Understanding New York City's Budget: a Guide

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2018-2019 Voter Analysis Report

20182019 VOTER ANALYSIS REPORT APRIL 2019 NEW YORK CITY CAMPAIGN FINANCE BOARD Board Chair Frederick P. Schaffer Board Members Gregory T. Camp Richard J. Davis Marianne Spraggins Naomi B. Zauderer Amy M. Loprest Executive Director Roberta Maria Baldini Assistant Executive Director for Campaign Finance Administration Kitty Chan Chief of Staff Daniel Cho Assistant Executive Director for Candidate Guidance and Policy Eric Friedman Assistant Executive Director for Public Affairs Hillary Weisman General Counsel THE VOTER ASSISTANCE ADVISORY COMMITTEE VAAC Chair Naomi B. Zauderer Members Daniele Gerard Joan P. Gibbs Okwudiri Onyedum Arnaldo Segarra Mazeda Akter Uddin Jumaane Williams New York City Public Advocate (Ex-Officio) Michael Ryan Executive Director, New York City Board of Elections (Ex-Officio) The VAAC advises the CFB on voter engagement and recommends legislative and administrative changes to improve NYC elections. 2018–2019 VOTER ANALYSIS REPORT TEAM Lead Editor Gina Chung, Production Editor Lead Writer and Data Analyst Katherine Garrity, Policy and Data Research Analyst Design and Layout Winnie Ng, Art Director Jennifer Sepso, Designer Maps Jaime Anno, Data Manager WELCOME FROM THE VOTER ASSISTANCE ADVISORY COMMITTEE In this report, we take a look back at the past year and the accomplishments and challenges we experienced in our efforts to engage New Yorkers in their elections. Most excitingly, voter turnout and registration rates among New Yorkers rose significantly in 2018 for the first time since 2002, with voters turning out in record- breaking numbers for one of the most dramatic midterm elections in recent memory. Below is a list of our top findings, which we discuss in detail in this report: 1. -

Glossary of Terms for Budget Publications

GLOSSARY OF TERMS ADOPTED EXPENSE AND REVENUE BUDGET: A BUDGET CODE: A 4-character code assigned to a financial plan for the City and its agencies for a fiscal schedule within an agency which identifies the year, setting forth operating expenditures and allocation made in such schedule in terms of its anticipated revenues, following due authorization accounting fund class, unit of appropriation, through the charter-mandated process. responsibility center, control category, local service district and program. ALLOCATION: A sum of money set aside for a specific purpose. BUDGET GAP: The difference between estimated expenditures and revenues for a future fiscal year. ANNUALIZATION: The impact of a new appropriation or expenditure reduction on the basis of a full year. For BUDGET LINE: An identified amount allocated for a instance, if an employee is terminated halfway through specific purpose in the expense budget supporting the fiscal year, the budget reduction in that year will schedules for each budget code within a unit of equal half the employee’s annual salary. The appropriation. Budget lines are used to provide “annualized” reduction is the full amount of the detailed information on the number of positions, titles, employee’s salary. salaries and other expenses in a budget code. ANNUAL RATE: Sum of the salaries paid to the full- BUDGET MODIFICATION: A change in an amount in time active employees in a title description. any budget line during the fiscal year. APPROPRIATION: A general term used to denote the BUDGET STABILIZATION ACCOUNT: An amount authorized in the budget for expenditure by an appropriation which applies excess revenues to prepay agency. -

Libraries Budget Overview MAY 29,2020

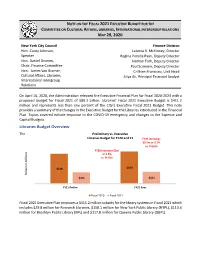

NOTE ON THE FISCAL 2021 EXECUTIVE BUDGET FOR THE COMMITTEE ON CULTURAL AFFAIRS, LIBRARIES, INTERNATIONAL INTERGROUP RELATIONS MAY 29, 2020 New York City Council Finance Division Hon. Corey Johnson, Latonia R. McKinney, Director Speaker Regina Poreda Ryan, Deputy Director Hon. Daniel Dromm, Nathan Toth, Deputy Director Chair, Finance Committee Paul Scimone, Deputy Director Hon. James Van Bramer, Crilhien Francisco, Unit Head Cultural Affairs, Libraries, Aliya Ali, Principal Financial Analyst International Intergroup Relations On April 16, 2020, the Administration released the Executive Financial Plan for Fiscal 2020-2024 with a proposed budget for Fiscal 2021 of $89.3 billion. Libraries’ Fiscal 2021 Executive Budget is $411.2 million and represents less than one percent of the City’s Executive Fiscal 2021 Budget. This note provides a summary of the changes in the Executive Budget for the Libraries introduced in the Financial Plan. Topics covered include response to the COVID-19 emergency and changes to the Expense and Capital Budgets. Libraries Budget Overview The Preliminary vs. Executive Libraries Budget for FY20 and 21 FY21 increases $0.5m or 0.1% vs. Prelim FY20 increases $2m or 0.5% vs. Prelim $428 $430 Dollars in Millions $411 $411 FY21 Prelim FY21 Exec Fiscal 2020 Fiscal 2021 Fiscal 2021 Executive Plan proposes a $411.2 million subsidy for the library systems in Fiscal 2021 which includes $29.8 million for Research Libraries, $150.1 million for New York Public Library (NYPL), $113.4 million for Brooklyn Public Library (BPL) and $117.8 million for Queens Public Library (QBPL). $410.7 Million Executive Plan $411.2 Million Fiscal 2021 Changes Fiscal 2021 Executive Preliminary • Research Libraries: • New Needs: None • Research Libraries: $30.1M • Other Adjustments: $29.9M • NYPL: $149.6M 458,000 • NYPL: $150.1M • BPL: $113.2M • PEGs: None • BPL: $113.4M • QBPL: $117.8M • QBPL: $117.8M Changes introduced in the Executive Plan increase the Libraries budget for Fiscal 2021 by $500,000. -

The Council of the City of New York Office of Council Member Antonio

The Council of the City of New York Office of Council Member Antonio Reynoso 250 Broadway, Suite 1740 NY, New York 10007 May 10th, 2018 Press Release For Immediate Release Kristina Naplatarski [email protected] (347) 581-2050 (C) (212) 788-7095 (O) Council Member Reynoso, East Brooklyn Congregations, and Metro IAF Call Upon the de Blasio Administration to Build More Affordable Senior Housing on Unutilized NYCHA Land May 10th, 2018 —Bushwick, NY— Today, New York City Council Member Antonio Reynoso in conjunction with East Brooklyn Congregations and Metro IAF called upon the de Blasio administration to build more affordable senior housing on vacant NYCHA land. In Mayor Bill de Blasio’s 2014 “Housing New York” plan, the administration promised to increase the supply of housing for seniors by reaching 15,000 households through a combined effort of new construction and preservation. In 2017, the administration doubled this effort, aiming to serve 30,000 units over an extended 12 year period. The administration has made progress towards this goal; several sites throughout the city, including a vacant lot in NYCHA’s Bushwick II campus, are currently in the RFP process and have stipulations for minimum residential senior units. Community members and elected officials called upon the administration to deliver on its promised targets by utilizing additional vacant NYCHA lots throughout the City. However, they stressed that these lots should be dedicated to the construction of deeply affordable and senior targeted units. In light of our City’s rapidly aging population, it is more crucial than ever that we invest in affordable senior housing. -

Preparing a Short-Term Cash Flow Forecast

Preparing a short-term What is a short-term cash How does a short-term cash flow forecast and why is it flow forecast differ from a cash flow forecast important? budget or business plan? 27 April 2020 The COVID-19 crisis has brought the importance of cash flow A short-term cash flow forecast is a forecast of the The income statement or profit and loss account forecasting and management into sharp focus for businesses. cash you have, the cash you expect to receive and in a budget or business plan includes non-cash the cash you expect to pay out of your business over accounting items such as depreciation and accruals This document explores the importance of forecasting, explains a certain period, typically 13 weeks. Fundamentally, for various expenses. The forecast cash flow how it differs from a budget or business plan and offers it’s about having good enough information to give statement contained in these plans is derived from practical tips for preparing a short-term cash flow forecast. you time and money to make the right business the forecast income statement and balance sheet decisions. on an indirect basis and shows the broad categories You can also access this information in podcast form here. of where cash is generated and where cash is spent. Forecasts are important because: They are produced on a monthly or quarterly basis. • They provide visibility of your future cash position In contrast, a short-term cash flow forecast: and highlight if and when your cash position is going to be tight. -

New York City Council Districts and Asian Communities (2018)

New York City Council Districts and Asian Communities (2018) 25, which includes Jackson Heights, Queens; District 38 encompassing Sunset Park, Brooklyn; and As our City Council starts this new term with 11 Introduction District 24, which include parts of Jamaica, Queens. new members and 40 returning members, the Asian American Federation has compiled data from Almost three in four Asian New Yorkers are the 2015 American Community Survey (ACS) on the immigrants. Overall, 26 percent of all immigrants Asian populations for each of the City Council citywide are Asians. Council District 20 has the Districts.1 We will highlight the growth in each highest percent of Asian immigrants among all district’s Asian population and highlight the Asian immigrant populations, accounting for 79 percent languages most commonly spoken in each district. of all immigrants in the district. District 1 has the second largest Asian immigrant population, with 66 percent of all immigrants, followed by District 23 at 60 percent; District 19 at 54 percent; District 38 at The Asian population continues to be the fastest Overall Asian Population 51 percent; and District 43 at 48 percent. growing major race and ethnic group in New York City. According to the most recent Census Bureau As Asian immigrants and their families become population estimates, the Asian population in New more established, they have become a growing part York City reached 1.23 million in 2015, accounting of the potential voter base, comprising 11 percent for nearly 15 percent of the city’s population. of the total voting-age citizen population in New York City. -

Joint Analysis Enacted 2021-22 Budget July 13, 2021

Joint Analysis Enacted 2021-22 Budget July 13, 2021 Table of Contents BACKGROUND ..........................................................................................................3 INTRODUCTION ........................................................................................................3 BUDGET OVERVIEW ..................................................................................................3 Budget Shaped by recovery from covid-related Recession .............................................. 3 Investments focus on relief and recovery for californians................................................ 4 CALIFORNIA COMMUNITY COLLEGES FUNDING ..........................................................5 Immediate Action Package ............................................................................................... 5 Proposition 98 Estimates.................................................................................................. 6 California Community Colleges Funding Levels ............................................................... 6 Changes in Funding .......................................................................................................... 7 Local Support Funding by Program ................................................................................ 17 Capital Outlay ................................................................................................................. 21 State Operations ........................................................................................................... -

Critical Tax Policy: a Pathway to Reform? Nancy J

Northwestern Journal of Law & Social Policy Volume 9 | Issue 2 Article 2 2014 Critical Tax Policy: a Pathway to Reform? Nancy J. Knauer Recommended Citation Nancy J. Knauer, Critical Tax Policy: a Pathway to Reform?, 9 Nw. J. L. & Soc. Pol'y. 206 (2014). http://scholarlycommons.law.northwestern.edu/njlsp/vol9/iss2/2 This Article is brought to you for free and open access by Northwestern University School of Law Scholarly Commons. It has been accepted for inclusion in Northwestern Journal of Law & Social Policy by an authorized administrator of Northwestern University School of Law Scholarly Commons. Copyright 2014 by Northwestern University School of Law Vol. 9, Issue 2 (2014) Northwestern Journal of Law and Social Policy CRITICAL TAX POLICY : A PATHWAY TO REFORM ? ∗ Nancy J. Knauer TABLE OF CONTENTS INTRODUCTION .................................................................................................... 207 I. THE COSTS OF FALSE NEUTRALITY ............................................................... 214 A. All Part of a Larger “Blueprint” ............................................................ 215 B. Hidden Choices and Embedded Values .................................................. 218 Taxpayer neutrality ..................................................................................... 219 Equity and efficiency .................................................................................. 221 C. Critical Tax Theory and Scholarship ...................................................... 223 II. CHOOSING A CRITICAL -

An Overview of Capital Gains Taxes FISCAL Erica York FACT Economist No

An Overview of Capital Gains Taxes FISCAL Erica York FACT Economist No. 649 Apr. 2019 Key Findings • Comparisons of capital gains tax rates and tax rates on labor income should factor in all the layers of taxes that apply to capital gains. • The tax treatment of capital income, such as capital gains, is often viewed as tax-advantaged. However, capital gains taxes place a double-tax on corporate income, and taxpayers have often paid income taxes on the money that they invest. • Capital gains taxes create a bias against saving, which encourages present consumption over saving and leads to a lower level of national income. • The tax code is currently biased against saving and investment; increasing the capital gains tax rate would add to the bias against saving and reduce national income. The Tax Foundation is the nation’s leading independent tax policy research organization. Since 1937, our research, analysis, and experts have informed smarter tax policy at the federal, state, local, and global levels. We are a 501(c)(3) nonprofit organization. ©2019 Tax Foundation Distributed under Creative Commons CC-BY-NC 4.0 Editor, Rachel Shuster Designer, Dan Carvajal Tax Foundation 1325 G Street, NW, Suite 950 Washington, DC 20005 202.464.6200 taxfoundation.org TAX FOUNDATION | 2 Introduction The tax treatment of capital income, such as from capital gains, is often viewed as tax-advantaged. However, viewed in the context of the entire tax system, there is a tax bias against income like capital gains. This is because taxes on saving and investment, like the capital gains tax, represent an additional layer of tax on capital income after the corporate income tax and the individual income tax. -

Voter Analysis Report Campaign Finance Board April 2020

20192020 VOTER ANALYSIS REPORT CAMPAIGN FINANCE BOARD APRIL 2020 NEW YORK CITY CAMPAIGN FINANCE BOARD Board Chair Frederick P. Schaffer Board Members Gregory T. Camp Richard J. Davis Marianne Spraggins Naomi B. Zauderer Amy M. Loprest Executive Director Kitty Chan Chief of Staff Sauda Chapman Assistant Executive Director for Campaign Finance Administration Daniel Cho Assistant Executive Director for Candidate Guidance and Policy Eric Friedman Assistant Executive Director for Public Affairs Hillary Weisman General Counsel THE VOTER ASSISTANCE ADVISORY COMMITTEE VAAC Chair Naomi B. Zauderer Members Daniele Gerard Joan P. Gibbs Christopher Malone Okwudiri Onyedum Mazeda Akter Uddin Jumaane Williams New York City Public Advocate (Ex-Officio) Michael Ryan Executive Director, New York City Board of Elections (Ex-Officio) The VAAC advises the CFB on voter engagement and recommends legislative and administrative changes to improve NYC elections. 2019–2020 NYC VOTES TEAM Public Affairs Partnerships and Outreach Eric Friedman Sabrina Castillo Assistant Executive Director Director for Public Affairs Matthew George-Pitt Amanda Melillo Engagement Coordinator Deputy Director for Public Affairs Sean O'Leary Field Coordinator Marketing and Digital Olivia Brady Communications Youth Coordinator Intern Charlotte Levitt Director Maya Vesneske Youth Coordinator Intern Winnie Ng Art Director Policy and Research Jen Sepso Allie Swatek Graphic Designer Director Crystal Choy Jaime Anno Production Manager Data Manager Chase Gilbert Jordan Pantalone Web Content Manager Intergovernmental Liaison Public Relations NYC Votes Street Team Matt Sollars Olivia Brady Director Adriana Espinal William Fowler Emily O'Hara Public Relations Aide Kevin Suarez Maya Vesneske VOTER ANALYSIS REPORT TABLE OF CONTENTS How COVID-19 is Affecting 2020 Elections VIII Introduction XIV I. -

Alphabets, Letters and Diacritics in European Languages (As They Appear in Geography)

1 Vigleik Leira (Norway): [email protected] Alphabets, Letters and Diacritics in European Languages (as they appear in Geography) To the best of my knowledge English seems to be the only language which makes use of a "clean" Latin alphabet, i.d. there is no use of diacritics or special letters of any kind. All the other languages based on Latin letters employ, to a larger or lesser degree, some diacritics and/or some special letters. The survey below is purely literal. It has nothing to say on the pronunciation of the different letters. Information on the phonetic/phonemic values of the graphic entities must be sought elsewhere, in language specific descriptions. The 26 letters a, b, c, d, e, f, g, h, i, j, k, l, m, n, o, p, q, r, s, t, u, v, w, x, y, z may be considered the standard European alphabet. In this article the word diacritic is used with this meaning: any sign placed above, through or below a standard letter (among the 26 given above); disregarding the cases where the resulting letter (e.g. å in Norwegian) is considered an ordinary letter in the alphabet of the language where it is used. Albanian The alphabet (36 letters): a, b, c, ç, d, dh, e, ë, f, g, gj, h, i, j, k, l, ll, m, n, nj, o, p, q, r, rr, s, sh, t, th, u, v, x, xh, y, z, zh. Missing standard letter: w. Letters with diacritics: ç, ë. Sequences treated as one letter: dh, gj, ll, rr, sh, th, xh, zh. -

Guiding Principles of Good Tax Policy: a Framework for Evaluating Tax Proposals

Tax Policy Concept Statement 1 Guiding principles of good tax policy: A framework for evaluating tax proposals i About the Association of International Certified Professional Accountants The Association of International Certified Professional Accountants (the Association) is the most influential body of professional accountants, combining the strengths of the American Institute of CPAs (AICPA) and The Chartered Institute of Management Accountants (CIMA) to power opportunity, trust and prosperity for people, businesses and economies worldwide. It represents 650,000 members and students in public and management accounting and advocates for the public interest and business sustainability on current and emerging issues. With broad reach, rigor and resources, the Association advances the reputation, employability and quality of CPAs, CGMAs and accounting and finance professionals globally. About the American Institute of CPAs The American Institute of CPAs (AICPA) is the world’s largest member association representing the CPA profession, with more than 418,000 members in 143 countries, and a history of serving the public interest since 1887. AICPA members represent many areas of practice, including business and industry, public practice, government, education and consulting. The AICPA sets ethical standards for its members and U.S. auditing standards for private companies, nonprofit organizations, federal, state and local governments. It develops and grades the Uniform CPA Examination, offers specialized credentials, builds the pipeline of future talent and drives professional competency development to advance the vitality, relevance and quality of the profession. About the Chartered Institute of Management Accountants The Chartered Institute of Management Accountants (CIMA), founded in 1919, is the world’s leading and largest professional body of management accountants, with members and students operating in 176 countries, working at the heart of business.