Valustrat Qatar Real Estate Research Q1 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Build Your Own Plan! MME Urges Public to Cut Food Waste

European Al Duhail Central Bank eye strong stimulus on track show at FIFA as economy Club World struggles Cup Business | 13 Sport | 16 FRIDAY 22 JANUARY 2021 9 JUMADA II - 1442 VOLUME 25 NUMBER 8510 www.thepeninsula.qa 2 RIYALS Build your own plan! Terms & Conditions Apply Saudi FM: Embassy in MME urges public to cut food waste Qatar to reopen ‘in days’ SANAULLAH ATTAULLAH MME official says large quantities of food wastes have been Marri said: “A total of 37 projects THE PENINSULA REUTERS — DUBAI observed at municipal waste management and collection were planned under the strategy. Many of them were Saudi Arabia’s The Ministry of Municipality points. launched in 2019 and 2020. The Foreign Minister H H and Environment (MME) has remaining will be implemented Prince Faisal bin raised concerns about wastage The Ministry is implementing a programme aimed at reducing in coming years.” Farhan (pictured) has of food items by people. A food waste from the entire supply chain. He said 10 projects of green- said that Saudi senior official of the Ministry houses with the capacity of Arabia’s embassy in has urged consumers to change Qatar is 106% self-sufficient in fresh milk, 127% in fresh 21,000 tonnes of vegetables in Qatar will reopen “in their behaviour to food habits chicken, and 35% each in eggs and vegetables. a year and 10 projects for fat- days”, Al Arabiya TV to reduce food wastage. tening of animals with the channel said Qatar has taken many steps MME has provided 1,600 greenhouses and 1,700 net-houses to capacity of 50,000 animals in yesterday. -

Name Cuisine Address Timings Phone Number Category

NAME CUISINE ADDRESS TIMINGS PHONE NUMBER CATEGORY AKBAR RESTAURANT (SWISS- 16th Floor, Swiss-Belhotel, JaBr Bin 5 PM to 12 Midnight (Mon, BELHOTEL) INDIAN,MUGHLAI Mohamed Street, Al Salata, Doha Tue, Wed, Thu, Sat, Sun)... 44774248 Medium ANJAPPAR CHETTINAD 11 a.m .till 11:30 p.m.(Mon- RESTAURANT INDIAN Building 16, Barwa Village, Doha Sun) 44872266 Medium Beside Al Mushri Company, Near ANJAPPAR CHETTINAD Jaidah Flyover, Al Khaleej Street, 11:30 a.m .till 11:30 p.m.(Mon- RESTAURANT INDIAN MusheireB, Doha Sun) 44279833 Medium 12 Noon to 11 PM (Mon- Food Court, Villaggio, Al WaaB, Doha & Wed),12 Noon to 11:30 PM 44517867/44529028 ASHA'S INDIAN AL Gharafa (Thu... 44529029 Medium Beside MoBile 1 Center, Old Airport 6 AM to 11:30 PM (Mon, Tue, ASIANA INDIAN Road, Al Hilal, Doha Wed, Thu, Sat, Sun), 12... 44626600 Medium Near Jaidah Flyover, Al Khaleej Street, 7 AM to 3 PM, 6 PM to 11 PM BHARATH VASANTA BHAVAN SOUTH INDIAN/NORTH INDIAN Fereej Bin Mahmoud, Doha (Mon-Sun) 44439955 Budget Opposite Nissan Service Center, Pearl RoundaBout, Al Wakrah Main Street, Al 11:30 AM to 11:30 PM (Mon, BIRYANI HUT INDIAN Wakrah, Doha Tue, Wed, Sat, Sun)... 44641401/33668172 Budget BOLLYWOOED LOUNGE & Mezzanine, Plaza Inn Doha, Al Meena Closed (Mon),12 Noon to 3 RESTAURANT (PLAZA INN) INDIAN Street, Al Souq, Doha PM, 7 PM to 11 PM (Tue-Sun) 44221111/44221116 Medium Ground Floor, Radisson Blu Hotel, BOMBAY BALTI (RADISSON BLU) INDIAN Salwa Road, Al Muntazah, Doha 6 PM to 11 PM (Mon-Sun) 44281555 High-End Opposite The Open Theatre, Katara Closed (Mon, Tue, Wed, Sun), BOMBAY CHAAT INDIAN STREET FOOD Cultural Village, Katara, Doha 4 PM to 11 PM (Thu-Sat) 44080808 Budget Beside Family Food Center, Old Airport BOMBAY CHOWPATTY-I INDIAN STREET FOOD Road, Old Airport Area, Doha 24 Hours (Mon-Sun) 44622100 Budget Near Al Meera, Aasim Bin Omar Street, 5 AM to 12:30 AM (Mon, Tue, BOMBAY CHOWPATTY-II INDIAN STREET FOOD Al Mansoura, Doha Wed, Thu, Sat, Sun), 7.. -

1 Population 2019 السكان

!_ اﻻحصاءات السكانية واﻻجتماعية FIRST SECTION POPULATION AND SOCIAL STATISTICS !+ الســكان CHAPTER I POPULATION السكان POPULATION يعتﺮ حجم السكان وتوزيعاته املختلفة وال يعكسها Population size and its distribution as reflected by age and sex structures and geographical الﺮكيب النوي والعمري والتوزيع الجغراي من أهم البيانات distribution, are essential data for the setting up of اﻻحصائية ال يعتمد علا ي التخطيط للتنمية .socio - economic development plans اﻻقتصادية واﻻجتماعية . يحتوى هذا الفصل عى بيانات تتعلق بحجم وتوزيع السكان This Chapter contains data related to size and distribution of population by age groups, sex as well حسب ا ل ن وع وفئات العمر بكل بلدية وكذلك الكثافة as population density per zone and municipality as السكانية لكل بلدية ومنطقة كما عكسا نتائج التعداد ,given by The Simplified Census of Population Housing & Establishments, April 2015. املبسط للسكان واملساكن واملنشآت، أبريل ٢٠١٥ The source of information presented in this chapter مصدر بيانات هذا الفصل التعداد املبسط للسكان is The Simplified Population, Housing & واملساكن واملنشآت، أبريل ٢٠١٥ مقارنة مع بيانات تعداد Establishments Census, April 2015 in comparison ٢٠١٠ with population census 2010 تقدير عدد السكان حسب النوع في منتصف اﻷعوام ١٩٨٦ - ٢٠١٩ POPULATION ESTIMATES BY GENDER AS OF Mid-Year (1986 - 2019) جدول رقم (٥) (TABLE (5 النوع Gender ذكور إناث المجموع Total Females Males السنوات Years ١٩٨٦* 247,852 121,227 369,079 *1986 ١٩٨٦ 250,328 123,067 373,395 1986 ١٩٨٧ 256,844 127,006 383,850 1987 ١٩٨٨ 263,958 131,251 395,209 1988 ١٩٨٩ 271,685 135,886 407,571 1989 ١٩٩٠ 279,800 -

Mbs Has to Be Dealt with for Khashoggi Murder: US Senator

BUSINESS | Page 1 SPORT | Page 8 Imam, Hafeez steer Pakistan to Synergistic opportunities victory over prevail between Qatar and South Africa Canada, says Doha Bank CEO published in QATAR since 1978 SUNDAY Vol. XXXIX No. 11069 January 20, 2019 Jumada I 14, 1440 AH GULF TIMES www. gulf-times.com 2 Riyals Warm welcome for rally champion In brief More Al Furjan stores QATAR | Offi cial scheduled to open soon Amir to attend Arab summit in Beirut today QNA The motivation behind this project His Highness the Amir Sheikh Tamim Doha is the estimated increase in popula- bin Hamad al-Thani will attend tion within the city of Doha and its the Arab Economic and Social surroundings. The retail mix has been Development Summit to be held he Qatar Development Bank devised to cater to the most important today in Beirut at the invitation of (QDB) announced yesterday that needs. Lebanese President General Michel Tthe construction of the second QDB will not raise rental rates for Aoun. An off icial delegation is batch of outlets for Al Furjan Markets 2 commercial outlets included in Phase accompanying the Amir. project has begun. 2 of its Al Furjan Markets project, al- The new markets will be located in Khalifa had said earlier. QATAR | Diplomacy areas such as Ain Khalid, Luaib, Bani He said the existing rents at Al Furjan Hajer, Al Aziziya, Al Gharafa, Muaither, Markets across the country are pegged Amir and Mali president Al Shamal and Al Wakrah. at QR6,000 per month. hold phone conversation The fi rst batch of Al Furjan Markets His Highness the Amir Sheikh Tamim was located in Umm Al Qarn and Al The markets will provide all bin Hamad al-Thani yesterday held Khor among other areas. -

Qatar Real Estate Q1, 2020

Qatar Real Estate Q1, 2020 www.alasmakhrealestate.com Indicators Q1 2020 Micro Economics – Current Standings Steady increase in population partially supports the deMand for housing. Delay in delivery of under Total Population* GDP at Current Price* construction projects is expected due to outbreak of pandeMic in the region. 2,795,484 QAR 163.45 Billion Office supply in new CBD areas mounts pressure on * Mar 2020 * Q2 2019 price correction in old town business districts. Operation of Doha Metro in the vicinity of priMe Malls Industrial adds on to increased footfall. Producer Price Index* Production Index* GovernMent supports hospitality sector by 61.4 points 109.6 points converting hotels to quarantine centers. Ref: QSA * Sep 2019 * Aug 2019 Overall land rates are stabilizing across Qatar. No of Properties Sold Municipalities 923 Value of Properties Sold Al Shamal QAR 6.06 Billion Al Khor Ref: MDPS For the period December 2019. January 2020 and February 2020 Al Daayen Real Estate Price Index (QoQ) Umm Slal Doha 300 8.0% Al Rayyan 250 6.0% 4.0% 200 2.0% 150 0.0% -2.0% Al Wakra 100 -4.0% 50 -6.0% 0 -8.0% Jul-17 Jul-18 Jul-19 Jan-17 Jan-18 Jan-19 Sep-17 Sep-18 Sep-19 Mar-17 Nov-17 Mar-18 Nov-18 Mar-19 Nov-19 May-17 May-18 May-19 Ref: QCB 2 Residential Q1 2020 YTD Snapshot Supply in Pipeline Expected Delivery Overall Available Units 360,000 90,000 units 2020 Q1 2020 Villa Occupancy 72%* Median Selling Price Median Rental Rate ApartMent Occupancy QAR 10,500 PSF QAR 6,500 (2BR) 60%* Ref: AREDC Research Current Annual Yield Key DeMand Drivers 4.9%* * Average 25% 13% GovernMent Companies Residential Concentration GovernMent and coMpanies are taking residential units for their employees under HRA. -

Work on Qatar's 1St Cable-Stayed Bridge Begins

BUSINESS | Page 1 SPORT | Page 1 Nantes keep PSG waiting Qatar streamlining investment, business for title initiatives: MoCI published in QATAR since 1978 THURSDAY Vol. XXXX No. 11157 April 18, 2019 Sha’baan 13, 1440 AH GULF TIMES www. gulf-times.com 2 Riyals In brief Jordan king meets defence minister QATAR | Offi cial Amir condoles with Work on Qatar’s president of Congo His Highness the Amir Sheikh Tamim bin Hamad al-Thani and His Highness 1st cable-stayed the Deputy Amir Sheikh Abdullah bin Hamad al-Thani sent yesterday cables of condolences to the President of the Democratic Republic of Congo, Felix Tshisekedi, on the victims of the bridge begins sunken ship, wishing the injured a speedy recovery. O Bridge to be ready in the first quarter of 2021 ARAB WORLD | Unrest he Public Works Authority Bashir moved to prison (Ashghal) has started the con- Tstruction of Qatar’s fi rst cable- as protesters rally Jordan’s King Abdullah II, Supreme Commander of the Jordanian Armed Forces, met with HE the Deputy Prime Minister and stayed bridge and the conversion of Sudan’s military rulers have Minister of State for Defence Aff airs Dr Khalid bin Mohamed al-Attiyah at the Al Husseiniya Palace in Amman yesterday. HE al- Haloul Roundabout into a two-level transferred ousted president Omar al- Attiyah, who is on an off icial visit to Jordan, conveyed the greetings of His Highness the Amir Sheikh Tamim bin Hamad al-Thani interchange as part of Sabah Al Ahmad Bashir to prison, a family source said to King Abdullah II. -

Madinat Khalifa and Ghar Tri Logistics Buses For

Tri Logistics Buses for Compass International School of Doha C1 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops 5:30AM 5:36AM 6:05AM C1 House 6:15AM 6:30AM 6:43AM C2 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops 5:50AM 2:40AM 6:10AM 6:15AM 6:33AM C2 House 6:35AM 6:37AM 6:40AM 6:42AM 6:55AM C3 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops No Pick-up 5:50AM C3 House No Pick-up 5:59AM 6:03AM 6:08AM C3 House 6:15AM 6:19AM 6:40AM C4 - Madinat Khalifa Campus Pick-up AM Pick-up Time AM Bus Stops 5:10AM 5:18AM 5:28AM 5:34AM 5:36AM 5:33AM C4 House 5:38AM 6:58AM 6:18AM 6:23AM C5 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops 5:31AM 5:35AM 5:53AM 6:08AM 6:13PM C5 House 6:18AM 6:28AM 6:38AM 6:45AM 6:58AM Rayyan Campus Pick-up AM Pick-up Time AM Bus Stops 5:40AM 6:10AM 6:30AM 6:30AM 6:32AM C6 House 6:40AM 6:50AM 6:55AM C7 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops 6:00AM Club- C7 6:20AM 6:24AM 6:27AM House 6:32AM 6:40AM C8 - Rayyan Campus Pick-up AM Pick-up Time AM Bus Stops 5:43AM 5:55AM C8 House 5:57AM 6:20AM 6:25AM 6:28AM 6:33AM No Pick-up C9 - Rayyan Campus Pick-up AM Pick-up Time AM Bus Stops 5:43AM 5:56AM C9 House 6:12AM C9 House 6:15AM 6:22AM C10 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops 6:15AM House 6:30AM C10 Club- 6:45AM house Tri Logistics Buses for Compass International School of Doha C1 - Madinat Khalifa and Gharaffa Campus Drop-off PM Address Time PM Bus Jaffar Bin Abi Talib St. -

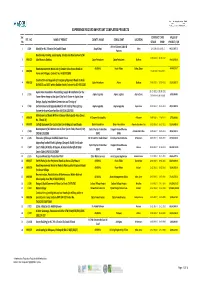

Experience Record Important Completed Projects

EXPERIENCE RECORD IMPORTANT COMPLETED PROJECTS Ser. CONTRACT DATE VALUE OF REF . NO . NAME OF PROJECT CLIENT'S NAME CONSULTANT LOCATION No STRART FINISH PROJECT / QR Artline & James Cubitt & 1 J/149 Masjid for H.E. Ghanim Bin Saad Al Saad Awqaf Dept. Dafna 12‐10‐2011/31‐10‐2012 68,527,487.70 Partners Road works, Parking, Landscaping, Shades and Development of Al‐ 22‐08‐2010 / 21‐06‐2012 2 MRJ/622 Jabel Area in Dukhan. Qatar Petroleum Qatar Petroleum Dukhan 14,428,932.00 Road Improvement Works out of Greater Doha Access Roads to ASHGHAL Road Affairs Doha, Qatar 48,045,328.17 3 MRJ/082 15‐06‐2010 / 13‐06‐2012 Farms and Villages, Contract No. IA 09/10 C89G Construction and Upgrade of Emergency/Approach Roads to Arab 4 MRJ/619 Qatar Petroleum Atkins Dukhan 27‐06‐2010 / 10‐07‐2012 23,583,833.70 D,FNGLCS and JDGS within Dukhan Fields,Contract No.GC‐09112200 Aspire Zone Foundation Dismantling, Supply & Installation for the 01‐01‐2011 / 30‐06‐2011 5 J / 151 Aspire Logistics Aspire Logistics Aspire Zone 6,550,000.00 Tower Flame Image at the Sport City Torch Tower in Aspire Zone Extension to be issued Design, Supply, Installation.Commission and Testing of 6 J / 155 Enchancement and Upgrade Work for the Field of Play Lighting Aspire Logestics Aspire Logestics Aspire Zone 01‐07‐2011 / 25‐11‐2011 28,832,000.00 System for Aspire Zone Facilities (AF/C/AL 1267/10) Maintenance of Roads Within Al Daayen Municipality Area (Zones 7 MRJ/078 Al Daayen Municipality Al Daayen 19‐08‐2009 / 11‐04‐2011 3,799,000.00 No. -

Qatar Provider Network Call Center No. +974 4040 2000

QATAR PROVIDER NETWORK CALL CENTER NO. +974 4040 2000 Elite Network members have access to: All Elite, Premium & Prime Network Premium Network members have access to: All Premium & Prime Network (no access to Elite Network Providers) Prime Network members have access to: All Prime Network (no access to Elite & Premium Network Providers) NETWORK SPECIALTY ADDRESS TELEPHONE المركز الصحي العنوان التخصص المستشفيات HOSPITALS Elite Al Ahli Hospital Multispeciality Bin Omran St. Opp. Town Centre, near TV Roundabout 4489 8888 المستشفى اﻻهلي بن عمران, مقابل مركز المدينه قرب دوار التلفزيون تخصصات متعددة Premium Al Emadi Hospital Multispeciality Hilal West Area, Near The Mall R/A, along D-Ring Road 4466 6009 مستشفى العمادي المنطقه الغربيه, قرب دوار المول, الدائري الرابع, الهﻻل تخصصات متعددة Prime American Hospital Clinics Multispeciality C-Ring Road, Near Andaloos Petrol Station, Muntazah 4442 1999 المستشفى اﻻمريكي الدائري الثالث, المنتزه قرب محطة بترول المنتزه تخصصات متعددة Prime Doha Clinic Hospital Multispeciality New Mirqab Street, Fareej Al Nasr Area 4438 4390 مستشفى عيادات الدوحة شارع المرقاب الجديد / فريج النصر تخصصات متعددة Premium Dr Moopen's Aster Hospital Multispeciality Behind Family Food Center, Matar Qadeem, D-Ring Road 4031 1900 مركز استر الطبي - دكتور موبين الدائري الرابع , المطار القديم , خلف مركز التموين العائلي تخصصات متعددة انف واذن وحنجرةِ طب طب العيون Premium Magrabi Eye & Ear Centre E.N.T & Opthalmology & dental Old Airport near Al Safeer Hypermarket 4423 8888 مركز مغربي للعيون واﻻنف المطار القديم , قرب سفاري هايبرماركت واﻻسنان -

Access to Quality Education for Displaced Children Stressed

BUSINESS | 23 SPORT | 29 Nebras records Disgraced Smith, huge jump in 2017 Warner out for 12 revenue months Thursday 29 March 2018 | 12 Rajab I 1439 www.thepeninsula.qa Volume 23 | Number 7480 | 2 Riyals Freedom to roam with Bill Protection! Terms & conditions apply Access to quality education for Emir holds talks with Rosneft Chief Executive Officer displaced children stressed THE PENINSULA H H Sheikha Moza Grandi. The discussion touched bint Nasser, while on the ways to ensure education GENEVA: H H Sheikha Moza speaking during for refugees and internally dis- bint Nasser, Chairperson of placed persons, in order to build Qatar Foundation (QF) and a high-level panel a prosperous future for all. Education Above All Foundation discussion at the During the discussion, H H (EAA), has urged the global UN headquarters in Sheikha Moza spoke about the community to facilitate access Geneva, urged the obstacles facing the education of to quality education for refugee and displaced children, displaced children and to global community to which prevents them from con- enforce severe penalties for facilitate access to tributing to the building of their perpetrators of armed conflict. quality education for communities. Her Highness H H Sheikha Moza bint added that education must be Nasser, Advocate for the UN displaced children given priority as it is the tool for Sustainable Development and to enforce the children of the present and Goals, participated yesterday future. A global approach needs severe penalties for Emir H H Sheikh Tamim bin Hamad Al Thani met yesterday at Al Bahr Palace office with Igor Sechin, in a high-level panel discussion to be adapted, in order to remove perpetrators of Chief Executive Officer of Rosneft, and the delegation accompanying him on the occasion of his visit organised by the EAA in coop- institutional barriers which eration with the United Nations armed conflict. -

1 Population \307\341\323\337\307\344.Xls

!_ اءات ا وا FIRST SECTION POPULATION AND SOCIAL STATISTICS !+ اــ ن CHAPTER I POPULATION ان POPULATION ان وز ا وا Population size and its distribution as reflected by ا آ%$ ا#" وا ي وا ز اا ا ا age and sex structures and geographical distribution, together with the characteristics ا012 ا / .- ا %% وا,وا+% *( أه related to educational and marital status are ا%8ت ا126% ا 5 "% ا essential date for the setting up of economic and %# 3%4 ا6: 2د واsocial development plans. %" +6 - ى ه=ا ا2> " .%8ت ; .- وز This Chapter contains data related to size and ان $ ا#ع وAت ا .> .5 وآ=@ ا? distribution of population by age qroups, sex as well as popuation density per zone and ا8% > .5 و*#4/ آ " C1 8 ا 5اد ,municipality as given by Census Population ا م ن واآ( وا#HIت، أ. > ٢٠١٠ .Housing & Establishments, April 2010 - ى ا2> أ Lً " .%8ت "( ا- ا %% The Chapter also covers data related to وا,وا+% وز ت ا/ة اI ا#4I وا% education status, marital status and distribution of manpower into economically active and . 4I8 ا: 2د ً .inactive persons و*52ر .%8ت ه=ا ا2> ا 5اد ا م ن واآ( The source of infomation presented in this أ. > ٢٠١٠ */ر8 * .%8ت 5اد ١٩٨٦ و ١٩٩٧ & chapter is the Population, Housing Establishments Census April 2010 in comparison . و ٢٠٠٤ .with population census 1986,1997, 2004 )'&% $د ا "ن 0/ . -,+ ا*$ ام ١٩٨٦ - ٢٠١٣ POPULATION ESTIMATE AS OF MIDDLE 1986 - 2013 ول ر (٥) (TABLE (5 ا ع Gender ذآ ر اث ا ع Total F M ا ات Years ١٩٨٦* 247,852 121,227 369,079 *1986 ١٩٨٦ 250,328 123,067 373,395 1986 ١٩٨٧ 256,844 127,006 383,850 1987 ١٩٨٨ -

QIA Acquires Sizeable Stake in Oryx Midstream Services

BUSINESS | 13 SPORT | 19 QCB's foreign Serena, Osaka reserves top Forbes’ list of rise to best-paid female QR196.2bn athletes Thursday 8 August 2019 | 7 Dhul-Hijja 1440 www.thepeninsula.qa Volume 24 | Number 7977 | 2 Riyals QIA acquires sizeable stake in Oryx Midstream Services QNA The total QIA to lead Oryx in partnership with TEXAS these world-class investors.” investment in Oryx The Co-founder and CEO of Qatar Investment Authority will be approximately Stonepeak, Michael Dorrell, for (QIA) announced yesterday that $550m. QIA has his part said: “We are delighted it acquired a significant stake in committed to invest to have QIA investing alongside Oryx Midstream Services (Oryx), Stonepeak in supporting Oryxs the largest privately-held in the development continued development. We midstream crude operator in the of Oryx alongside believe Oryx is a uniquely posi- Permian Basin from an affiliate Stonepeak. tioned strategic platform and a of Stonepeak Infrastructure core North American infra- Minister of Justice and Acting Minister of State for Cabinet Affairs H E Dr Issa bin Saad Al Jafali Al Nuaimi Partners (Stonepeak). structure asset. Stonepeak and in Singapore. The total QIA investment in provides consistent, reliable Oryx remain focused on pro- Oryx will be approximately service for its customers. viding critical midstream $550m. QIA has committed to The CEO of QIA, Mansoor Al services to accommodate invest in the development of Mahmoud, said: “We believe that growing Permian production, Qatar joins Singapore Oryx alongside Stonepeak. Oryx represents a strong mid- and QIAs commitment to Oryx Since its founding in 2013, stream platform with tre- meaningfully furthers this goal.” Oryx has established itself as one mendous growth potential, and QIA is a leading Sovereign Convention on Mediation of the leading midstream oper- we look forward to working with Wealth Fund in the world that ators in the Permian Basin in the our new partners at Stonepeak.