Functional Reference

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Scanned Image

3130 W 57th St, Suite 105 Sioux Falls, SD 57108 Voice: 605-373-0201 Fax: 605-271-5721 [email protected] www.greatplainsfa.com Securities offered through First Heartland Capital, Inc. Member FINRA & SIPC. Advisory Services offered through First Heartland Consultants, Inc. Great Plains Financial Advisors, LLC is not affiliated with First Heartland Capital, Inc. In this month’s recap: the Federal Reserve eases, stocks reach historic peaks, and face-to-face U.S.-China trade talks formally resume. Monthly Economic Update Presented by Craig Heien with Great Plains Financial Advisors, August 2019 THE MONTH IN BRIEF July was a positive month for stocks and a notable month for news impacting the financial markets. The S&P 500 topped the 3,000 level for the first time. The Federal Reserve cut the country’s benchmark interest rate. Consumer confidence remained strong. Trade representatives from China and the U.S. once again sat down at the negotiating table, as new data showed China’s economy lagging. In Europe, Brexit advocate Boris Johnson was elected as the new Prime Minister of the United Kingdom, and the European Central Bank indicated that it was open to using various options to stimulate economic activity.1 DOMESTIC ECONOMIC HEALTH On July 31, the Federal Reserve cut interest rates for the first time in more than a decade. The Federal Open Market Committee approved a quarter-point reduction to the federal funds rate by a vote of 8-2. Typically, the central bank eases borrowing costs when it senses the business cycle is slowing. As the country has gone ten years without a recession, some analysts viewed this rate cut as a preventative measure. -

New Years Trading Schedule 2021

New Years Trading Schedule 2021 Product Thurs Dec 31st Fri Jan 1st Mon Jan 4th Tues Jan 5th Australian Securities Exchange | ASX 9:30pm Wednesday Night All Products Early Close Closed Normal Hours Normal Hours Chicago Mercantile Exchange | CME Currency & Eurodollar Normal Hours Closed Normal Hours Normal Hours Equity Index Normal Hours Closed Normal Hours Normal Hours Livestock 8:30am Livestock & Lumber Normal Hours Closed Open/Lumber 9am Open Normal Hours Dairy 1:55pm Early Close Closed Normal Hours Normal Hours Globex Bitcoin Normal Hours Closed Normal Hours Normal Hours Globex Currency & Eurodollar Normal Hours Closed Normal Hours Normal Hours Globex Equity Index Normal Hours Closed Normal Hours Normal Hours Pre-Open 8am - Livestock 8:30am Open/Pre-Open Globex Livestock & Lumber Normal Hours Closed 6am - Lumber 9am Open Normal Hours Globex Dairy 1:55pm Early Close Closed Normal Hours Normal Hours Chicago Board of Options Exchange | CBOE CBOE/CFE 12:15pm Early Close Closed Normal Hours Normal Hours Chicago Board of Trade | CBOT Treasuries Normal Hours Closed Normal Hours Normal Hours Grains Normal Hours Closed 8:30am Open Normal Hours Globex Treasuries Normal Hours Closed Normal Hours Normal Hours MGEX Wheat Pre-Open 7:45am/Pre-Open 8:00am - Globex Grains Normal Hours Closed 8:30am Open Normal Hours Montreal Exchange | MX Interest Rates 12:30pm Early Close Closed Normal Hours Normal Hours Stock Indices Normal Hours Closed Normal Hours Normal Hours ICE Futures Canada | ICE All Products Normal Hours Closed Normal Hours Normal Hours European -

Additional Provisions Applicable When Trading Asian Markets Using Electronic Connectivity

ADDITIONAL PROVISIONS APPLICABLE WHEN TRADING ASIAN MARKETS USING ELECTRONIC CONNECTIVITY A. Rules for Trading on Asian markets 1. Applicable Law You acknowledge and agree that you must comply in all respects with Applicable Law, including in relation to short sales of securities when using the Trading System. 2. Asian Exchange “Asian Exchange” means exchanges, markets or associations of dealers to which the Relevant JPMorgan Entity (either directly or through its agents) from time to time provides DMA to Client for the purchase and sale of securities, including, without limitation, exchanges in Australia, Hong Kong, Japan, Korea, Singapore, Taiwan, India, Indonesia, Malaysia, Thailand and/or such other countries as may be determined from time to time. 3. Relevant JPMorgan Entity “Relevant JPMorgan Entity” means any one or more of the JPMorgan brokers with whom you have a contractual relationship to trade securities electronically, and for the avoidance of doubt may include, without limitation, any one or more of the following: J.P. Morgan Securities Australia Limited, J.P. Morgan Securities Singapore Private Limited, JPMorgan Securities Japan Co. Ltd., J.P. Morgan Securities (Asia Pacific) Limited, J.P. Morgan Broking (Hong Kong) Limited, J.P. Morgan Securities (Far East) Ltd., Seoul Branch, J.P. Morgan Securities (Taiwan) Limited, J.P. Morgan India Private Limited, PT J.P. Morgan Securities Indonesia, JPMorgan Securities (Malaysia) Sdn. Bhd., JPMorgan Securities (Thailand) Limited and any of their successors or assigns. B. Rules for Trading on Australian Markets 1. Prohibited conduct 1.1 You must not, and must procure that your Representatives do not, take any action or omit to take any action so that you breach any Applicable Law and in particular you must advise Relevant JPMorgan Entity immediately if you believe that you or any of your Representatives have breached, or may breach, any provision of this Clause 1.1. -

List of Execution Venues Made Available by Societe Generale

List of Execution Venues made available by Societe Generale January 2018 Note that this list of Execution Venues is not exhaustive and will be kept under review and updated in accordance with Societe Generale’s execution practices. Societe Generale reserves the right to use other Execution Venues in addition to those listed below where it deems it appropriate in accordance with execution practices. Where Societe Generale acts as the Execution Venue, it will consider all sources of reasonably available information to obtain the best possible outcome. Fixed Income . The main Execution Venue is Societe Generale SA (and its affiliates) . When the trading obligation for derivatives applies, execution will take place on MiFID trading venues (Regulated Markets, or MTF or OTF or all equivalent venues as SEF) Alternative Venues include: BGC Bloomberg Bloomberg FIET Brokertec GFI Marketaxess MTP MTS TP ICAP Tradeweb Tradition Forex . The main Execution Venue is Societe Generale SA (and its affiliates) Alternative Venues include: 360T Alpha BGC Bloomberg Currenex EBS Equilend FX Connect FX Spotstream FXall Hotpspot ICAP Integral FX inside Reuters Tradertools Cash Equities Abu Dhabi Securities Exchange EDGEA Exchange NYSE Amex Alpha EDGEX Exchange NYSE Arca AlphaY EDGX NYSE Stock Exchange Aquis Equilend Omega ARCA Stocks Euronext Amsterdam OMX Copenhagen ASX Centre Point Euronext Block OMX Helsinki Athens Stock Exchange Euronext Brussels OMX Stockholm ATHEX Euronext Cash Amsterdam OneChicago Australia Securities Exchange Euronext Cash Brussels Oslo -

Doing Data Differently

General Company Overview Doing data differently V.14.9. Company Overview Helping the global financial community make informed decisions through the provision of fast, accurate, timely and affordable reference data services With more than 20 years of experience, we offer comprehensive and complete securities reference and pricing data for equities, fixed income and derivative instruments around the globe. Our customers can rely on our successful track record to efficiently deliver high quality data sets including: § Worldwide Corporate Actions § Worldwide Fixed Income § Security Reference File § Worldwide End-of-Day Prices Exchange Data International has recently expanded its data coverage to include economic data. Currently it has three products: § African Economic Data www.africadata.com § Economic Indicator Service (EIS) § Global Economic Data Our professional sales, support and data/research teams deliver the lowest cost of ownership whilst at the same time being the most responsive to client requests. As a result of our on-going commitment to providing cost effective and innovative data solutions, whilst at the same time ensuring the highest standards, we have been awarded the internationally recognized symbol of quality ISO 9001. Headquartered in United Kingdom, we have staff in Canada, India, Morocco, South Africa and United States. www.exchange-data.com 2 Company Overview Contents Reference Data ............................................................................................................................................ -

Voluntary Delisting in Korea: Causes and Impact on Company Performance Sun Min Kang, Ph.D., Chung-Ang University, South Korea

The Journal of Applied Business Research – March/April 2017 Volume 33, Number 2 Voluntary Delisting In Korea: Causes And Impact On Company Performance Sun Min Kang, Ph.D., Chung-Ang University, South Korea ABSTRACT This research investigates the attributes of firms that choose to voluntarily delist in Korea, including the evolution of firms after delisting, using performance indicators such as total assets, revenue, and net income. Empirical evidence suggests that the higher the shareholding ratio of the largest shareholder and the higher the growth prospects and liquidity, the greater the incentive for voluntary delisting. In addition, firms in non-high-tech industries choose to delist more often than those in high-tech industries. Further, firms that have delisted show lower total assets, revenues, and net incomes than listed firms, and these gaps increase over time. Keywords: Voluntary Delisting; The Largest Shareholder Ratio; Growth Prospect; Performance INTRODUCTION elisting refers to the loss of the trading eligibility of a listed company’s marketable securities and the cancellation of a qualified listing. Generally, delisting happens under the authority of a stock exchange. When a serious management problem occurs (e.g., bankruptcy) and investors incur losses, Dor when there is a risk of undermining the order of the stock market, the stock exchange will delist a company that meets the delisting criteria in order to protect investors, unless the reason for delisting is resolved during a certain grace period. Alternatively, a company may voluntarily delist itself through the public purchase of treasury stock. Many unlisted companies undertake an initial public offering (IPO) to obtain funding without debt by issuing shares, despite the complicated conditions and procedures of IPOs. -

Bofa List of Execution Venues

This List of Execution Venues and the associated Bank of America EMEA Order Execution Policy Summary form part of the General Terms & Conditions of Business available on the Bank of America MifID II Website www.bofaml.com/mifid2 The tables below set out the execution venues accessed by entities in the Bank of America Entities List and Associated Companies. These tables are not exhaustive and we may amend them from time to time in accordance with our policies. MLI and BofASE may also use other execution venues from time to time where they deem appropriate but in accordance with their policies (including the Bank of America Order Execution Policy). Asset class Region Regulated Markets of which MLI / BofASE is a direct member and MTFs accessed by MLI / BofASE Equities EMEA Aquis UK Equities EMEA Athex Group Equities EMEA Bloomberg BV Equities EMEA Bloomberg UK Equities EMEA Borsa Italiana Equities EMEA Cboe BV Equities EMEA Cboe UK Equities EMEA Deutsche Borse Xetra Equities EMEA Equiduct Equities EMEA Euronext Amsterdam Equities EMEA Euronext Brussels Equities EMEA Euronext Dublin Equities EMEA Euronext Lisbon Equities EMEA Euronext Oslo Equities EMEA Euronext Paris Equities EMEA ITG Posit Equities EMEA Liquidnet Equities EMEA Liquidnet Europe Equities EMEA London Stock Exchange 1 – ©2020 Bank of America Corporation Asset class Region Regulated Markets of which MLI / BofASE is a direct member and MTFs accessed by MLI / BofASE Equities EMEA NASDAQ OMX Nordic – Helsinki Equities EMEA NASDAQ OMX Nordic – Stockholm Equities EMEA NASDAQ OMX -

List of Execution Venues

List of Execution Venues Version 2.0 Effective January 2019 Bank of America Merrill Lynch (“BofAML”) (including its affiliates) uses the following execution venues when obtaining best execution as defined by MiFID. The list detailed below is not exhaustive and may be subject to change and reissued from time to time, as set out in BofAML’s Policy. BofAML may also use other execution venues where it deems appropriate from time to time in accordance with the guidelines set out in the Policy. Regulated Markets of which MLI is a direct member and MTFs Asset class Region accessed by MLI Aquis UK Equities EMEA Athex Group Equities EMEA Bloomberg UK Equities EMEA Borsa Italiana Equities EMEA Cboe UK Equities EMEA Deutsche Borse Xetra Equities EMEA Equiduct Equities EMEA Euronext Amsterdam Equities EMEA Euronext Brussels Equities EMEA Euronext Paris Equities EMEA Euronext Lisbon Equities EMEA Irish Stock Exchange Equities EMEA ITG Posit Equities EMEA London Stock Exchange Equities EMEA NASDAQ OMX Nordic- Copenhagen Equities EMEA NASDAQ OMX Nordic – Helsinki Equities EMEA NASDAQ OMX Nordic – Stockholm Equities EMEA Oslo Børs Equities EMEA Six Swiss Exchange Equities EMEA Tel Aviv Stock Exchange Equities EMEA Trade Web UK Equities EMEA Version 2.0 – January 2019 ©2019 Bank of America Corporation 1 Proprietary List of Execution Venues Version 2.0 Effective January 2019 Turquoise Equities EMEA UBS Equities EMEA Warsaw Stock Exchange Equities EMEA Wiener Börse Equities EMEA Regulated Markets of which BofASE is/will be a direct member and MTFs that are/will be accessed by BofASE subject to BofASE Asset class Region membership approval. -

Execution Venues Equities and Fixed Income

UBS AG London Branch 5 Broadgate London EC2M 2QS United Kingdom UBS Europe SE OpernTurm Bockenheimer Landstraße 2-4 60306 Frankfurt am Main Germany www.ubs.com/ibterms Execution venues Equities and fixed income Version: December 2020 For information about our investment bank entities, visit www.ubs.com/ibterms Execution venues This is a non-exhaustive list of the main execution venues that we use outside UBS and our own systematic internalisers. We will review and update it from time to time in accordance with our UK and EEA MiFID Order Handling & Execution Policy. We may use other execution venues where appropriate. Equities Cash Equities Direct access Aquis Exchange Europe Aquis Exchange PlcAthens Stock Exchange BATS Europe, a CBOE Company Borsa Italiana CBOE NL CBOE UK Citadel Securities (Europe) Limited SI Deutsche Börse Group - Xetra Euronext Amsterdam Stock Exchange Euronext Brussels Stock Exchange Euronext Lisbon Stock Exchange Euronext Paris Stock Exchange Instinet Blockmatch Euronext DublinITG Posit London Stock Exchange Madrid Stock Exchange Nasdaq Copenhagen Nasdaq Helsinki Nasdaq Stockholm Oslo Bors Sigma X Europe Sigma X MTFTower Research Capital Europe Limited SI Turquoise Europe TurquoiseUBS Investment Bank UBS MTF Vienna Stock Exchange Virtu Financial Ireland Limited Warsaw Stock Exchange Via intermediate broker Budapest Stock Exchange Cairo & Alexandria Stock Exchange Deutsche Börse - Frankfurt Stock Exchange Istanbul Stock Exchange Johannesburg Stock Exchange Moscow Exchange Prague Stock Exchange SIX Swiss Exchange Tel Aviv Stock Exchange Structured Products Direct access Börse Frankfurt (Zertifikate Premium) Börse Stuttgart (EUWAX) Xetra SIX Swiss Exchange SeDeX Milan Euronext Amsterdam London Stock Exchange Madrid Stock Exchange NASDAQ OMX Stockholm JSE Johannesburg Stock Exchange OTC matching CATS-OS Fixed Income Cash bonds Via Bond Port Bloomberg EuroTLX Euronext ICE (KCG) BondPoint Market Axess MOT MTS BondsPro 1 © UBS 2020. -

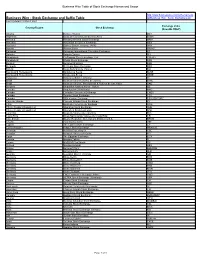

Stock Exchange and Suffix Table Ml/Business Wire Stock Exchanges.Pdf Last Updated 12 March 2021

Business Wire Table of Stock Exchange Names and Usage http://www.businesswire.com/schema/news Business Wire - Stock Exchange and Suffix Table ml/Business_Wire_Stock_Exchanges.pdf Last Updated 12 March 2021 Exchange Value Country/Region Stock Exchange (NewsML ONLY) Albania Bursa e Tiranës BET Argentina Bolsa de Comercio de Buenos Aires BCBA Armenia Nasdaq Armenia Stock Exchange ARM Australia Australian Securities Exchange ASX Australia Sydney Stock Exchange (APX) APX Austria Wiener Börse WBAG Bahamas Bahamas International Securities Exchange BS Bahrain Bahrain Bourse BH Bangladesh Chittagong Stock Exchange, Ltd. CSEBD Bangladesh Dhaka Stock Exchange DSE Belgium Euronext Brussels BSE Bermuda Bermuda Stock Exchange BSX Bolivia Bolsa Boliviana de Valores BO Bosnia and Herzegovina Banjalucka Berza BLSE Bosnia and Herzegovina Sarajevska Berza SASE Botswana Botswana Stock Exchange BT Brazil Bolsa de Valores do Rio de Janeiro BVRJ Brazil Bolsa de Valores, Mercadorias & Futuros de Sao Paulo SAO Bulgaria Balgarska fondova borsa - Sofiya BB Canada Aequitas NEO Exchange NEO Canada Canadian Securities Exchange CNSX Canada Toronto Stock Exchange TSX Canada TSX Venture Exchange TSX VENTURE Cayman Islands Cayman Islands Stock Exchange KY Chile Bolsa de Comercio de Santiago SGO China, People's Republic of Shanghai Stock Exchange SHH China, People's Republic of Shenzhen Stock Exchange SHZ Colombia Bolsa de Valores de Colombia BVC Costa Rica Bolsa Nacional de Valores de Costa Rica CR Cote d'Ivoire Bourse Regionale Des Valeurs Mobilieres S.A. BRVM Croatia -

TOKYO STOCK EXCHANGE GROUP Annual Report 2008 a Bout the Tokyo Stock Exchange Group

TOKYO STOCK EXCHANGE GROUP Annual Report 2008 A bout the Tokyo Stock Exchange Group Profile The Tokyo Stock Exchange (TSE) has served as Japan’s The TSE tirelessly strives to maintain abundant liquidity “central market” since its foundation in 1878, and has and a high level of integrity, and provide market played a crucial role in the growth and expansion of the participants from Japan and abroad with attractive nation’s economy. In 2007, the TSE accounted for an investment opportunities. overwhelming 95% of the total value of all stock trading on domestic stock exchanges. The TSE, which became a stock corporation in November 2001, revamped its corporate structure in 2007 to cement The TSE had a market value of ¥396 trillion as of the end the independence and effectiveness of its self-regulatory of March 2008, and a trading value of ¥720 trillion for the function, as well as enable it to act with more flexibility in fiscal year ended March 31, 2008, making it one of the its international business strategy. The TSE established the leading stock exchanges in the world in terms of both size holding company, Tokyo Stock Exchange Group, Inc., in and liquidity. August 2007, and the self-regulatory corporation, Tokyo Stock Exchange Regulation, was created in October of the The TSE group offers a wide range of exchange services. same year. In November 2007, the TSE shifted to a new In addition to its core Japanese stock market, the TSE organizational system wherein the TSE, a market provides markets for derivatives products such as operation company and Tokyo Stock Exchange Regulation Japanese government bond futures and TOPIX futures. -

Insights Into Trading System Dynamics Deutsche Börse's

Insights into Trading System Dynamics Deutsche Börse’s T7® July 2021 23 April, 2021 Content 3 Introduction 34 What you need to be fast 7 Recent Developments 37 T7 Overview 12 Latency Analysis 47 Appendix 23 Market data Deutsche Börse Group 2 3 Introduction T7® Technology Roadmap Deutsche Börse is pursuing its technology roadmap to deliver innovative and superior trading technology. Recent developments Outlook • February/March 2021: Hardware refresh of Matching Engine ▪ July 2021: Additional Matching Engine tuning measures servers ▪ 31 August 2021: Decommissioning (old) FIX gateway back- • February/March 2021: First rollout step of optional new FIX LF office sessions gateway architecture ▪ 22 November 2021: T7 Release 10.0 • 29 March 2021: Introduction of additional Eurex order entry and ▪ Q4/2021: New FIX LF gateway trading sessions market data switches for Colo 2.0 ▪ Q2/2022: Decommissioning (old) FIX gateway trading sessions • March-May 2021: Consolidation of PS gateway and Matching Engine process into a single process • 25 May 2021: Introduction of DSCP field & discard IP for Xetra • 28 June 2021: T7 Release 9.1 Deutsche Börse Group 4 T7® Technology Roadmap Timeline of updates 2021 Jan Feb Hardware refresh Matching Engines First step of new FIX LF gateway architecture Mar Start of consolidation PS gateway and Matching Engine Apr Introduction of additional Eurex Colo 2.0 order entry and market data switches May Finish roll-out of consolidation PS gateway and Matching Engine EOBI DSCP field & discard IP for Xetra Jun T7® Release 9.1 Jul Additional tuning measures Aug Sep Decommissioning (old) FIX gateway back-office sessions Oct Nov T7® Release 10.0 Dec Deutsche Börse Group 5 Processed Transactions and Response Times T7 request – response round-trip times ▪ Deutsche Börse has continuously invested in its trading system and is holding up transparency while providing a low latency trading venue.