Ramsey Final Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Minnesota Public Radio News and Humphrey Institute Poll

Minnesota Public Radio News and Humphrey Institute Poll Dayton Starts with Edge in Democratic Primary and Fall Election Report prepared by the Center for the Study of Politics and Governance Humphrey Institute of Public Affairs University of Minnesota Lawrence R. Jacobs Director, Center for the Study of Politics and Governance Joanne M. Miller Research Associate, Center for Study of Politics and Governance Associate Professor, Department of Political Science According to a Minnesota Public Radio News and Humphrey Institute poll, Mark Dayton starts the election season leading his rivals in the Democratic Party primary among likely voters and Dayton may also enjoy a slight edge over the presumptive Republican gubernatorial candidate, Tom Emmer, among Minnesota adults. Dayton leads Emmer by a 35% to 31% margin, which is within the margin of error and is a toss-up in statistical terms. Emmer is deadlocked with the two other contenders for the Democratic Party’s nomination, the Democratic Party’s endorsed candidate Margaret Anderson Kelliher and Matt Entenza. These are fluid races in which a quarter or more have not made up their mind and the endorsed Independence Party candidate, Tom Horner, is drawing about 10%. U.S. Senator Amy Klobuchar wins the popularity contest among Minnesota politicians, with a majority favoring her re-election in 2012 while Governor Tim Pawlenty’s popularity sank to its lowest level in polling by MPR News/Humphrey and has reached a near record low according to other polls that date back to his 2003 inauguration. The survey was conducted of 701 Minnesota adults between May 13 to May 16, 2010, which follows the endorsing conventions by the three major parties in Minnesota. -

1998 Campaign Finance Summary

STATE OF MINNESOTA CAMPAIGN FINANCE & PUBLIC DISCLOSURE BOARD 1998 CAMPAIGN FINANCE SUMMARY CANDIDATES FOR CONSTITUTIONAL OFFICE AND STATE REPRESENTATIVE STATE SENATE OFFICEHOLDERS OTHER REGISTERED PRINCIPAL CAMPAIGN COMMITTEES POLITICAL PARTY UNITS POLITICAL COMMITTEES AND POLITICAL FUNDS Issued: May 24, 1999 CAMPAIGN FINANCE & PUBLIC DISCLOSURE BOARD First Floor South, Centennial Building 658 Cedar Street St. Paul MN 55155-1603 Telephone: 651/296-5148 or 800/657-3889 Fax: 651/296-1722 TTY: 800/627-3529, ask for 296-5148 Email: [email protected] Worldwide web site: http://www.cfboard.state.mn.us EXECUTIVE SUMMARY - ELECTION YEAR 1998 The Campaign Finance and Public Disclosure Board is charged with the administration of the Ethics in Government Act, Minnesota Statutes Chapter 10A. During an election year campaign committees of candidates who file for office are required to file three Reports of Receipts and Expenditures: pre-primary, pre-general, and year-end. Campaign committees of candidates whose office is not up for election and candidates who chose not to file for office file one year-end report. Offices open for election in 1998 were: Constitutional, House of Representatives, and certain Judicial seats. Political party units, political committees, and political funds that attempt to influence state elections also filed pre-primary, pre-general, and year-end reports. This summary is based on reports for election year 1998, as filed with the Board by principal campaign committees of candidates for five constitutional offices (36 candidates filed), 134 state representative seats (290 candidates filed), and by 17 candidates for elective judicial seats. Additionally, this summary includes data supplied by 67 senate officeholders; 8 state judicial officeholders, 384 committees of candidates who did not file for election in 1998; 323 political party committees; and 346 political committees and political funds. -

Congressional Directory MINNESOTA

140 Congressional Directory MINNESOTA MINNESOTA (Population 2000, 4,919,479) SENATORS PAUL D. WELLSTONE, Democrat, of Northfield, MN; born in Washington, DC, July 21, 1944; attended Wakefield and Yorktown High Schools, Arlington, VA; B.A., political science, University of North Carolina, Chapel Hill, 1965; Ph.D., political science, University of North Carolina, Chapel Hill, 1969; professor of political science, Carleton College, Northfield, MN, 1969–90; director, Minnesota Community Energy Program; member, Democratic Farmer Labor Party, and numerous peace and justice organizations; publisher of three books: ‘‘How the Rural Poor Got Power’’, ‘‘Powerline’’ and ‘‘The Conscience of a Liberal Reclaiming the Compas- sionate Agenda’’; published several articles; married to the former Sheila Ison; three children: David, Marcia, and Mark; committees: Agriculture; Foreign Relations; Health, Education, Labor, and Pensions; Indian Affairs; Small Business and Entrepreneurship; Veterans’ Affairs; elected to the U.S. Senate on November 6, 1990; reelected to each succeeding Senate term. Office Listings http://www.senate.gov/∼wellstone [email protected] 136 Hart Senate Office Building, Washington, DC 20510–2303 ............................... (202) 224–5641 Administrative Assistant.—Colin McGinnis. FAX: 224–8438 Office Manager.—Jeffrey Levensaler. Legislative Director.—Brian Ahlberg. Court International Building, 2550 University Avenue West, St. Paul, MN 55114– 1025 .......................................................................................................................... -

STATE of MINNESOTA Office of Governor Mark Dayton 130 State Capitol• 75 Rev

STATE OF MINNESOTA Office of Governor Mark Dayton 130 State Capitol• 75 Rev. Dr. Martin Luther King Jr. Boulevard• Saint Paul, MN 55155 April 4, 2018 The Honorable Thomas D. Homan Acting Director U.S. Immigration and Customs Enforcement 500 12th Street Southwest Washington, DC 20536 Re: Dr. Mzenga Wanyama Alien Number: A070885623 Dear Director Homan: I am writing to request that you use all possible prosecutorial discretion in order to allow Dr. Mzenga Wanyama to remain in the United States. I join in this request with a great many Minnesotans, including Senators Amy Klobuchar and Tina Smith, Congressman Keith Ellison, and Minneapolis Mayor Jacob Frey. Dr. Wanyama is a great asset to Minnesota. He has dedicated himself to teaching the young minds, who attend Augsburg University. His deportation would be a terrible loss to the hundreds of students he influencesand also to his family and friends, who love him. Deporting Dr. Wanyama would disrupt an entire community. Over 15,000 people have signed a petition supporting him, which evidences his wide support. I ask you to use your authority to ensure that Dr. Wanyama can remain in our country. It is my understanding that the focusof your Administration is to deport those, who have committed crimes. Dr. Wanyama has no criminal record. Not only does he pose no threat to this country, but he is also an outstanding contributor to our state. As Governorof Minnesota, I attest that he is fullywelcome here. Please allow him to stay. Governor cc: Dr. Mzenga Wanyama Voice: (651) 201-3400 or (800) 657-3717 Fax: (651) 797-1850 MN Relay (800) 627-3529 Website: http:/ / governor.state.mn. -

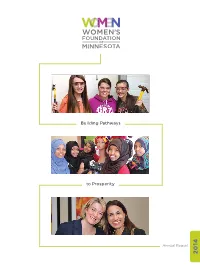

Building Pathways to Prosperity Annual Report

Building Pathways to Prosperity Annual Report 2014 Lee Roper-Batker, Foundation president and CEO, was among a group of key community leaders whose organizations helped move the Women’s Economic Security Act of 2014 through the state Legislature to its signing into state law on Mother’s Day, May 11, 2014. 2 (L-r) Jean Adams and Lee Roper-Batker Dear Friends, second year of multi-year funding (pgs. 4, 6-9). As a key partner of the Women’s Foundation of Through the girlsBEST (girls Building Economic Minnesota, you are integral to our collective Success Together) Fund, we launched a brand new impact toward gender equality – equality that is cohort of 21 grantees, awarding $333,000 for one paved with economic opportunity and ultimately, year of funding (pgs. 4, 12-15). prosperity. It was another landmark year for our MN Girls What is the groundwork we must lay to Are Not For Sale campaign, one where we build pathways to economic opportunity and witnessed a true sea-change in our statewide prosperity for women? communities’ response to child sex trafficking. We’ve changed laws, increased housing, funded Every programmatic decision we make and research, and mobilized the public against child strategic direction we take begins with this sex trafficking. Through MN Girls, we awarded question and goal in mind. To get there, the dreams $405,000 in grants to 13 organizations focused we all share for women’s economic opportunity, on advocacy, housing, and demand (pgs. 4, 10-11). safety, health and reproductive rights, and leadership serves as our beacon, lighting the way. -

Why Are the Twin Cities So Segregated?

Why Are the Twin Cities So Segregated? February, 2015 Executive Summary Why are the Twin Cities so segregated? The Minneapolis-Saint Paul metropolitan area is known for its progressive politics and forward-thinking approach to regional planning, but these features have not prevented the formation of the some of the nation’s widest racial disparities, and the nation’s worst segregation in a predominantly white area. On measures of educational and residential integration, the Twin Cities region has rapidly diverged from other regions with similar demographics, such as Portland or Seattle. Since the start of the twenty-first century, the number of severely segregated schools in the Twin Cities area has increased more than seven- fold; the population of segregated, high-poverty neighborhoods has tripled. The concentration of black families in low-income areas has grown for over a decade; in Portland and Seattle, it has declined. In 2010, the region had 83 schools made up of 90 percent nonwhite students. Portland had two. The following report explains this paradox. In doing so, it broadly describes the history and structure of two growing industry pressure groups within the Twin Cities political scene: the poverty housing industry (PHI) and the poverty education complex (PEC). It shows how these powerful special interests have worked with local, regional, and state government to preserve the segregated status quo, and in the process have undermined school integration and sabotaged the nation’s most effective regional housing integration program and. Finally, in what should serve as a call to action on civil rights, this report demonstrates how even moderate efforts to achieve racial integration could have dramatically reduced regional segregation and the associated racial disparities. -

Editor's Note

Editor’s notE Editor Laura Weber Design and Typesetting Percolator “More than entertainment” mnhs.org/mnhistory Minnesota History (ISSN 00265497) (USPS 351660) In Minnesota History’s first hundred years, only seven individuals held published quarterly, copyright 2018 by the Minne- sota Historical Society, 345 Kellogg Blvd West, the title of editor. Solon J. Buck founded the periodical in 1915. He was St Paul, MN 55102-1906. Periodicals postage paid succeeded by another distinguished historian, Theodore Blegen, who at St Paul, MN. held the position of editor from 1923 to 1939. The redoubtable Bertha Postmaster: Send address changes to Membership Heilbron then wielded the blue pencil for two decades, retiring in 1961. Office, 345 Kellogg Blvd West, St Paul, MN 55102- 1906. Each year, the periodical considers articles for awards named after its first two editors: the Buck Award for best article published in the Membership in MNHS includes a subscription to Minnesota History. Basic individual memberships are previous calendar year by an author not on the MNHS staff; the Blegen $50; for more information, write the Member ship Award for best article written by a staff member. The first recipient Office at the address above or at membership@ mnhs.org or call 651-259-3131. of the latter (for an article she wrote on the fur trade) was Minnesota History’s fourth editor, Rhoda Gilman. Her death this spring at the age Back issues of Minnesota History are $5 each plus Minnesota tax and handling; go to mnhs.org of 91 prompted this foray into editorial genealogy. /mnhistory. Gilman began her distinguished career at the Minnesota Historical Magazine text is available in alternative format: Society in 1958. -

Genealogists' Guide to the West Central Minnesota Historical Center

University of Minnesota Morris Digital Well University of Minnesota Morris Digital Well Miscellaneous Campus Publications UMM Archives 6-2017 Genealogists' Guide to the West Central Minnesota Historical Center Dawn Benson Follow this and additional works at: https://digitalcommons.morris.umn.edu/miscpubs Part of the United States History Commons Recommended Citation Benson, Dawn, "Genealogists' Guide to the West Central Minnesota Historical Center" (2017). Miscellaneous Campus Publications. 19. https://digitalcommons.morris.umn.edu/miscpubs/19 This Report is brought to you for free and open access by the UMM Archives at University of Minnesota Morris Digital Well. It has been accepted for inclusion in Miscellaneous Campus Publications by an authorized administrator of University of Minnesota Morris Digital Well. For more information, please contact [email protected]. Updated June 2017 Genealogists’ Guide to the West Central Minnesota Historical Center By Dawn Benson The Minnesota Regional Research Center Network is a system of regional historical research centers established in the 1970s to meet the need to collect historical records and recollections. The center at the University of Minnesota Morris collects primary history sources for the West Central Minnesota area, including the counties of Big Stone, Chippewa, Douglas, Grant, Pope, Stevens, Swift, and Traverse. The primary sources include oral interviews on a wide variety of topics, business, government and institutional records, and the personal papers of individuals. The collections are donations from individuals, businesses, and institutions and are not complete and exhaustive of any topic. The Oral Histories are of particular interest because they represent personal knowledge and memories which may not otherwise be available. -

History of the Item Veto in Minnesota

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Joel Michael, Legislative Analyst Updated: September 2018 History of the Item Veto in Minnesota This information brief provides a history of the Minnesota item veto power—the constitutional power of governors to veto items of appropriations in bills containing multiple appropriations, while approving the rest of the bill. The brief describes the 1876 amendment that established the item veto, the unsuccessful attempt to expand the item veto power in 1915, the use of the item veto by Minnesota governors, and court challenges to use of the item veto. Table of Contents Executive Summary ......................................................................................... 2 The 1876 Item Veto Amendment .................................................................... 4 The 1915 Proposed Amendment ...................................................................... 6 Minnesota Governors’ Use of the Item Veto Power ........................................ 9 Legislative Overrides of Item Vetoes ............................................................ 23 Court Challenges to Item Vetoes ................................................................... 25 Appendix ........................................................................................................ 33 Copies of this publication may be obtained by calling 651-296-6753. This document can be made available in alternative formats for people with disabilities -

State of Minnesota District Court

STATE OF MINNESOTA DISTRICT COURT COUNTY OF HENNEPIN FOURTH JUDICIAL DISTRICT Case Type: Other Civil Alejandro Cruz-Guzman, as guardian and Court File No. next friend of his minor children; Me’Lea Connelly, as guardian and next friend of her minor children; Ke’Aundra Johnson, as guardian and next friend of her minor child; Izreal Muhammad, as guardian and next friend of his minor children; Roxxanne O’Brien, as guardian and next friend of her minor children; Diwin O’Neal Daley, as guardian and next friend of his minor children; Lawrence Lee, as guardian and next friend of his minor child; and One Family One Community, a Minnesota non-profit corporation, Plaintiffs, CLASS ACTION COMPLAINT vs. State of Minnesota; Mark Dayton, Governor, State of Minnesota; Minnesota Department of Education; Dr. Brenda Cassellius, Commissioner, Minnesota Department of Education; Minnesota Senate; Sandra L. Pappas, President of the Minnesota Senate; Minnesota House of Representatives; Kurt Daudt, Speaker of the Minnesota House of Representatives, Defendants. Plaintiffs above-named, for their complaint against defendants above-named, complain and allege as follows: NATURE OF ACTION 1. Plaintiffs above-named, parents, as guardians and next friends of children enrolled, or expected to be enrolled during the pendency of this action, in the Minneapolis Public Schools, Special School District No. 1, and the Saint Paul Public Schools, Independent School District 625, bring this lawsuit in order to redress the denial to them by the defendants of the fundamental right of the plaintiffs to receive an adequate education, a right secured to the plaintiff class by the Education Clause of the Minnesota Constitution, Article XIII, Section 1, by the Equal Protection Clause of the Minnesota State Constitution, Article I, Section 2, and by the Due Process Clause of the Minnesota Constitution, Article I, Section 7. -

Federal Government President of the United States

Chapter Eight Federal Government President of the United States .......................................................................466 Vice President of the United States ................................................................466 President’s Cabinet .........................................................................................466 Minnesota’s U.S. Senators .............................................................................467 Minnesota Congressional District Map ..........................................................468 Minnesota’s U.S. Representatives ..................................................................469 Minnesotans in Congress Since Statehood .....................................................472 Supreme Court of the United States ...............................................................477 Minnesotans on U.S. Supreme Court Since Statehood ..................................477 U.S. Court of Appeals .....................................................................................478 U.S. District Court .........................................................................................478 Office of the U.S. Attorney ............................................................................479 Presidents and Vice Presidents of the United States ......................................480 Federal Government PRESIDENT OF THE UNITED STATES Donald J. Trump (Republican) 45th President of the United States Elected: 2016 Term: Four years Term expires: January 2021 Salary: $400,000 -

State of the State Address Governor Mark Dayton: Wednesday, February 09, 2011

State of the State Address Governor Mark Dayton: Wednesday, February 09, 2011 A FIVE-POINT PLAN FOR MINNESOTA’S FUTURE PROSPERITY On January 29, 2002, as a Minnesota Senator, I attended President George W. Bush’s first State of the Union address. It occurred just four months after the terrible events of September 11, 2001. He began with these words. “As we gather tonight, our nation is at war, our economy is in recession and the civilized world faces unprecedented dangers. Yet the state of our union has never been stronger.” The President’s words rang true. On the night of 9/11, I had joined with other Members of Congress on the steps of the United States Capitol, which had been spared destruction that day by the heroic actions of passengers aboard United Flight #93, led by Minnesota native Thomas Burnet, Jr. We gathered, not as Republicans or Democrats, but as Americans. We wanted to show our nation and the world that, despite the day’s horrors, our country stood strong, our leaders were united, and our government was working . together. A few days later, we went together to the Pentagon and to Ground Zero. Then I traveled with a small bi-partisan group of Senators to Afghanistan, just after American forces had routed the Taliban and al Qaeda and reopened the American Embassy, though still surrounded by razor wire and Marines. So, when I heard the President’s words, “The state of our union has never been stronger,”I agreed that 9/11’s disaster had united our country, our citizens, and our leaders.