Qatar Real Estate Q1, 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Name Cuisine Address Timings Phone Number Category

NAME CUISINE ADDRESS TIMINGS PHONE NUMBER CATEGORY AKBAR RESTAURANT (SWISS- 16th Floor, Swiss-Belhotel, JaBr Bin 5 PM to 12 Midnight (Mon, BELHOTEL) INDIAN,MUGHLAI Mohamed Street, Al Salata, Doha Tue, Wed, Thu, Sat, Sun)... 44774248 Medium ANJAPPAR CHETTINAD 11 a.m .till 11:30 p.m.(Mon- RESTAURANT INDIAN Building 16, Barwa Village, Doha Sun) 44872266 Medium Beside Al Mushri Company, Near ANJAPPAR CHETTINAD Jaidah Flyover, Al Khaleej Street, 11:30 a.m .till 11:30 p.m.(Mon- RESTAURANT INDIAN MusheireB, Doha Sun) 44279833 Medium 12 Noon to 11 PM (Mon- Food Court, Villaggio, Al WaaB, Doha & Wed),12 Noon to 11:30 PM 44517867/44529028 ASHA'S INDIAN AL Gharafa (Thu... 44529029 Medium Beside MoBile 1 Center, Old Airport 6 AM to 11:30 PM (Mon, Tue, ASIANA INDIAN Road, Al Hilal, Doha Wed, Thu, Sat, Sun), 12... 44626600 Medium Near Jaidah Flyover, Al Khaleej Street, 7 AM to 3 PM, 6 PM to 11 PM BHARATH VASANTA BHAVAN SOUTH INDIAN/NORTH INDIAN Fereej Bin Mahmoud, Doha (Mon-Sun) 44439955 Budget Opposite Nissan Service Center, Pearl RoundaBout, Al Wakrah Main Street, Al 11:30 AM to 11:30 PM (Mon, BIRYANI HUT INDIAN Wakrah, Doha Tue, Wed, Sat, Sun)... 44641401/33668172 Budget BOLLYWOOED LOUNGE & Mezzanine, Plaza Inn Doha, Al Meena Closed (Mon),12 Noon to 3 RESTAURANT (PLAZA INN) INDIAN Street, Al Souq, Doha PM, 7 PM to 11 PM (Tue-Sun) 44221111/44221116 Medium Ground Floor, Radisson Blu Hotel, BOMBAY BALTI (RADISSON BLU) INDIAN Salwa Road, Al Muntazah, Doha 6 PM to 11 PM (Mon-Sun) 44281555 High-End Opposite The Open Theatre, Katara Closed (Mon, Tue, Wed, Sun), BOMBAY CHAAT INDIAN STREET FOOD Cultural Village, Katara, Doha 4 PM to 11 PM (Thu-Sat) 44080808 Budget Beside Family Food Center, Old Airport BOMBAY CHOWPATTY-I INDIAN STREET FOOD Road, Old Airport Area, Doha 24 Hours (Mon-Sun) 44622100 Budget Near Al Meera, Aasim Bin Omar Street, 5 AM to 12:30 AM (Mon, Tue, BOMBAY CHOWPATTY-II INDIAN STREET FOOD Al Mansoura, Doha Wed, Thu, Sat, Sun), 7.. -

1 Population 2019 السكان

!_ اﻻحصاءات السكانية واﻻجتماعية FIRST SECTION POPULATION AND SOCIAL STATISTICS !+ الســكان CHAPTER I POPULATION السكان POPULATION يعتﺮ حجم السكان وتوزيعاته املختلفة وال يعكسها Population size and its distribution as reflected by age and sex structures and geographical الﺮكيب النوي والعمري والتوزيع الجغراي من أهم البيانات distribution, are essential data for the setting up of اﻻحصائية ال يعتمد علا ي التخطيط للتنمية .socio - economic development plans اﻻقتصادية واﻻجتماعية . يحتوى هذا الفصل عى بيانات تتعلق بحجم وتوزيع السكان This Chapter contains data related to size and distribution of population by age groups, sex as well حسب ا ل ن وع وفئات العمر بكل بلدية وكذلك الكثافة as population density per zone and municipality as السكانية لكل بلدية ومنطقة كما عكسا نتائج التعداد ,given by The Simplified Census of Population Housing & Establishments, April 2015. املبسط للسكان واملساكن واملنشآت، أبريل ٢٠١٥ The source of information presented in this chapter مصدر بيانات هذا الفصل التعداد املبسط للسكان is The Simplified Population, Housing & واملساكن واملنشآت، أبريل ٢٠١٥ مقارنة مع بيانات تعداد Establishments Census, April 2015 in comparison ٢٠١٠ with population census 2010 تقدير عدد السكان حسب النوع في منتصف اﻷعوام ١٩٨٦ - ٢٠١٩ POPULATION ESTIMATES BY GENDER AS OF Mid-Year (1986 - 2019) جدول رقم (٥) (TABLE (5 النوع Gender ذكور إناث المجموع Total Females Males السنوات Years ١٩٨٦* 247,852 121,227 369,079 *1986 ١٩٨٦ 250,328 123,067 373,395 1986 ١٩٨٧ 256,844 127,006 383,850 1987 ١٩٨٨ 263,958 131,251 395,209 1988 ١٩٨٩ 271,685 135,886 407,571 1989 ١٩٩٠ 279,800 -

Qatar 2022 Overall En

Qatar Population Capital city Official language Currency 2.8 million Doha Arabic Qatari riyal (English is widely used) Before the discovery of oil in Home of Al Jazeera and beIN 1940, Qatar’s economy focused Media Networks, Qatar Airways on fishing and pearl hunting and Aspire Academy Qatar has the third biggest Qatar Sports Investments owns natural gas reserves in the world Paris Saint-Germain Football Club delivery of a carbon-neutral tournament in 2022. Under the agreement, the Global Carbon Trust (GCT), part of GORD, will Qatar 2022 – Key Facts develop assessment standards to measure carbon reduction, work with organisations across Qatar and the region to implement carbon reduction projects, and issue carbon credits which offset emissions related to Qatar 2022. The FIFA World Cup Qatar 2022™ will kick off on 21 November 2022. Here are some key facts about the tournament. Should you require further information, visit qatar2022.qa or contact the Supreme Committee for Delivery & Legacy’s Tournament sites are designed, constructed and operated to limit environmental impacts – in line with the requirements Media Team, [email protected]. of the Global Sustainability Assessment System (GSAS). A total of nine GSAS certifications have been awarded across three stadiums to date: 21 November 2022 – 18 December 2022 The tournament will take place over 28 days, with the final being held on 18 December 2022, which will be the 15th Qatar National Day. Eight stadiums Khalifa International Stadium was inaugurated following an extensive redevelopment on 19 May 2017. Al Janoub Stadium was inaugurated on 16 May 2019 when it hosted the Amir Cup final. -

Qatar and Korea – a Role Model for Strong Bilateral Relations

Special Supplement Thursday, October 01, 2020 Qatar and Korea – A role model for strong bilateral relations extend my heartfelt greetings to the Korean community and Its gradual approach helped people go through difficult times conversation to discuss friends of Korea in the State of Qatar on the occasion of with confidence and resilience. Taking this opportunity, I would the bilateral relations and Ithe 4,353rd Gaecheonjeol, the Korean National Foundation like to renew my appreciation to the government of the State cooperation amid this Day that falls on October 3rd. The word Gaecheonjeol, the of Qatar and many people in the healthcare and medical field pandemic. Korean name for this holiday, literally means “the day heaven for creating a safe environment and helping people stay safe. I am particularly pleased opened”, the birth of Gojoseon that is the first kingdom of The State of Qatar is one of Korea’s most important friends. that Korea partnered with the Korean peninsula. Koreans regard ‘Gaecheonjeol’ as the Both countries have been enjoying strong and enduring Qatar in our common effort day when the nation’s long history began. The philosophy of friendships over decades, and we attach great importance to to combat this virus, and this first kingdom was ‘hongik ingan’, which aims to benefit all this mutually beneficial partnership. very much honored to mankind. This national day makes us reflect the long history be part of this friendship of Korea and rethink about our future-oriented vision that will Qatar is the largest source of LNG supply to Korea, and Korea and partnership between benefit all. -

Sigma Paints Qatar W.L.L

COMPANY PREQUALIFICATION FOR SIGMA PAINTS QATAR W.L.L. INDEX Section 1 ………………………….. GENERAL INFORMATION Section 2 ………………………….. COMPANY ORGANISATION Section 3…………………………... ISO CERTIFICATE Section 4 ………………………….. PROJECT REFERENCES PROTECTIVE COATINGS Section 5 ………………………….. PROJECT REFERENCES DECORATIVE COATINGS Section 6 ………………………….. COMPANY BROCHURES FOR: - DECORATIVE COATINGS - PROTECTIVE COATINGS - MARINE COATINGS GENERAL INFORMATION GENERAL INFORMATION Company Name : SIGMA PAINTS QATAR W.L.L. Office Address : P.O. Box 1296 Doha Qatar Telephone Number : (+974) 44607770 Fax Number : (+974) 44606575 Nature of Business : The Marketing of Protective, Marine, Industrial and Decorative Paints and Coatings. Location of Use : Location of use is Petrochemical Plants, Refineries, Gas Terminals, Sewage Treatment Plant, Pipelines, Storage Tanks, Offshore Facilities as well as Civil Building Projects, Industry and Marine. Commercial Registration : # 23365 dated 19/02/2001 (Georgian) Ownership : A joint venture between Sigma Paints Saudi Arabia. (Part of SigmaKalon Worldwide, a BU of PPG Industries U.S.A) & Sheikh Hamad Bin Faisal Bin Thani Al Thani. Founded As Sigma Coatings BV, an International organization was founded in 1722. Bank Details : HSBC Bank, Doha, Qatar PRODUCTION INFORMATION Production Facility : SIGMA PAINTS factory on the First Industrial Estate in Dammam, KSA was designed and built to the very highest European standards and is capable of Producing a full range of Industrial, Decorative, Marine, Offshore and Protective paint products. -

Health Official FAZEENA SALEEM Community and Help the Health “Getting a Flu Shot This Year the PENINSULA System in Times of COVID-19

QIIB wins World No. 1 4 coveted Farag leads prizes as star cast part of IFN at Qatar Awards 2020 Classic Business | 01 Sport | 12 TUESDAY 20 OCTOBER 2020 3 RABIA I - 1442 VOLUME 25 NUMBER 8416 www.thepeninsula.qa 2 RIYALS Watch Disney+ Streaming App Originals as a gift Terms & Conditions Apply Commissioned by Amir, Sheikh Thani bin Hamad attends opening of Ibn Haldun University QNA — ISTANBUL at the regional and interna- tional level. Commissioned by Amir H H H E Sheikh Thani bin Sheikh Tamim bin Hamad Al Hamad Al Thani, in the Thani in response to the invi- presence of the Turkish Pres- tation of President of the ident, witnessed the signing of Republic of Turkey H E Recep an agreement between Qatar Tayyip Erdogan, H E Sheikh University and Ibn Haldun Uni- Thani bin Hamad Al Thani versity regarding the granting attended the official opening of a joint PhD in many aca- ceremony of Ibn Haldun demic programmes offered by University (IHU), which was held the two universities. yesterday in Istanbul. The opening was attended During the ceremony, H E by a number of Their Excel- Sheikh Thani bin Hamad Al lencies ministers and senior Thani received from the uni- Turkish officials, in addition to versity administration ‘Al Fateh members of the university’s Key ‘, in appreciation of the administrative and teaching President of the Republic of Turkey, H E Recep Tayyip Erdogan, and H E Sheikh Thani bin Hamad Al Thani attending the official opening efforts of the State of Qatar in staff and guests of the ceremony of Ibn Haldun University (IHU), in Istanbul, yesterday. -

Cover Spread

ALMANA DESIGN CONSULTANTS INTERNATIONAL I COMPANY PROFILE Location and Description of the Project Description : The project is a commercial building with 2B+G+M+7 configuration. The buildup area of the project is approximately 50,000 sq.m. Two underground basements are used for car parks, while the ground floor and mezzanine floor are for show rooms and the rest of the floors are for office purpose Airport Road Location : Project Works Description : The project comprised of complete Design and preparation of Tender documents and obtaining all Local Authorities approvals i.e. Architectural, Planning, Kahramaa, Water, Drainage, Ooredoo & QCDD. Nature of Involvement Specialist : Architectural Design (E-Square Architects – Consultants Lebanon) Sub-Consultants : Almana Design Consultants International (MEP Design Only) Complete design of MEP Services which includes HVAC, Fire Protection, Plumbing, Drainage, Electrical and ELV Systems. Review of complete design of Architectural layouts to make sure that the design adheres to Local and International Codes and Standards including obtaining all Local Authorities approvals. DESIGN OF COMMERCIAL BUILDING AT AIRPORT ROAD Value of Contract : QR 285 million ✓ Type of Services: Design - Supervision - Project Management Start and Completion Dates Start Date : February 2012 Completion Date : January 2013 ALMANA DESIGN CONSULTANTS INTERNATIONAL I COMPANY PROFILE Location and Description of the Project Description : The building is an office building with adjoining two towers . Each tower has 32 floors with 3 levels of common basements for car parks. The buildup area is approximately 98,500 sq.m. The building is designed for QSAS rating two (2) stars. Lusail Location : Project Works Description : The project comprised of complete Design and preparation of Tender documents and obtaining all Local Authorities approvals i.e. -

More Classified Contd. on Following Pages

Gulf Times 1 Thursday, April 06, 2017 CLASSIFIED ADVERTISING SITUATION VACANT CEVA Logistics Qatar WLL A reputed company in Qatar has an CEVA provides world class supply chain solutions for large and medium-size excellent employment opportunity for: national and multinational companies across the globe. HEAVY EQUIPMENT Local Candidates are invited to apply for the If you are a qualified candidate, interested in applying to any of the below listed roles, following full time position please send your CV to e-mail address: [email protected] OPERATORS (Excavator, Bulldozer, Loader, Grader) ROLE BRIEF DESCRIPTION GULF Candidates must have Minimum of two 1. Female HR Coordinator / Recruiter • 3 years in sales Role in Freight forwarding or Logistics TIMES (2) year experience and Valid Qatari (Job Ref. 005) Business Development • Experience in Qatar Market Operator’s license. Tozzi Qatar W.L.L. is the local subsidiary of an Italian • Valid Qatar driving license Change of Sponsorship is a must. Executive - Doha • Communication Skills – English, Arabic is a Plus Classified Industrial Group leader in the Electrical and Instrumentation • Transferable visa status Advertising Projects for Oil & Gas, Power and Industrial Plants. Mail your CV with copies of certificates to [email protected] or • 3 years in senior sales Role in Freight forwarding or Tel: Only Candidates with Local Transferable Visa are required to forward their CV through our website: Logistics 44466609 Fax to 44600225 (after 5 p.m.). www.tozziqatar.com.qa or Business Development • Experience in Qatar Market 44466648 [email protected] Manager - Doha • Valid Qatar driving license • Communication Skills – English, Arabic is a Plus . -

Work on Qatar's 1St Cable-Stayed Bridge Begins

BUSINESS | Page 1 SPORT | Page 1 Nantes keep PSG waiting Qatar streamlining investment, business for title initiatives: MoCI published in QATAR since 1978 THURSDAY Vol. XXXX No. 11157 April 18, 2019 Sha’baan 13, 1440 AH GULF TIMES www. gulf-times.com 2 Riyals In brief Jordan king meets defence minister QATAR | Offi cial Amir condoles with Work on Qatar’s president of Congo His Highness the Amir Sheikh Tamim bin Hamad al-Thani and His Highness 1st cable-stayed the Deputy Amir Sheikh Abdullah bin Hamad al-Thani sent yesterday cables of condolences to the President of the Democratic Republic of Congo, Felix Tshisekedi, on the victims of the bridge begins sunken ship, wishing the injured a speedy recovery. O Bridge to be ready in the first quarter of 2021 ARAB WORLD | Unrest he Public Works Authority Bashir moved to prison (Ashghal) has started the con- Tstruction of Qatar’s fi rst cable- as protesters rally Jordan’s King Abdullah II, Supreme Commander of the Jordanian Armed Forces, met with HE the Deputy Prime Minister and stayed bridge and the conversion of Sudan’s military rulers have Minister of State for Defence Aff airs Dr Khalid bin Mohamed al-Attiyah at the Al Husseiniya Palace in Amman yesterday. HE al- Haloul Roundabout into a two-level transferred ousted president Omar al- Attiyah, who is on an off icial visit to Jordan, conveyed the greetings of His Highness the Amir Sheikh Tamim bin Hamad al-Thani interchange as part of Sabah Al Ahmad Bashir to prison, a family source said to King Abdullah II. -

Madinat Khalifa and Ghar Tri Logistics Buses For

Tri Logistics Buses for Compass International School of Doha C1 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops 5:30AM 5:36AM 6:05AM C1 House 6:15AM 6:30AM 6:43AM C2 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops 5:50AM 2:40AM 6:10AM 6:15AM 6:33AM C2 House 6:35AM 6:37AM 6:40AM 6:42AM 6:55AM C3 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops No Pick-up 5:50AM C3 House No Pick-up 5:59AM 6:03AM 6:08AM C3 House 6:15AM 6:19AM 6:40AM C4 - Madinat Khalifa Campus Pick-up AM Pick-up Time AM Bus Stops 5:10AM 5:18AM 5:28AM 5:34AM 5:36AM 5:33AM C4 House 5:38AM 6:58AM 6:18AM 6:23AM C5 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops 5:31AM 5:35AM 5:53AM 6:08AM 6:13PM C5 House 6:18AM 6:28AM 6:38AM 6:45AM 6:58AM Rayyan Campus Pick-up AM Pick-up Time AM Bus Stops 5:40AM 6:10AM 6:30AM 6:30AM 6:32AM C6 House 6:40AM 6:50AM 6:55AM C7 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops 6:00AM Club- C7 6:20AM 6:24AM 6:27AM House 6:32AM 6:40AM C8 - Rayyan Campus Pick-up AM Pick-up Time AM Bus Stops 5:43AM 5:55AM C8 House 5:57AM 6:20AM 6:25AM 6:28AM 6:33AM No Pick-up C9 - Rayyan Campus Pick-up AM Pick-up Time AM Bus Stops 5:43AM 5:56AM C9 House 6:12AM C9 House 6:15AM 6:22AM C10 - Madinat Khalifa and Gharaffa Campus Pick-up AM Pick-up Time AM Bus Stops 6:15AM House 6:30AM C10 Club- 6:45AM house Tri Logistics Buses for Compass International School of Doha C1 - Madinat Khalifa and Gharaffa Campus Drop-off PM Address Time PM Bus Jaffar Bin Abi Talib St. -

Experience Record Important Completed Projects

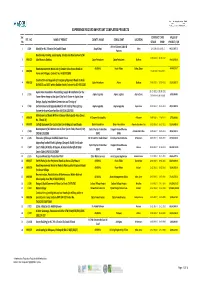

EXPERIENCE RECORD IMPORTANT COMPLETED PROJECTS Ser. CONTRACT DATE VALUE OF REF . NO . NAME OF PROJECT CLIENT'S NAME CONSULTANT LOCATION No STRART FINISH PROJECT / QR Artline & James Cubitt & 1 J/149 Masjid for H.E. Ghanim Bin Saad Al Saad Awqaf Dept. Dafna 12‐10‐2011/31‐10‐2012 68,527,487.70 Partners Road works, Parking, Landscaping, Shades and Development of Al‐ 22‐08‐2010 / 21‐06‐2012 2 MRJ/622 Jabel Area in Dukhan. Qatar Petroleum Qatar Petroleum Dukhan 14,428,932.00 Road Improvement Works out of Greater Doha Access Roads to ASHGHAL Road Affairs Doha, Qatar 48,045,328.17 3 MRJ/082 15‐06‐2010 / 13‐06‐2012 Farms and Villages, Contract No. IA 09/10 C89G Construction and Upgrade of Emergency/Approach Roads to Arab 4 MRJ/619 Qatar Petroleum Atkins Dukhan 27‐06‐2010 / 10‐07‐2012 23,583,833.70 D,FNGLCS and JDGS within Dukhan Fields,Contract No.GC‐09112200 Aspire Zone Foundation Dismantling, Supply & Installation for the 01‐01‐2011 / 30‐06‐2011 5 J / 151 Aspire Logistics Aspire Logistics Aspire Zone 6,550,000.00 Tower Flame Image at the Sport City Torch Tower in Aspire Zone Extension to be issued Design, Supply, Installation.Commission and Testing of 6 J / 155 Enchancement and Upgrade Work for the Field of Play Lighting Aspire Logestics Aspire Logestics Aspire Zone 01‐07‐2011 / 25‐11‐2011 28,832,000.00 System for Aspire Zone Facilities (AF/C/AL 1267/10) Maintenance of Roads Within Al Daayen Municipality Area (Zones 7 MRJ/078 Al Daayen Municipality Al Daayen 19‐08‐2009 / 11‐04‐2011 3,799,000.00 No. -

Al Thumama Stadium Achieves Major Work Safety Milestone Third Qatar

IQ becomes sole Qatar ownerow of QAFCO, remains the the world’s home of Asian largestlar single-site football: QFA urea producer President Business | 01 Sport | 12 MONDAY 14 SEPTEMBER 2020 26 MUHARRAM - 1442 VOLUME 25 NUMBER 8380 www.thepeninsula.qa 2 RIYALS Choose the network of heroes Enjoy the Internet Amir meets Afghan HCNR Chairman QNA — DOHA Amir H H Sheikh Tamim bin Hamad Al Thani met at the Amiri Diwan Office yesterday morning with Chairman of the High Council for National Reconciliation of Afghanistan (HCNR), H E Dr. Abdullah Abdullah, and the accompanying delegation, who called on H H the Amir to greet him on the occasion of their visit to the country to participate in the Afghanistan Peace Negotiations. At the outset of the meeting, H H the Amir expressed pleasure and satisfaction with the launch of these negotiations. H H the Amir also wished that these negotiations will be a success and achieve the Afghan people’s aspirations for national unity, progress and prosperity. For his part, H E Dr. Abdullah Abdullah expressed sincere thanks and appreciation to H H the Amir for the State of Qatar’s Amir H H Sheikh Tamim bin Hamad Al Thani meeting with the Chairman of the High Council for National Reconciliation of Afghanistan, H E Dr. hosting of the Afghan Peace Negotiations, and its constant Abdullah Abdullah, and the accompanying delegation, at the Amiri Diwan Office yesterday. keenness to establish peace, security and stability in Afghanistan. Third Qatar-US Strategic Dialogue begins in Washington today IRFAN BUKHARI economies in the world.