Proposed Acquisition of the Office Components of OUE Downtown and Rights Issue

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Clinics in Downtown Core Open on Friday 24 Jan 2020

LIST OF CLINICS IN DOWNTOWN CORE OPEN ON FRIDAY 24 JAN 2020 POSTAL S/N NAME OF CLINIC BLOCK STREET NAME LEVEL UNIT BUILDING TEL OPENING HOURS CODE 1 ACUMED MEDICAL GROUP 16 COLLYER QUAY 02 03 INCOME AT RAFFLES 049318 65327766 8.30AM-12.30PM 2 AQUILA MEDICAL 160 ROBINSON ROAD 05 01 SINGAPORE BUSINESS FEDERATION CENTER 068914 69572826 11.00AM- 8.00PM 3 AYE METTA CLINIC PTE. LTD. 111 NORTH BRIDGE ROAD 04 36A PENINSULA PLAZA 179098 63370504 2.30PM-7.00PM 4 CAPITAL MEDICAL CENTRE 111 NORTH BRIDGE ROAD 05 18 PENINSULA PLAZA 179098 63335144 4.00PM-6.30PM 5 CITYHEALTH CLINIC & SURGERY 152 BEACH ROAD 03 08 GATEWAY EAST 189721 62995398 8.30AM-12.00PM 6 CITYMED HEALTH ASSOCIATES PTE LTD 19 KEPPEL RD 01 01 JIT POH BUILDING 089058 62262636 9.00AM-12.30PM 7 CLIFFORD DISPENSARY PTE LTD 77 ROBINSON ROAD 06 02 ROBINSON 77 068896 65350371 9.00AM-1.00PM 8 DA CLINIC @ ANSON 10 ANSON ROAD 01 12 INTERNATIONAL PLAZA 079903 65918668 9.00AM-12.00PM 9 DRS SINGH & PARTNERS, RAFFLES CITY MEDICAL CENTRE 252 NORTH BRIDGE RD 02 16 RAFFLES CITY SHOPPING CENTRE 179103 63388883 9.00AM-12.30PM 10 DRS THOMPSON & THOMSON RADLINK MEDICARE 24 RAFFLES PLACE 02 08 CLIFFORD CENTRE 048621 65325376 8.30AM-12.30PM 11 DRS. BAIN + PARTNERS 1 RAFFLES QUAY 09 03 ONE RAFFLES QUAY - NORTH TOWER 048583 65325522 9.00AM-11.00AM 12 DTAP @ DUO MEDICAL CLINIC 7 FRASER STREET B3 17/18 DUO GALLERIA 189356 69261678 9.00AM-3.00PM 13 DTAP @ RAFFLES PLACE 20 CECIL STREET 02 01 PLUS 049705 69261678 8.00AM-3.00PM 14 FULLERTON HEALTH @ OFC 10 COLLYER QUAY 03 08/09 OCEAN FINANCIAL CENTRE 049315 63333636 -

Singapore- Office Q2 2020

M A R K E T B E AT SINGAPORE Office Q2 2020 Singapore Economy Buckles Under Impact of Pandemic 12-Mo. Singapore’s GDP growth turned negative at -0.7% yoy in Q1 2020 as the economy buckled under the impact of the pandemic. Office-using Forecast employment grew by only 2,700 workers during the first quarter, a significant decrease from the 5,800 workers added in the preceding quarter. The $10.37 government is expecting the country to enter its deepest recession ever, with full-year GDP growth in the range of -7.0 to -4.0%. Rent (S$/sf/mo) Leasing Activity Remained Muted With Risk of Long-Term Structural Shift Leasing activity remained muted during the second quarter as brokers were unable to close deals during the circuit breaker period. With remote -2.3% working continuing as the default mode, and corporate occupiers putting the brakes on expansion plans to focus on operational issues arising from Rental Growth the pandemic, future leasing demand in the short-term is likely to remain weak. 2.9% In the long-term, there are concerns that there could be a structural shift in the market if banks and tech firms opt to save on real estate costs and Vacancy Rate let a large proportion of their workforce continue remote working post-pandemic, which could lead to a lower level of office demand. Large tech firms have already made public commitments, with Twitter and Square announcing that all of their employees would be able to work from home indefinitely, while Facebook unveiled a plan for up to half of its 48,000 workers to telecommute permanently within the decade. -

POISED for a GRADUAL RECOVERY Senior Associate Director | Research | Singapore +65 6531 8567 [email protected]

COLLIERS QUARTERLY OFFICE | SINGAPORE | RESEARCH | Q4 2020 | 14 JANUARY 2021 Shirley Wong POISED FOR A GRADUAL RECOVERY Senior Associate Director | Research | Singapore +65 6531 8567 [email protected] Tricia Song 2021–25 Director and Head | Research | Insights & Q4 2020 Full Year 2021 Annual Average Singapore > CBD Grade A office showed resilience with +65 6531 8536 Recommendations [email protected] 336,900 sq ft net absorption in 2020 despite CBD Grade A rents declined 2.1% GDP contraction of 5.8%, driven by previous QOQ in Q4 2020 and 5.4%* for Demand flexible workspace commitments. In 2021, -59,600 sq ft 787,900 sq ft 894,000 sq ft the full year to SGD9.57 (USD7.24) we expect technology to drive demand. per sq foot, on weak global > We expect relatively muted CBD Grade A economic conditions. We forecast supply in 2021-2022, with annual expansion rents to grow 5.5% by the end of averaging 2.6% of stock versus 4.7% for the 0 sq ft 783,900 sq ft 883,000 sq ft 2021, on an eventual economic Supply last five years. 2023 should see higher supply rebound and benign supply. at 4.5% of stock. We forecast new demand in 2021 Annual Average to be driven by the technology QOQ / YOY / Growth 2021–25 / End Q4 End 2021 End 2025 sector. Meanwhile, Q4 2020 CBD > CBD Grade A rents declined 2.1% in Q4 2020 Grade A vacancy of 5.2% (+1.8pp 1.0pp-2.1%* +3.7% and 5.4%* for the full year to SGD9.57 5.5% YOY) could tighten over the next (USD7.24) per sq foot. -

AXA Insurance Pte Ltd Company Reg No. 199903512M 8 Shenton Way, #24-01, AXA Tower Singapore 068811 Thank You for Investing with AXA

03/2018 AXA Insurance Pte Ltd Company Reg No. 199903512M 8 Shenton Way, #24-01, AXA Tower Singapore 068811 Thank you for investing with AXA We are pleased to present to you the Annual Report of AXA Pulsar, AXA Polaris and AXA Optimus range of sub-funds for the 12 months ending 31 December 2017. Bullish markets with low volatility 2017 was considered a very good year for investments in general as stock markets around the world had strong returns with very low volatility. Worries over the new US President Donald Trump initiating trade protectionist measures simmered down as he focused more on immigration measures and verbal sparring with the North Koreans. Economies around the world also reported generally better growth than previous years with unemployment numbers falling. Inflation remained weaker than expected, likely due to slow wage increases and technology disruptions bringing down costs. Global equity markets had another good year (MSCI World was up about 14% in Singapore dollar terms) with the European markets driving the best returns in Singapore dollar terms. Emerging markets have outperformed global markets in 2017 as economic growth in this region is improving as well (MSCI Emerging Markets was up more than 27% in Singapore dollar terms with China being the main contributor). Fixed income markets on the other hand continue to face challenges with the anticipation of more Federal Reserve rate hikes and the gradual ending of Quantitative Easing by the other developed nations. Government bonds were mainly flat while bonds with higher risks delivered low positive returns. We are pleased to share that our fixed income delivered mostly positive returns ranging from -2% to 11% while our mixed assets funds delivered positive returns from 4% to 12% (all in Singapore dollar terms). -

A Review of the Singapore Office Market

Singapore Q1/Q2 2019 Published 1st March 2019 Singapore | Hong Kong The Office A review of the Singapore office market Index P2 Building Rental Table (Islandwide) P3 Leasing Options – New Downtown & Economy Range P4 Demand – who is moving where P5 Featured New Development – 9 Penang Road P6 Special Feature – Co-working space P7 Leasing Options – Raffles Place & Tanjong Pagar P8 Supply / Rentals / Forecast Corporate Locations (S) Pte Ltd License No. L3010044A Marina One T +65 6320 8355 / [email protected] / www.corporatelocations.com.sg RENTAL GUIDE 1st March 2019 Summary of Asking Rates Raffles Place / New Downtown Bangkok Bank Building TBA City Hall / Marina Centre / Beach Rd Chinatown / River Valley Road BEA Building $7.50 18 Robinson $12.00 Capital Tower $10.00 11 Beach Road Full Central Mall $7.00 20 Collyer Quay $11.00-$13.00 Cecil Court $5.80 30 Hill Street Full CES Centre $5.50+ 55 Market Street $7.00 China Square Central $8.50 Beach Centre $7.80 Chinatown Point $6.50 6 Battery Road $14.00 City House $7.80+ Bugis Junction Towers $7.80 Great World City $7.00 Asia Square T1 & T2 $14.00 Far East Finance Bldg $7.00 Centennial Tower $14.80 Kings Centre $7.00 Bank of China Building Full Far Eastern Bank Bildg Full Duo Tower $10.50 The Central $9.80 Bank of Singapore Centre $9.50 GB Building $6.00+ Funan $9.00 UE Square $8.00 Bharat Building $6.50 Keck Seng Tower $6.00 Manulife Centre $10.00+ Valley Point $7.00 CapitaGreen $13.50 Manulife Tower $9.50 Millenia Tower $14.80 Capital Square Full MYP Plaza $7.00 Odeon Tower -

Stay Fit & Feel Good Memorable Events at The

INTEGRATED DINING DESTINATION SINGAPORE ISLAND MAP STAY FIT & FEEL GOOD Food warms the soul and we promise that it is always a lavish gastronomic experience Relax after a day of conference meeting or sightseeing. Stay in shape at our 24-hour gymnasium, at the Grand Copthorne Waterfront Hotel. have a leisurely swim in the pool, challenge your travel buddies to a game of tennis or soothe your muscles in the outdoor jacuzzi. MALAYSIA SEMBAWANG SHIPYARD NORTHERN NS11 Pulau MALAYSIA SEMBAWANG SEMBAWANG Seletar WOODLANDS WOODLANDS SUNGEI BULOH WETLAND CHECKPOINT TRAIN CHECKPOINT RESERVE NS10 ADMIRALTY NS8 NS9 MARSILING WOODLANDS YISHUN SINGAPORE NS13 TURF CLUB WOODLANDS YISHUN Pulau SARIMBUN SELETAR RESERVOIR EXPRESSWAY Punggol KRANJI NS7 Barat KRANJI Pulau BUKIT TIMAH JALAN Punggol NS14 KHATIB KAYU Timor KRANJI Pulau Pulau LIM CHU KANG RESERVOIR SELETAR PUNGGOL Serangoon Tekong KRANJI SINGAPORE RESERVOIR PUNGGOL (Coney Island) WAR ZOO AIRPORT Pulau Ubin MEMORIAL NEE LOWER SELETAR NE17 SOON RESERVOIR PUNGGOL Punggol EXPRESSWAY UPPER NIGHT TAMPINES EXPRESSWAY (TPE) LRT (PG) NS5 SAFARI SELETAR YEW TEE RESERVOIR MEMORABLE EVENTS AT THE WATERFRONT (SLE) SERANGOON NE16 RESERVOIR Bukit Panjang SENGKANG RIVER Sengkang LRT (BP) SAFARI With 33 versatile meeting rooms covering an impressive 850 square metres, SENGKANG LRT (SK) CAFHI JETTY NS4 CHOA CHU YIO CHU CHOA CHU KANG KANG CHANGI the Waterfront Conference Centre truly offers an unparalleled choice of meeting KANG NE15 PASIR NS15 BUANGKOK VILLAGE EASTERN DT1 BUKIT YIO CHU KANG TAMPINES EXPRESSWAY (TPE) BUKIT PANJANG (BKE) RIS Boasting a multi-sensory dining experience, interactive Grissini is a contemporary Italian grill restaurant spaces with natural daylight within one of the best designed conference venues PANJANG HOUGANG (KPE) EW1 CHANGI PASIR RIS VILLAGE buffet restaurant, Food Capital showcases the best specialising in premium meats and seafood prepared in DT2 LOWER NS16 NE14 in the region. -

A Review of the Singapore Office Market

September 2018 Singapore | Hong Kong The Office A review of the Singapore office market Demand / Supply / Rentals / Forecast P2 Four Best Premium Leasing Options P3 Common Myths You Need to Know P3 Six Best Value For Money Opportunities P4 Eight Most Competitive Leasing Options P5 Summary of New Developments 2018 P6 Frequently Asked Questions P6 Complete Rental Table (Islandwide) P7 Four Most Expensive Office Buildings P8 Future Developments P8 Finding Office Space For You, With You Corporate Locations (S) Pte Ltd License No. L3010044A Marina One T +65 6320 8355 / [email protected] / www.corporatelocations.com.sg Demand Rentals A healthy take-up of space in 2018 Top premium asking rates are now around $14.00+ per sq ft The office leasing market has continued its momentum from 2017 and The top premium asking rates are now around $14.00+ per sq ft, with there has indeed been a healthy take-up of space in 2018. Many of the less room to negotiate than before but effective rates are still averaging preferred locations have been busy, whilst some other locations not around $11.50 - $12.00 per sq ft for prime space. As in any strong so active. Last year the talk of the town was all about the new tenants leasing market, the gap between the upper end and lower end tends to relocating to the brand new schemes such as Marina One and UIC stretch, which is exactly what is happening right now. Building. The story this year so far, has been all the new tenants that have committed to Frasers Tower and Duo Tower. -

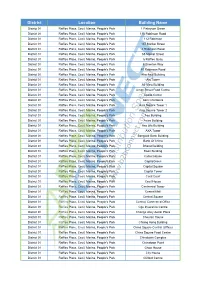

District Location Building Name

District Location Building Name District 01 Raffles Place, Cecil, Marina, People's Park 1 Finlayson Green District 01 Raffles Place, Cecil, Marina, People's Park 110 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park 112 Robinson District 01 Raffles Place, Cecil, Marina, People's Park 137 Market Street District 01 Raffles Place, Cecil, Marina, People's Park 4 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park 55 Market Street District 01 Raffles Place, Cecil, Marina, People's Park 6 Raffles Quay District 01 Raffles Place, Cecil, Marina, People's Park 6 Shenton Way District 01 Raffles Place, Cecil, Marina, People's Park 80 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park Afro-Asia Building District 01 Raffles Place, Cecil, Marina, People's Park Aia Tower District 01 Raffles Place, Cecil, Marina, People's Park Air View Building District 01 Raffles Place, Cecil, Marina, People's Park Amoy Street Food Centre District 01 Raffles Place, Cecil, Marina, People's Park Apollo Center District 01 Raffles Place, Cecil, Marina, People's Park Asia Chambers District 01 Raffles Place, Cecil, Marina, People's Park Asia Square Tower 1 District 01 Raffles Place, Cecil, Marina, People's Park Asia Square Tower 2 District 01 Raffles Place, Cecil, Marina, People's Park Aso Building District 01 Raffles Place, Cecil, Marina, People's Park Aviva Building District 01 Raffles Place, Cecil, Marina, People's Park Axa Life Building District 01 Raffles Place, Cecil, Marina, People's Park AXA Tower District 01 -

2020 MICE Directory

2020 MICE Directory EMPOWERING COMMERCE, CAPABILTIES, COMMUNITY CONTENTS MESSAGES 5 Message from SACEOS President 6 Message from Singapore Tourism Board EVENT CALENDARS 28 Calendar of Conferences 2020 31 Calendar of Exhibitions 2020 36 Calendar of Conferences 2021 38 Calendar of Exhibitions 2021 VENUE 44 Auditorium, Conventions & Exhibitions Centres 57 Hotels 69 Unique Venues DIRECTORY LISTING 81 SACEOS Members Listings 116 General Listings 209 Singapore Statutory Boards & Government Agencies 217 Advertiser’s Index SACEOS DIRECTORY 2020 Message from SACEOS President I Message from Singapore Tourism Board MR ALOYSIUS ARLANDO MS MELISSA OW President Singapore Association of Deputy Chief Executive Convention & Exhibition Singapore Tourism Board Organisers & Suppliers (SACEOS) Welcome to the 2020 edition of MICE e-directory – the industry’s go-to guide. SACEOS is a community-based association of the MICE industry whose members contribute to a rich history of successful corporate events, business meetings and conventions and exhibitions in Singapore. 2019 was another exciting year for Singapore’s business events landscape. The city maintains its momentum as a leading global business events hub, This year in 2020, SACEOS rang in the new decade with a big bang - by unveiling our brand playing host to a vibrant array of business events across various industry PRESIDENT new visual identity, a symbol of transformation, and a timely reflection that represents a hallmark clusters, and keeping its position as Asia Pacific’s leading city in the 2018 for the next phase of our growth, our hope, our unified future. global ranking by the International Congress and Convention Association MESSAGE (ICCA), and top international meeting country since 2013 in the Union of Singapore is a key player in the ASEAN region and the rest of the world. -

Singapore Office Market Review

Q2 2021 Published 8 April 2021 Singapore Office Market Review DEMAND Pg 3 SUPPLY Pg 4 Special Feature: Guoco Midtown Pg 6 New Developments: B1/2 Category Pg 7 Rentals Forecasts Top prime rates for premium Grade A buildings have softened from a • Market still dominated by tech firms and the financial services high of $14.00 per sq ft a year ago, to around $11.50 - $12.00 per sq ft. / investment sector, as well as displaced tenants looking for new Average prime rates in the Raffles Place area are in the region of office premises. $9.50 per sq ft. Office rates in theRobinson Road / Shenton Way area are in the $7.00 - $8.50 per sq ft bracket. • Demand for co-working space to continue with hybrid solutions proving popular. There is not much difference in the rental costs for Tanjong Pagar, which averages around $7.50 per sq ft. City Hall ranges from $7.00 to • Ample choice of supply at the moment and the amount of shadow $9.00 per sq ft and Beach Road averages around $7.25 per sq ft. space is increasing, due to companies rightsizing. There has been little movement on Orchard Road, and as such this • Supply will begin to tighten later in the year. location still enjoys a relatively high occupancy rate. Rents range from $7.50 to $9.50 per sq ft in this district. • Only two sizeable office developments due for completion this year in the CBD (CapitaSpring and Afro-Asia iMark). Edge of CBD like Novena, River Valley Road and decentralized locations like Harbourfront Centre and Paya Lebar Square range from • Rates to soften by 7% across the board, but rate of decline will $6.00 to $7.00 per sq ft. -

Property Portfolio As at 30 June 2019 Integrated Development

CapitaLand Property Portfolio as at 30 June 2019 Integrated Development Values Country City Property Holding Entity/ Fund/ REIT Note Effective Stake (%) Status Tenure Tenure Expiry Lease Type Currency Valuation as at 31 Dec 2018 (million) Valuation as at 30 Jun 2019 (million) GFA (sqm) (Years) China Beijing Raffles City Beijing Raffles City China Income Ventures Limited 1 55.0 Leasehold 2046 Retail RMB 5,932 6,167 110,997 2056 Integrated Use - Chengdu CapitaMall Tianfu CapitaLand Mall China Development Fund III 50.0 Leasehold 2048 Commercial RMB 2,896 2,908 193,851 CapitaMall Tianfu* 2078 Residential - Raffles City Chengdu Raffles City China Income Ventures Limited 1 55.0 Leasehold 2046 RMB 4,378 4,549 237,310 Chongqing Raffles City Chongqing 2 100.0 A Leasehold 2057 Commercial RMB 7,554 8,108 816,105 2087 Residential - Hangzhou Raffles City Hangzhou Raffles City China Income Ventures Limited 1 55.0 Leasehold 2049 RMB 5,675 5,793 296,886 Ningbo Raffles City Ningbo Raffles City China Income Ventures Limited 1 55.0 Leasehold 2047 RMB 2,116 2,168 101,405 Y-Town 100.0 A Leasehold 2057 RMB 80 114 23,662 Shanghai Capital Square 70.0 Leasehold 2052 Retail RMB 2,946 3,002 75,117 2062 Office - CapitaMall Hongkou CapitaLand and CapitaLand Mall China Income Fund I 72.5 Leasehold 2057 RMB 9,090 9,398 205,119 CapitaMall LuOne CapitaLand Mall China Development Fund III 33.0 A Leasehold 2056 RMB 5,202 5,301 131,303 CapitaMall Minhang CapitaLand and CapitaLand Mall China Income Fund II 65.0 Leasehold 2053 RMB 4,750 4,896 146,843 Raffles City · The Bund -

A Review of the Singapore Office Market

November 2014 Singapore | Hong Kong The Office A review of the Singapore office market Demand still healthy Supply tightening Rents firming Index Page 02 Super Savers: $3.00 - $5.00 psf Demand 03 Premium Office Space: $10.00 - $14.00 psf 04 Economy Range: $5.00 - $6.00 psf Rentals 05 Lower Mid-Range: $6.00 - $7.00+ psf Rental History 06 Mid-Range: $7.50 - $8.00 psf Supply / Market Forecast Centennial Tower 07 Upper Mid-Range: $8.00 - $9.00 psf Useful Contacts 08 Rental Guide - Summary of Asking Rates Senior Rentals Team Corporate Locations (S) Pte Ltd License No. L3010044A T +65 6320 8355 / [email protected] / www.corporatelocations.com.sg SUPER SAVERS: Business / Commercial Space $3.00 - $5.00 psf 02 *All rents quoted are estimated target effective rates subject to negotiations and are not the landlords quoted figure Qualification for Business Space East up to $4.00 psf Important Note: to qualify for business space, tenants must be involved with software development, research and development, datacenter management, design functions or customer support services. For industrial space a 60:40 ruling applies where 60% of the space must be used for industrial purposes and 40% can be used for offices. If in doubt checks should be made through the URA providing detailed information of $3.50 - $3.70 psf* $4.00 psf* $3.20 psf* $3.00 psf* your specific operations and use of Units from 1,584 – 27,943 sq ft Units from 2,357 – 8,908 sq ft Units from 1,130 – 52,743 sq ft Units from 1,807 – 12,165 sq ft the premises.