Return of Organization Exempt from Income Tax 01V113 No 1545-M

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Faith Voices Letter

In Support Of Keeping Houses Of Worship Nonpartisan August 16, 2017 Dear Senator: As a leader in my religious community, I am strongly opposed to any effort to repeal or weaken current law that protects houses of worship from becoming centers of partisan politics. Changing the law would threaten the integrity and independence of houses of worship. We must not allow our sacred spaces to be transformed into spaces used to endorse or oppose political candidates. Faith leaders are called to speak truth to power, and we cannot do so if we are merely cogs in partisan political machines. The prophetic role of faith communities necessitates that we retain our independent voice. Current law respects this independence and strikes the right balance: houses of worship that enjoy favored tax-exempt status may engage in advocacy to address moral and political issues, but they cannot tell people who to vote for or against. Nothing in current law, however, prohibits me from endorsing or opposing political candidates in my own personal capacity. Changing the law to repeal or weaken the “Johnson Amendment” – the section of the tax code that prevents tax-exempt nonprofit organizations from endorsing or opposing candidates – would harm houses of worship, which are not identified or divided by partisan lines. Particularly in today’s political climate, engaging in partisan politics and issuing endorsements would be highly divisive and have a detrimental impact on congregational unity and civil discourse. I therefore urge you to oppose any repeal or weakening of the Johnson Amendment, thereby protecting the independence and integrity of houses of worship and other religious organizations in the charitable sector. -

Front Cover 01-2012.Ppp

The Official Publication of the Worldwide TV-FM DX Association JANUARY 2012 The Magazine for TV and FM DXers Anxious Dxers Camp out on a Snowy New Years Eve Anticipating huge Discounts on DX Equipment at Ozzy’s House of Antennas. Paul Mitschler Happy New DX Year 2012! Visit Us At www.wtfda.org THE WORLDWIDE TV-FM DX ASSOCIATION Serving the UHF-VHF Enthusiast THE VHF-UHF DIGEST IS THE OFFICIAL PUBLICATION OF THE WORLDWIDE TV-FM DX ASSOCIATION DEDICATED TO THE OBSERVATION AND STUDY OF THE PROPAGATION OF LONG DISTANCE TELEVISION AND FM BROADCASTING SIGNALS AT VHF AND UHF. WTFDA IS GOVERNED BY A BOARD OF DIRECTORS: DOUG SMITH, GREG CONIGLIO, KEITH McGINNIS AND MIKE BUGAJ. Editor and publisher: Mike Bugaj Treasurer: Keith McGinnis wtfda.org Webmaster: Tim McVey wtfda.info Site Administrator: Chris Cervantez Editorial Staff: Jeff Kruszka, Keith McGinnis, Fred Nordquist, Nick Langan, Doug Smith, Peter Baskind, Bill Hale and John Zondlo, Our website: www.wtfda.org; Our forums: www.wtfda.info _______________________________________________________________________________________ We’re back. I hope everyone had an enjoyable holiday season! So far I’ve heard of just one Es event just before Christmas that very briefly made it to FM and another Es event that was noticed by Chris Dunne down in Florida that went briefly to FM from Colombia. F2 skip faded away somewhat as the solar flux dropped down to the 130s. So, all in all, December has been mostly uneventful. But keep looking because anything can still happen. We’ve prepared a “State of the Club” message for this issue. -

Innovation Potential in the Tri-Valley Report

Innovation Potential in the Tri-Valley: A Special Report 1 Innovation Potential in the Tri-Valley A Special Report Prepared by the Innovation Tri-Valley Initiative JULY 22, 2010 Innovation Potential in the Tri-Valley: A Special Report 2 Contents Introduction 3 Executive Summary 5 Interview Highlights 14 Profile of the Tri-Valley 28 Ecology of Innovation 40 Overview 41 Details of the Tri-Valley Ecosystem 46 Benchmarking 74 Nashville, TN 76 The Research Triangle, NC 83 San Diego, CA 90 Austin, TX 98 Summary 104 Acknowledgements 105 Innovation Potential in the Tri-Valley: A Special Report 3 Introduction Innovation Potential in the Tri-Valley: A Special Report 4 Introduction The major purpose of the “Innovation Potential in the Tri-Valley” report is to identify and analyze the assets of the five-city California region (Danville, Dublin, Livermore, Pleasanton and San Ramon) in the context of its innovation potential. The report provides a basis for developing the innovation plan for the region. It also provides the background data and analysis for further assessment of the regions potential as an innovation hub. The research was commissioned by the steering committee of the Innovation Tri-Valley Initiative. The steering comitee conducted the research in a relatively short four-week period and prepared this report. The report consists of six sections and they are: 1. Executive Summary; 2. Results of interviews with leaders and stakeholders in the region; 3. Demographic and economic profile of the region; 4. The tech sector, gazelles, and corporate headquarters; 5. Ecology of innovation-Tri-Valley assets; 6. Benchmark study of four innovation regions. -

The Mission of Incarnate Word Parish

Third Sunday of Lent13416 Olive Boulevard, Chesterfield, Missouri 63017 • 314-576-5366February 28, 2016 www.incarnate-word.org The Mission of Incarnate Word Parish Endowed with the gifts of the Holy Spirit, We, the members of the Incarnate Word Faith community, dedicate ourselves in a spirit of mutual respect, to live and proclaim the gospel message of Jesus Christ. We are called to do this by reaching in to our parish family and reaching out to the universal Church and to the global community, by ministering to their spiritual, educational, social and material needs. We will do this by using our God-given gifts of time, talents, and treasures in an environment of collaborative ministry, in full harmony with the teachings and traditions of our Catholic faith. Third Sunday of Lent Incarnate Word Parish February 28, 2016 13416 Olive Blvd., Chesterfield, MO 63017 Phone (314) 576-5366 Fax (314) 576-2046 Website: www.incarnate-word.org Facebook: Incarnate Word Catholic Church Twitter: @IWParish Pastoral Staff Mass Schedule Pastor Rev. Timothy Vowels ext. 13 Sunday Masses: Saturday: 5:00 p.m. Senior Associate Pastor Rev. James Sullivan ext. 46 Sunday: 7:15 a.m., 8:45 a.m., 10:30 a.m., 12:15 p.m. and Sr. Associate Pastor-P/T Rev. Jack Schuler ext. 14 6:00 p.m. LifeTeen Mass Permanent Deacon Rev. Mr. Larry Stallings 560-4184 The Mother Teresa Infant Nursery is available during all Masses for the comfort of parents with infants. Closed-circuit Worship TV is available in the Mother Teresa Nursery. Music Director Dr. -

Temple Times

The Monthly Magazine of Temple Emanu-El of Tucson | 225 North Country Club Road, Tucson, AZ 85716 TEMPLE(520) 327-4501 TIMES www.tetucson.org Jane 2019 - Iyyar/Sivan 5779 Vol. LXVII No. 10 So Much to Celebrate in June YSaturday, June 8th, 8:00 pm - Tikkun L’eil Shavu’ot Festival Service, Torah Study and Ice Cream Social YThursday, June 13th, 7:00 pm - Celebrating 20 Years of Song: A Concert in Honor of Cantorial Soloist Marjorie Hochberg YFriday, June 14th - Seeking Shabbat Services in honor of Cantorial Soloist Marjorie Hochberg 5:00 pm - Noshes 5:30 pm - Seeking Shabbat Services 6:30 pm - Shabbat dinner YSaturday, June 15th, 10 am - B’not Mitzvah of Shishiniyot Ron Benacot and Rotem Rapaport Mazal Tov to our Confirmands: Ben Sargus, Malachi Fisher, Darian German, and Kyra Glassey (photo by Steve Shawl) FROM RABBI MUSICAL NOTES APPEL’S DESK It’s All About Me. Shavu’ot Music@Emanu-El Presents: 20 Years of Song th We reach the end of our counting Thursday, June 13 at 7:00 pm. of days and weeks this month with (520) 327-4501 the Festival of Shavu’ot. Beginning One of my colleagues at the Temple once the second night of Passover, we described my tenure here as a life sentence. have been counting up the days un- It might turn out that way: I recently calculated that I’ve til we reach the day that commemorates the giving been involved with Temple life for 38 years (!), but I’ve only of Torah at Mount Sinai. -

Marriage and the Family in the United States: Resources for Society a Review of Research on the Benefits Generated from Families Rooted in Marriage

Marriage and the Family in the United States: Resources for Society A review of research on the benefits generated from families rooted in marriage. 2012 Prepared by Theresa Notare, PhD Assistant Director, Natural Family Planning Program and H. Richard McCord, EdD Former Executive Director Secretariat of Laity, Marriage, Family Life and Youth, United States Conference of Catholic Bishops Washington, DC United States of America Marriage and the Family in the United States: Resources for Society A review of research on the benefits generated from families rooted in marriage. Contents Introduction .………………………..…………………………...… p. 1 Psychological Development and Emotional Well-Being .………… p. 3 Physical Health of Family Members ………….…………………. p. 11 Economic Benefits ......……………………….………………….. p. 16 Conclusion—Marriage is a Good for Society .….……………….. p. 23 The Family in the United States: A Resource for Society Review of the Research Introduction The family generates important social virtues and many benefits for individuals and society. The following is a review of the research that shows the married family’s positive influence on individual and societal well-being. Also briefly discussed are some of the negative outcomes generated by non-married families. Research on marriage and the family in the United States demonstrates that many individual and social benefits are rooted in the permanent union of one man with one woman.1 Studies consistently show what Catholic Church teaching has always affirmed, namely, that The well-being of the individual -

Burris, Durbin Call for DADT Repeal by Chuck Colbert Page 14 Momentum to Lift the U.S

THE VOICE OF CHICAGO’S GAY, LESBIAN, BI AND TRANS COMMUNITY SINCE 1985 Mar. 10, 2010 • vol 25 no 23 www.WindyCityMediaGroup.com Burris, Durbin call for DADT repeal BY CHUCK COLBERT page 14 Momentum to lift the U.S. military’s ban on Suzanne openly gay service members got yet another boost last week, this time from top Illinois Dem- Marriage in D.C. Westenhoefer ocrats. Senators Roland W. Burris and Richard J. Durbin signed on as co-sponsors of Sen. Joe Lie- berman’s, I-Conn., bill—the Military Readiness Enhancement Act—calling for and end to the 17-year “Don’t Ask, Don’t Tell” (DADT) policy. Specifically, the bill would bar sexual orien- tation discrimination on current service mem- bers and future recruits. The measure also bans armed forces’ discharges based on sexual ori- entation from the date the law is enacted, at the same time the bill stipulates that soldiers, sailors, airmen, and Coast Guard members previ- ously discharged under the policy be eligible for re-enlistment. “For too long, gay and lesbian service members have been forced to conceal their sexual orien- tation in order to dutifully serve their country,” Burris said March 3. Chicago “With this bill, we will end this discrimina- Takes Off page 16 tory policy that grossly undermines the strength of our fighting men and women at home and abroad.” Repealing DADT, he went on to say in page 4 a press statement, will enable service members to serve “openly and proudly without the threat Turn to page 6 A couple celebrates getting a marriage license in Washington, D.C. -

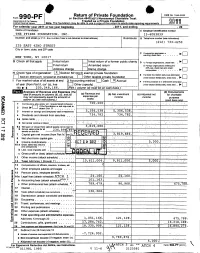

Return of Private Foundation CT' 10 201Z '

Return of Private Foundation OMB No 1545-0052 Form 990 -PF or Section 4947(a)(1) Nonexempt Charitable Trust Department of the Treasury Treated as a Private Foundation Internal Revenue Service Note. The foundation may be able to use a copy of this return to satisfy state reporting requirem M11 For calendar year 20 11 or tax year beainnina . 2011. and ending . 20 Name of foundation A Employer Identification number THE PFIZER FOUNDATION, INC. 13-6083839 Number and street (or P 0 box number If mail is not delivered to street address ) Room/suite B Telephone number (see instructions) (212) 733-4250 235 EAST 42ND STREET City or town, state, and ZIP code q C If exemption application is ► pending, check here • • • • • . NEW YORK, NY 10017 G Check all that apply Initial return Initial return of a former public charity D q 1 . Foreign organizations , check here . ► Final return Amended return 2. Foreign organizations meeting the 85% test, check here and attach Address chang e Name change computation . 10. H Check type of organization' X Section 501( exempt private foundation E If private foundation status was terminated Section 4947 ( a)( 1 ) nonexem pt charitable trust Other taxable p rivate foundation q 19 under section 507(b )( 1)(A) , check here . ► Fair market value of all assets at end J Accounting method Cash X Accrual F If the foundation is in a60-month termination of year (from Part Il, col (c), line Other ( specify ) ---- -- ------ ---------- under section 507(b)(1)(B),check here , q 205, 8, 166. 16) ► $ 04 (Part 1, column (d) must be on cash basis) Analysis of Revenue and Expenses (The (d) Disbursements total of amounts in columns (b), (c), and (d) (a) Revenue and (b) Net investment (c) Adjusted net for charitable may not necessanly equal the amounts in expenses per income income Y books purposes C^7 column (a) (see instructions) .) (cash basis only) I Contribution s odt s, grants etc. -

Annual Report on Charitable Solicitations

COLORADO SECRETARY OF STATE’S OFFICE ANNUAL REPORT ON CHARITABLE SOLICITATIONS 2003 Part 2 Part Two of the 2003 Annual Report provides summary financial information for all charitable organizations that filed financial reports covering any period that ended in 2002. Information believed to be of particular interest to potential donors has been excerpted from the complete financial report for each organization. On the revenue side, only Total Revenue and Contributions are displayed in the report. Each organization’s complete financial report includes additional revenue categories for Government Grants, Program Service Revenue, Investments, Special Events and Activities, Sales, and Other Expenses. On the expense side, the report displays Total Expenses, Program Services Expenses, Administration-Management-General Expenses, and Fundraising Expenses. Each organization’s complete financial report also includes expense categories for Payments to Affiliates and Other Expenses, which are not reflected in this report. The financial information displayed is information that was on file with the Secretary of State’s office as of noon, December 19, 2003. Since financial reports are due by the 15th day of the fifth month following the close of an organization’s fiscal year, the due dates vary. Nevertheless, the last 2002 reports due were those of calendar year organizations, whose accounting periods ended on Dec. 31, 2002. The due date for calendar year organizations was May 15, 2003. Since up to two extensions of the deadline may be requested by a charitable organization (three months each), all 2002 financial reports were due by Nov. 15, 2003, at the latest. For a number of reasons, it is possible that a charitable organization could be registered now, despite not being listed in Part Two of the 2003 Annual Report. -

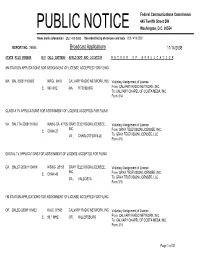

Broadcast Applications 11/14/2008

Federal Communications Commission 445 Twelfth Street SW PUBLIC NOTICE Washington, D.C. 20554 News media information 202 / 418-0500 Recorded listing of releases and texts 202 / 418-2222 REPORT NO. 26863 Broadcast Applications 11/14/2008 STATE FILE NUMBER E/P CALL LETTERS APPLICANT AND LOCATION N A T U R E O F A P P L I C A T I O N AM STATION APPLICATIONS FOR ASSIGNMENT OF LICENSE ACCEPTED FOR FILING MA BAL-20081110AES WFGL 8418 CALVARY RADIO NETWORK, INC. Voluntary Assignment of License E 960 KHZ MA , FITCHBURG From: CALVARY RADIO NETWORK, INC. To: CALVARY CHAPEL OF COSTA MESA, INC. Form 314 CLASS A TV APPLICATIONS FOR ASSIGNMENT OF LICENSE ACCEPTED FOR FILING VA BALTTA-20081110AIX WAHU-CA 47705 GRAY TELEVISION LICENSEE, Voluntary Assignment of License INC. E CHAN-27 From: GRAY TELEVISION LICENSEE, INC. VA , CHARLOTTESVILLE To: GRAY TELEVISION LICENSEE, LLC Form 316 DIGITAL TV APPLICATIONS FOR ASSIGNMENT OF LICENSE ACCEPTED FOR FILING GA BALCT-20081110AHX WSWG 28155 GRAY TELEVISION LICENSEE, Voluntary Assignment of License INC. E CHAN-43 From: GRAY TELEVISION LICENSEE, INC. GA , VALDOSTA To: GRAY TELEVISION LICENSEE, LLC Form 316 FM STATION APPLICATIONS FOR ASSIGNMENT OF LICENSE ACCEPTED FOR FILING OR BALED-20081110AEI KAJC 91565 CALVARY RADIO NETWORK, INC. Voluntary Assignment of License E 90.1 MHZ OR , MILLERSBURG From: CALVARY RADIO NETWORK, INC. To: CALVARY CHAPEL OF COSTA MESA, INC. Form 314 Page 1 of 32 Federal Communications Commission 445 Twelfth Street SW PUBLIC NOTICE Washington, D.C. 20554 News media information 202 / 418-0500 Recorded listing of releases and texts 202 / 418-2222 REPORT NO. -

Asenka Creative Services

Volume XII | Issue I | Winter 2013 the IVY LEAGUE CHRISTIAN OBSERVER Imani Jubilee’s Worship Tradition at Brown Page 7 Yale Discriminates Against Christian Fraternity Page 8 Evangelism Weekend at Cornell Page 11 Penn Students ‘Engage’ Philadelphia Page 12 Lecture at Columbia: The Sacred Call to Study Page 14 Following Tragedy, Harvard MARRIAGE 101 Journal Asks ‘Why?’ Roland Warren, Princeton ’83 and Wharton MBA ’86, Page 16 spoke on the virtues of covenantal marriage at the Sexuality, Integrity, and the University Dartmouth Freshman Serves Conference at Princeton University. God and Country Special section, pages 18-24 Page 27 Brown I Columbia I Cornell I Dartmouth Harvard I Penn I Princeton I Yale Developing Christian Leaders to Transform Culture The Ivy League Christian Observer is published by the Christian Union, an independent Christian ministry. PRAY WITH US FOR THE DEVELOPMENT OF CHRISTIAN LEADERS WHO WILL TRANSFORM CULTURE At Christian Union, we are prayerfully seeking God for transformation at Brown, Columbia, Cornell, Dartmouth, Harvard, Penn, Princeton, and Yale. Each year, thousands of students pass through the halls of these institutions and move out into positions of leadership in our society. Unfortunately, over 90% have had no regular Christian influence in their lives during these critical college years. Christian Union sends out monthly, campus- specific e-mails that describe the needs of the ministry. E-mails are available for Columbia, Cornell, Dartmouth, Harvard, Princeton, and Yale. Will you join us and pray regularly for the development of Christian leaders at some of our nation’s leading universities? To receive Christian Union’s prayer e-mail each month, sign up online at www.Christian-Union.org/prayer or send an e-mail to: [email protected] . -

Shabbat Bulletin May 18

Shabbos Bulletin Welcome to Nusach Hari B’nai Zion Affiliated with Union of Orthodox Congregations of America May 18, 2019 ~ 13 Iyar 5779 Candle Lighting 7:49 pm Shabbat Ends 8:53 pm Torah Portion: Parshas Emor Leviticus 21:1 - 24:23 Chumash pages 672-695 Haftorah: Ezekiel 44: 15-31 Chumash pages 1176-1177 ~ Welcome Rabbi Kasriel & Rebbetzin Pessie Gewirtzman ~ Erev Shabbos, May 17 Mincha & Ma’ariv ~ 7:00 pm Shabbos, May 18 Shabbat Services ~ 9:00 am - Pesukei D’Zimra: Howard Sandler - Haftorah: Bruce Waxman - Shacharis: Mateo John - Drasha: No Drasha - Leyning: Moshe Leib Cohen - Musaf: Alan Haber Learners’ Service ~ Led by Rabbi Yosef David ~ 9:30 am Starting Points ~ Led by Rabbi Ze’ev Smason ~10:15 am ~ Topic: “Common Mistakes Smart People Make” Garden of Eden Speaker Series ~ 11:15 am -12:15 pm ~ Speakers and Topics: Rabbi Kasriel Gewirtzman (visiting from Israel) - “Friendship” Rebbetzin Mimi David – “Modesty” (Women Only) Tot Shabbat and Junior Congregation with Bnot Sherut ~ 10:00 am Pre- Mincha Shuir ~ 6:45 pm ~ Rabbi Gewirtzman will speak on “Judging Favorably: Favor or Obligation?” Mincha / Ma’ariv / Shalosh Seudos ~ 7:35 pm ~ Rabbi Gewirtzman’s topic will be “Emor and Omer: Making Your Days Count.” This Week and Beyond…. Shabbos Sun. Mon. Tues. Wed. Thurs. Fri. Shabbos Minyan Times May 18 May 19 May 20 May 21 May 22 May 23 May 24 May 25 Shachris 9:00 am 8:00 am 7:00 am 7:00 am 7:00 am 7:00 am 7:00 am 9:00 am Mincha/Ma’ariv 7:35 pm 7:00 pm 7:00 pm 7:00 pm 7:00 pm 7:00 pm 7:00 pm 7:40 pm Morning Blessings and the first Kaddish are started five minutes prior to Shachris.