Powerpoint Migration

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

NUCOR Steel-Hertford's Petition to Intervene

Velson Mullins NelsonMullin sRile y& Scarborough LLP Attorneys and Counselors at Law Joseph W. Bason 4140 Parklake Avenue / GlenLake One / Second Floor / Raleigh. North Carolina 27612 Tel: 919.877.3807 Tel: 919.877.3800 Fax: 919.877.3799 Fax: 919.877.3140 www.nelsonmullins.co m [email protected] April 28,201 0 VIA HAND DELIVERY Ms. Renne Vance APR282Dtt North Carolina Utilities Commission ' ClericsOftc * 430 N. Salisbury Street 5th Floor- Clerks Office Raleigh,N C 27699-4325 Re: Inth e Matter of Application of Virginia Electric and Power Company, d/b/a Dominion North Carolina Power, for Authority to Transfer Functional Control of Transmission Assets to PJM Interconnection, LLC (NCUC, Docket No. E-22, Sub 418) Our FileNo . 19128/01513 Dear Ms. Vance: r^ Enclosed for filing on behalf of Nucor Steel-Hertford ("Nucor") are an original and thirty (30) vUt/lCJ copies ofNucor' s Petition to Intervene relating to the above-referenced matter. 96 n/Tllflffi ^•^so enc^ose^ IS an additional copy of thedocumen t to bestampe d as "filed" and returned to me ' . ," viam y courier. ( V11lO J Thank you for your assistance in this,matter . With best regards, Ia m \)j0^-^ ' Very truly yours, h W. Eason 36rtC5> JWE:nwilmot <c>O^JPp^nc*0Sures 7^ \rv\ cc: A^ parties of record (w/enc.) /ADA -PlAUptlanta • ^s*011 *Charlesto n • Charlotte • Columbia • Greenville • Myrtle Beach • Raleigh • Washington, DC • Winston-Salem •aaiito STATE OF NORTH CAROLINA UTILITIES COMMISSION RALEIGH APR282M DOCKET NO. E-22,Su b 418 CteriteOffic e BEFORE THE NORTH CAROLINA UTILITIES COMMISSION ^UfiBiesCommission In the Matter of ) Application of Virginia Electric and ) NUCOR STEEL-HERTFORD'S Power Company, d/b/a Dominion North ) PETITION TO INTERVENE Carolina Power, for Authority to Transfer ) Functional Control ofTransmissio n ) Assets to PJM Interconnection, LLC ) Pursuant to Rules Rl-17 of the Rules of Practice and Procedure of the North Carolina Utilities Commission, Nucor Steel-Hertford, a division of Nucor Corporation ("Nucor"), hereby moves to intervene in the above-captioned proceeding. -

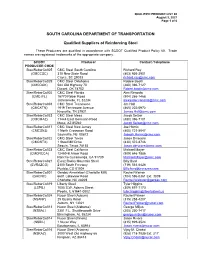

60 August 3, 2021 Page 1 of 6

QUALIFIED PRODUCT LIST 60 August 3, 2021 Page 1 of 6 SOUTH CAROLINA DEPARTMENT OF TRANSPORTATION Qualified Suppliers of Reinforcing Steel These Producers are qualified in accordance with SCDOT Qualified Product Policy 60. Trade names are registered trademarks of the appropriate company. SCDOT Producer Contact /Telephone PRODUCER CODE SteelRebarCo005 CMC Steel South Carolina Richard Ray (CMCCSC) 310 New State Road (803) 936-3901 Cayce, SC 29033 [email protected] SteelRebarCo029 CMC Steel Oklahoma Robbie Booth (CMCDOK) 584 Old Highway 70 (480) 396-7127 Durant, OK 74702 [email protected] SteelRebarCo002 CMC Steel Florida Alex Renosto (CMCJFL) 16770 Rebar Road (904) 266-1468 Jacksonville, FL 32234 [email protected] SteelRebarCo003 CMC Steel Tennessee Jim Hall (CMCKTN) 1919 Tennessee Avenue (865) 202-5972 Knoxville, TN 37921 [email protected] SteelRebarCo033 CMC Steel Mesa Jacob Selzer (CMCMAZ) 11444 East Germann Road (480) 396-7101 Mesa, AZ 85242 [email protected] SteelRebarCo017 CMC Steel New Jersey Joe Homic (CMCSNJ) 1 North Crossman Road (800) 721-8047 Sayreville, NJ 08872 [email protected] SteelRebarCo022 CMC Steel Texas Jason Dinscore (CMCSTX) 1 Steel Mill Drive (830) 372-8746 Seguin, Texas 78155 [email protected] SteelRebarCo023 CMC Steel California Michael Mayer (CMCRCCA) 12459-B Arrow Road (909) 646-7886 Rancho Cucamonga, CA 91739 [email protected] SteelRebarCo021 Evraz Rocky Mountain Steel Billy Byrd (EVRAZCO) 2100 South Freeway (719) 561-6426 Pueblo, CO 81004 [email protected] SteelRebarCo001 Gerdau Ameristeel (Charlotte Mill) Rachel Warren (GACNC) 6601 Lakeview Road (704) 596-0361 Ext. 3039 Charlotte, NC 28269 [email protected] SteelRebarCo019 Liberty Steel Tyler Higgins (LSPIL) 7000 S.W. -

Brief on Exceptions of Nucor Steel Auburn, Inc

STATE OF NEW YORK PUBLIC SERVICE COMMISSION CASE 03-E-0188 - Proceeding on Motion of the Commission Regarding a Retail Renewable Portfolio Standard. BRIEF ON EXCEPTIONS OF NUCOR STEEL AUBURN, INC. Overview The Recommended Decision (“RD”) issued on June 3, 2004, culminates a fifteen month effort to assess the practical ramifications of a Commission policy to spur development of renewable resources to serve New York’s growing electric load. As described in the Introduction and Background section to the RD, mounting state concerns regarding the environmental costs of fossil-fired generation (particularly air emissions) and growing dependence on natural-gas fired generators are the prime motivators for more aggressive pursuit of “clean” energy resources. This interest in renewable, low-emitting or non-emitting resources is inextricably linked to New York’s policies to promote economic development. As Chairman Flynn remarked in his address to the Center for Business Intelligence forum on New York Power Supply in New York City on June 11, 2004: From Clean-Fueled vehicle programs designed to encourage development of cleaner transportation technologies and alternative fuels, to Executive Order lll’s call for more efficient and cleaner use among state-owned facilities, to tax credits that encourage construction of “green” buildings, Governor Pataki has developed a comprehensive energy agenda that balances the need for more energy resources with the need to protect our environment and encourage economic development. The Governor has consistently emphasized the importance of energy’s role in linking environmental protection with economic development.1 Nucor Steel Auburn, Inc. (“Nucor”) has been an active participant in this docket. -

Nucor VR16 II™ Nucor VR16 II™ Vertical Rib Standing Seam Roof System

VERTICAL RIB STANDING SEAM ROOF SYSTEM Nucor VR16 II™ Nucor VR16 II™ Vertical Rib Standing Seam Roof System The Nucor Building Systems VR16 II-90 and VR16 II-360 Roof Systems are structural standing seam vertical rib roof panels that are perfect for architectural requirements in today’s marketplace. The seaming methods used in the VR16 II-90 and VR16 II-360 roof panels offer an attractive architectural system available both in Galvalume® and PVDF finishes as standard. Panels are installed with concealed fastener clips allowing for thermal movement, and mechanically seamed. VR16 II-90 Roof System Nucor VR16 II-90 Roof System panel uses a weathertight 90-degree seam for a battened architectural aesthetic ideal for buildings with various roof conditions including hips and valleys, and easily accommodates complex roof geometries. VR16 II-360 Roof System The VR16 II-360 Roof System features a full 360-degree rolled seam. With uninterrupted linear roof lines, VR16 II-360 offers an even greater level of architectural design to provide a sleek, modern appearance. Designed to withstand the most extreme weather conditions, it offers exceptional performance and weathertightness. Nucor VR16 II Warranties • 25 Year Galvalume Finish • 35 Year PVDF Paint Finish • 20 Year Weathertightness For specific details, please refer to the Warranty Guide online at www.nucorbuildingsystems.com Galvalume® is a registered trademark of BIEC International, Inc. Product Specifications & Details Product Specifications • Rib height: 2″ • Cover width: 16″ • Factory sealant applied along female rib • Minor striations to help reduce “oil canning” • Galvalume or painted PVDF finishes • Standard 24 ga. material (22 ga. -

News Release

News Release Nucor Breaks Ground on Kentucky Plate Mill BRANDENBURG, KENTUCKY, October 23, 2020 – Nucor Corporation, Kentucky state officials, and local government leaders held a groundbreaking today for the company’s new steel plate mill in Brandenburg, Kentucky. The new $1.70 billion plate mill will create more than 400 full-time jobs and be fully operational in 2022. “We are very excited to begin construction on our new plate mill in Kentucky. This state-of-the-art mill will make us a market leader in steel plate products,” said Leon Topalian, President & CEO of Nucor Corporation. “We have been doing business in Kentucky for over a decade and have benefited from the strong business climate and great local workforce.” When the mill is completed, Nucor will have the ability to produce 97 percent of the steel plate products consumed in the U.S. market. The location on the Ohio River will give Nucor transportation advantages in serving the Midwest plate market, which is the largest plate-consuming market in the U.S. “The new plate mill helps us advance our goal of expanding our product portfolio, particularly growing our production of value-added plate products. When it is completed and operational, we’ll be one of only two companies that can produce essentially all of the plate sizes consumed in the U.S. today,” said Al Behr, Executive Vice President of Plate & Structural Products. Nucor operates more than 15 facilites in the state and employs over 2,000 teammates. In addition to the new plate mill, Nucor has invested more than $800 million in its steel sheet mill in Ghent to add a new galvanizing line and expand the production capacity of the mill – a project that is expected to be completed by the middle of next year. -

The FOCUS® of Nucor Building Systems

The FOCUS® of Nucor Building Systems Nucor Building Systems entered the metal building industry in 1987, with our first full service plant in Indiana. Our goal was to deliver performance and value. Our FOCUS statement commits that we will concentrate on the things that matter most to our customers. Far more than a marketing acronym, the FOCUS statement is comprised the fundamental principles that drive our business behaviors every day. Every NBS employee understands the value of executing on these commitments. Fit Steel that fits. When you buy a car you expect it to start, and when you buy a building you expect it to fit…simple as that! Our greatest source of pride comes from jobs that ship with no back charges, back orders, or shortages. On Time Deliveries You get commitments that mean something with Nucor Building Systems. Whether it’s a small, single truck shipment or a large multi-phase job, we make sure that you have erectable steel based on your construction schedule. We will coordinate primary and secondary framing, sheeting, crane steel, bar joists, and trim to make sure you can actually build what we send. Competitive Pricing Nucor Building Systems has consistently led the industry in man-hours-per-ton in both production and design, making us one of the most efficient manufacturers and low cost suppliers in the industry. Our advanced computer pricing system is available to every Nucor Builder, offering the convenience of pricing many buildings in his/her own office with flexibility, speed, and significant design breadth. Unbeatable Service Since Nucor Building Systems utilizes support material produced by our own Nucor Steel divisions, we can assure a predictable supply of raw materials. -

By Nucor Steel— 1

BEFORE THE BEFORE THE CO PUBLIC SERVICE COMMISSION OFSOUTHOF SOUTH CAROLINA ,L-} DOCKET NO. 2006-1-E DOCKET NO. 2006-1-E ,,i ,'} .... ' , 4, r. L IN THE MATTER OF:OF ) ) t%,._,.,) ' Carolina Power &8 Light Company d/b/a ) PETITION TO INTERVENE _i ,..,,j Progress Energy Carolinas, Inc. ) BY NUCOR STEEL-STEEL— Annual Review of Base Rates for ) SOUTH CAROLINA Fuel Costs ) Nucor Steel-South Carolina ("Nucor"),("Nucor"), a Division of Nucor Corporation, pursuant to Rule 103-836 of the rulesrules and regulations of thethe South Carolina Public Service Commission ("Commission"),("Commission" ), hereby respectfully petitions to intervene in the above-captioned docket. Nucor states the following grounds in support of this petition: 1. Nucor owns and operates a steel production facilityfacility near Darlington, South Carolina. As a retail customer of Progress Energy Carolinas, Inc.Inc. ("Progress("Progress Energy")Energy" ) (formerly(formerly known as Carolina Power & Light Company ("CP&L")',),("CP8L")), Nucor purchases hundreds of millions of kWh of electricity annually at a cost of millions of dollars a year. Since thethe cost of electricity comprises one of the major costs of Nucor's manufacturing process, electric costs directly affect Nucor's ability to continue to produce steel at a competitive price. 2. This docket has been established to review Progress Energy's historical and projected fuel costs and to determine thethe appropriate fuel factor for the next twelvetwelve months. Nucor isis concerned about the impactimpact of Progress Energy's fuel costs on its rates and those of other customers. Nucor has a stake in, and will be directly and substantially affected by, thethe outcome of this proceeding. -

The Partnership of Nucor and Danieli Teams Will Bring the Gallatin Casting and Rolling Plant to the Next Level of High-Quality Production and Competitiveness

The partnership of Nucor and Danieli teams will bring the Gallatin casting and rolling plant to the next level of high-quality production and competitiveness. This is the first time that a classical compact thin slab casting and rolling plant is fully reconfigured into an ultra-modern QSP® (Quality Strip Production) plant. Both Nucor and Danieli teams are committed to set a new benchmark in Casting and Rolling Technology. Formerly known as the Gallatin Steel Company, the thin slab rolling plant located in Ghent, KY has a name plate capacity of 1.6 million shTPY of hot rolled coils having a thickness range from 1.4 to 12.7 mm, widths up to 1,625 mm and maximum coil weight of 35 shTon. The existing plant operates a 185 t twin shell DC EAF, a single LMF, a vertical caster, 206 m tunnel furnace, a six-stand close-coupled rolling mill, traditional laminar cooling and one down coiler. The current capabilities of the steel plant are mostly structural steel, micro-alloyed grades and thin line pipe grades. Like similar compact plants, Gallatin was originally designed for doubling the annual capacity by means of a second meltshop, second vertical caster and tunnel furnace connected by a swivel ferry system to the in-line HSM. The new equipment was originally meant to be a copy of the existing one. In October 2014, Nucor became the owner of the Gallatin Steel Company and has recently approved an investment to advance the technological capabilities and competitiveness of the Nucor Steel Gallatin Sheet Mill. Danieli is the selected technology supplier for the complete equipment and automation system, from raw materials to hot rolled coil. -

Nucor DRI Facility St

CASE STUDY Nucor DRI Facility St. James Parish, Louisiana PROJECT PARTNERS Owner Nucor Corporation – Charlotte, NC General Contractor Massmann Construction Co. – Kansas City, KS PRODUCTS Pipe Pile: 18” to 96” OD x 80’ to 115’ PROJECT TIME FRAME May 2011 to April 2012 HISTORY to be transported to the steel mills easily and needed for many stages of this construction Nucor Corporation, the largest steel company efficiently. Once a suitable site was identified, a project. in the United States, was looking for a way dock needed to be built that could handle the to increase its competitive advantage in the building materials for the plant, as well as the Nucor Skyline was able to use the steel coil industry. One way was to invest in a direct iron outflow of materials once production began. produced in Nucor’s Decatur, AL facility and ore reduction facility. This process involves transport it by barge to the Skyline facility in converting natural gas and iron ore pellets SOLUTION Iuka, MS. At this plant, the coil was rolled into into high-quality DRI (direct-reduced iron), The construction of a barge loading/unloading the proper-sized pipe, ranging from 18” to which is the raw material used by Nucor’s steel dock facility on the Mississippi River was 96” for the project. The pipe was needed in mills. Not only does this process employ the needed. The facility offloads ocean going ships lengths varying from 160 to 230 feet, and was latest technologies to reduce emissions, but loaded with iron ore. The iron ore is transferred produced in half-lengths, and barged from the it also provides a low-cost environment and to a processing plant on land by a conveyor Iuka plant to a vendor in New Orleans where operational flexibility. -

Petition to Object to the Nucor Steel Facility, St. James Parish, Louisiana

BEFORE THE ADMINISTRATOR U.S. ENVIRONMENTAL PROTECTION AGENCY In the Matter of Louisiana Department of Environmental Quality's Proposed Operating Permit and Prevention of Significant Deterioration Permit for Consolidated Environmental Management, Inc./Nucor Steel, Louisiana, St. James Parish, Louisiana LDEQ Agency Interest No. 157847 Activity Nos. PER2008000 1 and PER20080002 Permit Nos. 2560-00281-VO; PSD-LA-740 Proposed to Nucor Steel, Louisiana By the Louisiana Department of Environmental Quality on October 15 ,2008 PETITION REQUESTING THAT THE ADMINISTRATOR OBJECT TO THE TITLE V OPERATING AND PREVENTION OF SIGNIFICANT DETERIORATION PERMITS PROPOSED FOR NUCOR STEEL, LOUISIANA Pursuant to Section 505(b) of the Clean Air Act, 42 U.S.C. § 7661 deb )(2) and 40 C.F.R. §70.8( d) , Zen-Noh Grain Corporation ("Zen-Noh") petitions the Administrator of the U.S. Environmental Protection Agency ("Administrator") to object to Title V Air Operating Permit (No. 2560-00281 -VO) ("Operating Permit"). Zen-Noh also petitions the Administrator to reopen or revise Prevention of Significant Deterioration Permit (No. PSD-LA-740) ("PSD Pennit"). And, Zen-Noh petitions the Administrator to direct Louisiana Department of Environmental Quality ("LDEQ") to provide Zen-Noh and the public with all information necessary to the issuance or denial of the Operating Pennit and PSD Permit, provide a meaningful period for public review, and reopen the public comment period. Both the Operating Permit and PSD Permit were proposed on or about October 15, 2008 by LDEQ for issuance to Consolidated Environmental Management, Inc.INucor Steel Louisiana ("Nucor") for a Pig Iron Manufacturing Plant in St. James Parish, Louisiana. -

2019 Recycled Steel Content of Nucor Products (% by Total Weight) Total

NUCOR CORPORATION 1915 Rexford Road Charlotte, NC 28211 704.366.7000 July 2020 To: All Nucor Customers Re: 2019 Recycled Content of Nucor Steel Mill Products Nucor Corporation is North America’s largest recycler, using approximately 20.0 million net tons of scrap steel in 2019 to create new products. Nucor uses Electric Arc Furnace (EAF) technology at all of its steel recycling facilities. EAFs use post-consumer scrap steel material as the major feedstock, unlike blast furnace operations that use mined iron ore as the major feedstock. Nucor has prepared the following information to help calculate the recycled content for products being used in “Green Building” applications or for projects in the LEED® certification program. These percentages are based on the total weight of the products. The calculations are based on 2019 scrap steel delivered and hot metal tons produced and are defined in accordance with ISO 14021:2015. More specific product information may be available from facility representatives. You can find the division contact information here – Nucor LEED Contacts (PDF). Recycled Content – LEED 2009 MR 4; LEED v4 MR Credit: Sourcing of Raw Materials 2019 Recycled Steel Content of Nucor Products (% by Total Weight) Product Group Average Recycled Content Nucor Bar Products 97.0% Nucor Engineered Bar Products 85.5% Nucor Beam Products 79.7% Nucor Plate Products 60.5% Nucor Sheet Products 55.8% Nucor Castrip® 83.5% Total Nucor Steel Combined 70.9% Vulcraft Structural Products 97.0% www.nucor.com NUCOR CORPORATION 1915 Rexford Road Charlotte, NC 28211 704.366.7000 Vulcraft / Verco Decking 55.8% Nucor Grating / Fisher-Ludlow Grating 97.0% Nucor Building Group 70.9% Harris Rebar 97.0% Nucor Fastener Products 97.0% Nucor Wire Products 97.0% Nucor Cold Finish 85.5% Bar Mill Group – The Nucor Bar Mill Group produces rebar, angles, flats, rounds and other miscellaneous structural and non-structural shapes. -

Steel in Transition New Capacity, Trade, Transportation & Forecasts

AUGUST 26-28, 2019 SMU STEEL SUMMIT 2019 Georgia International Convention Center Atlanta, GA SteelMarketUpdate.com/Events/Steel-Summit STEEL IN TRANSITION NEW CAPACITY, TRADE, TRANSPORTATION & FORECASTS CONFERENCE AGENDA Monday, August 26, 2019 10:00 - 5:30 PM Conference Registration Georgia International Convention Center – South Lobby All-Day Beverage - Sponsored by: BMO Harris Bank 10:30 - 12:00 PM Price Risk Management Workshop Hosted by CME Group 10:30 - 10:45 General Introduction to futures markets 10:45 - 11:15 Hedging examples from consumer and producer perspectives 11:15 - 11:55 Panel discussion - development and status of the steel futures market 11:55 –-Q&A Andre Marshall, CEO and Founder, Crunch Risk Guarav Chhibbar, Partner, Metal Edge Partners Jeremy Flack, CEO, Flack Global Metals Sean Kessler, Manager - Metals Products, CME Group Only this event will be held at the Airport Marriott Gateway Hotel. All other events will be held at the GICC. 1:00 - 1:45 PM SMU/CRU Proprietary Indices & Forecasts John Packard, President & CEO Steel Market Update Chris Houlden, Research Manager – Steel and Head of Prices Development CRU Josh Spoores, Principal Analyst - Steel CRU 1:45 - 2:30 PM Transportation Issues & Solutions James Burg, President James Burg Trucking Company JR Schaaf (Jim), Group VP - Metals & Construction Norfolk Southern 2:30 - 2:50 PM Break - Sponsored by: Acero Prime 2:50 - 4:00 PM Steel Distribution & Processing: Demand Perspectives Edward J. Lehner, President & CEO Ryerson John G. Reid, Director, President & CEO Russel