Royal Caribbean Cruises Ltd. Royal

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Seatec International Maritime Review 2/2014

International Maritime Review The French Connection Finnish companies are actively involved in building Oasis 3 Mein Schiff 3 First TUI cruiser delivered from STX’s Turku shipyard seatec.fi/magazine smm-hamburg.com 53° 33‘ 47“ N, 9° 58‘ hamburg 33“ E keeping the course 9 – 12 september 2014 HAMBURG the leading international maritime trade fair new in 2014: THE3-- THEMEDAYS SEPT fi nance day SEPT environmental protection day SEPT security and defence day SEPT offshore day SEPT recruiting day scan the QR code and view the trailer or visit smm-hamburg.com/trailer DNV GL In the maritime industry DNV GL is the world’s leading classification society and a recognized advisor for the maritime industry. We enhance safety, quality, energy efficiency and environmental performance of the global shipping industry – across all vessel types and offshore structures. We invest heavily in research and development to find solutions, together with the industry, that address strategic, operational or regulatory challenges. SAFER, SMARTER, GREENER editorial seatec 2/2014 COME TOGETHER PUBLISHER The Finnish marine cluster is certainly an interesting industry. Presently, PubliCo Oy it has been reported that the German shipyard Meyer Werft is looking Pälkäneentie 19 A FI-00510 Helsinki to buy the Turku shipyard from its South Korean owner, STX Europe. Finland According to the plans, also the State of the Finland would be involved Phone +358 9 686 6250 [email protected] in a small ownership role, helping to secure the deal. www.publico.com The Finnish marine cluster is finding other ways to cope in a brave new world, too. -

A Qualitative Review of Cruise Service Quality: Case Studies from Asia

sustainability Article A Qualitative Review of Cruise Service Quality: Case Studies from Asia Yeohyun Yoon 1 and Kyoung Cheon Cha 2,* 1 School of Hotel and Tourism Management, Youngsan University, Busan 48015, Korea; [email protected] 2 Department of Business Administration, Dong-A University, Busan 49236, Korea * Correspondence: [email protected] Received: 2 September 2020; Accepted: 29 September 2020; Published: 30 September 2020 Abstract: Although the cruise sector is considered an ‘unreplaceable’ form of tourism, with the cruise industry recording steady growth over the years, there is a lack of research and analysis on cruise ships themselves. Accordingly, this study sought to determine whether service quality differences among ships operating in the Asian market could suggest broader implications for the sustainability of the cruise industry. We chose the SERVQUAL framework for the analysis; we also employed the multiple case study method and topic synthesis to compare the service quality of three ships. Of the ships investigated—the Costa Victoria, Diamond Princess, and Superstar Virgo—the Diamond Princess had the highest service quality. Based on the results, we outlined suggestions for improving the quality of cruise services, including introducing the latest large ships and high-tech facilities, complying with the departure and arrival times of sailing schedules, improving the ratio of crew members per passenger, establishing a cruise personnel training system, and expanding membership program operations. Keywords: cruise; service quality; SERVQUAL; onboard attributes 1. Introduction Cruise tourism is one of the fastest growing tourism segments, and it has undergone significant transformation, especially in the last few decades [1,2]. -

QUANTUM of the SEAS 2020 CHINA ADVENTURES Get Ready for an Immersive Adventure in Asia with China 2020 Sailings Now Ready to Book

QUANTUM OF THE SEAS 2020 CHINA ADVENTURES Get ready for an immersive adventure in Asia with China 2020 sailings now ready to book. Choose from two of our most revolutionary ships — sail from sky scraping Shanghai on Spectrum of the Seas®, the first Quantum Ultra Class ship, and specially tailored for our Chinese guests. Or go bold from Beijing onboard Quantum of the Seas®. And discover Okinawa, Nagasaki, Tokyo and beyond — plus late-night stays in Kobe and Osaka, Japan on select sailings. ITINERARY SAIL DATE PORT OF CALL 5-Night Nagasaki & May 12, 17, 26, 2020 Beijing (Tianjin), China • Cruising • Nagasaki, Fukuoka June 7, 2020 Japan • Fukuoka, Japan • Cruising • Beijing July 19, 2020 (Tianjin), China August 14, 2020 4-Night Best of Fukuoka May 22, 2020 Beijing (Tianjin), China • Cruising • Fukuoka, July 29, 2020 Japan • Cruising • Beijing (Tianjin), China August 19, 2020 September 22, 2020 7-Night Best of Japan May 31, 2020 Beijing (Tianjin), China • Cruising (2 nights) • July 12, 2020 Kyoto (Maizuru), Japan • Sakaiminato, Japan • August 2, 2020 Fukuoka, Japan • Cruising • Beijing (Tianjin), China 5-Night Fukuoka & June 12, 28, 2020 Beijing (Tianjin), China • Cruising • Fukuoka, Nagasaki August 9, 2020 Japan • Nagasaki, Japan • Cruising • Beijing (Tianjin), China For deployment information and marketing resources, visit LoyalToYouAlways.com/Deployment Features vary by ship. All itineraries are subject to change without notice. ©2019 Royal Caribbean Cruises Ltd. Ships’ registry: The Bahamas. ITINERARY SAIL DATE PORT OF CALL 4-Night Best -

Free Free Free

CWHEREruise WILL YOU ESCAPE TO? FREE FREE FREE DRINKS GRATUITIES STATEROOM £0 PACKAGES & ON BOARD CREDIT UPGRADES DEPOSITS Cruise1st Store, Lowry Outlet, MediaCityUKON SELECTED SKY SAILINGS CHANNEL 688 TV CRUISE CHANNEL 199 REVOLUTIONISED CELEBRITY SILHOUETTE FREE FREE FREE FREE OCEANVIEW GRATUITIES $300 DRINKS ON BOARD TO VERANDA CREDIT UPGRADES ON OCEANVIEW AND ABOVE IRELAND AND ICELAND CELEBRITY SILHOUETTE • 14 NTS • 30 MAY & 05 SEPT 2020 NOW FROM ▶ Southampton ▶ St.Peter Port, Channel Islands ▶ Cork (Cobh), Ireland £1309PP ▶ Dublin, Ireland (Overnight On Board) ▶ Reykjavik, Iceland (Overnight On VERANDA FR.£1799PP Board) ▶ Akureyri, Iceland ▶ Belfast, Northern Ireland ▶ Southampton CONCIERGE FR.£1989PP NORTHERN EUROPE CAPITALS ® The Celebrity Silhouette is impressive, with chic CELEBRITY SILHOUETTE • 14 NTS • 13 JUNE & 18 JULY 2020 NOW FROM upgrades to the iconic Lawn Club, Celebrity have ▶ Southampton ▶ Copenhagen, Denmark (Overnight On Board) ▶ Stockholm, £1719PP provided more space to relax, and socialize in the Sweden ▶ Helsinki, Finland ▶ St. Petersburg, Russia (Overnight On Board) VERANDA FR.£2259PP fresh sea air, plus the Lawn Club Grill offers an ▶ Berlin (Warnemunde), Germany ▶ Arhus, Denmark ▶ Southampton CONCIERGE FR.£2449PP interactive outdoor grilling experience. After a day of adventure unwind in your own cabana-styled haven MEDITERRANEAN DELIGHTS at The Alcoves. 85% of the ship's luxurious staterooms CELEBRITY SILHOUETTE • 14 NTS • 01 AUG 2020 NOW FROM are enhanced by sweeping veranda views. £1699PP Celebrity Cruises -

Royal-Caribbean-Brochure.Pdf

BEST BEST CRUISE LINE CRUISE LINE 2017 2017 DOMESTIC INTERNATIONAL DEPLOYMENT DEPLOYMENT AFTA National Travel AFTA National Travel Industry Awards Industry Awards Asia l Australia l New Zealand l South Pacific 2017-2019 Cruise Holidays RoyalCaribbean.co.nz North Star® See the world from a breathtaking 90 metres above sea level in our jewel-like observation capsule. Only on We’ve taken holidays to a whole new level with our incredible, state-of-the-art experiences you will only find on Royal Caribbean.® ROYAL RipCord® by iFLY® Take to the skies in the first ever skydiving simulator at sea. Ice Skating Watch dazzling ice skating shows or have a go yourself on the first ever ice rinks at sea. 2 Shrek, Madagascar, Kung Fu Panda and all related characters and properties ©2017 DreamWorks Animation LLC. *Fees apply. Venues and amenities vary by ship, see page 7 for details. DreamWorks Experience Take the kids on an ocean adventure with their favourite characters from Shrek®, Madagascar® and Kung Fu Panda™. FlowRider® Surf the high seas on our 12-metre-long surf simulator. Bionic Bar® Mixology meets technology as our unique robotic barmen mix you the perfect cocktail in minutes*. Look out for the orange ROYAL ONLY ON ROYAL badges for more exciting experiences only available on Royal Caribbean. mie's Italia Ja n A relaxed, family-friendly restaurant featuring delicious, rustic dishes created by one of the world's best-loved chefs. O N L L YA Y ON RO SeaPlex® The largest indoor play area at sea with thrilling features like bumper cars, a roller rink and much more. -

7-Night Alaska Cruise Aboard the Quantum of the Seas Round Trip: Seattle, Washington | Mon, Aug 29 2022 - Mon, Sep 05 2022

CardPlayerCruises.com Tel: 888 999 4880 7-Night Alaska Cruise Aboard the Quantum of the Seas Round trip: Seattle, Washington | Mon, Aug 29 2022 - Mon, Sep 05 2022 Call for pricing! As Low as $802** per person Join us on one of our most popular cruises! Day Port/City Arrival Departure Quantum of the Seas Operated by Royal Caribbean International Quantum of the Day 1 | Mon, Aug 29 2022 Seattle, Washington 4:00 p.m. Seas, is a Quantum-class cruise ship. Amenities include: skydiving simulator, Laser Tag, escape room, live entertain- Day 2 | Tue, Aug 30 2022 At Sea ment, 360-view observation ride, rock wall, multiple dining options, clubs, spa and more. Day 3 | Wed, Aug 31 2022 Ketchikan, Alaska 8:00 a.m. 5:00 p.m. Day 4 | Thu, Sep 01 2022 Sitka, Alaska 8:00 a.m. 5:00 p.m. Day 5 | Fri, Sep 02 2022 Endicott Arm & Dawes Glacier 5:00 a.m. 10:00 a.m. Day 5 | Fri, Sep 02 2022 Juneau, Alaska 1:00 p.m. 8:00 p.m. Day 6 | Sat, Sep 03 2022 At Sea Day 7 | Sun, Sep 04 2022 Victoria, British Columbia 4:00 p.m. 10:00 p.m. Day 8 | Mon, Sep 05 2022 Seattle, Washington 7:00 a.m. Dining Begins: To be announced. We request expedited service in the dining room so that everyone is out within 90 minutes. Reserved table tents for Card Player Cruises will be on our tables. Poker Room Card Player Cruises proudly features a professional, fully staed non-smoking poker room. -

Fleet Guide by Ship

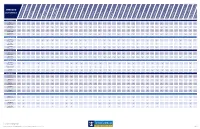

SM SM ® SM ® SM SM ONBOARD SM ® SM ® SM ® ACTIVITIES ® Amplified Vitality at Sea Adventure OceanAdventure Beach Pool Deck AquaTheater Arcade AR Adventure Broadway ShowsBroadway-Style Bumper Cars Carousel Casino Royale Conference Center FlowRider H2O Zone Ice Skating Laser Tag Mini Golf North Star Outdoor Movie Rip-cord by iFLY Rock Climbing WallRoyal Esplanade Royal Promenade Running Track SeaPlex Sky Pad Solarium Splashaway Bay Sports Court Studio B The Perfect StormTidal Wave To Dry For Zip Line (Royal App) Entertainment Royal Escape Room Screen Trapeze School Ultimate Abyss Fitness & Spa / Spa Oasis Class Allure of the Seas® • • • ••••• • ••••• • ••• •• Harmony of the Seas® • • • •••••••••••• • ••••• ••• Oasis of the Seas® ••• • ••••••••••••• • •••• • ••• Symphony of the Seas® • • • ••••••••••••• • ••••• ••• Quantum Class Anthem of the Seas® • •••••••••• ••••••••• •• Ovation of the Seas® • •••••••• •••••••••• •• Quantum of the Seas® • •••••••• ••••••••• •• Quantum Ultra Class Odyssey of the Seas® ••• • • • • • ••••••••• • • Spectrum of the Seas® • ••••••• •••••••••••• •• Freedom Class Freedom of the Seas® •• • • •••••••••••• ••••• • Independence of the Seas® • ••• ••••••••••••••••• • Liberty of the Seas® • ••• ••••••••• •••••• • Voyager Class Adventure of the Seas® • • • ••••••••• ••••• • Explorer of the Seas® • • • ••••••••• ••• • Mariner of the Seas® • • • •••••••••••••••• • Navigator of the Seas® ••• • ••••••••••• ••••• • Voyager of the Seas® • • • •••••••••• •••• • Radiance Class Brilliance of the Seas® •• • • •• ••• • •• • Jewel -

2020-2021 Deployment Summary Guide

2020-2021 DEPLOYMENT SUMMARY GUIDE Stay tuned for Phase II (remainder of deployment) to begin opening in March 2019 SHIP WINTER 2020 (JANUARY — MARCH) SPRING 2020 (APRIL — JUNE) SUMMER 2020(JULY — SEPTEMBER) FALL 2020 (OCTOBER — DECEMBER) WINTER 2021 (JANUARY — MARCH) CARIBBEAN, BAHAMAS & BERMUDA ADVENTURES 6-Night Western Caribbean - Fort Lauderdale 8-Night Eastern Caribbean - Fort Lauderdale 6-Night Western Caribbean - Fort Lauderdale 9/10-Night Bermuda & Caribbean – Bayonne (NY Metro) Adventure of the Seas® 12-Night Southern Caribbean - Fort Lauderdale 5-Night Bermuda– Bayonne (NY Metro) 8-Night Eastern/Southern Caribbean - Fort Lauderdale 5-Night Bermuda – Bayonne (NY Metro) 5/8/9-Night Bermuda & Caribbean - Bayonne (NY Metro) 5-Night Bermuda - Bayonne (NY Metro) 7-Night Eastern/Western Caribbean- Fort Lauderdale 7-Night Eastern/Western Caribbean - Miami 7-Night Eastern/Western Caribbean - Miami Allure of the Seas® Brilliance of the Seas® 4/5 -Night Western Caribbean - Tampa 4/5-Night Western Caribbean - Tampa 4/5-Night Western Caribbean - Galveston 4/5-Night Western Caribbean - Galveston 4/5-Night Western Caribbean - Galveston 4/5-Night Western Caribbean - Galveston Enchantment of the Seas® 7-Night Bahamas - Galveston 7-Night Bahamas - Galveston 5-Night Western Caribbean - Miami Explorer of the Seas® 9-Night Southern Caribbean - Miami Freedom of the Seas® 7-Night Southern Caribbean - San Juan 7-Night Southern Caribbean - San Juan 7-Night Southern Caribbean - San Juan 7-Night Southern Caribbean - San Juan 7 Night Southern Caribbean -

(More) ROYAL CARIBBEAN THANKS EMERGENCY SERVICES, NHS

MEDIA CONTACT: Lucy Radford [email protected] (+44) 07391 865165 Lyan Sierra-Caro [email protected] ROYAL CARIBBEAN THANKS EMERGENCY SERVICES, NHS AND ARMED FORCES WITH UK HOMECOMING, SET FOR THIS SUMMER Anthem of the Seas will be the Family Vacation of Choice to set Sail from Southampton, England Beginning in July 999 Free Sailings to be Offered to Those Working in the Emergency Services, NHS, Social Care Sector and Armed Forces LONDON, 31 March 2021* – Royal Caribbean International is setting a spectacular soundtrack this summer with its return to the UK. The cruise line has announced that Anthem of the Seas, a firm favorite in the region, will begin sailing from Southampton, England as soon as this 7th July. UK families can choose from a combination of 4-night Ocean Getaways in early July and 5- to 8-night British Isles cruises, starting 15th July, that feature visits to destinations such as Liverpool, England, Kirkwall in Scotland and Belfast, Northern Ireland. Plus, in recognition of the tremendous efforts of the emergency services, National Health Service (NHS), social care sector and armed forces over the last year, Royal Caribbean will offer 999 free staterooms on its first Ocean Getaways to those UK residents in these professions. The new summer itineraries open for bookings on 7th April. Sailing with fully vaccinated crew, the cruises – at this time – will be available to UK residents above the age of 18 who are fully vaccinated against COVID-19 and those under the age of 18 with negative test results. These current health and safety measures, like others, may evolve as they are evaluated on an ongoing basis. -

Ovation of the Seas

‘OVATION OF THE SEAS’ ARRIVES IN THE CITY AND HOSTS A “CEL-OVATION” OF THE MARVELS OF HONG KONG Royal Caribbean celebrates the largest cruise ship ever to homeport in Hong Kong and reinforces the development of cruise tourism Hong Kong, 17 June 2016 – Royal Caribbean International, the world’s largest global cruise brand, continues to make waves in Hong Kong’s cruise history. At the end of October, the iconic brand will homeport it’s magnificent, technologically advanced Ovation of the Seas® flagship cruise liner in Hong Kong for a season of five premium cruises to popular destinations such as Japan and Taiwan. Ovation of the Seas® is the largest and most advanced cruise ship ever to call Hong Kong home. A sister ship to Quantum of the Seas® which impressed the city with its visit last year, the 16-deck, 168,000 ton Ovation of the Seas® is the third vessel in Royal Caribbean’s ground-breaking Quantum Class, the second largest cruise class in the world. To enable Hong Kongers to get a first-hand glimpse of the massive ship, Royal Caribbean arranged for Ovation of the Seas® to visit Hong Kong today (17 June) and stay for one night en route her 52-day maiden voyage from Europe to Tianjin, China for a naming ceremony officiated by the first ever Chinese Godmother Fan Bing Bing. The Ship was officially delivered to Royal Caribbean on April 8th 2016. The grand entrance of Ovation of the Seas® into Hong Kong was marked with a prestigious ceremony graced by senior government dignitaries and key industry stakeholders. -

BEYOND a CRUISE. a GLOBAL ODYSSEY. Quantum of the Seas SM

R BEYOND A CRUISE. A GLOBAL ODYSSEY. SM Quantum of the Seas | Explore the best of the world on one extraordinary voyage. The new Quantum of the Seas SM is setting sail for a global journey from New York to Shanghai, bringing never- before-seen WOWs to four continents and incredible destinations—Barcelona, Dubai, Singapore and many more. Announcing the Quantum Global Odyssey. A one-time-only voyage. A once-in-a-lifetime WOW. Beginning May 20, 2014, Crown & Anchor® Society members enjoy early booking for the Quantum Global Odyssey, setting sail May 2015. General booking begins May 22, 2014. Barcelona, Spain Dubai, United Arab Emirates Singapore Revel in the passionate streets of Barcelona. Marvel at the stunning beauty, rich history Beneath the glittering modern surface of this Explore this historically intriguing destination and brilliant promise of one of the world’s magical city, you’ll uncover an eclectic mix of fi lled with unique sights, sounds and fl avors. fastest-growing luxury travel destinations. cultures, religions and other infl uences. ITINERARY SAIL DATES PORTS OF CALL 11-NIGHT OCEAN VOYAGE May 2, 2015 Cape Liberty, New Jersey • Cruising (5 nights) • Ponta Delgada, Azores • Cruising (2 nights) • Cartagena, Spain • Palma De Mallorca, Spain • Barcelona, Spain 16-NIGHT SUEZ CANAL May 13, 2015 Barcelona, Spain • Cruising • Rome (Civitavecchia), Italy • Naples/Capri, Italy • Cruising • Athens (Piraeus), Greece • Cruising (2 nights) • Suez Canal (Passage) • Aqaba, Jordan • Cruising (6 nights) • Dubai, United Arab Emirates 14-NIGHT -

2019 Cruise Ship Schedule

Bermuda 2019 CRUISE SHIP SCHEDULE Compiled by the Department of Marine and Ports Services Information subject to change without notice Dated: June 5th, 2019 www.marineandports.bm 1 | P a g e Capacities – 2019 Name of Ship Number of Length Projected Number of Crew Visits overall number of (Ft) Passengers Average/Total June - Sept Regular/Contract Ships Grandeur of the Seas 18 990 2,172/2,538 840 Anthem of the Seas 24 1,112 4,365/4,905 1,397 Norwegian Escape 27 1,069 4,450/5,000 1,651 Norwegian Gem 22 965 2,656/3,000 1,070 Summit 15 964 2,345/2,538 965 106 Occasional Callers AIDAluna 3 827 2,274/2,584 646 AIDAdiva 1 827 2,274 646 Adventure of the Seas 6 1,021 3,114/3,807 1,185 Aurora 1 886 1,521 816 Azamara Journey 4 592 672 306 Carnival Breeze 3 1,004 3,893 1,386 Carnival Magic 1 1003 3,600/4,400 1,380 Carnival Pride 4 960 2,358/2,680 1,029 Carnival Sunrise 8 892 2,909/3,300 1,100 Carnival Sunshine 4 892 3,307/3,758 1,150 Celebrity Edge 1 1,004 2,904 Celebrity Silhouette 2 1,047 2,768 1,210 Disney Magic 5 966 2,376 945 Divina 1 1,094 3,484 1,751 Hamburg 1 473 359 373 Insignia 6 594 734 386 Le Boreal 1 466 232 140 Marella Discovery 2 1 867 1,836 771 Norwegian Dawn 2 965 2,640 1,069 Norwegian Getaway 2 1,066 3,900 1,595 Norwegian Jade 1 965 2,341 1,076 Norwegian Pearl 2 965 2,341 1,076 Oriana 2 853 1,998 936 Queen Victoria 1 965 1,943 1,001 RCGS Resolute 2 410 146 100 Riviera 1 785 1,389 800 Rotterdam 1 708 1200/1404 600 Serenade of the Seas 3 962 2,191 858 Seven Seas Explorer 2 732 726 542 2 | P a g e Seven Seas Navigator 5 565 480 325 Seven Seas Voyager 1 669 616 445 Silver Spirit 1 642 475 370 Silver Whisper 1 610 341 295 Sirena 1 594 734 386 Spirit of Discovery 1 774 1,000 530 Ventura 1 951 2,835 1,239 Viking Sea 1 755 854 545 Viking Sky 1 755 845 545 Viking Sun 1 755 845 545 Zuiderdam 1 935 1,997 800 87 3 | P a g e KEY Anc GS At Anchor in Great Sound Ham 5/6 Hamilton, #5/6 Passenger Terminal KW King’s Wharf, Dockyard HW Heritage Wharf, Dockyard Pennos Pennos, St.