WIL Car Wheels Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Japanese Manufacturing Affiliates in Europe and Turkey

06-ORD 70H-002AA 7 Japanese Manufacturing Affiliates in Europe and Turkey - 2005 Survey - September 2006 Japan External Trade Organization (JETRO) Preface The survey on “Japanese manufacturing affiliates in Europe and Turkey” has been conducted 22 times since the first survey in 1983*. The latest survey, carried out from January 2006 to February 2006 targeting 16 countries in Western Europe, 8 countries in Central and Eastern Europe, and Turkey, focused on business trends and future prospects in each country, procurement of materials, production, sales, and management problems, effects of EU environmental regulations, etc. The survey revealed that as of the end of 2005 there were a total of 1,008 Japanese manufacturing affiliates operating in the surveyed region --- 818 in Western Europe, 174 in Central and Eastern Europe, and 16 in Turkey. Of this total, 291 affiliates --- 284 in Western Europe, 6 in Central and Eastern Europe, and 1 in Turkey --- also operate R & D or design centers. Also, the number of Japanese affiliates who operate only R & D or design centers in the surveyed region (no manufacturing operations) totaled 129 affiliates --- 125 in Western Europe and 4 in Central and Eastern Europe. In this survey we put emphasis on the effects of EU environmental regulations on Japanese manufacturing affiliates. We would like to express our great appreciation to the affiliates concerned for their kind cooperation, which have enabled us over the years to constantly improve the survey and report on the results. We hope that the affiliates and those who are interested in business development in Europe and/or Turkey will find this report useful. -

Creating “Satisfaction in Life” – the Work of the Topy Industries Group

Technology and quality flowing together in one perfect motion 2015 Creating “Satisfaction in Life” Technology and quality – the work of the Topy Industries Group flowing together in one perfect motion The Topy Industries Group plays an active role in various aspects of one’s life and society. It is our mission to create new value that lead to “Satisfaction in Life” through a wide range of business activities from At the Topy Industries Group, we use the phrase “One-piece Cycle” to describe making steel material – the foundation of society – to producing automobiles and industrial machinery components, our approach to building a richer, prosperous society. Our Group’s most distinctive quality is our integrated production system, which covers everything from raw materi- generating and distributing electric power, and sports / leisure businesses. als to finished products. The know-how cultivated by each of our many business divi- sions is shared throughout the Group, enabling us to develop technologies with great- We have an integrated production system from raw materials to finished products, which assures the manufacture of er ingenuity and to make products with greater added-value. From design to production, from raw materials to finished products, we at Topy Industries conglomer- high value-added products that meet the various needs of industries. ate are committed to working alongside other Topy Industries Group companies and the society that uses our products to create new ways of doing business. We have a flexible world-wide manufacturing network. By making the most of these strengths we continue to deliver technologies and products to make our society more livable, comfortable, and contribute to the global environment. -

Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone?

IRLE IRLE WORKING PAPER #188-09 September 2009 Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone? James R. Lincoln, Masahiro Shimotani Cite as: James R. Lincoln, Masahiro Shimotani. (2009). “Whither the Keiretsu, Japan's Business Networks? How Were They Structured? What Did They Do? Why Are They Gone?” IRLE Working Paper No. 188-09. http://irle.berkeley.edu/workingpapers/188-09.pdf irle.berkeley.edu/workingpapers Institute for Research on Labor and Employment Institute for Research on Labor and Employment Working Paper Series (University of California, Berkeley) Year Paper iirwps-- Whither the Keiretsu, Japan’s Business Networks? How Were They Structured? What Did They Do? Why Are They Gone? James R. Lincoln Masahiro Shimotani University of California, Berkeley Fukui Prefectural University This paper is posted at the eScholarship Repository, University of California. http://repositories.cdlib.org/iir/iirwps/iirwps-188-09 Copyright c 2009 by the authors. WHITHER THE KEIRETSU, JAPAN’S BUSINESS NETWORKS? How were they structured? What did they do? Why are they gone? James R. Lincoln Walter A. Haas School of Business University of California, Berkeley Berkeley, CA 94720 USA ([email protected]) Masahiro Shimotani Faculty of Economics Fukui Prefectural University Fukui City, Japan ([email protected]) 1 INTRODUCTION The title of this volume and the papers that fill it concern business “groups,” a term suggesting an identifiable collection of actors (here, firms) within a clear-cut boundary. The Japanese keiretsu have been described in similar terms, yet compared to business groups in other countries the postwar keiretsu warrant the “group” label least. -

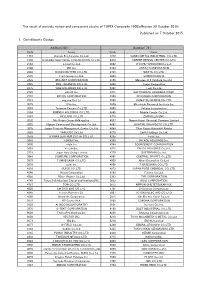

Published on 7 October 2016 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2016) Published on 7 October 2016 1. Constituents Change Addition( 70 ) Deletion( 60 ) Code Issue Code Issue 1810 MATSUI CONSTRUCTION CO.,LTD. 1868 Mitsui Home Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2196 ESCRIT INC. 2117 Nissin Sugar Co.,Ltd. 2198 IKK Inc. 2124 JAC Recruitment Co.,Ltd. 2418 TSUKADA GLOBAL HOLDINGS Inc. 2170 Link and Motivation Inc. 3079 DVx Inc. 2337 Ichigo Inc. 3093 Treasure Factory Co.,LTD. 2359 CORE CORPORATION 3194 KIRINDO HOLDINGS CO.,LTD. 2429 WORLD HOLDINGS CO.,LTD. 3205 DAIDOH LIMITED 2462 J-COM Holdings Co.,Ltd. 3667 enish,inc. 2485 TEAR Corporation 3834 ASAHI Net,Inc. 2492 Infomart Corporation 3946 TOMOKU CO.,LTD. 2915 KENKO Mayonnaise Co.,Ltd. 4221 Okura Industrial Co.,Ltd. 3179 Syuppin Co.,Ltd. 4238 Miraial Co.,Ltd. 3193 Torikizoku co.,ltd. 4331 TAKE AND GIVE. NEEDS Co.,Ltd. 3196 HOTLAND Co.,Ltd. 4406 New Japan Chemical Co.,Ltd. 3199 Watahan & Co.,Ltd. 4538 Fuso Pharmaceutical Industries,Ltd. 3244 Samty Co.,Ltd. 4550 Nissui Pharmaceutical Co.,Ltd. 3250 A.D.Works Co.,Ltd. 4636 T&K TOKA CO.,LTD. 3543 KOMEDA Holdings Co.,Ltd. 4651 SANIX INCORPORATED 3636 Mitsubishi Research Institute,Inc. 4809 Paraca Inc. 3654 HITO-Communications,Inc. 5204 ISHIZUKA GLASS CO.,LTD. 3666 TECNOS JAPAN INCORPORATED 5998 Advanex Inc. 3678 MEDIA DO Co.,Ltd. 6203 Howa Machinery,Ltd. 3688 VOYAGE GROUP,INC. 6319 SNT CORPORATION 3694 OPTiM CORPORATION 6362 Ishii Iron Works Co.,Ltd. 3724 VeriServe Corporation 6373 DAIDO KOGYO CO.,LTD. 3765 GungHo Online Entertainment,Inc. -

TOYOTA Toyota Motor North America, Inc

TOYOTA Toyota Motor North America, Inc. Vehicle Safety & Compliance Liaison Office Mail Stop: W4-2D 6565 Headquarters Drive Plano, TX 75024 February 27, 2019 DEFECT INFORMATION REPORT 1. Vehicle Manufacturer Name: Toyota Motor Corporation [“TMC”] 1, Toyota-cho, Toyota-city, Aichi-pref., 471-8571, Japan Affiliated U.S. Sales Company: Toyota Motor North America, Inc. [“TMNA”] 6565 Headquarters Drive, Plano, TX 75024 Assembler of run-flat tire to wheel: Topy Industries, Ltd. 1-2-2 Osaki, Shinagawa-ku, Tokyo, 141-8634, Japan Telephone: +81-3-3493-0777 Country of Origin: Japan 2. Identification of Involved Vehicles: Make/Car Line Model Year Manufacturer Production Period February 21, 2017 Lexus / LS 2018 TMC through July 20, 2018 Applicability Part Number Part Name Component Description 42600-5AG80 42600-5AM80 42600-5AJ50 42600-5AN10 MY2018 42600-5A410 Wheel Assy Wheel with run-flat tire Lexus LS 42600-5AN40 42600-5AL20 42600-5AL30 42600-5AM20 42600-5AM30 42600-5AM40 42600-5AM50 42600-5AM60 42600-5AM70 42600-5AM90 42600-5AN00 42600-5AN20 42600-5AN30 42600-5AQ20 NOTE: (1) Although the involved vehicles are within the above production period, not all vehicles in this range were sold in the U.S. (2) This issue only affects vehicles which are equipped with certain run-flat tires from a specific tire supplier, assembled to wheels by another supplier using a specific assembly process. Other Toyota or Lexus vehicles sold in the U.S. are not equipped with those run-flat tires. 3. Total Number of Vehicles Potentially Involved: 6,296 4. Percentage of Vehicles Estimated to Actually Contain the Defect: Based on results from non-representative inspections of 1,236 run-flat tires during the investigation, Toyota estimates that approximately 5% of the involved vehicles may have the cracked condition in the tire sidewall described in this document. -

Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017

Report of Activities Pursuant to Act 44 of 2010 Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017 Appendix D: Securities Held by Funds The Four Funds hold thousands of publicly and privately traded securities. Act 44 directs the Four Funds to publish “a list of all publicly traded securities held by the public fund.” For consistency in presenting the data, a list of all holdings of the Four Funds is obtained from Pennsylvania Treasury Department. The list includes privately held securities. Some privately held securities lacked certain data fields to facilitate removal from the list. To avoid incomplete removal of privately held securities or erroneous removal of publicly traded securities from the list, the Four Funds have chosen to report all publicly and privately traded securities. The list below presents the securities held by the Four Funds as of June 30, 2017. 1345 AVENUE OF THE A 1 A3 144A AAREAL BANK AG ABRY MEZZANINE PARTNERS LP 1721 N FRONT STREET HOLDINGS AARON'S INC ABRY PARTNERS V LP 1-800-FLOWERS.COM INC AASET 2017-1 TRUST 1A C 144A ABRY PARTNERS VI L P 198 INVERNESS DRIVE WEST ABACUS PROPERTY GROUP ABRY PARTNERS VII L P 1MDB GLOBAL INVESTMENTS L ABAXIS INC ABRY PARTNERS VIII LP REGS ABB CONCISE 6/16 TL ABRY SENIOR EQUITY II LP 1ST SOURCE CORP ABB LTD ABS CAPITAL PARTNERS II LP 200 INVERNESS DRIVE WEST ABBOTT LABORATORIES ABS CAPITAL PARTNERS IV LP 21ST CENTURY FOX AMERICA INC ABBOTT LABORATORIES ABS CAPITAL PARTNERS V LP 21ST CENTURY ONCOLOGY 4/15 -

Topyreport2012en.Pdf

The Topy Industries Group, a challenger At the Topy Industries Group, we use the phrase “One-piece Cycle” to describe to create new values our approach to building a richer, prosperous society. Our Group’s most distinc- tive quality is our integrated production system, which covers everything from in the global business arena raw materials to finished products. The know-how cultivated by each of our many business divisions is shared throughout the Group, enabling us to develop The Topy Industries Group seeks to create new values by boldly taking up chal- Technology and quality fl owing together in one technologies with greater ingenuity and to make products with greater added- lenges from a global perspective. perfect motion Topy has developed its business centered around “iron”, a valuable natural re- value. From design to production, from raw materials to fi nished products, we source on the Earth. at Topy Industries conglomerate are committed to working alongside other the Through years of experience working with and processing iron, we have intimate Topy Industries Group companies and the society that uses our products to cre- knowledge about the characteristics of iron that enable us to discover unimagi- ate new ways of doing business. nable new values. We work beyond borders and continue to contribute to national and regional de- velopment. Topy is fi rmly determined to explore every possibility and address the challenges with uncompromising spirit. The Topy Industries Group has accumu- lated knowledge, experience and resources over its 90 year history and is com- mitted to building a better tomorrow by establishing closer ties with people and Contents corporations, as well as countries and regions all over the world. -

FTSE Developed Asia Pacific All Cap

FTSE Russell Publications 19 August 2018 FTSE Developed Asia Pacific All Cap Indicative Index Weight Data as at Closing on 29 June 2018 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 77 Bank 0.02 JAPAN Anritsu 0.03 JAPAN Azbil Corp. 0.04 JAPAN a2 Milk 0.08 NEW Ansell 0.04 AUSTRALIA Bandai Namco Holdings 0.11 JAPAN ZEALAND Anton Oilfield Services <0.005 HONG KONG Bando Chem Inds 0.01 JAPAN AAC Technologies Holdings 0.14 HONG KONG AOI Electronics <0.005 JAPAN Bank of East Asia 0.07 HONG KONG Abacus Property Group 0.01 AUSTRALIA Aoki Holdings 0.01 JAPAN Bank of Iwate 0.01 JAPAN ABC-Mart 0.02 JAPAN Aomori Bank 0.01 JAPAN Bank of Kyoto 0.05 JAPAN Able C&C <0.005 KOREA Aoyama Trading 0.02 JAPAN Bank of Nagoya 0.01 JAPAN Accent Group 0.01 AUSTRALIA Aozora Bank 0.06 JAPAN Bank of Okinawa 0.01 JAPAN Accordia Golf Trust <0.005 SINGAPORE APA Group 0.12 AUSTRALIA Bank of Queensland Ltd. 0.04 AUSTRALIA Achilles <0.005 JAPAN Aplus Financial <0.005 JAPAN Bank of Ryukyus 0.01 JAPAN Acom 0.02 JAPAN APN Outdoor Group 0.01 AUSTRALIA Bank of Saga <0.005 JAPAN Adastria Holdings <0.005 JAPAN Appen 0.01 AUSTRALIA Bapcor 0.02 AUSTRALIA Adeka 0.02 JAPAN Aprogen Pharmaceuticals <0.005 KOREA Beach Energy 0.03 AUSTRALIA Adelaide Brighton 0.03 AUSTRALIA Arakawa Chemical Industries <0.005 JAPAN Beadell Resources <0.005 AUSTRALIA Advan <0.005 JAPAN Arata 0.01 JAPAN Bega Cheese 0.01 AUSTRALIA Advanced Process Systems <0.005 KOREA ARB Corporation 0.02 AUSTRALIA Beijing Enterprises Medical and Health <0.005 -

2018 the Topy Industries Group Corporate Basic Philosophy

Technology and quality flowing together in one perfect motion T OPY R e p o r t 2 0 1 8 Art Village Osaki Central Tower, 1-2-2, Osaki, Shinagawa-ku, Tokyo, Japan 141-8634 TEL:+81-3-3493-0777 FAX:+81-3-3493-0200 http://www.topy.co.jp/ 2018 The Topy Industries Group Corporate Basic Philosophy Win the trust and respect of society through the continuance and development of the Topy Industries Group and the execution of one’s duty as a public institution. The Topy Industries Group Corporate Code of Conduct − To win the trust and respect of society – Under the Corporate Philosophy, the management and employees of the Topy Industries Group shall strictly abide by all applicable laws and ordinances, the spirit reflected, and the Corporate Code of Conduct, while accepting full corporate social responsibility and fostering an open-minded and creative corporate culture. Contents Editorial Policy / Contents 1 Chapter 1 Knowing Topy 3 Businesses of the Topy Industries Group 3 Top Message 5 History of the Topy Industries Group 11 Strengths of the Topy Industries Group 13 Chapter 2 Topy’s Growth Strategies 15 Progress in the Medium-Term Management Plan 15 Steel Business 17 Automotive and Industrial Machinery Components Business (Wheels) 19 Automotive and Industrial Machinery Components Business (Undercarriage Components for Construction Machinery) 21 Other Businesses 23 Global Expansion of the Topy Industries Group 25 Chapter 3 Topy’s Sustainability Initiatives 27 Sustainability Initiatives of the Topy Industries Group 27 Environmental Initiatives 29 Social Responsibility 36 Chapter 4 Corporate Governance 42 Chapter 5 Corporate Data 46 Reporting Period Editorial Policy Our History 46 Reporting Scope Covers mainly FY2017 (April 1, 2017 to March 31, 2018), but includes This report covers all companies listed as a subsidiary of the Topy Indus- some activities that occurred on and after April 1, 2018. -

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

M Funds Quarterly Holdings 3.31.2020*

M International Equity Fund 31-Mar-20 CUSIP SECURITY NAME SHARES MARKET VALUE % OF TOTAL ASSETS 233203421 DFA Emerging Markets Core Equity P 2,263,150 35,237,238.84 24.59% 712387901 Nestle SA, Registered 22,264 2,294,710.93 1.60% 711038901 Roche Holding AG 4,932 1,603,462.36 1.12% 690064001 Toyota Motor Corp. 22,300 1,342,499.45 0.94% 710306903 Novartis AG, Registered 13,215 1,092,154.20 0.76% 079805909 BP Plc 202,870 863,043.67 0.60% 780087953 Royal Bank of Canada 12,100 749,489.80 0.52% ACI07GG13 Novo Nordisk A/S, Class B 12,082 728,803.67 0.51% B15C55900 Total SA 18,666 723,857.50 0.51% 098952906 AstraZeneca Plc 7,627 681,305.26 0.48% 406141903 LVMH Moet Hennessy Louis Vuitton S 1,684 625,092.87 0.44% 682150008 Sony Corp. 10,500 624,153.63 0.44% B03MLX903 Royal Dutch Shell Plc, Class A 35,072 613,753.12 0.43% 618549901 CSL, Ltd. 3,152 571,782.15 0.40% ACI02GTQ9 ASML Holding NV 2,066 549,061.02 0.38% B4TX8S909 AIA Group, Ltd. 60,200 541,577.35 0.38% 677062903 SoftBank Group Corp. 15,400 539,261.93 0.38% 621503002 Commonwealth Bank of Australia 13,861 523,563.51 0.37% 092528900 GlaxoSmithKline Plc 26,092 489,416.83 0.34% 891160954 Toronto-Dominion Bank (The) 11,126 473,011.14 0.33% B1527V903 Unilever NV 9,584 472,203.46 0.33% 624899902 KDDI Corp. -

Irex2019 Post Show Report

Post Show Report The way towards a friendlier society, bridged by robots Date Dec. 18(Wed.)‒21(Sat.), 2019 Opening hours:10:00 to 17:00 Venue Tokyo Big Sight Aomi Halls, West Halls, South Halls Organizers Japan Robot Association (JARA) THE NIKKAN KOGYO SHIMBUN One of the largest robot trade shows in the world The newest robot technologies and products from Japan and around the world. We are pleased to inform you that thanks to your supports, International Robot Exhibition 2019 (iREX 2019), held from 18th to 21st December, came to an end with great success. The number of exhibiters this year was 637 and the number of booths was 3,060. This marks the largest number ever, breaking the record of previous iREX in 2017. As organizers, we would like to express our deep gratitude to all the exhibitors, related authorities, organizations and associations as this achievement would not be made if it were not for your warm supports. The contents and the brief report on iREX2019 are shown in the following pages for your reference. Thank you very much again, and we sincerely appreciate your continued supports. Japan Robot Association (JARA) THE NIKKAN KOGYO SHIMBUN, LTD. 1 Show Overview ■ Name INTERNATIONAL ROBOT EXHIBITION 2019 (iREX 2019) ■Theme “The way towards a friendlier society, bridged by robots” ■Purpose The purpose of the exhibition is to gather and exhibit industrial/service robots and related equipment from around the globe under one roof, to help improve the technology to use robots and market development, and to contribute to the creation of new markets and promotion of industrial technology of robots.