Investing in Opportunity

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

REAL ESTATE July 2020

LISTED MARKETS – REAL ESTATE July 2020 Leo Zielinski Partner Tel. +44 (0)7980 809031 [email protected] John Rodgers Partner Tel. +44 (0)7810 307422 [email protected] Will Strachan Partner Tel. +44 (0)7929 885859 [email protected] Lloyd Davies We track the share price movement and regulatory announcements Partner of 57 real estate owning listed entities (“Gerald Eve tracked index”). Tel. +44 (0)7767 311254 A summary of the Gerald Eve tracked index in terms of GAV, NAV, [email protected] LTV, Dividend, Share Price, Market Cap, Discount/Premium to NAV and their respective weekly movement is attached. Lorenzo Solazzo Data Analyst We provide a comparison to share price data from 3 February 2020 Tel. +44 (0)783 309 5582 [email protected] (pre-Covid-19 level) to present day to demonstrate the impact across certain entities as a direct result of Covid-19. James Brown Surveyor As at 30 of June, the Gerald Eve tracked index is currently down 30% to pre- Tel. +44 (0)7464 656563 Covid-19 level, under-performing the FTSE350 which is slowly recovering and is [email protected] now down 16%. The tracked listed REITs share price decreased on average 3% since 1 June 2020 (March: -25%, April: +6%, May: -3%). To provide context around the share price movement, the average discount to NAV is currently 31% against 3% pre-Covid-19. It is unsurprising to note that specialist sector entities across Industrial, Healthcare and Supermarkets have out-performed the REIT universe relative to other strategies within the Gerald Eve tracked index. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Marten & Co / Quoted Data Word Template

Monthly roundup | Real estate August 2020 Kindly sponsored by Aberdeen Standard Investments Winners and losers in July Best performing companies in price terms in July Worst performing companies in price terms in July (%) (%) AEW UK REIT 18.9 Hammerson (20.0) UK Commercial Property REIT 14.9 Countryside Properties (14.4) Schroder REIT 14.5 U and I Group (14.0) Empiric Student Property 11.4 Real Estate Investors (13.4) Palace Capital 10.6 Tritax EuroBox (11.8) LondonMetric Property 9.7 St Modwen Properties (10.9) Triple Point Social Housing REIT 9.2 Drum Income Plus REIT (10.0) RDI REIT 8.5 Alternative Income REIT (8.4) SEGRO 8.3 Panther Securities (8.2) CLS Holdings 5.5 BMO Commercial Property Trust (7.1) Source: Bloomberg, Marten & Co Source: Bloomberg, Marten & Co. AEW UK REIT share price YTD A number of REITs Hammerson share price YTD Retail landlord and property Hammerson continued 110 companies saw big 300 to see its share price 95 255 share price gains 210 fall during July and has 80 over the month of 165 now lost 79.2% of its 120 65 July as covid-19 value in the year to 75 50 restrictions started to 30 date – the worst in the Dec Jan Feb Mar Apr May Jun Jul ease across the UK Dec Jan Feb Mar Apr May Jun Jul real estate sector. The Source: Bloomberg, Marten & Co and greater Source: Bloomberg, Marten & Co company, which owns economic stimulus shopping centres, retail was revealed. The biggest mover was AEW UK REIT. -

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Custodian REIT CREI Real Estate Investment Trusts — GBP 0.885 at close 03 August 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 03-Aug-2020 03-Aug-2020 03-Aug-2020 1.2 105 130 1D WTD MTD YTD Absolute -0.6 -0.6 -0.6 -22.4 100 Rel.Sector -0.5 -0.5 -0.5 2.2 1.1 120 Rel.Market -2.6 -2.6 -2.6 -2.7 95 1 110 VALUATION 90 Trailing Relative Price Relative 0.9 Price Relative 100 85 PE 16.1 Absolute Price (local currency) (local Price Absolute EV/EBITDA 15.8 0.8 90 80 PB 0.9 PCF 12.0 0.7 75 80 Div Yield 6.8 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Price/Sales 8.6 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.3 90 100 100 Div Payout +ve 80 90 90 ROE 5.6 80 70 80 Share Index) Share 70 Share Sector) Share - - 70 60 60 DESCRIPTION 60 50 50 50 40 The Company is a real estate investment trust. 40 RSI RSI (Absolute) 40 30 30 30 20 20 20 10 RSI (Relative to FTSE UKFTSE All to RSI (Relative RSI (Relative to FTSE UKFTSE All to RSI (Relative 10 10 0 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Past performance is no guarantee of future results. -

Industrial & Logistics Viewpoint

INDUSTRIAL & LOGISTICS VIEWPOINT 2020 UK CONTENTS FOREWORD 4 NATIONAL MARKET 6 LONDON & THE SOUTH EAST 8 WEST LONDON 10 SOUTH WEST 12 MIDLANDS 14 NORTH WEST 16 YORKSHIRE & THE NORTH EAST 18 SCOTLAND 20 NORTHERN IRELAND 22 CAPITAL MARKETS 24 2 3 We are pleased to launch our new Industrial and Logistics Viewpoint 2020, which is designed to give you an overview of national and regional activity. Despite the political and economic uncertainty that many businesses in the UK faced in 2019, the Industrial and Logistics sector has remained resilient. Some of the key findings of this Viewpoint include: • Demand for industrial and logistics space in 2019 remained strong with take-up reaching in excess of 30m sq ft for the year, exceeding the 10-year annual average by 17%, but 14% below the record breaking 2018 • The industrial sector out-performed all other property asset classes in 2019, partly driven by very strong rental growth in London and key South East locations • Rental growth is expected to moderate in 2020, although logistics units located in heavily populated areas will reach above average returns • At the beginning of the year we were expecting 2020 to be a record year in terms of demand. However, material downside risks associated with the Covid-19 virus may limit the occupational upside. Should the virus run its course in the first half of 2020, we may expect to see a busy second half as occupiers regroup and press ahead with urgent projects For an informal chat, please do not hesitate to get in touch with either myself or one of the team. -

2021 Quarterly Report (Unaudited)

JANUARY 31, 2021 2021 Quarterly Report (Unaudited) iShares Trust Table of Contents Page iShares Cohen & Steers REIT ETF.......................................................................................................................................... 3 iShares Core Dividend Growth ETF ........................................................................................................................................ 5 iShares Core High Dividend ETF............................................................................................................................................ 11 iShares Core U.S. REIT ETF ............................................................................................................................................... 14 iShares Dow Jones U.S. ETF ............................................................................................................................................... 17 iShares Global REIT ETF................................................................................................................................................... 29 iShares International Developed Real Estate ETF............................................................................................................................ 34 iShares International Select Dividend ETF................................................................................................................................... 38 iShares Morningstar Large-Cap ETF ....................................................................................................................................... -

2020 EPRA Annual Report Survey

MAKING THE JUMP 2020 EPRA Annual Report Survey Sustainability Best Practices Recommendations | 2020 EPRA Annual Report Survey | 2 CONTENTS Foreword 3 Scope of the Survey 5 2020 Awards Key Highlights 6 2020 Results Snapshot 7 2020 Award Winners 8 Analysis: Performance Measures 11 Analysis: Overarching Recommendations 13 Awards Methodology 16 Participants List 17 | ©2020 EPRA. All rights reserved. | 2020 EPRA Annual Report Survey | 3 FOREWORD In comparison with last year, 2020 results are extremely encouraging as the number of medals awarded has increased by 28% with 90 awarded companies, including 62 Gold Winners. Dominique Moerenhout - CEO EPRA This year has posed several challenges to our sector but the results To further support our industry to respond to the investment contained in this report demonstrates that the current COVID-19 community’s demand for greater transparency and accessibility crisis has only served to elevate the importance of sustainability of climate related information, EPRA has published this year new commitments. Before getting into the heart of the numbers, I would guidance for listed property companies already reporting against like to congratulate all our Members’ teams who collected data and the sBPR to meet the reporting requirements of the Task Force on coordinated the sBPR reporting, through the current challenges. Climate-related Financial Disclosures (TCFD). We hope the uptake 2020 marks exceptional results with 90 awarded companies, for the TCFD will follow the same path as the EPRA sBPR which have including 62 Gold Winners, representing almost 60% of the not stopped expanding in the last eight years. In view of this year’s responding companies. -

State Street AUT UK Screened (Ex Controversies and CW) Index

Report and Financial Statements For the year ended 31st December 2020 State Street AUT UK Screened (ex Controversies and CW) Index Equity Fund (formerly State Street UK Equity Tracker Fund) State Street AUT UK Screened (ex Controversies and CW) Index Equity Fund Contents Page Manager's Report* 1 Portfolio Statement* 9 Director's Report to Unitholders* 27 Manager's Statement of Responsibilities 28 Statement of the Depositary’s Responsibilities 29 Report of the Depositary to the Unitholders 29 Independent Auditors’ Report 30 Comparative Table* 33 Financial statements: 34 Statement of Total Return 34 Statement of Change in Net Assets Attributable to Unitholders 34 Balance Sheet 35 Notes to the Financial Statements 36 Distribution Tables 48 Directory* 49 Appendix I – Remuneration Policy (Unaudited) 50 Appendix II – Assessment of Value (Unaudited) 52 * These collectively comprise the Manager’s Report. State Street AUT UK Screened (ex Controversies and CW) Index Equity Fund Manager’s Report For the year ended 31st December 2020 Authorised Status The State Street AUT UK Screened (ex Controversies and CW) Index Equity Fund (the “Fund”) is an Authorised Unit Trust Scheme as defined in section 243 of the Financial Services and Markets Act 2000 and it is a UCITS Retail Scheme within the meaning of the FCA Collective Investment Schemes sourcebook. The unitholders are not liable for the debts of the Fund. The Fund's name was changed to State Street AUT UK Screened (ex Controversies and CW) Index Equity Fund on 18th December 2020 (formerly State Street UK Equity Tracker Fund). Investment Objective and Policy The objective of the Fund is to replicate, as closely as possible and on a “gross of fees” basis, the return of the United Kingdom equity market as represented by the FTSE All-Share ex Controversies ex CW Index (the “Index”), net of withholding taxes. -

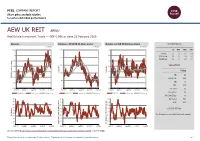

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 21 February 2020 AEW UK REIT AEWU Real Estate Investment Trusts — GBP 0.966 at close 21 February 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 21-Feb-2020 21-Feb-2020 21-Feb-2020 1.02 115 110 1D WTD MTD YTD Absolute -1.2 0.6 -1.8 -2.8 1 108 Rel.Sector -1.2 2.1 -3.9 -2.1 110 Rel.Market -0.8 0.7 -3.6 -1.3 0.98 106 105 VALUATION 0.96 104 Trailing 0.94 102 RelativePrice RelativePrice 100 PE 9.6 Absolute(localPrice currency) 0.92 100 EV/EBITDA 16.5 95 0.9 98 PB 1.0 PCF 11.7 0.88 90 96 Div Yield 6.6 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Price/Sales 8.9 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.3 90 90 90 Div Payout 78.0 80 80 80 ROE 10.5 70 70 70 Share Index) Share Share Sector) Share - 60 - 60 60 DESCRIPTION 50 50 50 40 The Company is a real estate investment company. 40 40 RSI RSI (Absolute) 30 20 30 30 10 20 20 RSI (Relative to FTSE UKFTSE All to RSI (Relative RSI (Relative to FTSE UKFTSE All to RSI (Relative 0 10 10 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 Feb-2019 May-2019 Aug-2019 Nov-2019 Feb-2020 See final page and http://www.londonstockexchange.com/prices-and-markets/stocks/services-stock/ftse-note.htm for further details. -

Ngs Super Portfolio Holdings Disclosure

NGS SUPER PORTFOLIO HOLDINGS DISCLOSURE PROPERTY – INCOME Effective date: 31 DEC 2020 PROPERTY 1 FARRER PLACE, SYDNEY 1 HEYINGTON AVENUE, THOMASTOWN 1 O’CONNELL STREET, SYDNEY 10 SPRING STREET, SYDNEY 101 SECOND STREET SAN FRANCISCO 1101 WESTLAKE AVENUE SEATTLE 131-137 SPRING STREET NEW YORK 139 SPRING STREET, NEW YORK 14-30 PETERKIN STREET, ACACIA RIDGE 15-31 AMERICAIN WAY, DANDENONG SOUTH 16 SPRING STREET, SYDNEY 1776 WILSON1776 WILSON BOULEVARD WASHINGTON DC 1800 LARIMER, DENVER 1937 IPSWICH ROAD, ROCKLEA 206 BELL STREET, SEATTLE 22 BOSTON WHARF RD, BOSTON 2270 BROADWAY AVE. SF EAST BAY 25 CONSTITUTION AVENUE, CANBERRA 25 NORTH, 14901 WASHINGTON STREET, DENVER 2642-2666 IPSWICH ROAD, DARRA 27-39 WHARF ROAD, PORT MELBOURNE 28-40 VELLA DRIVE, SUNSHINE 31-33 CARTER WAY, DANDENONG SOUTH 33 TEHAMA ST SAN FRANCISCO 35 BOUNDARY STREET, SOUTH BRISBANE 407 FIRST AVENUE, NEW YORK 4-10 BRIDGE STREET, PYMBLE 41-71 BESSEMER DRIVE, DANDENONG SOUTH Issued by NGS Super Pty Limited ABN 46 003 491 487 AFSL No 233 154 the trustee of NGS Super ABN 73 549 180 515 ngssuper.com.au 1300 133 177 NGS SUPER – PORTFOLIO HOLDINGS DISCLOSURE 1 PROPERTY – INCOME Effective date: 31 DEC 2020 430 WEST 15TH STREET, 430 W 15TH STREET, NEW YORK 46-50 WIRRAWAY DRIVE, PORT MELBOURNE 485 LA TROBE STREET, MELBOURNE 495-501 BLACKBURN ROAD, MOUNT WAVERLEY 4TH & COLORADO, 407 COLORADO AVENUE, LOS ANGELES 50 JAYCO DRIVE, DANDENONG SOUTH 51ST STREET SELF STORAGE, 1000 50TH STREET, AUSTIN 5250 PARK, 8500 NW 52ND AVE, MIAMI 55 CAMBRIDGE PARKWAY BOSTON 55 KIRBY STREET, RYDALMERE 6 CLARENDON STREET, ARTARMON 631 HOWARD631 HOWARD ST. -

Wilmington Funds Holdings Template DRAFT 04.30.2021.Xlsx

Wilmington Real Asset Fund as of 4/30/2021 (Portfolio composition is subject to change) ISSUER NAME % OF ASSETS DFA COMMODITY STRATEGY PORTFOLIO 15.83% SCHWAB US TIPS ETF 10.16% INVESCO OPTIMUM YIELD DIVERSIFIED COMMODITY STRATEGY NO K-1 ETF 8.73% CREDIT SUISSE COMMODITY RETURN STRATEGY FUND 8.00% VANGUARD COMMODITY STRATEGY FUND 5.44% SCHWAB U.S. REIT ETF 4.53% SPDR S&P GLOBAL NATURAL RESOURCES ETF 4.39% VANGUARD GLOBAL EX-U.S. REAL ESTATE ETF 4.26% PARAMETRIC COMMODITY STRATEGY FUND 3.91% DREYFUS GOVT CASH MGMT-I 3.76% ISHARES GOLD TRUST 3.22% ABERDEEN STANDARD BLOOMBERG ALL COMMODITY STRATEGY K-1 FREE ETF 2.26% TORTOISE MLP & PIPELINE FUND 2.20% PROLOGIS INC 0.96% ISHARES SILVER TRUST 0.75% EQUINIX INC 0.71% DIGITAL REALTY TRUST INC 0.49% PUBLIC STORAGE 0.48% SIMON PROPERTY GROUP INC 0.44% VONOVIA SE 0.41% WELLTOWER INC 0.35% AVALONBAY COMMUNITIES INC 0.30% REALTY INCOME CORP 0.29% EQUITY RESIDENTIAL 0.28% GOODMAN GROUP 0.27% ALEXANDRIA REAL ESTATE EQUITIES INC 0.26% SUN HUNG KAI PROPERTIES LTD 0.25% MITSUBISHI ESTATE CO LTD 0.25% VENTAS INC 0.23% MITSUI FUDOSAN CO LTD 0.23% LINK REIT 0.22% INVITATION HOMES INC 0.22% DEUTSCHE WOHNEN SE 0.22% DAIWA HOUSE INDUSTRY CO LTD 0.22% EXTRA SPACE STORAGE INC 0.22% SUN COMMUNITIES INC 0.21% ESSEX PROPERTY TRUST INC 0.21% MID-AMERICA APARTMENT COMMUNITIES INC 0.20% HEALTHPEAK PROPERTIES INC 0.20% DUKE REALTY CORP 0.19% VICI PROPERTIES INC 0.19% SEGRO PLC 0.18% SUMITOMO REALTY & DEVELOPMENT CO LTD 0.18% CK ASSET HOLDINGS LTD 0.17% BOSTON PROPERTIES INC 0.17% UDR INC 0.14% MEDICAL PROPERTIES TRUST -

What Effect Did the BREXIT Have on the Abnormal Stock Returns of Reits and How Do Different Firm Characteristics Affect This Relationship

What effect did the BREXIT have on the abnormal stock returns of REITs and how do different firm characteristics affect this relationship Bachelor thesis at the University of Amsterdam Thesis supervisor: Mario Bersem Bachelor student: Koen Spelde Student number: 10819606 BsC Economie & Bedrijfskunde Field: Finance & Economics Statement of Originality This document is written by Koen Martijn Spelde who declares to take full responsibility for the contents of this document. I declare that the text and the work presented in this document are original and that no sources other than those mentioned in the text and its references have been used creating it. The Faculty of Economics and Business responsible solely for the supervision of completion of the work, not for the contents. 2 Contents: 1. Introduction 5 2. Literature overview 7 3. Methodology 11 3.1 Event study methodology 11 3.2 Regression analysis methodolgy 15 4. Data 18 5. Results 19 5.1 Event study results 19 5.2 Regression analysis results 23 6. Conclusion 24 7. Appendix 25 8. References 32 3 Abstract: The Brexit outcome affected the stock market on almost every sector both domestically as internationally. In this paper the effect of the Brexit on the real estate sector of the UK is examined. This is done by conducting an event study to test how UK REITS performed during the Brexit. The model used is the market adjusted model and found a negative overall effect of cumulative abnormal returns for the REIT sector and negative significant cumulative abnormal returns for 35 of the 39 REITS. Thereafter a regression analysis is provided to test the relation between the cumulative abnormal return and the market capitalization of the REITS.