Aviation Activity Forecasts BOWERS FIELD AIRPORT AIRPORT MASTER PLAN

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

0821 Piper Flyer.Pdf (207 Downloads)

piperflyer.org August 2021 / Volume 18 / Issue 8 …the heart of your aircraft® Aircraft Spruce is the leading worldwide distributor of general aviation parts and supplies. Our orders ship same day, at the lowest prices, and with the support of the most helpful staff in the industry. We look forward to our next opportunity to serve you! www.aircraftspruce.com ORDER YOUR FREE 2021-2022 CATALOG! 2 • Piper Flyer |August March 20212020 1000 PAGES OF PRODUCTS! Call Toll Free 1-877-4-SPRUCE …the heart of your aircraft® Aircraft Spruce is the leading worldwide distributor of general aviation parts and supplies. Our orders ship same day, at the lowest prices, and with the support of the most helpful staff in the industry. We look forward to our next opportunity to serve you! www.aircraftspruce.com ORDER YOUR FREE 2021-2022 CATALOG! 1000 PAGES OF PRODUCTS! Call Toll Free 1-877-4-SPRUCE August 2021 | Piper Flyer • 3 August 2021 What’s inside / VOLUME 18 / ISSUE 8 CONTENTS The View from Here 8 by Jennifer Dellenbusch Letters 8 Events 10 The High and the Writey 12 by Kevin Garrison Questions & Answers 14 by Steve Ells The Speed of Flight 18 by Tom Machum Comanche Landing Gear, Part 2 20 by Kristin Winter ATC: Unraveling the Mystery, 20 28 Part 3 by Robert Marks So, You Want to Be a Bush 34 Pilot? Here’s What You Need to Know 34 42 by Steve Ells Transponder and Altimeter/ 42 Static System Certification by Steve Ells Destination: 48 Minter Field by Steve Ells Press Releases 54 Aircraft Safety Alerts 58 Advertiser Index 64 Back When: Vintage Piper 66 Advertising and Marketing Cover: 1957 Piper PA-18 Super Cub on the beach at Hinchinbrook Island, Alaska- 2011 Valdez Fly-in, Alaska Daniel H. -

Serialization List Year Produced MODEL 18 D18S A-1 Thru A-37 1945 37

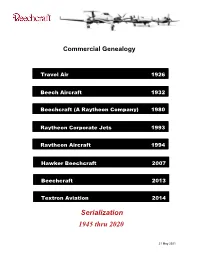

Commercial Genealogy Travel Air 1926 Beech Aircraft 1932 Beechcraft (A Raytheon Company) 1980 Raytheon Corporate Jets 1993 Raytheon Aircraft 1994 Hawker Beechcraft 2007 Beechcraft 2013 Textron Aviation 2014 Serialization 1945 thru 2020 21 May 2021 HAWKER 4000 BRITISH AEROSPACE AIRCRAFT HAWKER 1000 HAWKER 900XP HAWKER SIDDELEY 125-400 BEECHCRAFT HAWKER 125-400 U125A HAWKER 800 • HAWKER SIDDELEY 125 HAWKER 800XP HAWKER 800XPi HAWKER 850 HAWKER 800XPR SERIES 1 HAWKER 125-700 HAWKER 750 HAWKER 125-600 MODEL 400 BEECHJET • HAWKER SIDDELEY 125 400A BEECHJET 400A HAWKER 400XP HAWKER 400XPR SERIES 3 S18A T1A XA-38 GRIZZLY MODEL 2000 STARSHIP PREMIER I PREMIER IA S18 AT-10 KING AIR 350ER F2 KING AIR 350 • • • UC-45 U-21J SUPER KING AIR 300 KING AIR 350i KING AIR 350i D18S C45H SUPER E18 • • KING AIR B200 MODEL 18 SUPER H18 • • TWIN BEECH SUPER KING AIR 200 KING AIR B200GT KING AIR 250 KING AIR 250 C-12 AIR FORCE C-12 NAVY JRB-1 C-12 ARMY 1300 AIRLINER • • • • RC-12K C-12K JRB-2 • JRB-6 C-12 AIR FORCE U21F AT-11 • C-12 NAVY/MARINES KING AIR 100 • • • AT-7 KING AIR A100 B100 C-12 ARMY VC-6A B90 KING AIR B100 Legendary Innovation— • • • C90 SNB-1 MODEL 90 KING AIR T-44A E90 F90 KING AIR C90A Yesterday, Today and Tomorrow. SNB-2 • SNB-5P • • KING AIR C90B KING AIR C90GT KING AIR C90GTx KING AIR C90GTx U-21 RU-21 KING AIR F90-1 With a rich history dating back more than 80 years, Beechcraft Corporation continues to design, build NU-8F MODEL 99 AIRLINER B99 • and support a versatile and globally renowned fl eet of aircraft. -

Business & Commercial Aviation

BUSINESS & COMMERCIAL AVIATION LEONARDO AW609 PERFORMANCE PLATEAUS OCEANIC APRIL 2020 $10.00 AviationWeek.com/BCA Business & Commercial Aviation AIRCRAFT UPDATE Leonardo AW609 Bringing tiltrotor technology to civil aviation FUEL PLANNING ALSO IN THIS ISSUE Part 91 Department Inspections Is It Airworthy? Oceanic Fuel Planning Who Says It’s Ready? APRIL 2020 VOL. 116 NO. 4 Performance Plateaus Digital Edition Copyright Notice The content contained in this digital edition (“Digital Material”), as well as its selection and arrangement, is owned by Informa. and its affiliated companies, licensors, and suppliers, and is protected by their respective copyright, trademark and other proprietary rights. Upon payment of the subscription price, if applicable, you are hereby authorized to view, download, copy, and print Digital Material solely for your own personal, non-commercial use, provided that by doing any of the foregoing, you acknowledge that (i) you do not and will not acquire any ownership rights of any kind in the Digital Material or any portion thereof, (ii) you must preserve all copyright and other proprietary notices included in any downloaded Digital Material, and (iii) you must comply in all respects with the use restrictions set forth below and in the Informa Privacy Policy and the Informa Terms of Use (the “Use Restrictions”), each of which is hereby incorporated by reference. Any use not in accordance with, and any failure to comply fully with, the Use Restrictions is expressly prohibited by law, and may result in severe civil and criminal penalties. Violators will be prosecuted to the maximum possible extent. You may not modify, publish, license, transmit (including by way of email, facsimile or other electronic means), transfer, sell, reproduce (including by copying or posting on any network computer), create derivative works from, display, store, or in any way exploit, broadcast, disseminate or distribute, in any format or media of any kind, any of the Digital Material, in whole or in part, without the express prior written consent of Informa. -

Top Turboprop Series: We Compare Popular Pre-Owned Models

FOR THE PILOTS OF OWNER-FLOWN, CABIN-CLASS AIRCRAFT SEPTEMBER 2019 $3.95 US VOLUME 23 NUMBER 9 Top Turboprop Series: We Compare Popular Pre-Owned Models Five Questions The Latest on One Pilot’s with Corporate the Cessna Denali Introduction Angel Network & SkyCourier to Aerobatics Jet It US One year $15.00, two years $29.00 Canadian One year $24.00, two years $46.00 Overseas One Year $52.00, Two Years $99.00 Single copies $6.50 PRIVATE. FAST. SMART. EDITOR Rebecca Groom Jacobs SEPTEMBER2019 • VOL. 23, NO. 9 (316) 641-9463 Contents [email protected] EDITORIAL OFFICE 2779 Aero Park Drive 4 Traverse City, MI 49686 Editor’s Briefing Phone: (316) 641-9463 E-mail: [email protected] 2 A Career Shaped by Turboprops PUBLISHER by Rebecca Groom Jacobs Dave Moore PRESIDENT Position Report Dave Moore 4 What Makes a Turboprop CFO Safer? Answer: You Rebecca Mead PRODUCTION MANAGER by Dianne White Mike Revard PUBLICATIONS DIRECTOR Jake Smith GRAPHIC DESIGNER Marci Moon 6 TWIN & TURBINE WEBSITE 6 Top Turboprop Series: www.twinandturbine.com Pre-Owned Piper Meridian ADVERTISING DIRECTOR and Daher TBM 700C2 John Shoemaker Twin & Turbine by Joe Casey 2779 Aero Park Drive Traverse City, MI 49686 12 Five on the Fly with Phone: 1-800-773-7798 Corporate Angel Network Fax: (231) 946-9588 [email protected] by Rebecca Groom Jacobs ADVERTISING ADMINISTRATIVE COORDINATOR & REPRINT SALES 14 The Latest on the Betsy Beaudoin Cessna Denali and Phone: 1-800-773-7798 [email protected] SkyCourier ADVERTISING ADMINISTRATIVE by Rich Pickett ASSISTANT Jet It Erika Shenk 22 Intro to Aerobatics Phone: 1-800-773-7798 by Jared Jacobs [email protected] SUBSCRIBER SERVICES Rhonda Kelly Diane Smith Jamie Wilson Molly Costilow 22 Kelly Adamson P.O. -

Arctic Discovery Seasoned Pilot Shares Tips on Flying the Canadian North

A MAGAZINE FOR THE OWNER/PILOT OF KING AIR AIRCRAFT SEPTEMBER 2019 • VOLUME 13, NUMBER 9 • $6.50 Arctic Discovery Seasoned pilot shares tips on flying the Canadian North A MAGAZINE FOR THE OWNER/PILOT OF KING AIR AIRCRAFT King September 2019 VolumeAir 13 / Number 9 2 12 30 36 EDITOR Kim Blonigen EDITORIAL OFFICE 2779 Aero Park Dr., Contents Traverse City MI 49686 Phone: (316) 652-9495 2 30 E-mail: [email protected] PUBLISHERS Pilot Notes – Wichita’s Greatest Dave Moore Flying in the Gamble – Part Two Village Publications Canadian Arctic by Edward H. Phillips GRAPHIC DESIGN Rachel Wood by Robert S. Grant PRODUCTION MANAGER Mike Revard 36 PUBLICATIONS DIRECTOR Jason Smith 12 Value Added ADVERTISING DIRECTOR Bucket Lists, Part 1 – John Shoemaker King Air Magazine Be a Box Checker! 2779 Aero Park Drive by Matthew McDaniel Traverse City, MI 49686 37 Phone: 1-800-773-7798 Fax: (231) 946-9588 Technically ... E-mail: [email protected] ADVERTISING ADMINISTRATIVE COORDINATOR AND REPRINT SALES 22 Betsy Beaudoin Aviation Issues – 40 Phone: 1-800-773-7798 E-mail: [email protected] New FAA Admin, Advertiser Index ADVERTISING ADMINISTRATIVE ASSISTANT PLANE Act Support and Erika Shenk International Flight Plan Phone: 1-800-773-7798 E-mail: [email protected] Format Adopted SUBSCRIBER SERVICES by Kim Blonigen Rhonda Kelly, Mgr. Kelly Adamson Jessica Meek Jamie Wilson P.O. Box 1810 24 Traverse City, MI 49685 1-800-447-7367 Ask The Expert – ONLINE ADDRESS Flap Stories www.kingairmagazine.com by Tom Clements SUBSCRIPTIONS King Air is distributed at no charge to all registered owners of King Air aircraft. -

The Years of Change

The Years of Change In early January of 1993 all the B-2 structural tests were successfully completed. The static load tests were taken to failure to 161% of maximum stress, and the durability test completed more than 2 lifetimes, which represented 20,000 design flight hours. January 1993 confidence was high for the $4-billion PAMPA Program as the company prepared to complete its first flight evaluation aircraft. However, the realities of the “post-cold war” era forced management to gear up for a tough year as the battle of the defense budget continued in Washington. The ailing commercial aviation industry presented additional challenges for the company. Boeing cut production on all their programs, and 1993 looked very gloomy. The company announced plans for down-sizing up to 1,500 people by the end of the year. Vought president Gordon Williams streamlined the management team to help the company ride out the business downturn, and still continue to meet its customer requirements. He stated that “business will be smaller but stronger.” In March 1993 Vought shipped its last engine nacelle for the Canadair business jet while continuing production on the regional jet nacelles. The 500th horizontal stabilizer for the Boeing 767 was shipped during March, and 141 employees elected to retire. In the meantime, Loral Corporation formed a new missiles group by combining Loral Vought Systems and Loral Aeronutronic during the month. At the end of April, 104 employees elected to retire. McDonnell Douglas certified Vought’s business processes in early May, which was another milestone on the way to becoming a preferred supplier for McDonnell Douglas. -

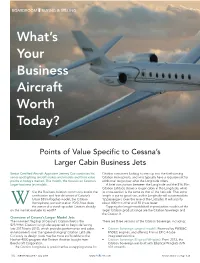

What's Your Business Aircraft Worth Today?

BR Buying & Selling 2 JuLY17.qxp_Layout 1 19/06/2017 14:54 Page 1 BOARDROOM T BUYING & SELLING What’s Your Business Aircraft Worth Today? Points of Value Specific to Cessna’s Larger Cabin Business Jets Senior Certified Aircraft Appraiser Jeremy Cox continues his Citation customers looking to step up into the forthcoming series spotlighting aircraft makes and models and their value Citation Hemisphere, and who typically have a requirement for points in today’s market. This month, the focus is on Cessna’s additional range over what the Longitude offers. larger business jet models… A brief comparison between the Longitude and the $16.35m Citation Latitude shows a longer cabin in the Longitude, while hile the Business Aviation community awaits the its cross-section is the same as that of the Latitude. That extra certification and first deliveries of Cessna’s length is put to good use, as the Longitude will accommodate W future $35m flagship model, the Citation 12 passengers (over the nine of the Latitude). It will also fly Hemisphere, sometime after 2020, how does about 800nm further and 30 knots faster. the owner of a stand-up cabin Citation already Topping the longer-established in-production models of the on the market evaluate its worth? larger Citation product range are the Citation Sovereign and the Citation X. Overview of Cessna’s Larger Model Jets The imminent flagship of Cessna’s Citation fleet is the There are three versions of the Citation Sovereign, including: $23.995m Citation Longitude (expected to begin delivering late 2017/early 2018), which provides performance and cabin • Citation Sovereign (original model): Powered by PW306C enhancements over the ‘game-changing’ Citation Latitude. -

The Great Vrcs Kit List for 1981

THE GREAT VRCS KIT LIST FOR 1981 - 1983 - PAGE 1 OF 3 compiled by Bruce Tharpe * Kits marked with as asterisk were introduced in 1983 and are “newly eligible” for VRCS events in 2019. ACE R/C BALSA USA BRIDI / GREAT CASS ENGINEERING Pacer Phaeton Biplane PLANES (contInued) Pulsar Bipe Super Pacer Tempo II AT-6 Texan Super Skybolt Mach None Moonraker Chipmunk GLH II Taube Kraft Super Fli CHAMP MODEL PROD Upstart II Fly Baby F-7F Tigercat SST 40 Whizard Fly Baby Biplane T-28 Dick's Dream Sopwith Pup Cosmic Wind CHAMPION MODEL Shrike Swizzle Stick 30, 40, 60 Corben Ace AEROPLANE CO. Guppy Pee Wee Stick Rearwin Speedster The Hammer* Nomad II Excalibur Dalotel DM-165 Stampe SV-4* Alpha, Alpha 15 Smoothie Cap 20L Sportster 20* All Star Bipe 1/4-Scale Piper Cub Littlest Stick Eindecker BUD NOSEN CONCEPT MODELS Air Scout Force 1 (plan in RCM) Aeronca Champ Fleet* Ace High Mk II* Der Jager D IX* Cessna 310 Super-Fli* Bristol M1* Champion Citabria Airscout* AIRTRONICS Super Stick* Mr. Mulligan Barnstormer* Q-Tee, S-Tee Gere Sport Travel Air* Gere Sport BILL EVANS Piper J-3 Cub New Era 20, 40 Simitar 540 P-51 Mustang COVERITE New Era III Simitar Sport F-4U Corsair Gee Bee Sportster Acro-Star Bipe Hot Rock P-47 Gee Bee Model E* Cadet Crosswind Trainer Art Chester Jeep* Cessna Centurian Big Stick Sportavia Gas, Elec BOB DIVELY Rookie CRAFT AIR Piper Arrow Christen Eagle 1 Citabria 65”* Bull-Pup Warlock 05, 40 Skybolt Viking I-II Monarch 05 T.B. -

June 2021 Issue 45 Ai Rpi Lo T

JUNE 2021 ISSUE 45 AI RPI LO T INSIDE HRHTHE DUKE OF EDINBURGH 1921-2021 A Portrait of our Patron RED ARROWS IN 2021 & BEYOND Exclusive Interview with Red One OXFORD v CAMBRIDGE AIR RACE DIARY With the gradual relaxing of lockdown restrictions the Company is hopeful that the followingevents will be able to take place ‘in person’ as opposed to ‘virtually’. These are obviously subject to any subsequent change THE HONOURABLE COMPANY in regulations and members are advised to check OF AIR PILOTS before making travel plans. incorporating Air Navigators JUNE 2021 FORMER PATRON: 26 th Air Pilot Flying Club Fly-in Duxford His Royal Highness 30 th T&A Committee Air Pilot House (APH) The Prince Philip Duke of Edinburgh KG KT JULY 2021 7th ACEC APH GRAND MASTER: 11 th Air Pilot Flying Club Fly-in Henstridge His Royal Highness th The Prince Andrew 13 APBF APH th Duke of York KG GCVO 13 Summer Supper Girdlers’ Hall 15 th GP&F APH th MASTER: 15 Court Cutlers’ Hall Sqn Ldr Nick Goodwyn MA Dip Psych CFS RAF (ret) 21 st APT/AST APH 22 nd Livery Dinner Carpenters’ Hall CLERK: 25 th Air Pilot Flying Club Fly-in Weybourne Paul J Tacon BA FCIS AUGUST 2021 Incorporated by Royal Charter. 3rd Air Pilot Flying Club Fly-in Lee on the Solent A Livery Company of the City of London. 10 th Air Pilot Flying Club Fly-in Popham PUBLISHED BY: 15 th Air Pilot Flying Club The Honourable Company of Air Pilots, Summer BBQ White Waltham Air Pilots House, 52A Borough High Street, London SE1 1XN SEPTEMBER 2021 EMAIL : [email protected] 15 th APPL APH www.airpilots.org 15 th Air Pilot Flying Club Fly-in Oaksey Park th EDITOR: 16 GP&F APH Allan Winn EMAIL: [email protected] 16 th Court Cutlers’ Hall 21 st Luncheon Club RAF Club DEPUTY EDITOR: 21 st Tymms Lecture RAF Club Stephen Bridgewater EMAIL: [email protected] 30 th Air Pilot Flying Club Fly-in Compton Abbas SUB EDITOR: Charlotte Bailey Applications forVisits and Events EDITORIAL CONTRIBUTIONS: The copy deadline for the August 2021 edition of Air Pilot Please kindly note that we are ceasing publication of is 1 st July 2021. -

FROM the GROUNDUP September 2004 CAPABILITIES BROCHURE

Vought Aircraft Industries, Inc. www.voughtaircraft.com INTEGRATED AEROSTRUCTURES FROM THE GROUNDUP September 2004 CAPABILITIES BROCHURE Airbus A330/A340 In 1988, we became the Boeing 747 We’ve built panels for the main first major U.S. structural assemblies supplier to fuselage, doors and the empennage section for more Airbus with the award of wing components for than 1,350 Boeing 747 aircraft since the program the A330/A340 long-range aircraft. Deliveries began in 1968. began in 1990, exceeding the 500 shipset mark in 2002. 2 PROVEN Lockheed Martin C-130J Hercules Northrop Grumman B-2 Spirit Our company has delivered more than 2,200 We were one of three team members on the empennage sections to Lockheed Martin B-2 program, with responsibility for more since becoming a supplier on the C-130 structure than any other team member. program in the 1950s. Through our heritage companies, we have been a premier supplier to the aerospace industry for nearly nine decades. Vought is a proven leader in providing aerostructures of superior quality to our customers. We’ve helped shape many major aircraft programs over the years – from small business jets to jumbo airplanes, and tactical fighters to cargo aircraft. From the ground up, Vought creates quality structures that help our customers take flight. 3 Boeing C-17 Globemaster III Robotic Tack Cell Machine We have consistently driven down the price of the Our new robotic tack cell transforms a six-step C-17 components we build through continuous process into a single operation. The six-axis producibility improvements. -

CHAMPION AEROSPACE LLC AVIATION CATALOG AV-14 Spark

® CHAMPION AEROSPACE LLC AVIATION CATALOG AV-14 REVISED AUGUST 2014 Spark Plugs Oil Filters Slick by Champion Exciters Leads Igniters ® Table of Contents SECTION PAGE Spark Plugs ........................................................................................................................................... 1 Product Features ....................................................................................................................................... 1 Spark Plug Type Designation System ............................................................................................................. 2 Spark Plug Types and Specifications ............................................................................................................. 3 Spark Plug by Popular Aircraft and Engines ................................................................................................ 4-12 Spark Plug Application by Engine Manufacturer .........................................................................................13-16 Other U. S. Aircraft and Piston Engines ....................................................................................................17-18 U. S. Helicopter and Piston Engines ........................................................................................................18-19 International Aircraft Using U. S. Piston Engines ........................................................................................ 19-22 Slick by Champion ............................................................................................................................. -

Cessna Citation X

The Conklin & de Decker Report Cessna Citation X Created on August 21, 2019 by Doug Strangfeld © 2019 Conklin & de Decker Associates, Inc PO BOX 121184 1006 North Bowen, Suite B Arlington, TX 76012 www.conklindd.com Data version: V 19.1 Cessna Citation X RANGE 2,890 nm SPEED 525 kts PASSENGERS 8 people Cost ACQUISITION COST ANNUAL COST VARIABLE COST FIXED COST $9,200,000 $2,424,365 $3,834/hr $890,791 MAX PAYLOAD 2,375 lb ENGINES 2 Rolls Royce AE 3007C1 TOTAL CABIN AREA 538 cu ft AVIONICS Honeywell Primus Elite WINGSPAN 63.9 ft APU Standard Assumptions This report uses custom assumptions that differ from Conklin & de Decker default values for Annual Utilization (Hours), Fuel Price (Jet A). ANNUAL UTILIZATION (DISTANCE) 188,400 nm FUEL PRICE (JET A) $4.45/gal ANNUAL UTILIZATION (HOURS) 400 hrs LABOR COST $136/hr AVERAGE SPEED (STANDARD TRIP) 471 kts ACQUISITION COST $9,200,000 Cessna Aircraft Company Canadian Air Force ordered an additional 180 T-50s. The Cessna-Roos Aircraft Company was incorporated on September 7, 1927, by During WWII, Cessna expanded from a company that employed 200 people in 1940 to Clyde V. Cessna and Victor Roos. One month later, Roos resigned and sold his 6,074 by 1944. At the end of the war, Cessna was able to continue producing aircraft interest back to Cessna. Later that year, the company was renamed the Cessna to sustain a short-lived demand for small aircraft that could be used for short flights. Aircraft Company. Cessna continued work on the "A" series of aircraft he had begun Cessna entered the business aircraft market in 1954 with production of the T-37, its during his partnership with Walter Beech, Lloyd Stearman and the Travel Air Aircraft first jet-powered aircraft.