Master's Project COMPUTATIONAL METHODS for the RIEMANN

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Riemann Sums Fundamental Theorem of Calculus Indefinite

Riemann Sums Partition P = {x0, x1, . , xn} of an interval [a, b]. ck ∈ [xk−1, xk] Pn R(f, P, a, b) = k=1 f(ck)∆xk As the widths ∆xk of the subintervals approach 0, the Riemann Sums hopefully approach a limit, the integral of f from a to b, written R b a f(x) dx. Fundamental Theorem of Calculus Theorem 1 (FTC-Part I). If f is continuous on [a, b], then F (x) = R x 0 a f(t) dt is defined on [a, b] and F (x) = f(x). Theorem 2 (FTC-Part II). If f is continuous on [a, b] and F (x) = R R b b f(x) dx on [a, b], then a f(x) dx = F (x) a = F (b) − F (a). Indefinite Integrals Indefinite Integral: R f(x) dx = F (x) if and only if F 0(x) = f(x). In other words, the terms indefinite integral and antiderivative are synonymous. Every differentiation formula yields an integration formula. Substitution Rule For Indefinite Integrals: If u = g(x), then R f(g(x))g0(x) dx = R f(u) du. For Definite Integrals: R b 0 R g(b) If u = g(x), then a f(g(x))g (x) dx = g(a) f( u) du. Steps in Mechanically Applying the Substitution Rule Note: The variables do not have to be called x and u. (1) Choose a substitution u = g(x). du (2) Calculate = g0(x). dx du (3) Treat as if it were a fraction, a quotient of differentials, and dx du solve for dx, obtaining dx = . -

Polynomial Sequences of Binomial Type and Path Integrals

Preprint math/9808040, 1998 LEEDS-MATH-PURE-2001-31 Polynomial Sequences of Binomial Type and Path Integrals∗ Vladimir V. Kisil† August 8, 1998; Revised October 19, 2001 Abstract Polynomial sequences pn(x) of binomial type are a principal tool in the umbral calculus of enumerative combinatorics. We express pn(x) as a path integral in the “phase space” N × [−π,π]. The Hamilto- ∞ ′ inφ nian is h(φ)= n=0 pn(0)/n! e and it produces a Schr¨odinger type equation for pn(x). This establishes a bridge between enumerative P combinatorics and quantum field theory. It also provides an algorithm for parallel quantum computations. Contents 1 Introduction on Polynomial Sequences of Binomial Type 2 2 Preliminaries on Path Integrals 4 3 Polynomial Sequences from Path Integrals 6 4 Some Applications 10 arXiv:math/9808040v2 [math.CO] 22 Oct 2001 ∗Partially supported by the grant YSU081025 of Renessance foundation (Ukraine). †On leave form the Odessa National University (Ukraine). Keywords and phrases. Feynman path integral, umbral calculus, polynomial sequence of binomial type, token, Schr¨odinger equation, propagator, wave function, cumulants, quantum computation. 2000 Mathematics Subject Classification. Primary: 05A40; Secondary: 05A15, 58D30, 81Q30, 81R30, 81S40. 1 Polynomial Sequences and Path Integrals 2 Under the inspiring guidance of Feynman, a short- hand way of expressing—and of thinking about—these quantities have been developed. Lewis H. Ryder [22, Chap. 5]. 1 Introduction on Polynomial Sequences of Binomial Type The umbral calculus [16, 18, 19, 21] in enumerative combinatorics uses poly- nomial sequences of binomial type as a principal ingredient. A polynomial sequence pn(x) is said to be of binomial type [18, p. -

The Definite Integrals of Cauchy and Riemann

Ursinus College Digital Commons @ Ursinus College Transforming Instruction in Undergraduate Analysis Mathematics via Primary Historical Sources (TRIUMPHS) Summer 2017 The Definite Integrals of Cauchy and Riemann Dave Ruch [email protected] Follow this and additional works at: https://digitalcommons.ursinus.edu/triumphs_analysis Part of the Analysis Commons, Curriculum and Instruction Commons, Educational Methods Commons, Higher Education Commons, and the Science and Mathematics Education Commons Click here to let us know how access to this document benefits ou.y Recommended Citation Ruch, Dave, "The Definite Integrals of Cauchy and Riemann" (2017). Analysis. 11. https://digitalcommons.ursinus.edu/triumphs_analysis/11 This Course Materials is brought to you for free and open access by the Transforming Instruction in Undergraduate Mathematics via Primary Historical Sources (TRIUMPHS) at Digital Commons @ Ursinus College. It has been accepted for inclusion in Analysis by an authorized administrator of Digital Commons @ Ursinus College. For more information, please contact [email protected]. The Definite Integrals of Cauchy and Riemann David Ruch∗ August 8, 2020 1 Introduction Rigorous attempts to define the definite integral began in earnest in the early 1800s. A major motivation at the time was the search for functions that could be expressed as Fourier series as follows: 1 a0 X f (x) = + (a cos (kw) + b sin (kw)) where the coefficients are: (1) 2 k k k=1 1 Z π 1 Z π 1 Z π a0 = f (t) dt; ak = f (t) cos (kt) dt ; bk = f (t) sin (kt) dt. 2π −π π −π π −π P k Expanding a function as an infinite series like this may remind you of Taylor series ckx from introductory calculus, except that the Fourier coefficients ak; bk are defined by definite integrals and sine and cosine functions are used instead of powers of x. -

RIEMANN's HYPOTHESIS 1. Gauss There Are 4 Prime Numbers Less

RIEMANN'S HYPOTHESIS BRIAN CONREY 1. Gauss There are 4 prime numbers less than 10; there are 25 primes less than 100; there are 168 primes less than 1000, and 1229 primes less than 10000. At what rate do the primes thin out? Today we use the notation π(x) to denote the number of primes less than or equal to x; so π(1000) = 168. Carl Friedrich Gauss in an 1849 letter to his former student Encke provided us with the answer to this question. Gauss described his work from 58 years earlier (when he was 15 or 16) where he came to the conclusion that the likelihood of a number n being prime, without knowing anything about it except its size, is 1 : log n Since log 10 = 2:303 ::: the means that about 1 in 16 seven digit numbers are prime and the 100 digit primes are spaced apart by about 230. Gauss came to his conclusion empirically: he kept statistics on how many primes there are in each sequence of 100 numbers all the way up to 3 million or so! He claimed that he could count the primes in a chiliad (a block of 1000) in 15 minutes! Thus we expect that 1 1 1 1 π(N) ≈ + + + ··· + : log 2 log 3 log 4 log N This is within a constant of Z N du li(N) = 0 log u so Gauss' conjecture may be expressed as π(N) = li(N) + E(N) Date: January 27, 2015. 1 2 BRIAN CONREY where E(N) is an error term. -

On the Approximation of Riemann-Liouville Integral by Fractional Nabla H-Sum and Applications L Khitri-Kazi-Tani, H Dib

On the approximation of Riemann-Liouville integral by fractional nabla h-sum and applications L Khitri-Kazi-Tani, H Dib To cite this version: L Khitri-Kazi-Tani, H Dib. On the approximation of Riemann-Liouville integral by fractional nabla h-sum and applications. 2016. hal-01315314 HAL Id: hal-01315314 https://hal.archives-ouvertes.fr/hal-01315314 Preprint submitted on 12 May 2016 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. On the approximation of Riemann-Liouville integral by fractional nabla h-sum and applications L. Khitri-Kazi-Tani∗ H. Dib y Abstract First of all, in this paper, we prove the convergence of the nabla h- sum to the Riemann-Liouville integral in the space of continuous functions and in some weighted spaces of continuous functions. The connection with time scales convergence is discussed. Secondly, the efficiency of this approximation is shown through some Cauchy fractional problems with singularity at the initial value. The fractional Brusselator system is solved as a practical case. Keywords. Riemann-Liouville integral, nabla h-sum, fractional derivatives, fractional differential equation, time scales convergence MSC (2010). 26A33, 34A08, 34K28, 34N05 1 Introduction The numerous applications of fractional calculus in the mathematical modeling of physical, engineering, economic and chemical phenomena have contributed to the rapidly growing of this theory [12, 19, 21, 18], despite the discrepancy on definitions of the fractional operators leading to nonequivalent results [6]. -

Computation and the Riemann Hypothesis: Dedicated to Herman Te Riele on the Occasion of His Retirement

Computation and the Riemann Hypothesis: Dedicated to Herman te Riele on the occasion of his retirement Andrew Odlyzko School of Mathematics University of Minnesota [email protected] http://www.dtc.umn.edu/∼odlyzko December 2, 2011 Andrew Odlyzko ( School of Mathematics UniversityComputation of Minnesota and [email protected] Riemann Hypothesis: http://www.dtc.umn.edu/ Dedicated toDecember2,2011 Herman te∼ Rieodlyzkole on) the 1/15 occasion The mysteries of prime numbers: Mathematicians have tried in vain to discover some order in the sequence of prime numbers but we have every reason to believe that there are some mysteries which the human mind will never penetrate. To convince ourselves, we have only to cast a glance at tables of primes (which some have constructed to values beyond 100,000) and we should perceive that there reigns neither order nor rule. Euler, 1751 Andrew Odlyzko ( School of Mathematics UniversityComputation of Minnesota and [email protected] Riemann Hypothesis: http://www.dtc.umn.edu/ Dedicated toDecember2,2011 Herman te∼ Rieodlyzkole on) the 2/15 occasion Herman te Riele’s contributions towards elucidating some of the mysteries of primes: numerical verifications of Riemann Hypothesis (RH) improved bounds in counterexamples to the π(x) < Li(x) conjecture disproof and improved lower bounds for Mertens conjecture improved bounds for de Bruijn – Newman constant ... Andrew Odlyzko ( School of Mathematics UniversityComputation of Minnesota and [email protected] Riemann Hypothesis: http://www.dtc.umn.edu/ Dedicated toDecember2,2011 -

Umbral Calculus and Cancellative Semigroup Algebras

Preprint funct-an/9704001, 1997 Umbral Calculus and Cancellative Semigroup Algebras∗ Vladimir V. Kisil April 1, 1997; Revised February 4, 2000 Dedicated to the memory of Gian-Carlo Rota Abstract We describe some connections between three different fields: com- binatorics (umbral calculus), functional analysis (linear functionals and operators) and harmonic analysis (convolutions on group-like struc- tures). Systematic usage of cancellative semigroup, their convolution algebras, and tokens between them provides a common language for description of objects from these three fields. Contents 1 Introduction 2 2 The Umbral Calculus 3 arXiv:funct-an/9704001v2 8 Feb 2000 2.1 Finite Operator Description ................... 3 2.2 Hopf Algebras Description .................... 4 2.3 The Semantic Description .................... 4 3 Cancellative Semigroups and Tokens 5 3.1 Cancellative Semigroups: Definition and Examples ....... 5 3.2 Tokens: Definition and Examples ................ 10 3.3 t-Transform ............................ 13 ∗Supported by grant 3GP03196 of the FWO-Vlaanderen (Fund of Scientific Research- Flanders), Scientific Research Network “Fundamental Methods and Technique in Mathe- matics”. 2000 Mathematics Subject Classification. Primary: 43A20; Secondary: 05A40, 20N++. Keywords and phrases. Cancellative semigroups, umbral calculus, harmonic analysis, token, convolution algebra, integral transform. 1 2 Vladimir V. Kisil 4 Shift Invariant Operators 16 4.1 Delta Families and Basic Distributions ............. 17 4.2 Generating Functions and Umbral Functionals ......... 22 4.3 Recurrence Operators and Generating Functions ........ 24 5 Models for the Umbral Calculus 28 5.1 Finite Operator Description: a Realization ........... 28 5.2 Hopf Algebra Description: a Realization ............ 28 5.3 The Semantic Description: a Realization ............ 29 Acknowledgments 30 It is a common occurrence in combinatorics for a sim- ple idea to have vast ramifications; the trick is to real- ize that many seemingly disparate phenomena fit un- der the same umbrella. -

Using the TI-89 to Find Riemann Sums

Using the TI-89 to find Riemann sums Z b If function f is continuous on interval [a, b], f(x) dx exists and can be approximated a using either of the Riemann sums n n X X f(xi)∆x or f(xi−1)∆x i=1 i=1 (b−a) where ∆x = n and n is the number of subintervals chosen. The first of these Riemann sums evaluates function f at the right endpoint of each subinterval; the second evaluates at the left endpoint of each subinterval. n X P To evaluate f(xi) using the TI-89, go to F3 Calc and select 4: ( sum i=1 The command line should then be completed in the following form: P (f(xi), i, 1, n) The actual Riemann sum is then determined by multiplying this ans by ∆x (or incorpo- rating this multiplication into the same command line.) [Warning: Be sure to set the MODE as APPROXIMATE in this case. Otherwise, the calculator will spend an inordinate amount of time attempting to express each term of the summation in exact symbolic form.] Z 4 √ Example: To approximate 1 + x3 dx using Riemann sums with n = 100 subinter- 2 b−a 2 i vals, note first that ∆x = n = 100 = .02. Also xi = 2 + i∆x = 2 + 50 . So the right endpoint approximation will be found by entering √ P( (2 + (1 + i/50)∧3), i, 1, 100) × .02 which gives 10.7421. This is an overestimate, since the function is increasing on the given interval. To find the left endpoint approximation, replace i by (i − 1) in the square root part of the command. -

Fractional Calculus

Generalised Fractional Calculus Penelope Drastik Supervised by Marianito Rodrigo September 2018 Outline 1. Integration 2. Fractional Calculus 3. My Research Riemann sum: P tagged partition, f :[a; b] ! R n X S(f ; P) = f (ti )(xi − xi−1) i=1 The Riemann sum Partition of [a; b]: Non-overlapping intervals which cover [a; b] a = x0 < x1 < ··· < xi−1 < xi < ··· xn = b Tagged partition of [a; b]: Intervals in partition paired with tag points n P = f([xi−1; xi ]; ti )gi=1 The Riemann sum Partition of [a; b]: Non-overlapping intervals which cover [a; b] a = x0 < x1 < ··· < xi−1 < xi < ··· xn = b Tagged partition of [a; b]: Intervals in partition paired with tag points n P = f([xi−1; xi ]; ti )gi=1 Riemann sum: P tagged partition, f :[a; b] ! R n X S(f ; P) = f (ti )(xi − xi−1) i=1 The Riemann integral R b a f (x)dx = A means that: For all " > 0, there exists δ" > 0 such that if a tagged partition P satisfies 0 < xi − xi−1 < δ" for i = 1;:::; n then jS(f ; P) − Aj < " The Generalised Riemann integral R b a f (x)dx = A means that: For all " > 0, there exists a strictly positive function δ" :[a; b] ! R+ such that if a tagged partition P satisfies ti 2 [xi−1; xi ] ⊆ [ti − δ(ti ); ti + δ(ti )] for i = 1;:::; n then jS(f ; P) − Aj < " Riemann-Stieltjes integral: R b a f (x)dα(x) = A means that: For all " > 0, there exists δ" > 0 such that if a tagged partition P satisfies 0 < xi − xi−1 < δ" for i = 1;:::; n then jS(f ; P; α) − Aj < " The Riemann-Stieltjes integral Riemann-Stieltjes sum of f : Integrator α : I ! R, partition P n X S(f ; P; α) = f (ti )[α(xi -

1.1 Limits: an Informal View 4.1 Areas and Sums

Chapter 4 Integrals from Calculus: Concepts & Computation by David Betounes and Mylan Redfern | 2016 Copyright | 9781524917692 Property of Kendall Hunt Publishing 4.1 Areas and Sums 257 4 Integrals Calculus Concepts & Computation 1.1 Limits: An Informal View 4.1 Areas and Sums > with(code_ch4,circle,parabola);with(code_ch1sec1); [circle, parabola] [polygonlimit, secantlimit] This chapter begins our study of the integral calculus, which is the counter-part to the differential calculus you learned in Chapters 1–3. The topic of integrals, otherwise known as antiderivatives, was introduced in Section 3.7, and you should The General Area Problem read that discussion before continuing here. A major application of antiderivatives, or integrals, is the measurement of areas of planar regions D. In fact, a principal motive behind the invention of the integral calculus was to solve the area problem. See Figure 4.1.1. D Before we learn how to measure areas of such general regions D, it is best to think about the areas of simple regions, and, indeed, reflect on the very notion of what is meant by “area.” This we discuss here. Then, in the next two sections, Sections 4.2 and 4.3 , we look at the details of measuring areas of regions “beneath the graphs of continuous functions.” Then in Section 5.1 we tackle the task of finding area of more complicated regions, such as the region D in Figure 4.4.1. We have intuitive notions about what is meant by the area of a region. It is a positive Find the area Figure 4.1.1: number A which somehow measures the “largeness” of the region and enables us of the region D bounded by a to compare regions with different shapes. -

Evaluation of Engineering & Mathematics Majors' Riemann

Paper ID #14461 Evaluation of Engineering & Mathematics Majors’ Riemann Integral Defini- tion Knowledge by Using APOS Theory Dr. Emre Tokgoz, Quinnipiac University Emre Tokgoz is currently an Assistant Professor of Industrial Engineering at Quinnipiac University. He completed a Ph.D. in Mathematics and a Ph.D. in Industrial and Systems Engineering at the University of Oklahoma. His pedagogical research interest includes technology and calculus education of STEM majors. He worked on an IRB approved pedagogical study to observe undergraduate and graduate mathe- matics and engineering students’ calculus and technology knowledge in 2011. His other research interests include nonlinear optimization, financial engineering, facility allocation problem, vehicle routing prob- lem, solar energy systems, machine learning, system design, network analysis, inventory systems, and Riemannian geometry. c American Society for Engineering Education, 2016 Evaluation of Engineering & Mathematics Majors' Riemann Integral Definition Knowledge by Using APOS Theory In this study senior undergraduate and graduate mathematics and engineering students’ conceptual knowledge of Riemann’s definite integral definition is observed by using APOS (Action-Process- Object-Schema) theory. Seventeen participants of this study were either enrolled or recently completed (i.e. 1 week after the course completion) a Numerical Methods or Analysis course at a large Midwest university during a particular semester in the United States. Each participant was asked to complete a questionnaire consisting of calculus concept questions and interviewed for further investigation of the written responses to the questionnaire. The research question is designed to understand students’ ability to apply Riemann’s limit-sum definition to calculate the definite integral of a specific function. Qualitative (participants’ interview responses) and quantitative (statistics used after applying APOS theory) results are presented in this work by using the written questionnaire and video recorded interview responses. -

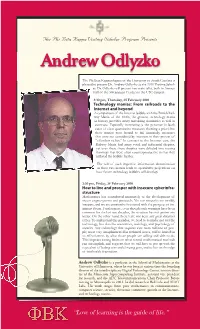

USC Phi Beta Kappa Visiting Scholar Program

The Phi Beta Kappa chapter of the University of South Carolina is pleased to present Dr. Andrew Odlyzko as the 2010 Visiting Schol- ar. Dr. Odlyzko will present two main talks, both in Amoco Hall of the Swearingen Center on the USC campus: 3:30 pm, Thursday, 25 February 2010 Technology manias: From railroads to the Internet and beyond A comparison of the Internet bubble with the British Rail- way Mania of the 1840s, the greatest technology mania in history, provides many tantalizing similarities as well as contrasts. Especially interesting is the presence in both cases of clear quantitative measures showing a priori that these manias were bound to fail financially, measures that were not considered by investors in their pursuit of “effortless riches.” In contrast to the Internet case, the Railway Mania had many vocal and influential skeptics, yet even then, these skeptics were deluded into issuing warnings that were often counterproductive in that they inflated the bubble further. The role of such imperfect information dissemination in these two manias leads to speculative projections on how future technology bubbles will develop. 2:30 pm, Friday, 26 February 2010 How to live and prosper with insecure cyberinfra- structure Mathematics has contributed immensely to the development of secure cryptosystems and protocols. Yet our networks are terribly insecure, and we are constantly threatened with the prospect of im- minent doom. Furthermore, even though such warnings have been common for the last two decades, the situation has not gotten any better. On the other hand, there have not been any great disasters either.