NMBZ Holdings Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

An Assessment of the Causes of Non Performing Loans In

AN ASSESSMENT OF THE CAUSES OF NON PERFORMING LOANS IN TANZANIA COMMERCIAL BANKS: A CASE OF NMB BANK PLC BY Phides Selestine Mchopa A Dissertation Submitted to School of Business in Partial Fulfillment of the Requirements for the Award of Master Degree in Business Administration (MBA - Corporate Management) of Mzumbe University 2013 i CERTIFICATION We, the undersigned, certify that we have read and hereby recommend for acceptance by the Mzumbe University, a dissertation/thesis entitled an assessment of the causes of non-performing loans in Tanzania commercial banks; a case of NMB bank PLC, Kenyatta road branch (Mwanza), in partial/fulfillment of the requirements for award of the degree of Master of Business Administration of Mzumbe University. ____________________________________ Major Supervisor ____________________________________ Internal Examiner Accepted for the Board of School of Business ______________________________________________ DEAN, BOARD OF SCHOOL OF BUSINESS ii DECLARATION AND COPYRIGHT I, Phides Selestine Mchopa, declare that this Dissertation is my own original work and that it has not been presented and will not be presented to any other university for a similar or any other degree award. Signature ___________________________ Date________________________________ © This dissertation is a copyright material protected under the Berne Convention, the Copyright Act 199 and other international and national enactments, in that behalf, on intellectual property. It may not be reproduced by any means in full or in part, except for short extracts in fair dealings, for research or private study, critical scholarly review or discourse with an acknowledgement, without the written permission of Mzumbe University, on behalf of the author. iii ACKNOWLEDGEMENT First of all I would like to express my exceptional thanks to almighty God for energizing me and make me able to fulfill my academic responsibilities. -

Nmb Market Share

2018-19 Annual Report Contents Integrated Report NMB at Glance ................................................................................................................................................................................................................................................................ 5 Introduction ........................................................................................................................................................................................................................................................................... 6 Subsidiaries .......................................................................................................................................................................................................................................................................... 8 Key Highlights ................................................................................................................................................................................................................................................................. 9 Reminiscing the Journey ......................................................................................................................................................................................................................... 10 Milestones .............................................................................................................................................................................................................................................................................. -

Annual Report 2019 NMB Final.Indd

Contents Chairman’s Statement ....................................................................................................................................................................................................................... 3 Directors Report ................................................................................................................................................................................................................................................. 5 CEO’s Message ...................................................................................................................................................................................................................................................... 25 Financial Graphs ............................................................................................................................................................................................................................................. 27 Annual Financial Statements FY 2018-19 NMB Bank Ltd. ....................................................................................................................................................................................................................................................... 33 Annual Financial Statements FY 2018-19 OM Development Bank Ltd................................................................................................................................................................................................ -

IFC Deal Query Based on IFC Investment Services Projects

IFC Deal Query Based on IFC Investment Services Projects Date Disclosed Project Name Project Number Product Line 07/23/2021 DCM UBP Social Bond 44900 Loan 07/07/2021 RATCH Loan 43901 Loan 07/01/2021 HDFC II 44139 Loan 06/30/2021 Erste_CRO_MREL 44745 Loan 06/30/2021 OCB green loan 43733 Loan 06/30/2021 Aspen Pharmacare 45174 Loan 06/29/2021 PSL - Ultratech 45146 Loan 06/28/2021 Banco BV SEF Credit Line 43661 Loan 06/24/2021 CTP Bond 44887 Loan 06/23/2021 WCS COVID NMBTZ 44080 Loan 06/22/2021 NSG RSE FACILITY 45366 Loan 06/15/2021 Axian Togo 44666 Loan Page 1 of 1315 09/29/2021 IFC Deal Query Based on IFC Investment Services Projects Company Name Country Sector UNION BANK OF THE Philippines Financial Institutions PHILIPPINES RH INTERNATIONAL Thailand Infrastructure (SINGAPORE) CORPORATION PTE. LTD. HOUSING DEVELOPMENT India Financial Institutions FINANCE CORPORATION LIMITED ERSTE & Croatia Financial Institutions STEIERMARKISCHE BANK D. D. ORIENT COMMERCIAL Vietnam Financial Institutions JOINT STOCK BANK ASPEN FINANCE South Africa other PROPRIETARY LIMITED PRECIOUS SHIPPING Thailand Infrastructure PUBLIC COMPANY LIMITED BANCO VOTORANTIM S.A. Brazil Financial Institutions CTP N.V. Central Europe Region other NMB BANK PLC Tanzania Financial Institutions NSG UK ENTERPRISES Argentina Manufacturing LIMITED LA SOCIETE HOLDING Togo Telecommunications, Media, and Technology Page 2 of 1315 09/29/2021 IFC Deal Query Based on IFC Investment Services Projects Environmental Category Department Status FI-2 Regional Industry - FIG Asia & Pac Active B Regional -

Annual Report 2018 SCBF Annual Report 2018

Annual Report 2018 SCBF Annual Report 2018 Mission The Swiss Capacity Building Facility is dedicated to promoting responsible financial inclusion that meets the needs of smallholder farmers and small-scale entrepreneurs, especially women and those living in rural areas, to improve their livelihoods and rise out of poverty. Page 2 SCBF Annual Report 2018 Table of Contents 4 Acronyms 5 Message from the SCBF Chair 6 SCBF at a Glance 7 Key Figures 8 Global Perspective 10 Members and Sponsors 11 SCBF Events 13 Outcome Studies 15 SCBF Impact Logic 16 Interventions Approved in 2018 20 Ongoing Interventions 21 Interventions Completed in 2018 Insurance Programmes 24 ACRE, Tanzania - Agricultural Insurance 27 Manushi, Nepal - Life Insurance 29 Enda Tamwheel, Tunisia - Life Insurance 31 Lead Foundation, Egypt - Health Insurance Loan Programmes 33 IMF Hekima, Democratic Republic of the Congo - Housing Finance 35 Swisscontact, El Salvador, Peru and Nicaragua - Microleasing 38 Microfund for Women, Jordan - Refugee Lending 41 Venture South / Biashara na Fedha, Kenya - Solar Lending 44 Sèvis Finansye Fonkoze, Haiti - Rural Lending Financial Education 46 EMI, Laos - Insurance Education 48 Utkarsh Microfinance, India - Rural Education SCBF Management and Finances 49 Institutional Changes and Achievements 50 Strategic Orientation 2019 51 Funding and Contributions 52 Audit Report 2018 Appendices 59 Appendix I Organizational Structure 60 Appendix II Financial Overview Since Inception 61 Appendix III Institutions Supported by the SCBF Since Inception 62 Appendix -

![NMB Bank Limited ICRA Nepal Reaffirms Issuer Rating of [ICRANP-IR] A- and Subordinated Debenture Rating of [ICRANP] LA-; Withdra](https://docslib.b-cdn.net/cover/1471/nmb-bank-limited-icra-nepal-reaffirms-issuer-rating-of-icranp-ir-a-and-subordinated-debenture-rating-of-icranp-la-withdra-3301471.webp)

NMB Bank Limited ICRA Nepal Reaffirms Issuer Rating of [ICRANP-IR] A- and Subordinated Debenture Rating of [ICRANP] LA-; Withdra

NMB Bank Limited ICRA Nepal reaffirms issuer rating of [ICRANP-IR] A- and subordinated debenture rating of [ICRANP] LA-; withdraws ratings assigned to matured debentures April 27, 2021 Summary of rated instruments Facility/Instrument Amount Rating Action (April 2021) Issuer Rating NA [ICRANP-IR] A-; reaffirmed Subordinated debentures (10% NMB Debenture 2085) NPR 1,684.505 million1 [ICRANP] LA-; reaffirmed Subordinated debentures (7% NMB Debenture 2077) NPR 500 million2 [ICRANP] LA-; withdrawn Rating action ICRA Nepal has reaffirmed the rating of [ICRANP-IR] A- (pronounced ICRA NP issuer rating A minus) to NMB Bank Limited (NMB), indicating an adequate degree of safety regarding the timely servicing of financial obligations. Such issuers carry low credit risk. This rating is only an opinion on the general creditworthiness of the rated entity and is not specific to any debt instrument. ICRA Nepal has also reaffirmed the rating of [ICRANP] LA- (pronounced ICRA NP long-term debt rating A minus) to NMB’s existing subordinated3 debenture programme worth ~NPR 1,684.505 million. Instruments with this rating are considered to have an adequate degree of safety regarding the timely servicing of financial obligations. Such instruments carry a low credit risk. ICRA Nepal has withdrawn the rating of [ICRANP] LA- (pronounced ICRA NP L A minus) assigned to NPR 500- millionsubordinated debentures of NMB. The rating assigned to it has been withdrawn upon the maturity of the bonds. The bank, through an electronic mail, has highlighted that ~NPR 0.068 million is pending to be claimed by some individual bondholders and the payable amount has been kept in a separate account. -

The Key to Unlocking Financial Inclusion in Developing Economies

The LEI: The Key to Unlocking Financial Inclusion in Developing Economies Plus: A Spotlight on Africa How LSEG (London Stock Exchange Group), Zimbabwe’s NMB Bank Limited, GLEIF, Cenfri and Cornerstone Advisory Plus are unlocking access to trade finance and boosting economic potential for African businesses. Introduction 65 A 2017 report from the International Finance Corporation (IFC) contends that million firms 65 million firms around the world, including 45 per cent of small to medium sized globally enterprises (SMEs) in developing countries, have an unmet annual total financing need of $5.2 trillion.1 Today’s African economies, for example, suffer from a severe trade finance gap currently estimated to be more than US$81bn.2 including The root of the problem, both for banks seeking to expanding trade finance portfolios and international businesses looking for supply chain partnerships, lies in the need for 45% greater transparency among SMEs. Too many do not possess the business credentials of SMEs in needed to support counterparty due diligence processes and their associated risk developing assessments. countries This is a major obstacle impeding global economic growth. It is felt most acutely in developing economies where it prevents capital from flowing into SMEs, through both unmet annual trade finance and domestic and international partnerships. total financing need of $5.2 trillion The Legal Entity Identifier (LEI) can solve this problem as it enhances transparency in the marketplace and builds greater trust between market participants. This e-book explores how financial institutions and SMEs in developing economies across the world can use the LEI, a globally recognized and standardized form of business ID, to address these problems head-on. -

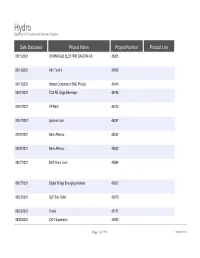

Date Disclosed Project Name Project Number Product Line 09/15/2021 OSMANGAZI ELEKTRIK DAGITIM AS 45265

Hydro Based on IFC Investment Services Projects Date Disclosed Project Name Project Number Product Line 09/15/2021 OSMANGAZI ELEKTRIK DAGITIM AS 45265 09/13/2021 A91 Fund II 45858 09/13/2021 Khaadi Corporation SMC Pvt Ltd 45445 09/07/2021 FCS RE Kings Beverage 44796 09/07/2021 AP Bank 45736 09/07/2021 Ipoteka Loan 45287 09/02/2021 Bank Alliance 45832 09/02/2021 Bank Alliance 45832 08/27/2021 BOP Omni Loan 43584 08/27/2021 Digital Bridge Emerging Markets 45362 08/23/2021 GyT Sub. Debt 43670 08/23/2021 Toters 45171 08/20/2021 CIDT Expansion 45030 Page 1 of 1790 09/24/2021 Hydro Based on IFC Investment Services Projects Company Name Country Sector OSMANGAZI ELEKTRIK Turkey Infrastructure DAGITIM AS A91 EMERGING FUND II India Funds LLP KHAADI SMC PVT. LTD. Pakistan Tourism, Retail, and Property KINGS BEVERAGES PVT Sierra Leone Agribusiness and Forestry LIMITED AGROPROSPERIS BANK, Ukraine Financial Institutions PAT IPOTEKA BANK JSC Uzbekistan Financial Institutions MORTGAGE BANK BANK ALLIANCE PUBLIC Ukraine Financial Institutions JOINT STOCK COMPANY BANK ALLIANCE PUBLIC Ukraine Financial Institutions JOINT STOCK COMPANY Omni S.A Credito Brazil Financial Institutions Financiamento e Investimento DIGITAL COLONY Latin America Region Telecommunications, Media, and Technology ACQUISITIONS BANCO G AND T Guatemala Financial Institutions CONTINENTAL S.A. TAN HOLDING SAL Lebanon Tourism, Retail, and Property COMPAGNIE IVOIRIENNE Cote D'Ivoire Agribusiness and Forestry Page 2 of 1790 09/24/2021 Hydro Based on IFC Investment Services Projects Environmental -

Collect USD Cash at NMB Bank When You Receive Money Via

Enquiries: NMBZ HOLDINGS LIMITED Benefit P Washaya, Chief Executive Officer, NMBZ Holdings Limited [email protected] Benson Ndachena, Chief Finance Officer, NMBZ Holdings Limited [email protected] Website: http://www.nmbz.co.zw Email: [email protected] Telephone: (+263-4) 759 651/9 Cash Guaranteed Collect USD Cash at NMB Bank when you receive money via 31 December 31 December FINANCIAL SUMMARY 2018 2017 CONDENSED AUDITED US$ US$ Total income (US$) 74740671 53606281 CONSOLIDATED Operating profit before impairment charge (US$) 31 155 227 16 870 839 Totalcomprehensiveincome(US$) 21267632 10029136 RESULTS Basic earnings per share (US cents) 5.43 2.58 Dividend per share (US cents) 0.96 0.36 Total deposits (US$) 434957949 348956385 FOR THE YEAR ENDED Totalgrossloansandadvances(US$) 262335026 211005418 Total shareholders’ funds and shareholders’ 31 DECEMBER 2018 liabilities (US$) 79962313 65651843 CHAIRMAN’SCHAIRMAN’S STATEMENTSTATEMENT Capital (continued) TheThe Group’sGroup’s shareholders’shareholders’ fundsfunds andand shareholders’ liabilities have increased by 22% from US$65 651 843 as at 31 INTRODUCTIONINTRODUCTION December 2017 to US$79 962 313 as at 31 December 2018 as a result of the current year’s total comprehensive income. TheThe GroupGroup hashas continuedcontinued inin thethe pursuitpursuit ofof itsits shortshort andand mediummedium termerm goalsgoals andand thethe accompanyingaccompanying resultsresults areare testimonytestimony toto thethe considerableconsiderable progressprogress towardstowards ourour statedstated strategy.strategy. Thehe financialfinancial r resultsesults c continueontinue t too b bee l largelyargely d drivenriven b byy t thehe The Bank’s regulatory capital as at 31 December 2018 was US$74 927 487 and is above the minimum required Bank’sBank’s continuedcontinued diversificationdiversification i intonto t thehe b broaderroader m amarketrket se segmegments,nts, enhancedenhanced useuse ofof thethe bank’sbank’s digitaldigital offerings,offerings, stricterstricter regulatory capital of US$25 million. -

Evaluation of Customer Satisfaction at Nmb Bank Ltd, Nepal

© 2019 JETIR May 2019, Volume 6, Issue 5 www.jetir.org (ISSN-2349-5162) EVALUATION OF CUSTOMER SATISFACTION AT NMB BANK LTD, NEPAL. AUTHOR- RAMESH YADAV, (Roll No – 17301E0036) MBA 2017-2019 Batch. STUDENT AT JAWAHARLAL NEHRU TECHNOLOGICAL UNIVERSITY, KUKATPALLY, HYDERABAD, INDIA Under the guidance of Ms. A. SANTOSH KUMARI, Associate Professor, SMS, JNTUH Abstract Banks are financial institutions on which the economy stands. They cater to the needs of the customer from the individual small saver to huge conglomerates providing services of saving, loan, mortgage etc. Banking is the pillar of every economy providing employment, raising the standard of living and helps to raise the overall growth parameters such as GDP, per capita income etc. Banking as a sector of economy is crucial as it helps to support new firms, give financial support to ailing firms, finance government projects etc. Bank also help legalize the economy and helps use utilize ever depleting funds to finance the economy. Basically, we can say that banking is the link the needy with the one who has spare fund. Finally, it helps to validate the economy. One thing that has remained absolute as a parameter of success of any business irrespective of sector is CUSTOMER SATISFACTION. It represents the sense of gratification a customer feels after utilizing the product or service. Over the years from the beginning of industrial revolution to this digital age the real success of an organization is measured by the level of customer satisfaction and almost all companies from fortune 500 to startups are utilizing customer satisfaction as measure to evaluate success. -

![NMB Bank Limited ICRA Nepal Reaffirms Issuer Rating of [ICRANP-IR]](https://docslib.b-cdn.net/cover/7514/nmb-bank-limited-icra-nepal-reaffirms-issuer-rating-of-icranp-ir-5237514.webp)

NMB Bank Limited ICRA Nepal Reaffirms Issuer Rating of [ICRANP-IR]

NMB Bank Limited ICRA Nepal reaffirms issuer rating of [ICRANP-IR] A- and [ICRANP] LA- to subordinated debentures programme April 27, 2020 Summary of rated instruments Facility/Instrument Amount Rating Action (April 2020) Issuer Rating NA [ICRANP-IR] A-; reaffirmed Subordinated debentures (7% NMB Debenture 2077) NPR 500 million [ICRANP] LA-; reaffirmed Subordinated debentures (10% NMB Debenture 2085) NPR 1,684.505 million1 [ICRANP] LA-; reaffirmed Rating action ICRA Nepal has assigned a rating of [ICRANP-IR] A- (pronounced ICRA NP issuer rating A minus) to NMB Bank Limited (NMB), indicating adequate degree of safety regarding the timely servicing of financial obligations. Such issuers carry low credit risk. This rating is only an opinion on the general creditworthiness of the rated entity and is not specific to any debt instrument. ICRA Nepal has also assigned a rating of [ICRANP] LA- (pronounced ICRA NP long-term debt rating A minus) to NMB’s existing subordinated2 debenture programme worth ~NPR 2,184 million. Instruments with this rating are considered to have an adequate degree of safety regarding the timely servicing of the financial obligations. Such instruments carry a low credit risk. Rationale The assigned ratings continue to derive comfort from NMB’s good ownership profile and its adequate track record in the industry. The ratings also factor in the bank’s growth in the scale of operation and its adequate market share3 in the industry, which is backed by the bank’s increasing footprint across the country (through 163 branch networks as of mid- January 2020). Mergers/acquisition with retail-focussed regional BFIs has increased the granularity of NMB’s credit portfolio, mitigating asset quality concerns arising from simultaneous slippages from large accounts. -

Nmbz Holdings Limited Group Annual Report 31 December

NMBZ HOLDINGS LIMITED GROUP ANNUAL REPORT 31 DECEMBER 2009 CONTENTS Financial Highlights 2 Group Profile 3 Chairman’s Statement 4 - 5 Report of The Directors 6 - 13 Statement of Directors’ Responsibility 14 - 16 Report of the Independent Auditors 17 - 18 Consolidated Statements of Comprehensive Income 19 Consolidated Statements of Financial Position 20 Consolidated Statements of Changes in Equity 21 Consolidated Statements of Cash Flows 22 Accounting Policies 23 - 32 Notes to the Financial Statements 33 - 85 Historical Five Year Financial Summary 86 - 88 Notice to Members 89 Shareholders’ Analysis 90 - 91 Shareholders’ Information 92 Secretary and Registered Office 93 1 HIGHLIGHTS 2009 Attributable profit (US$) 2 278 287 Basic earnings per share (US cents) 0.14 Total deposits (US$) 28 720 120 Shareholders’ funds (US$) 8 363 889 Enquiries: NMBZ HOLDINGS LIMITED Tel: +263-4-759 651/9 Benefit Peter Washaya, Chief Executive Officer [email protected] Benson Ndachena, Chief Financial Officer [email protected] Website: http://www.nmbz.co.zw Email: [email protected] 2 NMBZ HOLDINGS LIMITED GROUP PROFILE year ended 31 December 2009 The NMBZ Holdings Group comprises the company plus the operating subsidiaries, NMB Bank Limited (the Bank) and Stewart Holdings Limited (equity holdings). The Bank was established in 1993 as a bank incorporated under the Companies Act (Chapter 24:03) and is registered as a commercial bank in terms of the Banking Act (Chapter 24:20). It operates through a branch network in Harare, Bulawayo, Mutare and Gweru. The Bank’s branch network is constantly growing to service customers and meet demands in suitable and convenient locations.