APPENDIX 1.1 PART-A State Profile (Reference: Paragraphs- Profile of Gujarat and 1.1; Page 1 and 2) A

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Narrating North Gujarat: a Study of Amrut Patel's

NARRATING NORTH GUJARAT: A STUDY OF AMRUT PATEL’S CONTRIBUTION TO FOLK LITERATURE A MINOR RESEARCH PROJECT :: SUBMITTED TO :: UNIVERSITY GRANTS COMMISSION :: SUBMITTED BY :: DR.RAJESHKUMAR A. PATEL ASSOCIATE PROFESSOR SMT.R.R.H.PATEL MAHILA ARTS COLLEGE, VIJAPUR DIST.MEHSANA (GUJARAT) 2015 Preface Literature reflects human emotions, thoughts and expressions. It’s a record of activities and abstract ideas of human beings. The oral tradition of literature is the aspect of literature passing ideas and feelings mouth to mouth. I’ve enjoyed going through the precious and rare pieces of folk literature collected and edited by Amrut Patel. I congratulate and salute Amrut Patel for rendering valuable service to this untouchable, vanishing field of civilization. His efforts to preserve the vanishing forms of oral tradition stand as milestone for future generation and students of folk literature. I am indebted to UGC for sanctioning the project. The principal of my college, Dr.Sureshbhai Patel and collegues have inspired me morally and intellectually. I thank them. I feel gratitude to Nanabhai Nadoda for uploding my ideas and making my work easy. Shaileshbhai Paramar, the librarian has extended his time and help, I thank him. Shri Vishnubhai M.Patel, Shri R.R.Ravat, Shri.D.N.Patel, Shri S.M.Patel, Shri R.J.Brahmbhatt, Shri J.J.Rathod., Shri D.S.Kharadi, B.L.Bhangi and Maheshbhai Limbachiya have suppoted me morally. I thank them all. DR.Rajeshkumar A.Patel CONTENTS 1. Introduction: 1.1 North Gujarat 1.2 Life and Works of Dr.Amrut Patel 1.3 Folk Literature-An Overview 2. -

S. No Name of the Unit Address Amount Sanctioned for Subsidy

SIDBI Actual disbursement of subsidy to Units will be done by banks after fulfillment of stipulated terms & conditions Date of issue 19/09/2017 vide sanction order No. 22/CLTUC/RF-1/SIDBI/2014-15 Amount (in Rs.) S. No Name of the unit Address Amount sanctioned for subsidy 1 VARSHA INDUSTRIES NO 65-A-1, 65-A-2, 65-A-3, 65-A-6, HOOTAGALLI INDUSTRIAL AREA, MYSORE 509671 2 SHREE SWAMI DAYANAND SPINEERS PVT LTD R S No 348 A, Hupri Road Mudshingi, Tal Karveer Dist Kolhapur 1377000 3 Shree Hari Industries Plot no 8A, Vishwakarma Estate - 2, S No 232 P1 - P2, At Dhuva, Tal Wankaner, Dist - Morbi 382000 4 JYOTI RICE MILLS MEHRAJ ROAD, RAMPURA PHUL, TEHSIL-PHUL DISST- BHATHINDA, PUNJAB 422250 5 CUTTING EDGE ENGINEERING SOLUTION GAT NO 190 JYOTIBA NAGAR TALAWADE HAVELI PUNE PUNE 412114 374371 6 Sree Lakshmi Ganesh Enterprises plot no 177 industrial park kondapalli ibrahimpatnam krishna andhrapradesh 1018200 7 Natural Aromatics g 22 udyog kunj industrial area 1500000 8 Shankheshwar Enterprises b xxxii e 9/1396 street no 5 kali sarak 993000 9 NELSON LAMINATE PVT LTD SURVEY NO 394 P2 P1 HARIPAR KERALA ROAD 8A NATIONAL HIGHWAY NAVA SADULKA MORBI 1500000 363642 10 Jay Agro Industries plot no 1043 GIDC industrial estate Waghodiya Vadodara 1259487 11 vyom fasteners private limited c-89 kaushalya bunglows vill-nani kadi ta kadi 1500000 12 BEAS FIBRES 219 SECTOR-12 DISTT PANIPAT HARYANA 1500000 13 AMAN CREATION 45, B-34, KEHAR SINGH NAGAR, HAIBOWAL KALAN, Ludhiana 332495 14 Empire products Opp Gurdwara Somasar Sahib Vill Tibba Ludhiana Punjab 141003 542193 15 CHAKSON ENGINEERING COMPANY C-161, NARAINA INDUSTRIAL AREA, PHASE-I, NEW DELHI 1050000 16 BABA FARID INDUSTRIES C 10-11,focal point,Kotkapura 633000 17 PARTH ENGINEERS R S NO 275/1 PLOT NO 14 N H 8 BSHAPAR KOTDA SANGANI 469723 18 Shree Laxmi Engineering Pvt. -

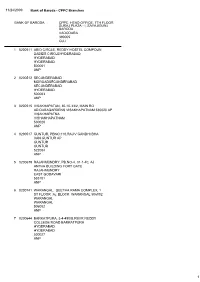

CPPC Branches BANK of BARODA CPPC, HEAD OFFICE, 7TH

11/24/2009 Bank of Baroda - CPPC Branches BANK OF BARODA CPPC, HEAD OFFICE, 7TH FLOOR SURAJ PLAZA - I, SAYAJIGUNJ BARODA VADODARA 390005. GUJ 1 0200511 ABID CIRCLE, REDDY HOSTEL COMPOUN DABIDS CIRCLEHYDERABAD HYDERABAD HYDERABAD 500001 ANP 2 0200512 SECUNDERABAD MGROADSECUNDERABAD SECUNDERABAD HYDERABAD 500003 ANP 3 0200515 VISAKHAPATAN, 30-10-33/2, MAIN RO AD DABAGARDENS VISAKHAPATNAM 530020 AP VISAKHAPATNA VISHAKHAPATNAM 530020 ANP 4 0200517 GUNTUR, PBNO:110,RAJIV GANDHI BHA VAN GUNTUR AP GUNTUR GUNTUR 522004 ANP 5 0200679 RAJAHMUNDRY, PB.NO-4, 31-1-40, AJ ANTHA BUILDING FORT GATE RAJAHMUNDRY EAST GODAVARI 533101 ANP 6 0200741 WARANGAL, SEETHA RAMA COMPLEX, 1 ST FLOOR `A¿ BLOCK WARANGAL 506002 WARANGAL WARANGAL 506002 ANP 7 0200644 BARKATPURA, 3-4-490/B,RBVR REDDY COLLEGE ROAD BARKATPURA HYDERABAD HYDERABAD 500027 ANP 1 11/24/2009 Bank of Baroda - CPPC Branches 8 0200939 CHARMINAR, 22-7-264, NIZAMBAGH, D IWAN DEODI CHARMINAR HYDERABAD HYDERABAD 500002 ANP 9 0200954 KHAIRATABAD, 6-1-84,KHUSRUJUNG HO USESECRETARIAT RDSAIFABAD HYDERABAD HYDERABAD 500004 ANP 10 0201264 ZAFARGARH, DOOR NO.1-51/1, MAIN R D MANDAL GHANPUR STN GHANPUR WARANG GHANPUR WARANGAL 506144 ANP 11 0201262 MARREDPALLY, WEST MARREDPALLY MAI N ROAD SECUNDERABAD SECUNDERABAD HYDERABAD 500026 ANP 12 0201312 NARMETTA, H.NO.4-98/1,MAIN RD.NAR METTAWARANGAL DT NARMETTA WARANGAL 506167 ANP 13 0201324 KADIPI KONDA, MAIN ROAD, KAZIPET, WARANGAL DIST AP WARANGAL WARANGAL 506003 ANP 14 0201809 JUBILEE HILL, PLOT 217 ROAD 17 JU BILEE HILLS HYDERABAD HYDERABAD HYDERABAD 500033 ANP -

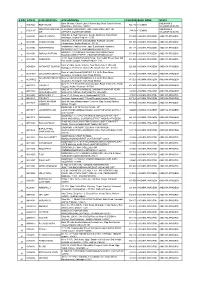

S No Atm Id Atm Location Atm Address Pincode Bank

S NO ATM ID ATM LOCATION ATM ADDRESS PINCODE BANK ZONE STATE Bank Of India, Church Lane, Phoenix Bay, Near Carmel School, ANDAMAN & ACE9022 PORT BLAIR 744 101 CHENNAI 1 Ward No.6, Port Blair - 744101 NICOBAR ISLANDS DOLYGUNJ,PORTBL ATR ROAD, PHARGOAN, DOLYGUNJ POST,OPP TO ANDAMAN & CCE8137 744103 CHENNAI 2 AIR AIRPORT, SOUTH ANDAMAN NICOBAR ISLANDS Shop No :2, Near Sai Xerox, Beside Medinova, Rajiv Road, AAX8001 ANANTHAPURA 515 001 ANDHRA PRADESH ANDHRA PRADESH 3 Anathapur, Andhra Pradesh - 5155 Shop No 2, Ammanna Setty Building, Kothavur Junction, ACV8001 CHODAVARAM 531 036 ANDHRA PRADESH ANDHRA PRADESH 4 Chodavaram, Andhra Pradesh - 53136 kiranashop 5 road junction ,opp. Sudarshana mandiram, ACV8002 NARSIPATNAM 531 116 ANDHRA PRADESH ANDHRA PRADESH 5 Narsipatnam 531116 visakhapatnam (dist)-531116 DO.NO 11-183,GOPALA PATNAM, MAIN ROAD NEAR ACV8003 GOPALA PATNAM 530 047 ANDHRA PRADESH ANDHRA PRADESH 6 NOOKALAMMA TEMPLE, VISAKHAPATNAM-530047 4-493, Near Bharat Petroliam Pump, Koti Reddy Street, Near Old ACY8001 CUDDAPPA 516 001 ANDHRA PRADESH ANDHRA PRADESH 7 Bus stand Cudappa, Andhra Pradesh- 5161 Bank of India, Guntur Branch, Door No.5-25-521, Main Rd, AGN9001 KOTHAPET GUNTUR 522 001 ANDHRA PRADESH ANDHRA PRADESH Kothapeta, P.B.No.66, Guntur (P), Dist.Guntur, AP - 522001. 8 Bank of India Branch,DOOR NO. 9-8-64,Sri Ram Nivas, AGW8001 GAJUWAKA BRANCH 530 026 ANDHRA PRADESH ANDHRA PRADESH 9 Gajuwaka, Anakapalle Main Road-530026 GAJUWAKA BRANCH Bank of India Branch,DOOR NO. 9-8-64,Sri Ram Nivas, AGW9002 530 026 ANDHRA PRADESH ANDHRA PRADESH -

Preface Under Section 4 of the Water Act, 1974 Government of Gujarat Constituted ‘Gujarat Pollution Control Board’ on 15Th October, 1974

Preface Under section 4 of the Water Act, 1974 Government of Gujarat constituted ‘Gujarat Pollution Control Board’ on 15th October, 1974. The Gujarat Pollution Control Board has been entrusted with the added responsibilities under various Environmental Acts. GPCB continued its efforts towards environment protection and better pollution control management. This Annual Report of GPCB is the statutory documentation of the activities carried out during the year 2016-2017. I am glad to share the following specific achievements of the GPCB: 1. Twenty seven regional offices & Four (04) Vigilance offices of the Board are functioning within the state at different locations to monitor and control the pollution sources from a shorter distance. 2. The Gujarat Pollution Control Board divided RO Kutch in to RO Kutch-West & RO Kutch-East to monitor and control the pollution sources from a shorter distance and also started the Laboratory at RO Kutch-West. 3. The Gujarat Pollution Control Board aims to develop all-round capabilities of the Board’s employees in the field of pollution prevention & control, Board induced more officers for the knowledge based training organized by CPCB, GPCB and other national and international organizations. 4. The Gujarat Pollution Control Board plays its role not merely as a regulator but off late, also developed a face as a facilitator. 5. In order to provide XGN system with ease to small & medium scale units (MSME), the Board has introduced avail free facility through Help Desk created at all Regional Offices including Head office. 6. Gujarat is leading in the country for the development of CETPs having total 31 operational CETPs with hydraulic capacity of approximately 556 MLD of serving approximately 5834 individual units. -

Medical Science Comparison of Economic Evaluation of Pavement Surface Maintenance by Micro Surfacing and Chip Seal

RESEARCH PAPER Engineering Volume - 5 | Issue - 1 | Jan Special Issue - 2015 | ISSN - 2249-555X Comparison of Economic Evaluation of Pavement Surface Medical Science Maintenance by Micro Surfacing and Chip Seal. KEYWORDS Hitesh A. Patel Chandresh G. Patel Dr. P. J.Gundaliya ABSTRA C T Micro-surfacing is a cost effective polymer modied cold mix paving system that can remedy a broad range of problems on today’s streets, highways and airelds. This paper presents economic evaluation of micro surfacing with chip seal for maintenance of Gozaria-Mahesana road, Gujarat state, India.The work describes review of different techniques of road maintenance on aspects of cost and also comparing estimating and costing between techniques. As output of the work best technique which can be used to perform in general course is suggested. I. INTRODUCTION intensity fatigue and block cracking, Restore surface Friction, Slurry surfacing originated in the 1930s in Germany, where it Temporary base course cover, Surface for light to medium was called “micro-asphalt concrete” (ISSA 2010a). It trafc ,Skid resistant surface etc.[3] Due to the severe growth consisted of a mixture of very ne aggregate, asphalt in trafc rate among many metro-Politian cities in India, road emulsion, and water. This technique for maintaining road treatment can't be done on every alternative year. So, it is surfaces started slurry surfacing development in the rest of essential to utilize a method which is economical than the the world. It was pioneered in Germany in the late 1960's and others as well as increases the life span of the road surface early 1970's. -

Instructions to Field Staff

DRAFT FOR OFFICIAL USE Instructions to Field Staff VOLUME-II SOCIO-ECONOMIC SURVEY NSS 57TH ROUND (JULY 2001 - JUNE 2002) SCHEDULES OF ENQUIRY Schedule 0.0: List of Households and Non-Agricultural Enterprises Schedule 2.345: Unorganised Services (excluding Trade and Finance) Schedule 1.0: Household Consumer Expenditure National Sample Survey Organisation Ministry of Statistics and Programme Implementation Government of India April 2001 Chapter One Introduction, Concepts, Definitions And Procedures 1.0 Introduction 1.0.1 The National Sample Survey (NSS), set up by the Government of India in 1950 to collect socio-economic data employing scientific sampling methods will start its fifty-seventh st round from 1 July 2001. 1.0.2 The fifty- seventh round of NSS is earmarked for collection of data on economic and operational characteristics of unorganized enterprises in service sector (excluding trade and finance), besides consumer expenditure and employment-unemployment. The field operations of the survey will commence on 1st July 2001 and will continue up to 30th June 2002. 1.0.3 During 1977, the first All-India Economic Census was conducted by the Central Statistical Organization (CSO) in collaboration with the State Statistical Bureaus with the objective of collecting some basic information on non-agricultural enterprises employing at least one hired worker on a fairly regular basis (hereinafter referred to as 'establishments'). Following this census, small establishments and enterprises not employing any hired worker on a fairly regular basis [and henceforth called 'own account enterprises' (OAEs)] engaged in the activities of trade, transport, hotels & restaurants and services was conducted by NSSO as part of its 34th round (1979-80) while larger establishments of these activities were surveyed by CSO during 1979-80. -

VG-2015 MSME - Approved Investment Intentions District : Mehsana Sr.No

VG-2015 MSME - Approved Investment Intentions District : Mehsana Sr.No. Name of Company Office Address 1 A I AGRO INDUSTRIES SHAHUPURA,,Shahupura (Gadh)-384350,Satlasana,Mehsana 2 A One Industies Plot No. 159 GIDC-2 Dediyasan, Mehsana,,Dediyasan-Mehsana,Mehsana 3 A R TUBE INDUSTRIES 265 G I D C -11 BESIDE MADHAV WIRE DEDIYASAN,,Dediyasan-Mehsana,Mehsana 4 AARYA BITUMEN INDUSTRIES LLP SR NO-455, SOBHASAN ROAD,SOBHASAN,Sobhasan-Mehsana,Mehsana 5 Aashish Industries Shed No. C1-60, GIDC-2 Mehsana,,Dediyasan-Mehsana,Mehsana 6 ABHAY ENGINEERING NR ESSAR PETROLPUMP,VISNAGAR ROAD MEHSANA,Mahesana-Mehsana,Mehsana 7 ABHAY ENGINEERING SR NO-732,NR S R PETROL PUMP,VISNAGAR ROAD, MEHSANA,Mahesana-384001,Mehsana,Mehsana 8 ABHIRAJ INDUSTRIES SURVEY NO. 532, SADRA-BHOYANI ROAD,,Sadra-Kadi,Mehsana 9 accurate engineering 13 kukarwada,,Kukarvada-Vijapur,Mehsana 10 Accurex Control Systems Plot No. 374, GIDC-2, Dediyasan, Mehsana,,Dediyasan-Mehsana,Mehsana 11 ACHYUT PACKAGING SR NO-2108/1 UNAVA,,Unava-Unjha,Mehsana 12 ACHYUT PACKAGING PVT LTD SR NO-2108/1,OPP SAHIL HOTEL,AT & PO-UNAVA,Unava-Unjha,Mehsana 13 ADARSH EDUCATION TRUST SARTANPUR,,Sartanpur (Gadh)-384330,Satlasana,Mehsana 14 ADROIT AQUATECH PVT LTD 33-34-35,SHOMESHWAR COMPLEX, OPP-PUJAN COMPLEX, MODHERA ROAD,,Mahesana-384002,Mehsana,Mehsana 15 ADVANCE EXPLORATION 7 NIRAMAN NAGAR SOCIETY NR JAY VIJAY SOCIETY DHOBI GHAT ROAD MEHSANA 384001,,Mahesana-384001,Mehsana,Mehsana 16 AGARWAL TRADERS 8/16/25 RAILWAY STATION ROAD , UNJHA,,Unjha-Unjha,Mehsana 17 AGRO PRICAST PIPE KUKAS,,Kukas-Mehsana,Mehsana 18 AGROW INDIA 46, Gunj Bazar, Market Yard, Visnagar,,Visnagar-384315,Visnagar,Mehsana 19 Akash Industries Plot No. -

Brief Industrial Profile of Mehsana District

Government of India Ministry of MSME Brief Industrial Profile of Mehsana District Carried out by MSME – DEVELOPMENT INSTITUTE Govt. of India Ministry of Micro, Small & Medium Enterprises Harsiddh Chambers, 4th Floor, Ashram Road, Ahmedabad-380 014 Tel.No. 079-27543147 & 27544248, Fax No.079-27540619 E-mail: [email protected] Website: www.msmediahmedabad.gov.in A C K N O W L D G E M E N T In the preparation of this District Industrial Profile of Jamnagar District, the Institute acknowledges the support and assistance of following Department for providing us the information and details: 1. District Industries Centre, Mehsana 2. Lead Bank –State Bank of India, Mehsana 3. District Agriculture Office, Mehsana 4. Animal Husbandry Office, Mehsana 5. Road and Building (PWD), Mehsana 6. GM, BSNL Telecom District, Mehsana 7. Dy. Conservator of Forest, Mehsana 8. Geology & Mining, Mehsana 9. District Statistical Office, Mehsana 10. GIDC, Mehsana 11. NABARD, Mehsana 12. District Education Office, Mehsana 13. Primary Education Office, Mehsana 14. Supdt. Of Post Office, Mehsana 15. Collector Office, Mehsana CONTENTS Sr.No. Topic Page No. 1. General Characteristics of the District 1 1.1 Location & Geographical Area 1 1.2 Topography 1 1.3 Availability of Minerals 1 1.4 Forest 2 1.5 Administrative set up 2 2. District at a glance 2 - 4 2.1 Existing Status of Industrial Area in the Mehsana District 4 3. Industrial Scenario of Mehsana District 5 3.1 Industry at a Glance 5 3.2 Year Wise Trend of Units Registered 5 3.3 Details of Existing Micro & Small Enterprises & Artisan Units in The District 5-6 3.4 Large Scale Industries/Public Sector undertakings 6 3.5 Major Exportable Item 6 3.6 Growth Trend 6 3.7 Vendorisation/Ancillarisation of the Industry 6 3.8 Medium Scale Enterprises 6 3.8.1 List of the unit in Medium Scale Industries in Mehsana & nearby Area 6-7 3.8.2 Major Exportable Item 8 3.9 Service Enterprises 8 3.9.1 Coaching Industry 8 3.9.2 Potentials areas for service industry 8 3.10 Potential for new MSMEs 8 4. -

Unclaimed Dividend 2011-12 As on 19-09-15

First Middle Last Father/H Father/H Father/H Address Country State District PINCode Folio Number of Investm Amount Proposed Name Name Name usband usband usband Securities ent Type Due(in Rs.) Date of First Middle Last transfer to Name Name Name IEPF (DD-MON- YYYY) A RAMDAS VAYYAPEN RAMDAS VAYYAPEN KOTTAPURATHU HOUSE, RAMAPURAM KEERIKADU INDIA Kerala Alappuzha 690508 0010180 Amount for150.00 unclaimed26-NOV-2019 and unpaid dividend RAJENDRA MADANLALMUNOT MADANLAL MUNOT DALMANDAI INDIA MaharashtraAhmednagar414001 0011234 Amount for150.00 unclaimed26-NOV-2019 and unpaid dividend RAMESH SONAJIRAOJADHAV SONAJIRAO JADHAV JUNIOR ENGINEER, M.S.E.B.,AT SONAI, TQ NEWASA,DIS. AHEMEDNAGAR INDIA MaharashtraAhmednagar414105 0011271 Amount for150.00 unclaimed26-NOV-2019 and unpaid dividend POPATLAL KANTILAL BHANDARI KANTILAL BHANDARI 375-A/P SHRI SHIVAJI NAGAR, TAL RAHURI INDIA MaharashtraAhmednagar413706 11628441 Amount for200.00 unclaimed26-NOV-2019 and unpaid dividend SHEKHAR KAILASH AJMERA KAILASH AJMERA 1438, SUDESH TAKIJ PARISAR,GRAM KOPARGAON, INDIA MaharashtraAhmednagar423601 10605977 Amount for2.00 unclaimed26-NOV-2019 and unpaid dividend ABHISHEK TUTEJA TUTEJA 'F-12 MALKA GANJ INDIA Delhi Delhi 110007 0010185 Amount for150.00 unclaimed26-NOV-2019 and unpaid dividend MANISH PARAGBHAIGAMI GAMI PARAGBHAI GAMI GAMI F/8, SULABH FLATS, NEAR MIRAMBIKA SCHOOL, NAVRANGPURA, INDIA Gujarat Ahmedabad380013 0012174 Amount for300.00 unclaimed26-NOV-2019 and unpaid dividend MANISH S KOTHARI S KOTHARI 904, SHANTI TOWER, NR. TULSI PARTI PLOT, B/H, VASNA BUS -

Regional Office, Banaskantha Office At: Shriram Complex, 2Nd Floor

Regional Office, Banaskantha Office At: Shriram Complex, 2nd Floor, Radhanpur Road, Mehsana, - 384002 Tel : 02762-254080,251003,7567883435 Fax : 02762- 250874 Email : [email protected] SALE NOTICE FOR SALE OF IMMOVEABLE/MOVABLES PROPERTIES [Under Rule 6(2) and 8(6) of Security Interest (Enforcement) Rules, 2002] E-auction sale notice for sale of movable/immovable assets under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 read with proviso to rule 6(2) and 8(6) of the Security Interest (Enforcement) Rules, 2002. Notice is hereby given to the public in general and in particular to the Borrower (s) Guarantor (s) that the below described movable/ immovable properties hypothecated/mortgaged/charged to the Bank of Baroda [Erstwhile Dena Bank amalgamated into Bank of Baroda with effect from 1st April 2019 in term of Gazette of India No. GSR No. 2E dated 2nd January 2019 issued by Ministry of Finance, Government of India] a body corporate constituted under the Banking Companies (Acquisition and Transfer of Undertaking) Act 1970 and having its Head office at Mandvi, Baroda, Gujarat State and one of the Branch mentioned as below as the secured creditor, the constructive / physical possession of which has been taken by the Authorised officer of Secured Creditor under section 13(4) of the Act, will be sold on “As is where is”, As is what is” and “Whatever there is” on 26.09.2019 for recovery of Rs. (as mentioned below) due to the Bank Of Baroda secured creditor from (Name of Borrower & Guarantor mentioned below). -

(MBA FB & E) Admission 2021

Admission 2021 Students’ Information Bulletin MBA Family Business & Entrepreneurship (MBA FB & E) प्रा셍थना याकु ꅍदेꅍदतु ुषारहारधवऱायाशभ्रु वस्त्रावतृ ा यावीणावरद赍डमण्赍डतकराया�वेतऩ饍मासना याब्रह्मा楍युतशकं रप्रभतृ तभभदेवै: सदावण्ꅍदता सामांऩातुसरस्त्वतीभगवतीतन:शेषजा蕍याऩहा Meaning - Salutations to Devi Saraswati, Who is pure white like Jasmine, with the coolness ofMoon, brightness of Snow and shine like the garland of Pearls; and Who is covered with purewhite garments, Whose hands are adorned with Veena (a stringed musical instrument) and theboon-giving staff; and Who is seated on pure white Lotus, Who is always adored by LordBrahma, Lord Acyuta (Lord Vishnu), Lord Shankara and other Devas, O Goddess Saraswati, pleaseprotect me and remove my ignorance completely. PREAMBLE This Information Bulletin contains information about Nirma University (NU), Institute of Management (IM), and Master of Business Administration Programmes offered by the Institute of Management. It also contains a summary of the Rules and Regulations about the academic requirements and academic and personal conduct of the students at the University. Further, the bulletin carries the important information on registration, curriculum, grading system, academic standards, attendance norms and the like. It is the responsibility of all the students to familiarize themselves with the rules and regulations of the Institute as well as of the University. The University reserves the right to amend the rules and regulations mentioned in the Handbook without any prior notice. The decision of the University shall be final on all matters. This bulletin is for the purpose of providing general information to the applicant about the University and its programmes and (is) not a Regulation book of the University.