Profiles in Innovation: Factory of the Future—Beyond the Assembly Line" Originally Published April 13, 2016 [83Pgs]

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WML- 30## User Manual (System Model: VI) the Purpose of This Manual Is to Explain Correct Way How to Integrate Module WML- 30## to the End Product

Page 1 of 10 WML-C30_User_Manual 25th Oct 2004 WML- 30## User Manual (system model: VI) The purpose of this manual is to explain correct way how to integrate module WML- 30## to the end product. It includes procedures that shall assist you to avoid unforeseen problems. This manual presents information that shows how module and OEM product, where module integrated, complies with regulations in certain regions. Any modifications, not expressly approved by the manufacturer could void the authority to operate in these regions. Content 1.General 2. Module design application. 3. Regulatory and Safety Compliance. European Union. 3.1 Declaration about performed tests. 3.2. Labelling 4. FCC Regulatory Information 4.1 Labelling. 4.2 Antenna implementation notes. 5. Other regulatory notes for OEM. 6. A separate approval. 1. General This Bluetooth radio module has to be installed and used in accordance with the technical description/installation instructions provided by the manufacturer. This Bluetooth radio module is intended to be placed on the market in all States, where the Bluetooth™ technology and the used frequency band is released. For detail information concerning type approval of this module (e.g. where this module is already pre-approved) please contact the authorised local distributor or the manufacturer. The system may only be implemented in the configuration that was authorized. Note that any changes or modifications to this equipment not expressly approved by the manufacturer could void the user’s authority to operate this equipment. COMMERCIAL IN CONFIDENCE This material may not in whole or part be copied, stored electronically or communicated to third parties without MITSUMI ELECTRIC CO., LTD’s prior agreement in writing. -

Integrated Report (Year Ended March 2019)

Introduction/ Chapter I Chapter II Chapter III Chapter IV President’s message Value Creation Story of MinebeaMitsumi Financial Strategy and Capital Policy Initiatives for Value Creation Initiatives to Support Value Creation 1986 2010 Hamamatsu Plant is established Suzhou Plant is established to expand Development in the electronic devices production of LED backlights Chapter I Value Creation Story of MinebeaMitsumi and components area is expanded History of MinebeaMitsumi Backlights Suzhou Plant (China) FDDs and MODs 2018 Global development ahead of other Hamamatsu Plant (Japan) Kosice Plant in Slovakia commences 2010 1988 production Our plant is established in Cambodia, and Lop Buri Plant is established in Thailand Supply to Europe market is commences production the next year Production in expanded companies For risk diversification, expansion of the electronic production and reduction of costs devices and components Cambodia Plant Speedy diversification through M&As area is expanded 1980 1963 Lop Buri Plant (Thailand) Ayutthaya Plant is AGA (Active Grill Plant is relocated from Kawaguchi, Saitama, and operations 1994 established 1984 Kosice Plant (Slovakia) Shutter) Actuators begin at the Karuizawa Plant, to become the mother The Company Bang Pa-in Plant is Minebea Electronics & plant of all the MinebeaMitsumi Group’s plants advances for the first established as the second Hi-Tech Components , in Miyota-machi, Nagano worldwide time into Thailand, the (Shanghai) Ltd. (our facility in Thailand Resonant devices Group’s largest first plant -

第 1 頁,共 5 頁 Hdmi :: ?喃? :: ? 熙? ?蝏 ? 2005/7/19

HDMI :: ?喃? :: ? 熙? ?蝏 ? 第 1 頁,共 5 頁 HDMI 组织 Hitachi, Ltd. Matsushita Electric Industrial Co., Ltd. (Panasonic) Sony Corporation Philips Consumer Electronics International B.V. Thomson, Inc. Silicon Image, Inc. Toshiba Corporation HDMI 许可采纳者 Last Updated on 7/18/2005 2Wire Inc Krell Industries 3S Digital Co Ltd Leader Electronics Corp. 690885 Ontario Inc. LeCroy Japan Corporation A&R Cambridge Ltd (Arcam) LG Electronics Advanced-Connectek Inc. Linktec Technologies Co Ltd Advanced Display Lab Inc. Linn Products Ltd Advanced Knowledge Associates Lin Shiung Enterprise Co Ltd Agilent Technologies Inc. Lite-On Corporation Akai Electric Co Ltd Loewe Opta GmbH Alco Digital Devices Limited Longwell Company Algolith Inc. LPS Device Co Ltd ALI Corporation Main Super Enterprises Co. Amoi Electronics Co Ltd Marshall Electronics AmTran Technology Master Co. LTD-Korea Analog Devices, Inc. Master Hill Electric Wire & Cable Analogix Semiconductor Inc MediaTek Corp. Anam Electronics Co Ltd Meridian Audio Limited Anchor Bay Technologies Metz-Werke GmbH & Co KG Asahi Kasei Microsystems Co Ltd Micronas GmbH http://cn.hdmi.org/about/adopters_founders.asp 2005/7/19 HDMI :: ?喃? :: ? 熙? ?蝏 ? 第 2 頁,共 5 頁 AstroDesign Inc. MIK21 Co., Ltd Asustek Computer Inc Y-S Electronic Co., Ltd ATI Technologies, Inc. Mitac Technology Corp Audio Partnership PLC Mitsubishi Electric Corporation Audio-Technica Corporation Mitsumi Electric Co., Ltd. Aurora Multimedia Corp Molex Incorporated Avid Technology Inc. Morning Star Industrial BAFO Technologies/TWN 1st Line Elect Cor Motorola, Inc. Bang & Olufsen MSL Enterprises Corp BBK AV Electronics Corp Ltd. Mstar Semiconductor, Inc. BenQ Corporation Murata Manufacturing Co.,Ltd. Beko Elektronik A.S. -

Proposal of a Data Processing Guideline for Realizing Automatic Measurement Process with General Geometrical Tolerances and Contactless Laser Scanning

Proposal of a data processing guideline for realizing automatic measurement process with general geometrical tolerances and contactless laser scanning 2018/4/4 Atsuto Soma Hiromasa Suzuki Toshiaki Takahashi Copyright (c)2014, Japan Electronics and Information Technology Industries Association, All rights reserved. 1 Contents • Introduction of the Project • Problem Statements • Proposed Solution – Proposal of New General Geometric Tolerance (GGT) – Data Processing Guidelines for point cloud • Next Steps Copyright (c)2014, Japan Electronics and Information Technology Industries Association, All rights reserved. 2 Contents • Introduction of the Project • Problem Statements • Proposed Solution – Proposal of New General Geometric Tolerance (GGT) – Data Processing Guidelines for Point Cloud • Next Steps Copyright (c)2014, Japan Electronics and Information Technology Industries Association, All rights reserved. 3 Introduction of JEITA What is JEITA? The objective of the Japan Electronics and Information Technology Industries Association (JEITA) is to promote healthy manufacturing, international trade and consumption of electronics products and components in order to contribute to the overall development of the electronics and information technology (IT) industries, and thereby to promote further Japan's economic development and cultural prosperity. JEITA’s Policy and Strategy Board > Number of full members: 279> Number of associate members: 117(as of May 13, 2014) - Director companies and chair/subchair companies - Policy director companies (alphabetical) Fujitsu Limited (chairman Masami Yamamoto) Asahi Glass Co., Ltd. Nichicon Corporation Sharp Corporation Azbil Corporation IBM Japan, Ltd. Hitachi, Ltd. Advantest Corporation Nippon Chemi-Con Corporation Panasonic Corporation Ikegami Tsushinki Co., Ltd. Japan Aviation Electronics Industry, Ltd. SMK Corporation Mitsubishi Electric Corporation Nihon Kohden Corporation Omron Corporation NEC Corporation JRC Nihon Musen Kyocera Corporation Sony Corporation Hitachi Metals, Ltd KOA Corporation Fuji Xerox Co., Ltd. -

USB 3.0 Adopters.Pdf

Adopting Party Name 3eYamaichi Electronics Co., Ltd. Aces Electronics Co., Ltd. ACES Electronics Co., Ltd. Action Star Enterprise Co., Ltd. Advanced‐Connectek Inc., Acon Agilent Technologies Inc. ALLTOP TECHNOLOGY CO., LTD. Amco Tec International Inc. American Megatrends, Inc. Amphenol Assemble Tech (Xiamen) Co., Ltd. Amphenol ShouhMin Industry (Shenzhen) Co., Ltd. Argosy Research Inc. Astron International Corp. Basler AG Bose Corporation Buffalo Inc. Buffalo Kokuyo Supply Inc. Cambridge Silicon Radio Limited Canon Inc. Chant Sincere Co., Ltd. Cheng Uei Precision Industry Co., Ltd. Chicony Electronics Co., Ltd. Chief Land Electronic Co., Ltd. China Electronics Technology Limited Chrontel, Inc. Circuit Assembly Corp. CNPLUS Co., Ltd. Compupack Technology Co. Ltd. Connect County Holdings Berhad DataFab Systems Inc. Digital Design Corporation Digital Information Technology Studies (ShenZhen) Ltd. DisplayLink (UK) Ltd DongGuan HYX Industrial Co., Ltd. Dongguan Kechenda Electronics Technology Co., Ltd. Dongguan Teconn Electronics Technology Co., Ltd. Dongguan Yuqin Electronics Co., Ltd. EchoStar Technologies, LLC Elektrobit, Inc. FCI USA LLC Foosung Tech Foxconn Interconnect Technology, Ltd ("FIT LTD") Freeport Resources Enterprises Corp. Fujitsu Limited Full in Hope Co., Ltd. Global Connector Technology Ltd. (GCT) Global Unichip Corp. Goodway Technology Co., Ltd. Harris Corporation Hewlett Packard High‐Top Precision Electronic Co., Ltd. Hirose Electric Co., Ltd. Hosiden Corporation Hsi Chin Electronics Co., Ltd. IBM Corporation ICT‐Lanto Limited I‐PEX USA LLC Integral Memory PLC Intel Corporation Japan Aviation Electronics Industry, Limited Jmicron Technology Corporation Jo‐Dan International Joinsoon Electronic Mfg. Co., Ltd. JPC/Main Super Inc J.S.T. Mfg. Co., Ltd. JVC KENWOOD Holdings, Inc. Kawasaki Microelectronics, Inc. Kycon, Inc. KYOCERA MITA Corporation Lenjoy Technology Limited Littelfuse Inc. -

Japan 500 2008 A-Z

FTJapan 500 2008 A-Z Japan rank Company 2008 Abc-Mart 349 Access 451 Acom 199 Advantest 167 Aeon 87 Aeon Credit Service 333 Aeon Mall 172 Aiful 282 Aioi Insurance 202 Air Water 377 Aisin Seiki 76 Ajinomoto 122 Alfresa 246 All Nippon Airways 99 Alps Electric 373 Amada 260 Aoyama Trading 430 Aozora Bank 177 Aruze 296 Asahi Breweries 85 Asahi Glass 57 Asahi Kasei 116 Asatsu-DK 404 Asics 309 Astellas Pharma 36 Awa Bank 459 Bank of Iwate 480 Bank of Kyoto 196 Bank of Nagoya 474 Bank of Yokohama 88 Benesse 175 Bosch 363 Bridgestone 54 Brother Industries 273 Canon 6 Canon Sales 274 Capcom 315 Casio Computer 209 Central Japan Railway 31 Chiba Bank 138 Chiyoda 381 Chubu Electric Power 39 Chugai Pharmaceuticals 132 Chugoku Bank 243 Chugoku Electric Power 104 Circle K Sunkus 432 Citizen Watch 253 Coca-Cola West Japan 285 Comsys 478 Cosmo Oil 287 Credit Saison 170 CSK 364 Dai Nippon Printing 73 Daicel Chemical Industries 358 Daido Steel 319 Daifuku 436 Daihatsu Motor 169 Daiichi Chuo Kisen 357 Daiichi Sankyo 34 Daikin Industries 60 Dainippon Sumitomo Pharma 225 Daiseki 458 Daishi Bank 442 Daito Trust Construction 125 Daiwa House Industry 143 Daiwa Securities Group 65 Davinci Advisors 495 Dena 259 Denki Kagaku Kogyo 415 Denso 24 Dentsu 130 Diamond Lease 276 DIC 297 Disco 433 Don Quijote 469 Dowa Mining 367 East Japan Railway 20 Ebara 473 Eisai 83 Electric Power Development 139 Elpida Memory 197 Exedy 453 Ezaki Glico 371 Familymart 231 Fanuc 32 Fast Retailing 89 Fuji Electric 261 Fuji Fire & Marine Insurance 479 Fuji Heavy Industries 247 Fuji Photo -

UNO Template

31 October 2014 Asia Pacific/Japan Equity Research Product Marketing Japan Monthly Highlights Research Analysts MONTHLY Daisuke Takato 813 4550 9671 [email protected] October 2014 ■ Tighter automobile emission standards around the globe will put the spotlight on Japanese component manufacturers such as Denso (6902), NGK Insulators (5333), and NGK Spark Plug (5334). In this Connection Series collaboration between analysts Masahiro Akita, Akinori Kanemoto and Jun Yamaguchi, we look at technology trends, competitive conditions, and market growth potential for filters, valves, spark plugs, exhaust gas sensors, and other products. ■ Hitoshi Hayakawa reinstated coverage of Softbank (9984) with an OUTPERFORM rating and ¥10,000 target price following Asia internet analyst Dick Wei's initiation of Alibaba (OUTPERFORM, TP $114). Hayakawa points out that the market is undervaluing Softbank's investment securities and existing business and has not priced in annual FCF in excess of ¥1tn. ■ Analyst Masashi Mori continued to expand his coverage, adding Sanrio (8136), Japan Tobacco (2914), and Calbee (2229). He rates Hello Kitty franchise owner Sanrio OUTPERFORM as he sees earnings rebounding next fiscal year. Japan Tobacco continues to deliver steady earnings by offsetting volume declines with price increases – he also rates the stock OUTPERFORM. He initated coverage of Calbee with a NEUTRAL rating as he believes the snack-food maker needs a stronger overseas growth strategy to complement its dominant position in the domestic market. Separately, in the diaper market, Uncharm (8113) is struggling in China’s online diaper market, while Kao (4452) is gaining share, according to channel checks. ■ The Japanese market is now trading at just under 1x HOLT net assets following recent strong performance. -

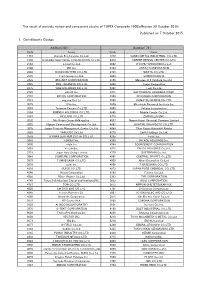

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

China's Tech Sector

SYNC. Global investment themes: technology, media and telecoms Issue No. 141 China’s Tech Sector 5 December 2016 The China Syndrome China’s government is intent on upgrading its manufacturing sector and Inside leading the world in a range of advanced technologies. Implicit in its “Made . Players in China 2025” 10-year plan is the notion that China will displace the US as . Trends the world’s dominant technological power. Value Chain . Industry analysis When we last looked at this issue, back in August 2015 (see “Tech Wars - Electric vehicles 2020: China vs US”), we concluded that the US was likely to remain a - Shared transport leader in all major advanced technologies over the next decade, with Baidu - Robotics the only Chinese player equipped to challenge the US’s lead in next - Consumer electronics generation technologies such as AI. Eighteen months on, the signs are that - Semiconductors China is closing the overall gap faster than we expected. - High perf. computing - Artificial intelligence Conclusions - Internet platforms This report researches the state and thrust of Chinese technology over the - Cloud infrastructure next two to five years and what it implies for global technology investors. - Genomics Here is what we found: . China Tech Scorecard - Who’s who . Electric vehicles: BYD (Hold) is the Chinese market leader, but - Thematic Screen competition from Alibaba, Baidu, Tencent and LeEco will disrupt things. - Valuation Screen - Risk Screen . Robotics: HollySys (Buy), Estun (Avoid) and Siasun (Avoid) are the . Stock Watch List domestic leaders, but best to play this theme via the Japanese parts . Private companies makers: Harmonic Drive, Keyence, Nachi-Fujikoshi, Omron and Daihen. -

1951 7 Nippon Miniature Bearing Co., Ltd., Japan's

A History of Achievements Nippon Miniature Bearing Co., Ltd., Japan’s Manufacturing subsidiary NMB Thai Limited 1951 7 first specialized manufacturer of miniature 8 (the present NMB-Minebea Thai Ltd.) is ball bearings, is incorporated in Azusawa, estab lished in Thailand. (Production begins Itabashi-ku, Tokyo. in 1982.) The Company relocates its headquarters to The marketing division of the Company is spun 1956 10 Nihonbashi-Kabuto-cho, Chuo-ku, Tokyo, and 1981 1 off as subsidiary NMB (Japan) Corporation, its factory to Kami Aoki-cho, Kawaguchi, which is charged with integrating marketing Saitama. operations for all manufacturing companies in A new plant is established at Aoki-cho, the Minebea Group. 1959 6 Kawaguchi, Saitama, to serve as the The Company absorbs four of its manufacturing Company’s integrated headquarters 10 affiliates—Tokyo Screw Co., Ltd., Shinko and factory. Communication Industry Co., Ltd., Shin Chuo The Company’s stock is listed on the over-the- Kogyo Co., Ltd., and Osaka Motor Wheel Co., 1961 8 counter market of the Tokyo Stock Exchange. Ltd.—and changes its name to Minebea Co., Ltd. With the establishment of the Second Section 1982 9 Sales subsidiary NMB Italia S.r.l. is established 10 of the Tokyo Stock Exchange, the company’s in Italy. stock is listed on this section. 1983 3 The Company acquires a cooling fan manufac- A representative office is set up in the turer, Kondo Electric Works Ltd. (the present 1962 11 United States to cultivate the U.S. market. Industrial Machinery BU). A plant is established in Karuizawa, Nagano. 1984 8 Two manufacturing subsidiaries, Minebea Thai 1963 3 Some operations are relocated to the Limited and Pelmec Thai Ltd. -

Trading Patterns and Excess Comovement of Stock Returns Author(S): Robin M

Trading Patterns and Excess Comovement of Stock Returns Author(s): Robin M. Greenwood and Nathan Sosner Source: Financial Analysts Journal , Sep. - Oct., 2007, Vol. 63, No. 5 (Sep. - Oct., 2007), pp. 69-81 Published by: Taylor & Francis, Ltd. Stable URL: https://www.jstor.org/stable/4480877 JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range of content in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new forms of scholarship. For more information about JSTOR, please contact [email protected]. Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at https://about.jstor.org/terms Taylor & Francis, Ltd. is collaborating with JSTOR to digitize, preserve and extend access to Financial Analysts Journal This content downloaded from 206.253.207.235 on Thu, 03 Dec 2020 18:55:42 UTC All use subject to https://about.jstor.org/terms Financial Analysts Jou rnal Volume 63 . Number 5 FM ?2007, CFA Institute Trading Patterns and Excess Comovement of Stock Returns Robin M. Greenwood and Nathan Sosner In April 2000, 30 stocks were replaced in the Nikkei 225 Index. The unusually broad index redefinition allowedfor a study of the effects of index-linked trading on the excess comovement of stock returns. A large increase occurred in the correlation of trading volume of stocks added to the index with the volume of stocks that remained in the index, and opposite results occurredfor the deletions. Daily index return betas of the additions rose by an average of 0.45; index return betas of the deleted stocksfell by an average of 0. -

YRP R&D Promotion Committee Members

YRP R&D Promotion Committee Members Total 127 members as of July 1, 2021 Aeterlink, INC. J・P・SYSTEMS CORPORATION ALPHA SYSTEMS INC. Japan Broadcasting Corporation Association of Radio Industries and Businesses Japan Cable and Telecommunicaitions Association Canon Inc. Kanto Bureau of Telecommunications Central Corridor Communications 21 Kawamoto Industry Corporation Central Research Institute of Electric Power Industry KDDI CORPORATION Communications and Information network Association of Japan KDDI Research, Inc. Dai Nippon Printing Co., Ltd. KEIKYU AD ENTERPRISE Co.,Ltd. DAIFUKU Co., Ltd. Keikyu Construction Corporation Denki Kogyo Company, Limited Keikyu Corporation DENSO CORPORATION KEIKYU Department Store Co. Development Bank of Japan Inc. KEIKYU ELECTRIC ENGINEERING Co., Ltd. DOCOMO Technology, Inc. KEIKYU REAL ESTATE Co., Ltd. DOI Norihisa Keikyu Service Co., Ltd. Eiden Co.,Ltd. KEIKYU STORE Co., ltd. EJK Japan, Ltd. Keikyu System Co., Ltd. ExH Corporation Kumagai Gumi Co.,Ltd. Flexible Factory Partner Alliance KYOCERA Corporation Energous Corporation Leonix Co.,Ltd FUGONO Nobuyoshi MABUCHI CONSTRUCTION CO.,LTD. FUJITSU LIMITED Marubun Corporation FURUKAWA ELECTRIC CO.,LTD. Minebea Mitsumi Inc. HATORI Mitsutoshi Ministry of Internal Affairs and Communications Hitachi Kokusai Electric Inc. MIROKU JYOHO SERVICE CO., LTD. Hitachi, Ltd. Mitsubishi Electric Corporation Hitachi-LG Data Storage, Inc. MITSUBISHI ELECTRIC ENGINEERING COMPANY LIMITED Honda Motor Co., Ltd. MITSUMI ELECTRIC CO., LTD. Information Task Force Co.,Ltd. MOTAI Akio ION Enterprise Inc. National Institute of Information and Communications Technology J・P・SYSTEMS CORPORATION NEC Corporation Japan Broadcasting Corporation NGK INSULATORS, LTD. Japan Cable and Telecommunicaitions Association NHK Technologies, Inc. Japan Cable Laboratories Nifco Inc Nihon Meccs Co.,Ltd. TAISEI CORPORATION NIPPON ANTENNA Co.,Ltd.