South Ayrshire Town Centre Assessment

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mobile Order (Via Costa App) Aberdeen

Mobile order (via Costa app) Aberdeen - Bon Accord Centre AB25 1HZ Aberdeen - Cults AB15 9SD Aberdeen - Union Square AB11 5PS Aberdeen Bridge of Don DT AB23 8JW Aberdeen, Abbotswell Rd, DT AB12 3AD Aberdeen, Beach Boulevard RP, 1A AB11 5EJ Aberdeen, Marischal Sq AB10 1BL Aberdeen, Next, Berryden Rd, 4 AB25 3SG Aberdeen, Westhill SC, 27 AB32 6RL Abergavenny NP7 5RY Abergavenny, Head of the Valleys DT NP7 9LL Aberystwth SY23 1DE Aberystwyth Parc Y Llyn RP, Next SY23 3TL Accrington BB5 1EY Accrington, Hyndburn Rd, DT BB5 4AA Alderley Edge SK9 7DZ Aldershot GU11 1EP Alnwick NE66 1HZ Altrincham, Sunbank Lane, DT WA15 0AF Amersham HP6 5EQ Amersham - Tesco HP7 0HA Amesbury Drive Thru SP4 7SQ Andover SP10 1NF Andover BP DT SP11 8BF Andover, Andover Bus Station SP10 1QP Argyll Street W1F 7TH Ascot SL5 7HY Ashbourne DE6 1GH Ashford Int Station TN23 1EZ Ashford RP TN24 0SG Ashord - Tesco TN23 3LU Ashton OL6 7JJ Ashton Under Lyne DT OL7 0PG Atherstone, Grendon, Watling St, DT CV9 2PY Aviemore, Aviemore RP, U4 PH22 1RH Aylesbury HP20 1SH Aylesbury - Tesco HP20 1PQ Aylesbury Shopping Park HP20 1DG Ayr - Central, Teran Walk KA7 1TU Ayr - Heathfield Retail Park KA8 9BF Bagshot DT GU19 5DH Baker Street W1U 6TY Bakewell, King St DE45 1DZ Baldock SG7 6BN Banbury OX16 5UW Banbury Cross RP OX16 1LX Banbury, Stroud Park DT OX16 4AE Bangor LL57 1UL Bangor RP - Next LL57 4SU Banstead SM7 2NL Barking - Tesco IG11 7BS Barkingside IG6 2AH Barnard Castle DL12 8LZ Barnsley S70 1SJ Barnsley J36 DT Barnsley, Birdwell, Kestrel Way, DT S70 5SZ Barnstaple EX31 1HX Barnstaple -

Retail Healthretail Sector» 2 » 2

RETAIL HEALTHRETAIL SECTOR» 2 » 2 << NEIL SHAWCROSS The adjacent painting was created by artist Neil Shawcross to illustrate the evolution of the McLaughlin & Harvey brand from 1853 to the present. It symbolises that while our face has changed, our values remain the same. “NOTHING CHANGES & YET EVERYTHING IS COMPLETELY DIFFERENT” ALDOUS HUXLEY RETAIL » 4 OUR APPROACH For over 160 years McLaughlin & Harvey has combined traditional values and experience, with an advanced innovative approach. We operate throughout the United We have a strong commitment to Shopping Centres Kingdom and Ireland, and pride delivering quality cost effective solutions RETAIL ourselves on delivering quality building for our customers within a safe, DEVELOPMENT construction, fit-out, civil engineering, considerate working environment. Woking | £15m and facilities management projects. Through proactive stakeholder We work in various sectors including engagement we have implemented a health, education, industrial, retail, strong Corporate Social Responsibility sporting venues, marine and rivers, (CSR) strategy, facilitating a sustainable transport infrastructure, offshore, business which supports the health, energy, commercial, and leisure. safety, welfare, and well-being of our workforce, customers, supply chain and the local communities in which we work. Our core values and strengths are: • Hands on accessible leadership • Strong relationships, collaboration and communication • Corporate resilience and capacity RETAIL » 6 Non-food MARKS & SPENCER Longbridge | £9m -

Property Investor Profiles

ANG Property Investor Profiles Fund Anglesea Capital Angelo, Gordon Europe Ltd 11 Hill Street, London W1J 5LF 25 Hanover Square, London W1S 1JF Tel: 020 7629 5324 Tel: 0207 758 5300 Fax: 0207 758 5420 Email: [email protected] Email: amittal@angelogordon. com Web: www.angleseacapital.com Web: www.angelogordon.com Contacts Contacts Rhys Lewis (Managing Director) Anuj Mittal (Real Estate) Nick Sowerbutts (Asset Manager) Comment Comment US private equity fund manager Angelo Gordon announced plans Anglesea Capital Ltd was formed by former Rockpoint director Rys to invest a substantial proportion of its $2bn of property funds in the Lewis. UK. (07/09) 12/11 - London & Stamford (94% interest) and Anglesea (6% The privately owned fund manager is investing two funds: its interest) sold the Triangle Distribution Portfolio and including the $800m AG Core Plus Realty Fund II, of which it has already spent recently acquired 5110 Magna Park, Lutterworth for a consideration around 35%; and its $1.25bn opportunity fund, the AG Realty Fund of £265m . Anglesea will continue to manage the portfolio with VII, of which around 25% is invested. Blackstone as its equity backer. 11/11 - Angelo, Gordon & Co bought the Frimley Business Park in Surrey, in partnership with Investream, for £15m - reflecting a Anglo Scottish Properties Plc 13.2% yield. The park comprises nine office buildings totalling 100a Chalk Farm Road, London NW1 8EH 161,074 sq ft on a 13.4-acre site. Tel: 020 7284 1144 Fax: 020 7267 2477 Email: [email protected] 06/12 - Angelo, Gordon paid Avestus Capital Partners £70m for Senator House, 85 Queen Victoria Street, EC4 - reflecting a net Contacts initial yield of 8.75%. -

GUEST INFORMATION | 01292 294990 Guest Information

GUEST INFORMATION www.westernhousehotel.co.uk | 01292 294990 Guest Information Contents 4. Essential Information 6 Food & Drink 7. Television & Radio / Business Facilities 8. Dialling Codes 9. Weddings & Events 10. Racing and Conference & Events at Ayr Racecourse 11. Local Attractions www.westernhousehotel.co.uk | 01292 294990 3 Essential Information To contact Reception call ‘0’ Baby Cots and Essential Supplies First Aid Please call Reception For emergency assistance please dial 9-999. For minor injuries, please call Reception. Blankets - Please call Reception Car Rentals - Please call Reception Flowers Fresh flowers can be ordered from Reception. Currency Exchange A foreign currency exchange service is available at Garment Press competitive rates. Please enquire at Reception. To have trousers pressed, please contact reception. An iron and ironing board are located in your wardrobe. Credit and Debit Cards We honour the following credit and debit cards: How to call an External Number Credit Cards:- American Express, Mastercard and Visa To gain access to an outside line, prefix the telephone Debit Cards:- Visa Debit, Delta, Switch and Maestro. number and code with 9 Electricity/Voltage How to call another Room If you wish to call another room simply dial the room The standard voltage is 230 volts. A razor socket is number’s 3 digits. provided in the bathroom with both 110/120 and 230 volt outlets. Reception can provide the use of an adaptor plug if required subject to availability. Laundry A next-day laundry service is available from Monday to Friday. All items received by 9.00am will be returned Emergency Exits the following day. -

Door to Door Breast Cancer Now Fundraiser Locations

Breast Cancer Now Fundraiser Locations - Week Commencing 07/06/2021 Venues Start date Venue City/Town Postcode Agency 07/06/2021 St Enoch Shopping Centre Glasgow G1 4BW Unique 07/06/2021 Clyde INT/EXT Shopping Centre Clydebank G81 2UA Unique 07/06/2021 Cannock shopping centre cannock WS11 1WS Unique 07/06/2021 Coatbridge Town Centre Coatbridge ML5 3EL Unique 07/06/2021 The Hardshaw Shopping Centre St. Helens WA10 1EB Unique 07/06/2021 St Georges Shopping Centre Preston PR1 2NQ Unique 07/06/2021 Rugby Central Rugby CV21 2JR Unique 07/06/2021 Hill Street Shopping Centre Middlesbrough TS1 1SU Unique 07/06/2021 Wulfrun Shopping Centre Wolverhampton WV1 3PR Unique 07/06/2021 Ayr Central Shopping Centre Ayr KA7 1TP Unique 07/06/2021 Antonine Shopping Centre Glasgow G67 1JW Unique 07/06/2021 The Regent Shopping Centre Hamilton ML3 7DZ Unique 11/06/2021 The National Motorhome & Campervan Show Peterborough PE2 6XE Unique Door to Door Start date Local Authority Postcode Agency 07/06/2021 Doncaster DN22 BRC 07/06/2021 Wakefield WF10 BRC 07/06/2021 Aberdeen City Council AB10 1 APPCO 07/06/2021 Aberdeen City Council AB10 6 APPCO 07/06/2021 Aberdeen City Council AB10 7 APPCO 07/06/2021 Aberdeen City Council AB11 5 APPCO 07/06/2021 Aberdeen City Council AB11 6 APPCO 07/06/2021 Aberdeen City Council AB11 7 APPCO 07/06/2021 Aberdeen City Council AB11 8 APPCO 07/06/2021 Aberdeen City Council AB11 9 APPCO 07/06/2021 Aberdeen City Council AB12 3 APPCO 07/06/2021 Aberdeen City Council AB13 0 APPCO 07/06/2021 Aberdeen City Council AB15 4 APPCO 07/06/2021 Aberdeen -

Property Reference Description / Situation Appellant / Agent Status Appealed Value Appeal Number

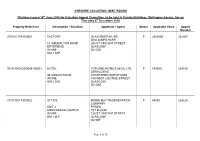

AYRSHIRE VALUATION JOINT BOARD Citations Issued 16th June 2016 for Valuation Appeal Committee, to be held in County Buildings, Wellington Square, Ayr on Thursday 8th December 2016 Property Reference Description / Situation Appellant / Agent Status Appealed Value Appeal Number 07/01/C47340/0051 FACTORY GLAXOSMITHKLINE P 2502000 234267 GVA JAMES BARR 51 SHEWALTON ROAD 206 ST VINCENT STREET DRYBRIDGE GLASGOW IRVINE G2 5SG KA11 5AP 07/01/D01620/0046 /00001 HOTEL TOPLAND HOTELS (NO2) LTD P 190000 234516 GERALD EVE 46 ANNICK ROAD CHARTERED SURVEYORS IRVINE 140 WEST GEORGE STREET KA12 0JG GLASGOW G2 2HG 07/01/D01730/0002 OFFICE IRVINE BAY REGENERATION P 45000 234220 COMPANY UNIT 2 RYDEN ANNICKBANK CAMPUS 1ST FLOOR IRVINE 130 ST VINCENT STREET KA11 4LF GLASGOW G2 5HF Page 1 of 75 AYRSHIRE VALUATION JOINT BOARD Citations Issued 16th June 2016 for Valuation Appeal Committee, to be held in County Buildings, Wellington Square, Ayr on Thursday 8th December 2016 Property Reference Description / Situation Appellant / Agent Status Appealed Value Appeal Number 07/01/D01730/0003A OFFICE ACCESS PLUS (SCOTLAND) LTD T 52000 234360 RYDEN ROSEMOUNT HOUSE 1ST FLOOR ANNICKBANK CAMPUS 130 ST VINCENT STREET IRVINE GLASGOW KA11 4LF G2 5HF 07/01/D01730/0003B OFFICE ROSEMOUNT HOLDINGS P 16400 234368 MOIRA WALKER ROSEMOUNT HOUSE (GL) RYDEN ANNICKBANK CAMPUS 130 ST VINCENT STREET IRVINE GLASGOW KA11 4LF G2 5HF 07/01/D02280/0028 /U0004 SHOP PIRGIN SINGH PAVITA P 12900 234237 SHERGILL Unit 4 & MRS GURMEJ KAUR 28 BANK STREET IRVINE KA12 0AD Page 2 of 75 AYRSHIRE VALUATION -

Aberdeen Abbotsweldt, Aberdeen Aberdeen DT, Aberdeen

Eat Out to Help Out participating stores Additional info Abbey Sands TQ2 5FB England Aberdare CF44 0AH Wales Aberdeen - Bon Accord Centre AB25 1HZ Scotland Aberdeen - Cults AB15 9SD Scotland Aberdeen - Tesco, Rousay Drive AB15 6XS Scotland Aberdeen - Union Square AB11 5PS Scotland Aberdeen AbbotswelDT, Aberdeen AB12 3AD Scotland Opening 07/08 Aberdeen DT, Aberdeen AB23 8JW Scotland Opening 07/08 Aberdeen, Beach Boulevard RP, 1A AB11 5EJ Scotland Aberdeen, Marischal Sq AB10 1BL Scotland Aberdeen, Next, Berryden Rd, 4 AB25 3SG Scotland Aberdeen, Westhill SC, 27 AB32 6RL Scotland Abergavenny NP7 5RY Wales Abergavenny DT, Abergavenny NP7 9LL Wales Opening 16/08 Aberystwth SY23 1DE Wales Aberystwyth Parc Y Llyn RP, Next SY23 3TL Wales Abingdon OX14 3QY England Abingdon Thameside OX14 3HE England Accrington BB5 1EY England Accrington Hyndburn Rd DT, Accrington BB5 1PY England Opening 05/08 Acocks Green B27 6BH England Acton W3 6QX England Aintree Racecourse Next L9 5AN England Airdrie ML6 6BU Scotland Albert Bygrave AL2 1DL England Albert Dock 2 L3 4AG England Alderley Edge SK9 7DZ England Aldershot GU11 1EP England Aldridge WS9 8QP England Alfreton DE55 7DP England Allerton Liverpool L18 2DD England Allerton Road 2 L18 1LG England Allestree 0 England Alloa FK10 1JF Scotland Alnwick NE66 1HZ England Alperton DT, Greenford UB6 8AA England Opening 07/08 Alsager ST7 2LP England Alton GU34 1AW England Altrincham - George Street WA14 1RJ England Altrincham Sunbank Lane DT, Manchester WA15 0AF England Opening 15/08 Amersham HP6 5EQ England Amersham -

Door to Door Breast Cancer Now Fundraiser Locations

Breast Cancer Now Fundraiser Locations - Week Commencing 14/06/2021 Venues Start date Venue City/Town Postcode Agency 14/06/2021 Parkgate EXT Shopping Centre Solihull B90 3GG Unique 14/06/2021 Springburn Shopping Centre Glasgow G21 1TS Unique 14/06/2021 INTU The Potteries shopping centre Stoke-On-Trent ST1 1RZ Unique 14/06/2021 The Forge Shopping Centre Gallowgate G31 4EB Unique 14/06/2021 Ayr Central Shopping Centre Ayr KA7 1TP Unique 14/06/2021 Ropewalk Shopping Centre Nuneaton CV11 5TQ Unique 14/06/2021 Trinity ( ABERDEEN ) Shopping Centre Aberdeen AB11 6BE Unique 14/06/2021 Rivergate Shopping Centre Scotland, KA12 8EJ Unique 14/06/2021 The Millgate Shopping Centre Bury BL9 0QQ Unique 15/06/2021 The Centre Livingston Livingstone EH54 6HR Unique 15/06/2021 Swan Shopping Centre Birmingham B25 8UJ Unique 14/06/2021 Co-op Bristol BS9 3DF APPCO Door to Door Start date Local Authority Postcode Agency 14/06/2021 Aberdeen City Council AB10 1 APPCO 14/06/2021 Aberdeen City Council AB10 6 APPCO 14/06/2021 Aberdeen City Council AB10 7 APPCO 14/06/2021 Aberdeen City Council AB11 5 APPCO 14/06/2021 Aberdeen City Council AB11 6 APPCO 14/06/2021 Aberdeen City Council AB11 7 APPCO 14/06/2021 Aberdeen City Council AB11 8 APPCO 14/06/2021 Aberdeen City Council AB11 9 APPCO 14/06/2021 Aberdeen City Council AB12 3 APPCO 14/06/2021 Aberdeen City Council AB13 0 APPCO 14/06/2021 Aberdeen City Council AB15 4 APPCO 14/06/2021 Aberdeen City Council AB15 5 APPCO 14/06/2021 Aberdeen City Council AB15 6 APPCO 14/06/2021 Aberdeen City Council AB15 7 APPCO 14/06/2021 -

For Sale/Lease

FOR SALE/LEASE PURPOSE BUILT OFFICE PREMISES www.shepherd.co.uk 68 Kyle Street, Ayr, KA7 1RZ ** RENT/PRICE REDUCED ** Purpose built upper floor office premises Excellent central commercial location Reception area, 4 main offices, staff toilet facilities Adjacent town centre public car park Approx. 83.4 sq. m. (898 sq. ft.) AYR OFFICE 01292 267 987 Location Services The property enjoys the benefit of an excellent central commercial location Mains drainage, water and electricity supplies are laid on to the property. adjacent to the Kyle Street pavement line, within 200 yards or so of both prime Electric heating units have been installed throughout the accommodation. High Street shopping and the popular Ayr Central retail complex. Rating Assessment Ayr is the principal settlement within the South Ayrshire Council area and has a resident population of around 46,500. The subjects are currently entered in the Valuation Roll as follows:- NAV/RV £6,300 Energy Performance Certificate (EPC) A copy of an EPC will be made available upon request. Lease Terms The property is available on a new full repairing and insuring lease of negotiable length. Prices Lease – offers in excess of £5,000 p.a. are invited. Sale – offers in excess of £60,000 are invited. Annual management charge approx. £650 to include building insurance premium. Value Added Tax All prices, rents and premiums, where quoted, are exclusive of VAT. Prospective purchasers/lessees are advised to satisfy themselves independently as to the incidence of Value Added Tax in respect of this The Property transaction. Modern fully fitted second floor office suite contained within purpose built Entry retail, office and residential development scheme constructed circa 1987. -

Feasibility Study Ayr Station Hotel

AY R S TAT I O N H O T E L F E A S I B I L I T Y S T U D Y February 2021 Contributors The Project Team have contributed to the Report. Architecture + Lead Transport Planning Atkins Atkins Structural Engineering Costs Atkins Faithful & Gould Building Services Planning & Heritage Atkins Iceni Economics Property Atkins Avison Young AYR STATION HOTEL FEASIBILITY STUDY 2 AYR STATION HOTEL FEASIBILITY STUDY 1.0 INTRODUCTION 1.0 Introduction 1.1 RIBA Stage 0 Following the RIBA Plan of Work 2020 Deliverables and Task Work undertaken Guidelines, the Core Objectives are to identify the Client’s » Site visit Business Case and Strategic Brief. » Consultation with key Stakeholders Other key tasks are reviewing all previous feedback and » Project Meetings collated information, assembling the team, establishing the » Design Team Meetings programme and concluding the stage with the Strategic Brief. » Preparation of CAD plans and 3D model of the building The team have agreed that a further output of this stage will be » Review and Validation of Structural Report an identification of a long list of options for sifting at the start » Site Constraint Analysis of Stage 1, of which the identified options will be developed further as the basis for the Business Case Report. » Review of Planning and Heritage context » Review of strategic policy documents A key output of Stage 0 is to collate, review and summarise the associated with the wider area large array of information already gathered on this project over » High level review of local property market the preceding months and years. -

Equity Costa Store List 2019 Live from 2Nd March 2019 Version 3.Xlsx

Store Name Address Blackheath 41 Tranquil Vale London SE3 0BU Hempstead Valley Shopping Centre 2 Unit F11a, Hempstead Valley Shopping Centre Kent ME7 3PD Aberdeen - Academy Unit 15, The Academy Aberdeen AB10 1LB Aberdeen - Bon Accord Centre Bon Accord Shopping Centre Aberdeen AB25 1HZ Aberdeen - Union Square Mall Café Aberdeen AB11 5PS Aberdeen - Cults 2-3 The Courtyard Aberdeen AB15 9SD Aberdeen - Tesco, Rousay Drive Rousay Drive Aberdeen AB15 6XS Aberdeen, Westhill SC, 27 Unit 27, Westhill Shopping Centre Aberdeen AB32 6RL Debenhams Aberdeen Debenhams, Unit 7 Aberdeen AB11 6BE Aberdeen, Next, Berryden Rd, 4 NEXT, Unit 4, Berryden Road Aberdeen AB25 3SG Aberdeen, Abbotswell Rd, DT Drive Thru Aberdeen AB12 3AD Aberdeen Bridge of Don DT Drive Thru, Bridge of Don Retail Park Aberdeen AB23 8JW Aberdeen, Marischal Sq Unit 1a, Marischal Square Aberdeen AB10 1BL Abergavenny, Head of the Valleys DT Westgate Abergavenny NP7 9LL Abergavenny 11 High Street Abergavenny NP7 5RY Aberystwth 5 Great Darkgate Street Aberystwth SY23 1DE Aberystwyth Parc Y Llyn RP, Next Costa Coffee, NEXT, Parc Y Llyn Retail Park Aberystwyth SY23 3TL Milton, Milton Gate 2, DT Drive Thru, 2 Milton Gate Abingdon OX14 4TX Accrington Unit 6 Broadway Accrington BB5 1EY Alderley Edge 24 London Road Alderley Edge SK9 7DZ Aldershot 49-51 Union Street Aldershot GU11 1EP Alnwick 69-71 Bondgate Within Alnwick NE66 1HZ Altrincham - George Street Unit SU207 Altrincham WA14 1RJ Timperley Paul House Altrincham WA15 7UG Hale Barns Unit 5, The Square Altrincham WA15 8ST Amersham 35-37 Sycamore -

June 2019 the Business of Retail Formerly Shopping Centre Magazine

RETAIL DESTINATION JUNE 2019 THE BUSINESS OF RETAIL FORMERLY SHOPPING CENTRE MAGAZINE PARKING OPERATORS TURN TO TECHNOLOGY TO FILL EMPTY SPACES Sustainability Parking Technology McArthurGlen starts work on More and more centres are Intu pilots new in-store cashback Europe’s largest living wall switching to cashless parking app for retailers to drive footfall RETAIL IS CHANGING. Create experiences that change with it. We combine giant LED platforms with larger-than-life creative to inspire, engage and interact at scale. Static interiors and architecture are transformed into digital canvases [LIVIFVERHWƽSYVMWLERHEYHMIRGIWEVIGETXMZEXIH[MXLZMWMXSVW staying longer and returning more frequently. See our vision for future retail destinations at www.adi.tv/create For more information visit www.adi.tv/create 0800 592 346 | [email protected] | www.adi.tv CONTENTS NEWS & ANALYSIS EDITOR'S LETTER 04 Inditex signs up for Edinburgh St James As Retail Destination went to press the SCEPTRE Awards judging panel were 06 Redevco opens new Lane for Brighton doing their homework ahead of the annual judging day. 08 Shopping centre values slashed We’ve introduced some new categories alongside the old favourites which attracted some high-quality entries It’s already clear that this year’s awards 12 St James has designs on Dover entry is going to present the judges with some tough decisions as they try to pick the winners. 13 MAPIC Food shines the spotlight on F&B The annual awards dinner is only weeks away so now is the time to think about FEATURES booking your place for one of the biggest events in the retail property calendar.