Qatar Real Estate Q4, 2019.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1 Population 2019 السكان

!_ اﻻحصاءات السكانية واﻻجتماعية FIRST SECTION POPULATION AND SOCIAL STATISTICS !+ الســكان CHAPTER I POPULATION السكان POPULATION يعتﺮ حجم السكان وتوزيعاته املختلفة وال يعكسها Population size and its distribution as reflected by age and sex structures and geographical الﺮكيب النوي والعمري والتوزيع الجغراي من أهم البيانات distribution, are essential data for the setting up of اﻻحصائية ال يعتمد علا ي التخطيط للتنمية .socio - economic development plans اﻻقتصادية واﻻجتماعية . يحتوى هذا الفصل عى بيانات تتعلق بحجم وتوزيع السكان This Chapter contains data related to size and distribution of population by age groups, sex as well حسب ا ل ن وع وفئات العمر بكل بلدية وكذلك الكثافة as population density per zone and municipality as السكانية لكل بلدية ومنطقة كما عكسا نتائج التعداد ,given by The Simplified Census of Population Housing & Establishments, April 2015. املبسط للسكان واملساكن واملنشآت، أبريل ٢٠١٥ The source of information presented in this chapter مصدر بيانات هذا الفصل التعداد املبسط للسكان is The Simplified Population, Housing & واملساكن واملنشآت، أبريل ٢٠١٥ مقارنة مع بيانات تعداد Establishments Census, April 2015 in comparison ٢٠١٠ with population census 2010 تقدير عدد السكان حسب النوع في منتصف اﻷعوام ١٩٨٦ - ٢٠١٩ POPULATION ESTIMATES BY GENDER AS OF Mid-Year (1986 - 2019) جدول رقم (٥) (TABLE (5 النوع Gender ذكور إناث المجموع Total Females Males السنوات Years ١٩٨٦* 247,852 121,227 369,079 *1986 ١٩٨٦ 250,328 123,067 373,395 1986 ١٩٨٧ 256,844 127,006 383,850 1987 ١٩٨٨ 263,958 131,251 395,209 1988 ١٩٨٩ 271,685 135,886 407,571 1989 ١٩٩٠ 279,800 -

QU Among Top 350 Varsities Worldwide in the World University

02 Thursday, September 3, 2020 Contact US: Qatar Tribune I EDITORIAL I Phone: 40002222 I ADMINISTRATION & MARKETING I Phone: 40002155, 40002122, Fax: 40002235 P.O. Box: 23493, Doha. Quick read FM, US President’S senior adVisor disCuss ties Governor, mayor of Beirut meet Deputy Prime Minister and Amir congratulates Minister of Foreign Affairs HE president of Vietnam Sheikh Mohammed bin Ab- Qatar’s envoy, review damages dulrahman Al Thani met with THE Amir His Highness Senior Advisor to US President Sheikh Tamim bin Hamad Al Jared Kushner in Doha on and losses from port explosion Thani on Wednesday sent a Wednesday. During the meet- QNA The governor and the mayor of Beirut cable of congratulations to ing, they reviewed bilateral rela- DOHA also hailed the humanitarian role played President of Vietnam Nguyen tions between the two countries by Qatar at this time of crisis by sending Phu Trong on his country’s and other issues of common GOVERNOR of Beirut Judge Marwan medical and relief aid. Independence Day. (QNA) concern. The foreign minister Abboud and Mayor of Beirut Munici- Qatar’s ambassador to Lebanon also affirmed Qatar’s position that pality Eng Jamal Itani separately met met with Secretary-General of the High Deputy Amir calls for a just settlement of with Ambassador of Qatar to Leba- Relief Commission Major-General Mo- congratulates the Palestinian issue on the non HE Mohammed Hassan Jaber Al hammed Khair. basis of international legitimacy Jaber. During the meeting, Khair praised Vietnamese president resolutions and the Arab Peace During the meetings, they reviewed the aid and the great support provided THE Deputy Amir His High- Initiative and on the basis of the losses and damages to the buildings, by Qatar to the Lebanese people amid the ness Sheikh Abdullah bin the two-state solution in a way institutions and homes of citizens follow- ordeal faced by them following the port Hamad Al Thani on Wednes- that promotes security and ing the port explosion in Beirut, as well disaster. -

Amir Issues Law on Shura Council Elections

1996 - 2021 SILVER JUBILEE YEAR Turkish Central Athletics stars Bank hikes carry Qatar’s inflation hopes at forecasts for Tokyo 2021-22 Olympics Business | 11 Sport | 16 FRIDAY 30 JULY 2021 20 DHUL-HIJJAH - 1442 VOLUME 26 NUMBER 8698 www.thepeninsula.qa 2 RIYALS Amir issues law on Shura Council elections — DOHA QNA & THE PENINSULA The Shura Council comprises 45 years old, and fluent in Arabic, members, 30 of whom are directly reading, and writing. The law Amir H H Sheikh Tamim bin caps campaign spending at Hamad Al Thani issued Law No. elected in a secret general ballot, QR2m. 6 of 2021 on the issuance of the while the remaining 15 are Candidates must be regis- Shura Council’s Electoral appointed by H H the Amir. tered in the electoral district in System law. The law is effective which he is contesting. starting from its date of issuance Citizens aged 18 and above and whose grandfather They should be of good rep- and is to be published in the was born in Qatar are eligible to vote in districts where utation, good conduct, and official gazette. known for honesty, integrity, their tribe or family reside. H H the Amir also issued a and good manners. decree No. 37 of 2021 defining The candidates must be of Qatari origin and at least 30 Candidates must not have the electoral districts of the years old and fluent in Arabic, reading, and writing. been finally convicted of a Shura Council and their crime against honour or trust respective regions. The law caps campaign spending at QR2m. -

District Energy Space2014

■■ North America District Energy Space 2014 Spotlighting Industry Growth More than 120 million square feet reported District■■ North America Energy Space 2014 Industry Growth around the World Dedicated to the growth and utilization of district energy as a means to enhance energy efficiency, provide more sustainable and reliable energy infrastructure, and contribute to improving the global environment. Established in 1909, the International District Energy Association (IDEA) serves as a vital commu- nications and information hub for the district energy industry, connecting industry professionals and advancing the technology around the world. With headquarters just outside of Boston, Mass., IDEA comprises over 2,000 district heating and cooling system executives, managers, engineers, consultants and equipment suppliers from 23 countries. IDEA supports the growth and utilization of district energy as a means to conserve fuel, increase energy efficiency and resilience, and reduce emissions. The publication of District Energy Space has become an annual tradition for the International District Energy Association since 1990. Each year, IDEA asks all of its member systems in North America (compilation initiated in 1990) and beyond North America (compilation initiated in 2004) to provide information on the number of buildings and their area in square feet that committed or recommitted to district energy service during the previous calendar year. This issue compiles growth that was reported for the calendar year 2014, or previously unreported for recent years. To qualify for consideration in District Energy Space, a renewal would have to be a contracted building or space that had been scheduled to expire and was subject to renewal under a contract with a duration of 10 years or more. -

The Case of Doha, Qatar

Mapping the Growth of an Arabian Gulf Town: the case of Doha, Qatar Part I. The Growth of Doha: Historical and Demographic Framework Introduction In this paper we use GIS to anatomize Doha, from the 1820s to the late 1950s, as a case study of an Arab town, an Islamic town, and a historic Arabian Gulf town. We use the first two terms advisedly, drawing attention to the contrast between the ubiquitous use of these terms versus the almost complete lack of detailed studies of such towns outside North Africa and Syria which might enable a viable definition to be formulated in terms of architecture, layout and spatial syntax. In this paper we intend to begin to provide such data. We do not seek to deny the existence of similarities and structuring principles that cross-cut THE towns and cities of the Arab and Islamic world, but rather to test the concepts, widen the dataset and extend the geographical range of such urban studies, thereby improving our understanding of them. Doha was founded as a pearl fishing town in the early 19th century, flourished during a boom in pearling revenues in the late 19th and early 20th century, and, after a period of economic decline following the collapse of the pearling industry in the 1920s, rapidly expanded and modernized in response to an influx of oil revenues beginning in 1950 (Othman, 1984; Graham, 1978: 255).1 As such it typifies the experience of nearly all Gulf towns, the vast majority of which were also founded in the 18th or early 19th century as pearl fishing settlements, and which experienced the same trajectory of growth, decline and oil-fuelled expansion (Carter 2012: 115-124, 161-169, 275-277).2 Doha is the subject of a multidisciplinary study (The Origins of Doha and Qatar Project), and this paper comprises the first output of this work, which was made possible by NPRP grant no. -

Second Qatari Field Hospital Inaugurated in Beirut

INDEX QATAR 2-4,12 COMMENT 10 BUSINESS | Page 1 QATAR | Page 3 ARAB WORLD 4 BUSINESS 1-8 Qatar’s cost of INTERNATIONAL 5-9, 11 SPORTS 1-8 Ashghal starts living declines DOW JONES QE NYMEX the Roads and 3.41% year-on- Infrastructure 27,931.02 9,602.49 42.16 Project in Al Ebb year in July +34.30 +49.39 -0.08 +0.12% +0.52% -0.19% and Leabaib Latest Figures (Package 4) published in QATAR since 1978 SATURDAY Vol. XXXXI No. 11641 August 15, 2020 Dhul-Hijjah 25, 1441 AH GULF TIMES www. gulf-times.com 2 Riyals Amir, Tunisian leader discuss bilateral ties His Highness the Amir Sheikh Tamim bin Hamad al-Thani Second Qatari held yesterday a telephone conversation with Tunisian President Kais Saied. During the call, they discussed the close bilateral relations between the fi eld hospital two brotherly countries and the prospects for strengthening them, besides regional and international developments of common concern. inaugurated Amir sends greetings to Pakistan president His Highness the Amir Sheikh Tamim bin Hamad al-Thani and His in Beirut Highness the Deputy Amir Sheikh Abdullah bin Hamad al-Thani sent yesterday cables of congratulations QNA diffi cult conditions faced by the health to Pakistan President Dr Arif Alvi Beirut sector in Lebanon due to the Beirut on the anniversary of his country’s Port explosion and the full or partial Independence Day. HE the Prime closure of several hospitals in addition Minister and Minister of Interior n the implementation of the di- to tackling the Covid-19 pandemic. -

Experience Record Important Completed Projects

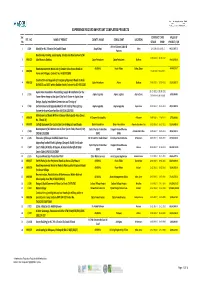

EXPERIENCE RECORD IMPORTANT COMPLETED PROJECTS Ser. CONTRACT DATE VALUE OF REF . NO . NAME OF PROJECT CLIENT'S NAME CONSULTANT LOCATION No STRART FINISH PROJECT / QR Artline & James Cubitt & 1 J/149 Masjid for H.E. Ghanim Bin Saad Al Saad Awqaf Dept. Dafna 12‐10‐2011/31‐10‐2012 68,527,487.70 Partners Road works, Parking, Landscaping, Shades and Development of Al‐ 22‐08‐2010 / 21‐06‐2012 2 MRJ/622 Jabel Area in Dukhan. Qatar Petroleum Qatar Petroleum Dukhan 14,428,932.00 Road Improvement Works out of Greater Doha Access Roads to ASHGHAL Road Affairs Doha, Qatar 48,045,328.17 3 MRJ/082 15‐06‐2010 / 13‐06‐2012 Farms and Villages, Contract No. IA 09/10 C89G Construction and Upgrade of Emergency/Approach Roads to Arab 4 MRJ/619 Qatar Petroleum Atkins Dukhan 27‐06‐2010 / 10‐07‐2012 23,583,833.70 D,FNGLCS and JDGS within Dukhan Fields,Contract No.GC‐09112200 Aspire Zone Foundation Dismantling, Supply & Installation for the 01‐01‐2011 / 30‐06‐2011 5 J / 151 Aspire Logistics Aspire Logistics Aspire Zone 6,550,000.00 Tower Flame Image at the Sport City Torch Tower in Aspire Zone Extension to be issued Design, Supply, Installation.Commission and Testing of 6 J / 155 Enchancement and Upgrade Work for the Field of Play Lighting Aspire Logestics Aspire Logestics Aspire Zone 01‐07‐2011 / 25‐11‐2011 28,832,000.00 System for Aspire Zone Facilities (AF/C/AL 1267/10) Maintenance of Roads Within Al Daayen Municipality Area (Zones 7 MRJ/078 Al Daayen Municipality Al Daayen 19‐08‐2009 / 11‐04‐2011 3,799,000.00 No. -

Download Al Meera Annual Report 2014

Al Meera Consumer Goods Co. (QSC) 2 Al Meera Consumer Goods Co. (QSC) HH Sheikh Tamim Bin Hamad Al Thani Emir of the State of Qatar HH Sheikh Hamad Bin Khalifa Al Thani Father of Emir BOARD OF DIRECTORS 6 Al Meera Consumer Goods Co. (QSC) H.E. Abdullah Bin Khalid Al Qahtani Chairman Dr. Saif Said Al Sowaidi H.E. Dr. Saleh Mohammed Al Nabit Mr. Ahmed Abdullah Al Khulaifi Vice Chairman Board Member Board Member Mr. Mohammad Abdulla Mr. Mohammed Ibrahim Al Sulaiti Mr. Hassan Abdallah Al Mustafawi Al Hashemi Board Member Hassan Ibrahem Al Asmakh Board Member Board Member Annual Report 2014 7 BRANCHES IN QATAR 29 N1 30 15 26 17 25 14 N3 N10 12 27 28 16 11 13 U9 22 10 U10 9 U2 U12 N9 7 24 U3 N7 U4 8 U8 3 4 5 20 6 U7 N2 19 2 U1N8 U5 N6 U13 U14 21 N4 23 31 N5 U6 1 32 Stores33 Location MAP BRANCHES IN DOHA OTHER BRANCHES IN QATAR BRANCHES GPS COORDINATES BRANCHES GPS COORDINATES BRANCHES GPS COORDINATES BRANCHES GPS COORDINATES 0 0 25 19' 54.05” N 0 0 25 16' 23.90” N 0 25 49' 45.20” N 25 13' 51.35” N 0 15 GHARAFAT AL RAYAN 51 25' 41.60” E 25 GHUWAIRIYA 0 1 MAMOURA 510 29' 51.30” E 8 AL MIRQAB 51 29' 29.35” E 51 14' 54.10” E 250 21' 16.74” N 16 AZGHAWA 510 26' 14.07” E 250 42' 52.10” N 250 15' 31.70” N 250 18' 11.91” N 26 RES. -

LUSAIL Rising from the Heart of the Arabian Peninsula, Qatar Has Become a Beacon of Sustainable and Continuous Growth Over the Past Two Decades

MAISONS BLANCHES LUSAIL Rising from the heart of the Arabian Peninsula, Qatar has become a beacon of sustainable and continuous growth over the past two decades. Led by an ambitious Vision 2030, the country offers unparalleled investment opportunities. And with the World Cup 2022 in its sights, the future is progressively looking brighter for Qatar. It has become the oasis that promises to quench the thirst of thinkers, dreamers and investors. Qatar is an international hub connected to the rest of the world through the Hamad International Airport QATAR where business and lifestyle merge into one cohesive environment, a place that moves ahead of the time, but one that remains always true to its heritage and identity. Major projects currently under development such as Lusail City and Qatar Rail will play a significant role in further boosting the country’s position as a global leader in the fields of urban architecture and property Where Luxury is Reinvented development. Maisons Blanches - Lusail Qatar’s ambitious vision to build a new, sustainable city that reflects its modern times resulted in one of the most grandiose projects today: Lusail City. Lusail City, located on the coast, in the northern part of the municipality of Al Daayen, is a city built for the future, introducing a modern, contemporary lifestyle while embracing the environment. The city is expected to accommodate up to 260,000 people and is a key attraction as part of Qatar’s 2022 FIFA World Cup. Lusail City is only 15 km away from the centre of Doha, and will be connected to the capital via the Qatar Rail LUSAIL CITY project, making commuting between the two cities convenient and efficient. -

FIFA Arab Cup to Be a Celebration of Arab Unity, Says Infantino

BUSINESS | Page 1 QATAR | Page 12 QIC Group Q1 net New quarantine guidelines for profi t jumps to people coming QR205mn from 6 countries published in QATAR since 1978 WEDNESDAY Vol. XXXXII No.11897 April 28, 2021 Ramadan 16, 1442 AH GULF TIMES www. gulf-times.com 2 Riyals In brief FIFA Arab Cup to be a celebration Amir, Indian PM discuss ways to fi ght Covid-19 of Arab unity, says Infantino His Highness the Amir Sheikh Tamim bin Hamad al-Thani held yesterday a Draw sets the stage for an exciting FIFA Arab Cup Qatar 2021 telephone conversation with Indian Prime Minister Narendra Modi, By Anil John tastic event, the fi rst of many more to during which they discussed the two Doha come, hopefully,” Infantino said in his countries’ latest eff orts in containing brief address. the novel coronavirus (Covid-19) “The event will prepare Qatar for the pandemic, and ways to enhance he FIFA Arab Cup 2021 in De- World Cup and unite the Arab world’s joint co-operation to contain the cember this year will be a great 450 million people who will cheer and virus and enhance protection Topportunity to unite the Arab cherish and fi nd out which of the 23 against it. World through football besides testing teams is the best in the Arab world,” he In that regard, the Amir expressed Qatar’s operational readiness for the added. Qatar’s solidarity with the Indian prestigious FIFA World Cup in 2022, The FIFA president added that prepa- people, in the eff orts India is the game’s global chief Gianni Infan- rations are on track for Qatar to deliver exerting in facing a new wave of the tino said yesterday. -

Use Outdoor Venues for Gatherings, Says Moph

BUSINESS | Page 3 QATAR | Page 3 Robust sales HMC’s Ambulance expansion in Service registers over private transport, 1.2mn electronic trailers, heavy patient encounters equipment: PSA published in QATAR since 1978 MONDAY Vol. XXXXI No. 11755 December 7, 2020 Rabia II 22, 1442 AH GULF TIMES www. gulf-times.com 2 Riyals Amir holds phone talk Corniche all decked out to welcome National Day with Somali president His Highness the Amir Sheikh Tamim bin Hamad al-Thani held a telephone conversation with Somali Use outdoor President Mohamed Abdullahi Farmaajo yesterday evening. During the phone call which the Amir received from the president of Somalia, they reviewed the bilateral relations and ways to enhance and venues for promote them, in addition to the situation in Somalia and issues of mutual concern. Amir, Moroccan gatherings, king review ties His Highness the Amir Sheikh Tamim bin Hamad al-Thani held a telephone conversation with King Mohamed VI of Morocco yesterday Doha Corniche has been beautifully illuminated in connection with the upcoming Qatar National Day celebrations. Many says MoPH evening. During the phone call buildings across Qatar are decorated with the national flag and in national colours. A night view of the West Bay skyline which the Amir received from the yesterday with illuminated palm trees in the foreground. PICTURE: Thajudheen Page 3 King of Morocco, they reviewed the he Ministry of Public Health try to public places,” it states, adding fraternal relations between the two (MoPH) has advised people to that people should refrain from physi- brotherly countries and prospects Qatar to get vaccine Tuse outdoor venues when pos- cal contact, including handshakes, of strengthening them, as well as sible for social gatherings. -

Prime Minister Opens Al Daayen Naval Base

BUSINESS | Page 1 SPORT | Page 1 England win cricket World Cup in Super QFC bolsters ties with Over key Hong Kong entities drama published in QATAR since 1978 MONDAY Vol. XXXX No. 11245 July 15, 2019 Dhul-Qa’da 12, 1440 AH GULF TIMES www. gulf-times.com 2 Riyals Prime minister opens Al Daayen Naval Base Personnel of the General Directorate of Coasts and Borders Security demonstrate their capabilities after the formal inauguration HE the Prime Minister and Minister of Interior Sheikh Abdullah bin Nasser bin Khalifa al-Thani is briefed about the facilities at the of the Al Daayen Naval Base yesterday. base after he formally inaugurated it yesterday. zGeneral Directorate of Coasts and Borders Security gets state-of-the-art facility to secure maritime borders QNA launched a number of new naval boats Base to enhance safety of whole region: Kuwait US commander lauds security co-operation with Doha belonging to the General Directorate of Coasts and Borders Security. He also Qatar; praises facilities at Al Daayen Naval Base witnessed a presentation by the de- A Kuwaiti security off icial confirmed establishment of such developed naval E the Prime Minister and Min- partment’s search and rescue team. that the Al Daayen Naval Base is a bases, based on modern methods in Commander of the US Naval Forces to enhance security and they have ister of Interior Sheikh Abdul- HE the prime minister toured a new addition to maritime security and marine protection and coast security. Central Command and US 5th Fleet common concerns about maritime Hlah bin Nasser bin Khalifa al- number of new buildings of the de- protection of regional waters from He also praised the naval equipment Vice Admiral James Malloy has security in this region.