Oklahoma Court of Criminal Appeals

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FY-08 Legislative Appropriations

Oklahoma House of Representatives FY‐08 Legislative Appropriations Centennial Edition Fiscal Year 2008 Legislative Appropriations Oklahoma House of Representatives Speaker Lance Cargill Appropriations and Budget Committee Representative Chris Benge, Chairman Representative Ken Miller, Vice Chair July, 2007 Prepared by: House Fiscal Staff Committee and Subcommittee Membership Appropriations and Budget Committee Chris Benge, Chair Ken Miller, Vice Chair John Auffet Guy Liebmann John Carey Bill Nations James Covey Randy Terrill Shane Jett Revenue & Taxation Subcommittee Randy Terrill, Chair Danny Morgan, Vice Chair Dale DeWitt Richard Morrissette Joe Dorman Earl Sears Tad Jones Rules Committee Shane Jett, Chair Bill Nations, Vice Chair James Covey Ryan Kiesel Joe Dorman Greg Piatt Rob Johnson Trebor Worthen Tad Jones Elections & Redistricting Subcommittee Trebor Worthen, Chair Purcy Walker, Vice Chair Dennis Adkins Randy Terrill Ryan McMullen Page i Education Committee Tad Jones, Chair Todd Thomsen, Vice Chair Neil Brannon Sally Kern Ann Coody Ray McCarter Doug Cox Jeannie McDaniel David Dank Eric Proctor Lee Denney Phil Richardson Joe Dorman Jabar Shumate Terry Hyman Dan Sullivan Terry Ingmire Common Education Subcommittee Ann Coody, Chair Neil Brannon, Vice Chair Ed Cannaday Weldon Watson Dale DeWitt Susan Winchester Ray McCarter Higher Education & Career Tech Subcommittee Terry Ingmire, Chair David Derby, Vice Chair Terry Hyman Pam Peterson Charlie Joyner Jabar Shumate Bill Nations Arts & Culture Subcommittee Lee Denney, Chair Ben Sherrer, -

Alumni Inducted Into Order of the Owl Jessica R

Sooner Lawyer Archive Volume 2013 | Issue 2 Fall 2013/Winter 2014 2013 Alumni Inducted into Order of the Owl Jessica R. Jones Follow this and additional works at: https://digitalcommons.law.ou.edu/soonerlawyer Part of the Legal Education Commons Recommended Citation Jones, Jessica R. (2013) "Alumni Inducted into Order of the Owl," Sooner Lawyer Archive: Vol. 2013 : Iss. 2 , Article 5. Available at: https://digitalcommons.law.ou.edu/soonerlawyer/vol2013/iss2/5 This Article is brought to you for free and open access by the OU College of Law Archives at University of Oklahoma College of Law Digital Commons. It has been accepted for inclusion in Sooner Lawyer Archive by an authorized editor of University of Oklahoma College of Law Digital Commons. For more information, please contact [email protected]. ALUMNI INDUctED INTO Order OF THE Owl | BY Jessica R. Jones | 10PublishedSOONER by University L AW YERof Oklahoma College of Law Digital Commons, 2013 Michael Burrage Kathy Taylor Ralph G. Thompson Lee West n a night full of laughter and heartfelt tributes, the University of Oklahoma College of Law had the privilege of inducting four distinguished alumni into the Order of the Owl Hall of Fame. Michael Burrage (’74), Kathy Taylor (’81), Ralph G. Thompson (‘61) and the Lee West (’56) became the third class of inductees honored Iat an October 30 dinner in the Molly Shi Boren Ballroom of Oklahoma Memorial Union. The Order of the Owl recognizes OU Law graduates who have made an indelible mark on the legal profession. The honorees are chosen based on their demonstrated leadership and service through outstanding accomplishments in their careers. -

Proceedings Honoring Judge William J. Holloway, Jr., on Thirty Years

OCULREV Spring 2015 61 0420 Thirty Years Proceedings 247--276 (Do Not Delete) 4/20/2015 2:50 PM 2015] Proceedings Honoring Thirty Years Service as Judge 247 In the United States District Court for the Western District of Oklahoma Proceedings Honoring Honorable William J. Holloway, Jr. On Thirty Years’ Service as Judge of the United States Court of Appeals for the Tenth Circuit, 1968–1998 5:00 p.m. September 25, 1998 Ceremonial Courtroom Third Floor United States Courthouse Fourth and Robinson Oklahoma City, Oklahoma [Editor’s note: Reprinted from 51 F. Supp. 2d LI (1998).] OCULREV Spring 2015 61 0420 Thirty Years Proceedings 247--276 (Do Not Delete) 4/20/2015 2:50 PM 248 Oklahoma City University Law Review [Vol. 40 Oklahom Oklahoma City, Oklahoma Top: 30th Anniversary Proceeding with Chief Judge Stephanie Seymour, presiding. Bottom: Gift from Oklahoma City University to express the great admiration held for Judge Holloway as a distinguished jurist and the University’s deep affection for Judge Holloway and his faithful friendship. OCULREV Spring 2015 61 0420 Thirty Years Proceedings 247--276 (Do Not Delete) 4/20/2015 2:50 PM 2015] Proceedings Honoring Thirty Years Service as Judge 249 Proceedings CHIEF JUDGE SEYMOUR: Good afternoon, ladies and gentlemen. Welcome to this extraordinary session of the 10th Circuit Court of Appeals. We are here today to celebrate the 30th anniversary of the appointment of Judge William J. Holloway to our court, who until about two minutes ago thought he was coming to an administrative meeting. We are honoring the affection and respect of our colleague and friend, for whom we have the highest regard. -

Oklahoma House of Representatives

Oklahoma FY-05 Legislative Appropriations House of Representatives Legislative Appropriations Oklahoma House of Representatives Speaker Larry Adair Appropriations and Budget Committee Representative Bill Mitchell, Chairman Representative Jack Bonny, Vice Chairman August, 2004 Research, Legal and Fiscal Divisions George V. Moser, Executive Director Debbie Terlip Scott C. Emerson Gregory Sawyer Acting Research Director Chief Counsel Fiscal Director APPROPRIATIONS AND BUDGET COMMITTEE Bill Mitchell, Chairman Jack Bonny, Vice-Chairman Dennis Adkins Joan Greenwood Richard Phillips Jari Askins* Terry Harrison Greg Piatt Chris Benge Jerry Hefner* Bob Plunk Debbie Blackburn* Joe Hutchison** Clay Pope Dan Boren** Terry Ingmire Larry Rice David Braddock* Tad Jones Paul Roan Kevin Calvey Ron Langmacher Curt Roggow John Carey M.C. Leist* John Smaligo Lance Cargill Al Lindley Glen Bud Smithson Bill Case Elmer Maddux Barbara Staggs Forrest Claunch Ray McCarter** Fred Stanley Carolyn Coleman Roy McClain Joe Sweeden James Covey Doug Miller Sue Tibbs Odilia Dank Ray Miller Opio Toure** Frank Davis Fred Morgan Dale Turner** Abe Deutschendorf Bill Nations** Purcy Walker** Joe Eddins* Jim Newport Dale Wells Stuart Ericson Mike O’Neal Jim Wilson Randall Erwin* Bill Paulk Mike Wilt Larry Ferguson Fred Perry Susan Winchester Darrell Gilbert** Ron Peterson Robert Worthen Bill Graves Wayne Pettigrew Ray Young * Denotes a Subcommittee Chairman ** Denotes a Subcommittee Vice-Chairman GENERAL CONFERENCE COMMITTEE ON APPROPRIATIONS SUBCOMMITTEE APPOINTEES Bill Mitchell, -

OKLAHOMA STATE BAR JOURNAL Vol

OKLAHOMA STATE BAR JOURNAL Vol. 1 APRIL 1930 No. 1 Published Monthly by The State Bar of Oklahoma A Message to the Members of the State Bar: It has been evident for many years that the lawyers of the State of Oklahoma, were in need of some organization publication, but for many reasons, and the small member- ship in the Oklahoma State Bar Association, all the law- yers of the State could not be reached; but since the advent, of the State Bar of Oklahoma, it is now possible to have a publication, though small to start with, that will reach all the lawyers in the state; by means of this publication, we hope that we will be able to keep the Bar acquainted with just what is being done by the State Bar and your Board of Governors; and we wish to invite all constructive criti- cisms and suggestions; we want you all to help us make this an efficient publication. The Editors. STATE BAR JOURNAL Some of them possibly are criminals themselves who have entered the profession to enhance their opportunities to successfully pursue their criminal instincts. Oklahoma State Bar Journal It is from this latter class that an insidious propaganda is being spawned and circulated for the purpose of undermining the efficient and effective working of Printed monthly for The State Bar of Oklahoma by The Alva Review-Courier Publishing Com- pany, Alva, Oklahoma. Application for entrance as Second Class Mail Matter filed the machinery set up under this Act to assist in benefiting the best interests of April 19, 1930 under the Act of August 24, 1912. -

Oklahoma Legislature

L 1400.5 W628 2005-2006 c.3 Who's Who 50th Oklahoma Legislature * * * * + + Oklahoma Department of Libraries WHO IS WHO 2005 and 2006 Legislative Sessions 50th Oklahoma Legislature February 2006 TABLE OF CONTENTS Oklahoma Elected Officials 1 Governor. 2 Lieutenant Governor 4 Cabinet Members 5 About the Oklahoma Legislature 6 Legislative Service Bureau 7 Senate Senate Leadership 7 President Pro Tempore 8 Senators by District 8 Senate Members 9 Senate Committees 29 Senate Contact Reference List 31 House Speaker of the House 32 House Leadership 33 State Representatives by District 34 House Members 35 House Contact Reference List 71 House Committees 74 This publication printed and issued by the Oklahoma Department of Libraries as authorized by 65 O.S. 1991, section 3- 110. Seventy-five (75) copies have been prepared at a cost of $364.09. Twenty-five (25) copies have been deposited with the Publications Clearinghouse of the Oklahoma Department of Libraries. 2/2006 Oklahoma Elected Officials Governor Brad Henry Insurance Commissioner State Capitol, Room 212 Kim Holland* Oklahoma City 73105 2401 NW 23rd, Suite 28 405/521-2342 FAX 405/521-3353 Oklahoma City 73107 Tulsa: State Office Building PO Box 53408 73152-3408 440 S. Houston, Suite 304, Tulsa 74127 405/521-2828 FAX 405/521-6652 918/581-2801 FAX 918/581-2835 800/522-0071 www.gov.ok.gov www.oid.state.ok. us Lieutenant Governor Commissioner of Labor Mary Fallin Brenda Reneau State Capitol, Room 211 4001 Lincoln Blvd. Oklahoma City 73105 Oklahoma City 73105 405/521-2161 FAX 405/525-2702 405/528-1500 FAX 405/528-5751 www. -

(BJA) Drug Court Clearinghouse Justice Programs Office, School of Public Affairs American University

Bureau of Justice Assistance (BJA) Drug Court Clearinghouse Justice Programs Office, School of Public Affairs American University Excerpts from Selected Opinions of Federal, State and Tribal Courts Relevant to Drug court Programs June 2015 DECISION SUMMARIES BY ISSUE AND JURISDICTION VOLUME ONE: DECISION SUMMARIES BY ISSUE [Preliminary/Partial Update] Compiled by: Caroline S. Cooper, Director BJA Drug Court Clearinghouse and Technical Assistance Project This report was prepared by the Bureau of Justice Assistance (BJA) Drug Court Clearinghouse and Technical Assistance Project at American University, Washington D.C. These projects are supported by Grant Nos. 95-DC- MX-KOO2, 98-NU-VX-K018, 2002-DC-BX-K013, 2005-DC-BX-K047, 2007-DC-BX K003, 2009-DC-BX-K0022, and 2012-DC-BX-K005 awarded initially by the Drug courts Program Office and, subsequently, by the Bureau of Justice Assistance, Office of Justice Programs, U.S. Department of Justice. The Bureau of Justice Assistance is a component of the Office of Justice Programs, which also includes the Bureau of Justice Statistics, the National Institute of Justice, the Office of Juvenile Justice and Delinquency Prevention, and the Office for Victims of Crime. Points of view or opinions in this document are those of the author and do not represent the official position or policies of the U.S. Department of Justice. _____________________________________________________________________________________________ Excerpts from Selected Opinions of Federal, State and Tribal Courts Relevant to Drug Court Programs: Decision Summaries. Volume One: Decision Summaries By Issue. BJA Drug Court Clearinghouse. American University. June 2015. [Preliminary/Partial Update] FOREWORD This Compilation of selected federal, state and tribal court decisions relating to drug courts has been prepared and updated annually by the Bureau of Justice Assistance (BJA) Drug Court Clearinghouse and Technical Assistance Project at American University to highlight legal issues which are being raised relating to drug court programs. -

Journal Header of Some Sort

House Journal -- Committees 1 STANDING COMMITTEES of the HOUSE OF REPRESENTATIVES Second Session Fiftieth Legislature Aerospace and Technology Chris Hastings, Chair Jabar Shumate, Vice-Chair Bill Case Ryan McMullen Abe Deutschendorf Paul Wesselhoft Mike Jackson Agriculture and Rural Development Dale DeWitt, Chair Phil Richardson, Vice-Chair Don Armes Ryan McMullen Lisa Billy Jerry McPeak James Covey Curt Roggow Jeff Hickman Wade Rousselot Terry Hyman Joe Sweeden Rob Johnson 2 House Journal -- Committees Appropriations and Budget Chris Benge, Chair Jim Newport, Vice-Chair Thad Balkman Bill Nations Debbie Blackburn Ron Peters David Braddock Curt Roggow John Carey John Smaligo Lance Cargill Daniel Sullivan Joe Eddins Opio Toure Tad Jones John Trebilcock Mark Liotta Purcy Walker Ray McCarter Subcommittee on Education Tad Jones, Chair Sally Kern, Vice-Chair Neil Brannon Ray McCarter Odilia Dank Bill Nations Lee Denney Pam Peterson Abe Deutschendorf Jabar Shumate Terry Ingmire Subcommittee on General Government and Transportation Mark Liotta, Chair Shane Jett, Vice-Chair Brian Bingman Bob Plunk Joe Dorman Wade Rousselot Guy Liebmann Subcommittee on Health and Social Services Thad Balkman, Chair Marian Cooksey, Vice-Chair Mike Brown Jerry Ellis Doug Cox Sue Tibbs Joe Eddins House Journal -- Committees 3 Subcommittee on Human Services Ron Peters, Chair Lisa Billy, Vice-Chair John Carey Mike Jackson Rebecca Hamilton Kris Steele Wes Hilliard Subcommittee on Natural Resources and Regulatory Services Curt Roggow, Chair Rex Duncan, Vice-Chair Dennis -

Journal Header of Some Sort

1 HOUSE JOURNAL First Regular Session of the Forty-eighth Legislature of the State of Oklahoma First Legislative Day, Tuesday, January 2, 2001 Pursuant to Article V, Section 26, of the Constitution of the State of Oklahoma, the First Regular Session of the House of Representatives for the Forty-eighth Legislature assembled in the House Chamber at 12:00 noon. Representative Glover called the House to order. Prayer was offered by Reverend James White, Stilwell Pentecostal Holiness Church, Stilwell. CERTIFICATION OF HOUSE MEMBERS Representative Hilliard moved that the Communication dated November 20, 2000, to the Speaker of the House of Representatives and furnished to the Chief Clerk of the House of Representatives by the Secretary of the State Election Board listing the persons elected to the House of Representatives for the Forty-eighth Legislature be accepted as prima facie evidence of membership in the House of Representatives and that said Members be seated in the House Chamber and the above-named Communication be printed in the House Journal, which motion was declared adopted. COMMUNICATION November 20, 2000 The Honorable Loyd Benson Speaker, Oklahoma State House of Representatives State Capitol Oklahoma City, Oklahoma 73105 Sir: 2 House Journal Upon the face of the returns of the General Election, November 7, 2000, certified to this office by the several County Election Boards of the State, the candidates named in the list attached appear to have been regularly elected as Members of the Oklahoma State House of Representatives for the districts indicated. Certificates of Election have been issued to them by this Board, entitling each to participate in the preliminary organization of the House of Representatives. -

LEGISLATIVE UPDATE 49Th Oklahoma Legislature Second Session – 2004

LEGISLATIVE UPDATE 49th Oklahoma Legislature Second Session – 2004 OKLAHOMA STATE REGENTS FOR HIGHER EDUCATION From: Carolyn McCoy & Lesa Jolly-Borin Friday, February 6, 2004 Welcome to the OSRHE Legislative Update Highlights this Week: College Connection’ Radio Program Debuts Saturday From State Regents Oklahomans are encouraged to tune in Saturday to a new radio program, “College Connection,” to find out the latest news on state and national higher education issues, as well as to hear a variety of guests provide valuable information on preparing for college. “College Connection,” sponsored by the Oklahoma State Regents for Higher Education, will air each Saturday beginning Feb. 7 on KFAQ 1170 AM in Tulsa from 6 a.m. to 7 a.m. and on KOMA- News/Talk 1520 AM in Oklahoma City from 6 p.m. to 7 p.m. “The State Regents look forward to the opportunity to provide information on a weekly basis that will help Oklahomans prepare for college both academically and financially,” said Chancellor Paul G. Risser. “‘College Connection’ provides families with another resource for college information while highlighting significant state and local higher education issues and featuring input from edu- cational and policy leaders.” In addition to news highlights from Oklahoma campuses and a recap of President George W. Bush’s State of the Union statement regarding community colleges, the debut program will also feature a discussion with Risser on the priorities and future of higher education in Oklahoma, as well as special guests sharing information on College Goal Sunday, a statewide event designed to provide financial aid and preparing for college information to students and their families. -

Judicial Branch

CHAPTER 5 JUDICIAL BRANCH Mother and Daughter Claire Custard and Glessie May Custard pose for a photograph in St. Louis in 1912. (photo cour- tesy of Donald E. Custard) 166 OFFICIAL MANUAL cuits. A presiding judge, elected by the other judges in the circuit, has general administrative authority over all judicial personnel in the circuit. He or she may assign other judges throughout the circuit to relieve caseload and administrative backlogs. The Supreme Court and court of appeals have general superintend- ing control over all courts and tribunals within their jurisdictions. Original remedial writs may be issued and determined at each Missouri’s Judicial level of the court system. Decisions of the Supreme Court are controlling in all other state courts. System Selection of Judges In the fi rst 30 years of Missouri’s statehood, the judges of the supreme, circuit and chancery courts were appointed by the From its inception in 1820, Missouri state government con- governor with the advice and consent of the Senate. After much stitutionally has been divided into three separate branches—leg- public discussion, the constitution was amended in 1850 to pro- islative, executive and judicial. The judicial branch’s function vide for the popular election of judges, and this system remains in is not to make the laws of the state or to administer them but effect for most Missouri courts today. In most circuits, the judges to adjudicate the controversies that arise between persons and are elected by the voters in partisan elections. parties, to determine fairly and justly the guilt or innocence of In 1940, Missouri voters amended the constitution by adopt- persons charged with criminal offenses and to interpret the laws ing the “Nonpartisan Selection of Judges Court Plan,” which was of the state as enacted by the legislature and carried out by the placed on the ballot by initiative petition and which provides for executive branch. -

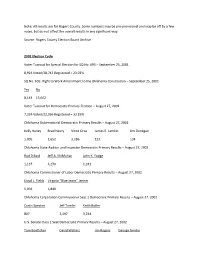

Results Are for Rogers County. Some Numbers May Be Pre-Provisional and May Be Off by a Few Votes, but Do Not Affect the Overall Results in Any Significant Way

Note: All results are for Rogers County. Some numbers may be pre-provisional and may be off by a few votes, but do not affect the overall results in any significant way. Source: Rogers County Election Board Archive 2002 Election Cycle Voter Turnout for Special Election for SQ No. 695 – September 25, 2001 8,924 Voted/38,742 Registered = 23.03% SQ No. 695: Right to Work Amendment to the Oklahoma Constitution – September 25, 2001 Yes No 8,143 13,662 Voter Turnout for Democratic Primary Election – August 27, 2002 7,324 Voted/22,066 Registered = 33.19% Oklahoma Gubernatorial Democratic Primary Results – August 27, 2002 Kelly Haney Brad Henry Vince Orza James E. Lamkin Jim Dunegan 1,005 2,652 3,286 122 134 Oklahoma State Auditor and Inspector Democratic Primary Results – August 27, 2002 Rod Dillard Jeff A. McMahan John K. Fodge 1,137 4,270 1,241 Oklahoma Commissioner of Labor Democratic Primary Results – August 27, 2002 Lloyd L. Fields Virginia “Blue Jeans” Jenner 5,094 1,840 Oklahoma Corporation Commissioner Seat 1 Democratic Primary Results – August 27, 2002 Curtis Speaker Jeff Tomlin Keith Butler 807 2,497 3,244 U.S. Senate Class 2 Seat Democratic Primary Results – August 27, 2002 Tom Boettcher David Walters Jim Rogers George Gentry 2,859 3,198 700 390 U.S. House of Representative District 2 Democratic Primary Results – August 27, 2002 Mike Mass Brad Carson Dorothy Vandiver 913 4,999 259 Rogers County Commissioner District 3 Democratic Primary Results – August 27, 2002 Frank A. Nichol Dick Bright Harvey Diem Randy Lee Baldridge Gavin O.