Annual Monitoring Report 2018 to 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

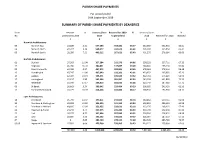

Parish Share Report

PARISH SHARE PAYMENTS For period ended 30th September 2019 SUMMARY OF PARISH SHARE PAYMENTS BY DEANERIES Dean Amount % Deanery Share Received for 2019 % Deanery Share % No Outstanding 2018 2019 to period end 2018 Received for 2018 received £ £ £ £ £ Norwich Archdeaconry 06 Norwich East 23,500 4.41 557,186 354,184 63.57 532,380 322,654 60.61 04 Norwich North 47,317 9.36 508,577 333,671 65.61 505,697 335,854 66.41 05 Norwich South 28,950 7.21 409,212 267,621 65.40 401,270 276,984 69.03 Norfolk Archdeaconry 01 Blofield 37,303 11.04 327,284 212,276 64.86 338,033 227,711 67.36 11 Depwade 46,736 16.20 280,831 137,847 49.09 288,484 155,218 53.80 02 Great Yarmouth 44,786 9.37 467,972 283,804 60.65 478,063 278,114 58.18 13 Humbleyard 47,747 11.00 437,949 192,301 43.91 433,952 205,085 47.26 14 Loddon 62,404 19.34 335,571 165,520 49.32 322,731 174,229 53.99 15 Lothingland 21,237 3.90 562,194 381,997 67.95 545,102 401,890 73.73 16 Redenhall 55,930 17.17 339,813 183,032 53.86 325,740 187,989 57.71 09 St Benet 36,663 9.24 380,642 229,484 60.29 396,955 243,433 61.33 17 Thetford & Rockland 31,271 10.39 314,266 182,806 58.17 300,933 192,966 64.12 Lynn Archdeaconry 18 Breckland 45,799 11.97 397,811 233,505 58.70 382,462 239,714 62.68 20 Burnham & Walsingham 63,028 15.65 396,393 241,163 60.84 402,850 256,123 63.58 12 Dereham in Mitford 43,605 12.03 353,955 223,631 63.18 362,376 208,125 57.43 21 Heacham & Rising 24,243 6.74 377,375 245,242 64.99 359,790 242,156 67.30 22 Holt 28,275 8.55 327,646 207,089 63.21 330,766 214,952 64.99 23 Lynn 10,805 3.30 330,152 196,022 59.37 326,964 187,510 57.35 07 Repps 0 0.00 383,729 278,123 72.48 382,728 285,790 74.67 03 08 Ingworth & Sparham 27,983 6.66 425,260 239,965 56.43 420,215 258,960 61.63 727,583 9.28 7,913,818 4,789,282 60.52 7,837,491 4,895,456 62.46 01/10/2019 NORWICH DIOCESAN BOARD OF FINANCE LTD DEANERY HISTORY REPORT MONTH September YEAR 2019 SUMMARY PARISH 2017 OUTST. -

Contents of Volume 14 Norwich Marriages 1813-37 (Are Distinguished by Letter Code, Given Below) Those from 1801-13 Have Also Been Transcribed and Have No Code

Norfolk Family History Society Norfolk Marriages 1801-1837 The contents of Volume 14 Norwich Marriages 1813-37 (are distinguished by letter code, given below) those from 1801-13 have also been transcribed and have no code. ASt All Saints Hel St. Helen’s MyM St. Mary in the S&J St. Simon & St. And St. Andrew’s Jam St. James’ Marsh Jude Aug St. Augustine’s Jma St. John McC St. Michael Coslany Ste St. Stephen’s Ben St. Benedict’s Maddermarket McP St. Michael at Plea Swi St. Swithen’s JSe St. John Sepulchre McT St. Michael at Thorn Cle St. Clement’s Erh Earlham St. Mary’s Edm St. Edmund’s JTi St. John Timberhill Pau St. Paul’s Etn Eaton St. Andrew’s Eth St. Etheldreda’s Jul St. Julian’s PHu St. Peter Hungate GCo St. George Colegate Law St. Lawrence’s PMa St. Peter Mancroft Hei Heigham St. GTo St. George Mgt St. Margaret’s PpM St. Peter per Bartholomew Tombland MtO St. Martin at Oak Mountergate Lak Lakenham St. John Gil St. Giles’ MtP St. Martin at Palace PSo St. Peter Southgate the Baptist and All Grg St. Gregory’s MyC St. Mary Coslany Sav St. Saviour’s Saints The 25 Suffolk parishes Ashby Burgh Castle (Nfk 1974) Gisleham Kessingland Mutford Barnby Carlton Colville Gorleston (Nfk 1889) Kirkley Oulton Belton (Nfk 1974) Corton Gunton Knettishall Pakefield Blundeston Cove, North Herringfleet Lound Rushmere Bradwell (Nfk 1974) Fritton (Nfk 1974) Hopton (Nfk 1974) Lowestoft Somerleyton The Norfolk parishes 1 Acle 36 Barton Bendish St Andrew 71 Bodham 106 Burlingham St Edmond 141 Colney 2 Alburgh 37 Barton Bendish St Mary 72 Bodney 107 Burlingham -

Kt Pens Parish News Issue 122 MARCH 2021

Kettlestone & Pensthorpe Parish News March 2021 If you would like to include an article for publication in the Parish News, please send your entry by 25th of the previous month to the Editor: [email protected]. To receive future copies of the Parish News electronically, just email your name and address to the Editor. Kettlestone Parish website: https://kettlestoneparishcouncil.norfolkparishes.gov.uk/ David Burgis Climate emergency We were shocked and saddened to hear the news The current COVID-19 pandemic is, no doubt, the that David Burgis passed away at home on 11th defining global health and socio-economic crisis of February. David was born in Manor Farmhouse our time and the greatest challenge we have faced and lived in Kettlestone all his life, firstly in since World War 2. However, we mustn’t lose sight Fulmodeston Road and then at Manor Cottage. He of the even more daunting challenge of global was farm manager at Alethorpe and then for Ralph warming, which is ultimately an existential threat to Harrison and Partners before retiring a few years ago. David was a stalwart member of the Parish the human race. A 4C or 5C warming could Council and the Kettlestone Charity trustees, entail a complete loss of civilisation as we know it. initially joining in the 1980s, and still in post at the Fossil fuels and our unsustainable lifestyle are time of his death. He was a previous Chairman of damaging our planet in irreparable ways, and at the Parish Council, a job he really did not enjoy current levels of carbon dioxide emissions the and was happy to pass on! He had an invaluable carbon budget under the 1.5C limit will be depth of local knowledge and could be relied upon exceeded in less than 8 years. -

North Norfolk District Council (Alby

DEFINITIVE STATEMENT OF PUBLIC RIGHTS OF WAY NORTH NORFOLK DISTRICT VOLUME I PARISH OF ALBY WITH THWAITE Footpath No. 1 (Middle Hill to Aldborough Mill). Starts from Middle Hill and runs north westwards to Aldborough Hill at parish boundary where it joins Footpath No. 12 of Aldborough. Footpath No. 2 (Alby Hill to All Saints' Church). Starts from Alby Hill and runs southwards to enter road opposite All Saints' Church. Footpath No. 3 (Dovehouse Lane to Footpath 13). Starts from Alby Hill and runs northwards, then turning eastwards, crosses Footpath No. 5 then again northwards, and continuing north-eastwards to field gate. Path continues from field gate in a south- easterly direction crossing the end Footpath No. 4 and U14440 continuing until it meets Footpath No.13 at TG 20567/34065. Footpath No. 4 (Park Farm to Sunday School). Starts from Park Farm and runs south westwards to Footpath No. 3 and U14440. Footpath No. 5 (Pack Lane). Starts from the C288 at TG 20237/33581 going in a northerly direction parallel and to the eastern boundary of the cemetery for a distance of approximately 11 metres to TG 20236/33589. Continuing in a westerly direction following the existing path for approximately 34 metres to TG 20201/33589 at the western boundary of the cemetery. Continuing in a generally northerly direction parallel to the western boundary of the cemetery for approximately 23 metres to the field boundary at TG 20206/33611. Continuing in a westerly direction parallel to and to the northern side of the field boundary for a distance of approximately 153 metres to exit onto the U440 road at TG 20054/33633. -

Parish Registers and Transcripts in the Norfolk Record Office

Parish Registers and Transcripts in the Norfolk Record Office This list summarises the Norfolk Record Office’s (NRO’s) holdings of parish (Church of England) registers and of transcripts and other copies of them. Parish Registers The NRO holds registers of baptisms, marriages, burials and banns of marriage for most parishes in the Diocese of Norwich (including Suffolk parishes in and near Lowestoft in the deanery of Lothingland) and part of the Diocese of Ely in south-west Norfolk (parishes in the deanery of Fincham and Feltwell). Some Norfolk parish records remain in the churches, especially more recent registers, which may be still in use. In the extreme west of the county, records for parishes in the deanery of Wisbech Lynn Marshland are deposited in the Wisbech and Fenland Museum, whilst Welney parish records are at the Cambridgeshire Record Office. The covering dates of registers in the following list do not conceal any gaps of more than ten years; for the populous urban parishes (such as Great Yarmouth) smaller gaps are indicated. Whenever microfiche or microfilm copies are available they must be used in place of the original registers, some of which are unfit for production. A few parish registers have been digitally photographed and the images are available on computers in the NRO's searchroom. The digital images were produced as a result of partnership projects with other groups and organizations, so we are not able to supply copies of whole registers (either as hard copies or on CD or in any other digital format), although in most cases we have permission to provide printout copies of individual entries. -

STATEMENT of PERSONS NOMINATED Election of Parish

STATEMENT OF PERSONS NOMINATED North Norfolk Election of Parish Councillors The following is a statement of the persons nominated for election as a Councillor for Aldborough and Thurgarton Reason why Name of Candidate Home Address Description (if any) Name of Proposer no longer nominated* BAILLIE The Bays, Chapel Murat Anne M Tony Road, Thurgarton, Norwich, NR11 7NP ELLIOTT Sunholme, The Elliott Ruth Paul Martin Green, Aldborough, NR11 7AA GALLANT Spring Cottage, The Elliott Paul M David Peter Green, Aldborough, NR11 7AA WHEELER 4 Pipits Meadow, Grieves John B Jean Elizabeth Aldborough, NR11 7NW WORDINGHAM Two Oaks, Freeman James H J Peter Thurgarton Road, Aldborough, NR11 7NY *Decision of the Returning Officer that the nomination is invalid or other reason why a person nominated no longer stands nominated. The persons above against whose name no entry is made in the last column have been and stand validly nominated. Dated: Friday 10 April 2015 Sheila Oxtoby Returning Officer Printed and published by the Returning Officer, Electoral Services, North Norfolk District Council, Holt Road, Cromer, Norfolk, NR27 9EN STATEMENT OF PERSONS NOMINATED North Norfolk Election of Parish Councillors The following is a statement of the persons nominated for election as a Councillor for Antingham Reason why Name of Candidate Home Address Description (if any) Name of Proposer no longer nominated* EVERSON Margra, Southrepps Long Trevor F Graham Fredrick Road, Antingham, North Walsham, NR28 0NP JONES The Old Coach Independent Bacon Robert H Graham House, Antingham Hall, Cromer Road, Antingham, N. Walsham, NR28 0NJ LONG The Old Forge, Everson Graham F Trevor Francis Elderton Lane, Antingham, North Walsham, NR28 0NR LOVE Holly Cottage, McLeod Lynn W Steven Paul Antingham Hill, North Walsham, Norfolk, NR28 0NH PARAMOR Field View, Long Trevor F Stuart John Southrepps Road, Antingham, North Walsham, NR28 0NP *Decision of the Returning Officer that the nomination is invalid or other reason why a person nominated no longer stands nominated. -

CPRE Norfolk Housing Allocation Pledge Signatures – Correct As of 24 March 2021 South Norfolk Alburgh Ashby St Mary Barford &A

CPRE Norfolk Housing Allocation Pledge Signatures – correct as of 24 March 2021 South Norfolk Alburgh Ashby St Mary Barford & Wramplingham Barnham Broom Bawburgh Bergh Apton Bracon Ash and Hethel Brockdish Broome Colney Costessey Cringleford Dickleburgh and Rushall Diss Framingham Pigot Forncett Gissing Great Melton Hempnall Hethersett Hingham Keswick and Intwood Kirby Cane and Ellingham Langley with Hardley Marlingford and Colton Mulbarton Rockland St Mary with Hellington Saxlingham Nethergate Scole Shelfanger Shelton and Hardwick Shotesham Stockton Surlingham Thurlton Thurton Thwaite St Mary Tivetshall St Margaret Tivetshall St Mary Trowse with Newton Winfarthing Wreningham Broadland Acle Attlebridge Beighton Blofield Brandiston Buxton with Lamas Cantley, Limpenhoe and Southwood Coltishall Drayton Felthorpe Frettenham Great Witchingham Hainford Hemblington Hevingham Honingham Horsford Horsham St Faiths Lingwood and Burlingham Reedham Reepham Ringland Salhouse Stratton Strawless Strumpshaw Swannington with Alderford and Little Witchingham Upton with Fishley Weston Longville Wood Dalling Woodbastwick Total = 72 Total parishes in Broadland & South Norfolk = 181 % signed = 39.8% Breckland Ashill Banham Bintree Carbrooke Caston Colkirk Cranworth East Tuddenham Foulden Garveston, Reymerston & Thuxton Gooderstone Great Ellingham Harling Hockering Lyng Merton Mundford North Tuddenham Ovington Rocklands Roudham & Larling Saham Toney Scoulton Stow Bedon & Breckles Swaffham Weeting with Broomhill Whinburgh & Westfield Wretham Yaxham Great Yarmouth -

Five-Year Supply of Housing Land 2020 - 2025

Five-Year Supply of Housing Land 2020 - 2025 April 2020 North Norfolk District Council Planning Policy Team 01263 516318 [email protected] Planning Policy Team, North Norfolk District Council, Holt Road, Cromer, NR27 9EN www.north-norfolk.gov.uk/localplan All documents can be made available in Braille, audio, large print or in other languages. Please contact 01263 516318 to discuss your requirements. Five Year Supply of Housing Land 2020-2025 Contents 1. Introduction .................................................................................................................................... 4 2. Context ........................................................................................................................................... 4 3. Headlines for 2019 ......................................................................................................................... 5 4. Methodology .................................................................................................................................. 6 Stage 1: Identifying the Five Year Period .......................................................................................... 6 Stage 2: The Requirement - Identifying the scale of housing provision to be delivered ................. 6 Stage 3: Deliverable Supply ............................................................................................................... 9 Stage 4: Calculating the years of supply ......................................................................................... -

North Norfolk Landscape Character Assessment Contents

LCA cover 09:Layout 1 14/7/09 15:31 Page 1 LANDSCAPE CHARACTER ASSESSMENT NORTH NORFOLK Local Development Framework Landscape Character Assessment Supplementary Planning Document www.northnorfolk.org June 2009 North Norfolk District Council Planning Policy Team Telephone: 01263 516318 E-Mail: [email protected] Write to: Planning Policy Manager, North Norfolk District Council, Holt Road, Cromer, NR27 9EN www.northnorfolk.org/ldf All of the LDF Documents can be made available in Braille, audio, large print or in other languages. Please contact 01263 516318 to discuss your requirements. Cover Photo: Skelding Hill, Sheringham. Image courtesy of Alan Howard Professional Photography © North Norfolk Landscape Character Assessment Contents 1 Landscape Character Assessment 3 1.1 Introduction 3 1.2 What is Landscape Character Assessment? 5 2 North Norfolk Landscape Character Assessment 9 2.1 Methodology 9 2.2 Outputs from the Characterisation Stage 12 2.3 Outputs from the Making Judgements Stage 14 3 How to use the Landscape Character Assessment 19 3.1 User Guide 19 3.2 Landscape Character Assessment Map 21 Landscape Character Types 4 Rolling Open Farmland 23 4.1 Egmere, Barsham, Tatterford Area (ROF1) 33 4.2 Wells-next-the-Sea Area (ROF2) 34 4.3 Fakenham Area (ROF3) 35 4.4 Raynham Area (ROF4) 36 4.5 Sculthorpe Airfield Area (ROF5) 36 5 Tributary Farmland 39 5.1 Morston and Hindringham (TF1) 49 5.2 Snoring, Stibbard and Hindolveston (TF2) 50 5.3 Hempstead, Bodham, Aylmerton and Wickmere Area (TF3) 51 5.4 Roughton, Southrepps, Trunch -

Police Report

FAKENHAM SAFER NEIGHBOURHOOD TEAM BRININGHAM, FULMODESTON, GUNTHORPE, HINDOLVESTON, KETTLESTONE, LITTLE SNORING, MELTON CONSTABLE, RYBURGH, STIBBARD, SWANTON NOVERS, THURNING, THURSFORD AND WOOD NORTON. www.norfolk.police.uk MAY 2021 WE ARE YOUR SAFER NEIGHBOURHOOD TEAM – WANT TO GET IN TOUCH? YOUR LOCAL BEAT MANAGER CONTACT US – E: [email protected] TEL: 101 Ext: 2166 FOLLOW US ON SOCIAL MEDIA FACEBOOK: North Norfolk Police TWITTER: @NorthNorfPolice PC 1673 RICHARD DAWSON UPDATE FROM YOUR ENGAGEMENT OFFICER WHAT’S HAPPENING IN YOUR AREA? Daisy Woodward-Smith Over the past 3 months Fakenham Safer Neighbourhood TEL: 07917 642073 Team has been focussing on anti-social behaviour specifically around Millennium Park, Church Lanes and E : [email protected] Gardens and Aldiss Park. PC Dawson has also been responding to complaints about speeding in the town. I’ve been working with local community groups to try As a result of working in partnership with Fakenham Town and gain an understanding and feedback around Council, the tree line in Millennium Park has been raised safety concerns of females in the Great Yarmouth and and ongoing work is nearing completion for a CCTV North Norfolk areas. camera to be installed for public reassurance during the evenings. I’m still hoping to talk to further groups in the North Going forward the team will be continuing to look at the Norfolk community so please do make contact with me potential issues of anti-social behaviour in the same via email > [email protected] locations and working towards resolving a vehicle anti- if you know of any women’s group or organisations that social behaviour issue on Oak Street in Fakenham. -

Norfolk Boreas Limited Document Reference: 5.1.12.3 Pursuant to APFP Regulation: 5(2)(Q)

Norfolk Boreas Offshore Wind Farm Consultation Report Appendix 12.3 Scoping area and PCZ mailing area map Applicant: Norfolk Boreas Limited Document Reference: 5.1.12.3 Pursuant to APFP Regulation: 5(2)(q) Date: June 2019 Revision: Version 1 Author: Copper Consultancy Photo: Ormonde Offshore Wind Farm This page is intentionally blank. Norfolk Boreas Offshore Wind Farm Appendices 585000 590000 595000 600000 605000 610000 615000 620000 625000 630000 635000 640000 Thornage Mundesley Indicative Onshore Elements of Brinton Hunworth Thorpe Market theSouth Project Creake (incl. Landfall, CableHoughton Hanworth St Giles Gunthorpe Stody Relay Station Zones, and Project Plumstead Matlaske Thurgarton Trunch F Great Snoring 335000 East Barsham Briningham Edgefield Alby Hill Knapton 335000 Substation Zone) Thursford West Barsham Little Bacton Ramsgate Barningham Wickmere Primary Consultation Zone Briston Antingham Little Swanton Street Suffield Snoring Novers Swafield Historic Scoping SculthorpeArea Barney Calthorpe Parish Boundaries (OS, 2017) Kettlestone Fulmodeston Itteringham Saxthorpe North Walsham Dunton Tattersett Fakenham Corpusty Crostwight 330000 330000 Hindolveston Thurning Hempton Happisburgh Common Oulton Tatterford Little Stibbard Lessingham Ryburgh Wood Norton Honing East Toftrees Great Ryburgh Heydon Bengate Ruston Guestwick Wood Dalling Tuttington Colkirk Westwick Helhoughton Aylsham Ingham Guist Burgh Skeyton Worstead Stalham next Aylsham East Raynham Oxwick Foulsham Dilham Brampton Stalham Green 325000 325000 Marsham Low Street Hickling -

North Norfolk District

Norfolk County Council Definitive Statement of Public Rights of Way Disrtict of North Norfolk Contains public sector information c Norfolk County Council; Available for re-use under the Open Government Licence v3: http://www.nationalarchives.gov.uk/doc/open-government-licence/version/3/ Statement downloaded 16th January 2021; latest version available online at: https://www.norfolk.gov.uk/out-and-about-in-norfolk/public-rights-of-way/ map-and-statement-of-public-rights-of-way-in-norfolk/definitive-statements Document compiled by Robert Whittaker; http://robert.mathmos.net/ DEFINITIVE STATEMENT OF PUBLIC RIGHTS OF WAY NORTH NORFOLK DISTRICT VOLUME I PARISH OF ALBY WITH THWAITE Footpath No. 1 (Middle Hill to Aldborough Mill). Starts from Middle Hill and runs north westwards to Aldborough Hill at parish boundary where it joins Footpath No. 12 of Aldborough. Footpath No. 2 (Alby Hill to All Saints' Church). Starts from Alby Hill and runs southwards to enter road opposite All Saints' Church. Footpath No. 3 (Dovehouse Lane to Footpath 13). Starts from Alby Hill and runs northwards, then turning eastwards, crosses Footpath No. 5 then again northwards, and continuing north-eastwards to field gate. Path continues from field gate in a south- easterly direction crossing the end Footpath No. 4 and U14440 continuing until it meets Footpath No.13 at TG 20567/34065. Footpath No. 4 (Park Farm to Sunday School). Starts from Park Farm and runs south westwards to Footpath No. 3 and U14440. Footpath No. 5 (Pack Lane). Starts from the C288 at TG 20237/33581 going in a northerly direction parallel and to the eastern boundary of the cemetery for a distance of approximately 11 metres to TG 20236/33589.