Adani Gas Limited: Rating Upgraded to [ICRA]AA-/A1+; Removed from Watch with Positive Implications and Stable Outlook Assigned

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

GC Influencers Have Been Chosen Following Research Among Private Practice Lawyers and Other In-House Counsel

v GC Influencers INDIA 2019 Thursday, 14th February 2019 Hyatt Regency Delhi Programme Engaging content, networking and celebration with leading General Counsel and top ranked lawyers globally. GC Influencers For more informationINDIA visit 2019 chambers.com A5-Advert-Forums.idml 1 22/10/2018 12:17 Welcome SARAH KOGAN Editor Chambers Asia-Pacific Meet the most influential General Counsel in India today. Chambers has provided insight into the legal profession for over 30 years. During this time, in-house lawyers and third-party experts have shared their views on the value and importance placed on the role of the General Counsel. No longer just the ethical and legal heart of a business, these professionals now sit as influential participants at board level. Effective mangers, industry pioneers, diversity and CSR champions: these Influencers show the way. Research Methodology: Our GC Influencers have been chosen following research among private practice lawyers and other in-house counsel. We identified the key areas in which GCs have displayed substantial influence: Engaging content, • Effective management and development of an in-house team • Navigation of substantial business projects such as M&A or strategic networking and business change. • Development of litigation strategy and understanding the pressures faced celebration with leading within industry General Counsel and top • Bringing diversity & inclusion and CSR to the forefront of industry. ranked lawyers globally. • Ability to influence and respond to regulatory change Our aim is to celebrate excellence within the legal profession. This dynamic hall of fame encourages collaboration among the in-house legal community. Our GC Influencers have created best practice pathways endorsed by both private practice and other in-house lawyers. -

Sustainable Growth with Goodness

Annual Report 2018-19 Sustainable Growth with Goodness “Excellence happens not by accident. It is a through our Project SuPoshan. SuPoshan has process. You have to work hard to achieve it” also been recognised at the global stage with - Dr. APJ Abdul Kalam the esteemed Public Affairs Asia (PAA) Gold Standard Award for Corporate Citizenship Our strive to achieve excellence during the (Community Relations). The project also won year in creating sustainable impact on the the silver award at the 53rd SKOCH State grounds echoed the above words of wisdom of Governance Summit 2018 and the from Dr. Kalam. Dainik Jagran CSR Awards for exceptional When we began the journey of Adani contribution towards Public Health. Foundation in 1996, we had set a goal to play Like every year, our teams went out of the the role of a facilitator to help people empower way to help people in times of crisis. One of themselves. Along the journey, aspiration of the devastating natural disasters that struck our beneficiaries and perspiration of our team the country this year was the floods in Kerala, members have been the motivating forces. in August. Within hours of the calamity, our Adani Vidya Mandir (AVM) Ahmedabad and on-ground teams worked relentlessly, Adani Public School Mundra created a participating in rescue coordination and flood benchmark by attaining the NABET relief activities in the worst affected areas. Accreditation under the Quality Council of The team of staff and volunteers, travelled India. AVM Ahmedabad has become the first through nights to remote villages distributing cost-free school in India to receive the NABET thousands of relief kits that included rations, accreditation; APS Mundra is the first school clothes and other necessary supplies. -

Adani Power (Jharkhand) Ltd

Intake Water System Detailed 2X800MW Thermal Power Plant, Godda , Jharkhand Project Project Proponent Adani Power (Jharkhand) Ltd. Report A Detail Project Report on Proposed Water Pipeline Route of 1600 (2 x 800) MW GODDA THERMAL POWER PROJECT GODDA, JHARKHAND ADANI POWER (JHARKHAND) LTD. Village - Motia, Tehsil Godda, District Godda, Jharkhand 1 Intake Water System Detailed 2X800MW Thermal Power Plant, Godda , Jharkhand Project Project Proponent Adani Power (Jharkhand) Ltd. Report Contents 1. GENERAL INFORMATION ................................................................................ 3 1.1 Company Profile ............................................................................................... 4 2. PROJECT BACKGOROUND / REQUIREMENT ............................................... 4 3. LOCATION MAP & KEY PLAN ......................................................................... 5 3.1 Jharkhand State Map ........................................................................................... 5 3.2 Godda Districts ..................................................................................................... 5 3.3 Project Site Water Intake location ................................................................ 6 3.4 Proposed Water Pipe Line Route ...................................................................... 6 4. KEY FEATURES OF THE PROJECT SITE ........................................................ 7 4.1 Site Location Details: .......................................................................................... -

Dossier on the Adani Group's Environmental and Social Record

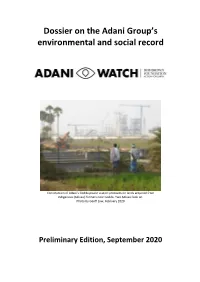

Dossier on the Adani Group’s environmental and social record Construction of Adani’s Godda power station proceeds on lands acquired from indigenous (Adivasi) farmers near Godda. Two Adivasi look on. Photo by Geoff Law, February 2020 Preliminary Edition, September 2020 Preamble AdaniWatch is a non-profit project established by the Bob Brown Foundation to shine a light on the Adani Group’s misdeeds across the planet. In Australia, Adani is best known as the company behind the proposed Carmichael coal mine in Queensland. However, the Adani Group is a conglomeration of companies engaged in a vast array of businesses, including coal-fired power stations, ports, palm oil, airports, defence industries, solar power, real estate and gas. The group’s founder and chairman, Gautam Adani, has been described as India’s second-richest man and is a close associate of Indian Prime Minister Narendra Modi. The Adani Group is active in several countries but particularly in India, where accusations of corruption and environmental destruction have dogged its rise to power. In central India, Adani intends to strip mine ancestral lands belonging to the indigenous Gond people. Large tracts of biodiverse forest, including elephant habitat, are in the firing line. Around the coastline of India, Adani’s plans to massively expand its ports are generating outcry from fishing villages and conservationists. In the country’s east, Adani is building a thermal power station designed to burn coal from Queensland and sell expensive power to neighbouring Bangladesh. Investigations, court actions and allegations of impropriety have accompanied Adani’s progress in many of these business schemes. -

Annual Report 2020-21

SMART Annual Report 2020-21 The 2-minute Annual Report Adani Green Energy Limited Our company is the world’s largest solar power generation company and will be the largest renewable power company by FY 29-30 The most powerful trigger for renewable energy growth in India 225 GW 450 GW India’s target for India’s target for renewable energy renewable energy capacity by 2022 capacity by 2030 The most effective triggers for renewable energy • Increasingly considered to be the bedrock of a progressive society • Government policies are driving the growth of the sector • India’s renewable share of energy mix 40% by 2030 • India to reduce carbon emissions by 33-35% (from the 2005 level) by 2030 Some of our key achievements of FY 20-21 – 1 55 3,470 % CAGR in MW, total installed operational capacity as on 31 capacity in five March 2021 years 925 13,700 MW assets added MW of bids for during the year which the company (575 MW greenfield emerged L1 bidder/ + 350 MW LOAs received acquisitions) Some of our key achievements of FY 20-21 – 2 3.93 ~25 US$ billion asset US$ billion Fully- base built asset base (USD/INR rate of 73.11) 50:50 JV between AGEL US$1.35 billion senior ~100 and TOTAL for 2,353 debt facility (one of % fixed PPA life; 25- MW solar assets Asia’s largest proj- year tariff profile (operational) and a ect financing deals), 20% equity stake with participation acquisition in AGEL from 12 internation- by TOTAL al banks Our broad-based resource mix 11,023 1,927 2,290 MW, Solar energy MW, Wind MW, Hybrid (solar- capacity, 31 energy wind) capacity, 31 March 2021 capacity, 31 March 2021 March 2021 Chairman Gautam S Adani’s overview COVID-19 is a wakeup call for all of us to While we can look back and feel satisfied about transform ourselves. -

Adani (Mundra) Port, Kutch, Gujarat

A Report on Industrial Visit At Adani (Mundra) Port, Kutch, Gujarat Organized By DEPARTMENT OF ELECTRICAL ENGINEERING Industry Profile: Company Name: Mundra Port & Special Economic Zone Ltd. Address: Adani House, Nr. Mithakhali Circle Navrangpura, Ahmedabad, Gujarat. PIN Code: 380009. Phone: Tel +91 79 2656 5555 Fax +91 79 2656 550 Homepage: [email protected] Work profile: Natural gateway for the cargo hubs functioning in the Northern and Western states of India as well as the NCR. About Mundra Port: Mundra Port is the largest private port of India located on the north shores of the Gulf of Kutch near Mundra, Kutch district, Gujarat. Formerly it was operated by Mundra Port and Special Economic Zone Limited (MPSEZ) owned by Adani Group which later it was expanded into Adani Ports & SEZ Limited (APSEZ) managing several ports. In 2013-2014, Mundra Port has handled 100 million tons of cargo in a year becoming the first Indian port to do so. It also became India's biggest port by cargo handled. About Visit: Department of Electrical Engineering organized the visit to Adani Mundra Port for the student of 6th sem B.Tech and Diploma Electrical on 23rd and 24th February 2018. Branch and No. of Date of Visit Accompanied Faculties Semester Students Mr. Bhargav D. Patel Electrical 8th & 6th Mr. Lokesh Shah 23/02/2018 76 Diploma Ms. Arpita Patel Mrs. Chand D Thakur M.Tech 2nd & Mr. Mayank Kapadiya 24/02/2018 38 Electronics 8th Ms. Karmani Rajput Activities on the Day of Visit: The private buses were boarded up to Ahmedabad. -

Indigo Soars with $33Bn A320neo Order

EEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE THE HINDU DELHI WEDNESDAY, OCTOBER 30, 2019 BUSINESS 15 EEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE market watch Awaiting clarity on AGR, 29-10-2019 % CHANGE Sensex dddddddddddddddddddddd 39,832 ddddddddddddddd1.48 IndiGo soars with $33bn A320neo order US Dollardddddddddddddddddddd 70.84 ddddddddddddddd0.08 Gold ddddddddddddddddddddddddddd 38,857 ddddddddddddd-1.39 Bharti defers Q2 results Brent oil ddddddddddddddddddddd 61.62 ddddddddddddddd0.16 300plane order is Airbus’ largest ever with a single airline; to take IndiGo’s A320neo count to 730 ‘Moving DoT to arrive at total amount’ SPECIAL CORRESPONDENT economic growth and mobil IndiGo is keen on the MUMBAI ity,” Ronojoy Dutta, CEO, In A321XLR, which is the next Special Correspondent matter arising out of recent N IFTY 50 InterGlobe Aviation Ltd., diGo, said in a statement. evolutionary -

Carmichael Coal Mine: a Case Study

Law Environment and Development JournalLEAD A CASE STUDY OF THE CARMICHAEL COAL MINE FROM THE PERSPECTIVES OF CLIMATE CHANGE LITIGATION AND SOCIO-ECONOMIC FACTORS Sandra Cassotta, Vladimir Pacheco Cueva & Malayna Raftopoulos ARTICLE VOLUME 17/1 LEAD Journal (Law, Environment and Development Journal) is a peer-reviewed academic publication based in New Delhi and London and jointly managed by the Law, Environment and Development Centre of SOAS University of London and the International Environmental Law Research Centre (IELRC). LEAD is published at www.lead-journal.org [email protected] ISSN 1746-5893 ARTICLE A CASE STUDY OF THE CARMICHAEL COAL MINE FROM THE PERSPECTIVES OF CLIMATE CHANGE LITIGATION AND SOCIO-ECONOMIC FACTORS Sandra Cassotta, Vladimir Pacheco Cueva & Malayna Raftopoulos This document can be cited as Sandra Cassotta, Vladimir Pacheco Cueva & Malayna Raftopoulos, ‘A Case Study of the Carmichael Coal Mine from the Perspectives of Climate Change Litigation and Socio-Economic Factors’, 17/1 Law, Environment and Development Journal (2021), p. 55, available at http://www.lead-journal.org/content/a1704.pdf Sandra Cassotta, Associate Professor in International, Environmental and Energy Law, Department of Law, Aalborg University, E-mail: [email protected]. Vladimir Pacheco Cueva, Associate Professor, School of Cultural and Society, Aarhus University. Malayna Raftopoulos, Associate Professor in Development Studies and International Relations/Latin American Studies, Department of Politics and Society. Published under a Creative Commons -

Aban Offshore ABG Shipyard ACC Limited Adani Group Aditya Birla

A . Aban Offshore . Amul[8] . ABG Shipyard . Andhra Bank . ACC Limited . Apollo Hospitals[9] . Adani Group . Apollo Tyres[10] . Aditya Birla Group.[2] . Archies Greetings & Gifts Ltd[11] . Ador Powertron Limited[3] . Aptech . Aftek . Arvind Mills . Air India[4] and subsidiary Air-India Express[5] . Ashok Leyland[12] . Air Sahara[6] . Asia Motor Works . Ajanta Group . Asian Paints[13][14] . Alang Ship Recycling Yard[7] . Axis Bank . Allahabad Bank . Ambuja Cements . Amrutanjan Healthcare [edit]B . Bajaj Auto[15] . Bhushan Steel . Balaji Telefilms[16] . Biocon . Bank of India[15] . BMR Advisors[21] . Bank of Baroda[17] . Bombay Dyeing[22] . Bharat Aluminium Company[18] . BPL group[23] . Bharat Electronics Limited[19] . Ballarpur Industries Limited[24] . Bharat Forge[20] . Bharat Earth Movers Limited . Bharat Heavy Electricals Limited[15] . Britannia Industries[25] . Bharat Petroleum[15] . BirlaSoft . Bharat Sanchar Nigam Limited . Bharati Shipyard . Bharti Airtel [edit]C . Camlin Ltd. Coal India Limited[31] . CMC Limited[26] . Container Corporation of India . Canara Bank[15] . Crest Animation Studios[32] . Cellebrum Technologies Limited[27] . Crompton Greaves . Central Bank of India . Cadila Healthcare[33] . CESC . Coromandel International[34] . CPCL . Catholic Syrian Bank . Cipla[28] . Cosmic Circuits . Club Mahindra Holidays[29] . Covansys India Limited[30] [edit]D . Dabur India Limited[35] . Dr. Reddy's . Damodar Valley Corporation[36] Laboratories[40] . Deccan Aviation Pvt. Ltd.[37][38] is an aviation company that operates Air . DLF Universal Limited Deccan . Directi . Delhi Metro Rail Corporation Limited[39] [edit]E . Educomp Solutions . Essar Group[44] . Eicher Motors[41] . Eureka Forbes . Engineers India Limited[42] . EID Parry . English Indian Clays Limited[43] . Evalueserve[45] . Escorts Group . -

Adani Gas Ltd Investor Presentation

Adani Gas Ltd Investor Presentation March 2019 Legal Disclaimer Certain statements made in this presentation may not be based on historical AGL assumes no responsibility to publicly amend, modify or revise any forward information or facts and may be “forward-looking statements,” including looking statements, on the basis of any subsequent development, information those relating to general business plans and strategy of Adani Gas Limited or events, or otherwise. Unless otherwise stated in this document, the (“AGL”), its future outlook and growth prospects, and future developments in information contained herein is based on management information and its businesses and competitive and regulatory environment, and statements estimates. The information contained herein is subject to change without which contain words or phrases such as ‘will’, ‘expected to’, etc., or similar notice and past performance is not indicative of future results. AGL may alter, expressions or variations of such expressions. Actual results may differ modify or otherwise change in any manner the content of this presentation, materially from these forward-looking statements due to a number of factors, without obligation to notify any person of such revision or changes. including future changes or developments in its business, its competitive No person is authorized to give any information or to make any representation environment, its ability to implement its strategies and initiatives and not contained in and not consistent with this presentation and, if given or respond to technological changes and political, economic, regulatory and made, such information or representation must not be relied upon as having social conditions in India. This presentation does not constitute a been authorized by or on behalf of AGL. -

Aviation Regulator DGCA on Saturday Suspended a First Officer of Spice

1 Revue de presse du 29 aout au 13 septembre 2019 Mumbai: Aviation regulator DGCA on Saturday suspended a first officer of SpiceJet for three months for mishearing an Air Traffic Control clearance, due to which he gave incorrect direction to the pilot-in-command (PIC), causing runway incursion at Mumbai airport, said a source. "DGCA probe found that Atul Yadav, who was first officer on Surat-Mumbai flight on July 5, told the PIC that their plane was cleared by ATC to cross runway 14. The truth is the clearance was given to the IndiGo plane that was ahead of his plane," the source told PTI. The SpiceJet plane had the call sign SEJ2763. When the regulator issued a show-cause notice to Yadav on August 19, he responded by admitting his mistake and stating the incursion happened on July 5 because another plane with a similar call sign which was ahead of their plane had received the ATC clearance to cross runway 14, the source said. The aircraft ahead of the SpiceJet plane was of IndiGo and it had a call sign IGO063, the source said. 31/08/19 PTI/Business Today New Delhi: In the last 2.5 years, IndiGo Airbus A320 Neos have on an average seen one faulty Pratt & Whitney (PW) engines powering these planes being changed every week. The Directorate General of Civil Aviation (DGCA) has in a RTI reply said 126 PW engines on IndiGo Neos have been replaced from 2016 to June 30, 2019. The almost once-a-week average of faulty engine replacement comes with 46 engines being replaced in calendar years 2017, 2018 each and 27 in the first six months of this year (remaining 7 in 2016). -

Outcome of Board Meeting

Media Release Adani Enterprises Consolidated Income from operations is Rs 44,023 crore in FY16 Consolidated EBIDTA is Rs 3,114 crore in FY16 CLARIFICATION NOTE With respect to the financial results for the fourth quarter and year ended 31st March, 2016 for Adani Enterprises Limited, please note that the statutorily published quarter and year-end figures are not comparable with the corresponding period, consequent to demerger of Ports, Power and Transmission businesses effective from 1st April 2015. EDITOR’S SYNOPSIS Operational Highlights: In FY16, Coal Mining volume grew by 85% to 5.5 MMT In FY16, City Gas Distribution volume is 381 MMSCM In FY16, Agro volume grew to 1.6 MMT Financial Highlights (Consolidated): Consolidated Income from operations for FY16 is Rs 44,023 crore Consolidated EBIDTA for FY16 is Rs 3,114 crore Consolidated PAT for FY16 is Rs 1,041 crore Consolidated Income from operations for Q4FY16 is Rs 10,950 crore Consolidated EBIDTA for Q4FY16 is Rs 731 crore Consolidated PAT for Q4FY16 is Rs 167 crore Ahmedabad, May 4, 2016: Adani Enterprises Ltd, the flagship company of the Adani Group, today announced its results for the fourth quarter and financial year ended March 31, 2016. Financial Highlights: The consolidated Total Income from Operations for the financial year ended March 31, 2016 is Rs 44,023 crore. The consolidated EBIDTA for the financial year is Rs 3,114 crore. The consolidated PAT for FY16 is Rs 1,041 crore. Adani Enterprises Ltd (CIN No : L51100GJ1993PLC019067) Registered Office : Adani House, Nr Mithakhali Circle, Navrangpura, Ahmedabad 380 009, Gujarat, India Phone : 079‐26565555 ; Fax : 079‐26565500 ; Email : [email protected] ; Website : www.adani.com The Consolidated Income from Operations for the quarter is Rs 10,950 crore.