmental Policy Commons energies Review Policies to Overcome Barriers for Renewable Energy Distributed Generation: A Case Study of Utility Structure and Regulatory Regimes in Michigan Emily Prehoda 1, Joshua M. Pearce 2,3,* and Chelsea Schelly 1 1 Department of Social Sciences, Michigan Technological University, Houghton, MI 49931, USA; [email protected] (E.P.); [email protected] (C.S.) 2 Department of Material Science & Engineering and Department of Electrical & Computer Engineering, Michigan Technological University, Houghton, MI 49931, USA 3 Department of Electronics and Nanoengineering, School of Electrical Engineering, Aalto University, FI-00076 Espoo, Finland * Correspondence: [email protected] or joshua.pearce@aalto.fi Received: 9 January 2019; Accepted: 14 February 2019; Published: 20 February 2019 Abstract: Because of its environmental damage and now often being the most expensive source for electricity production, coal use is declining throughout the United States.