Boryszew: 2021 Q1 Results

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Using the Idea of Market-Expected Return

BUSINESS, MANAGEMENT AND EDUCATION ISSN 2029-7491 print / ISSN 2029-6169 online 2012, 10(1): 11–24 doi:10.3846/bme.2012.02 USING THE IDEA OF MARKET-EXPECTED RETURN RATES ON INVESTED CAPITAL IN THE VERIFICATION OF CONFORMITY OF MARKET EVALUATION OF STOCK-LISTED COMPANIES WITH THEIR INTRINSIC VALUE Paweł Mielcarz1, Emilia Roman2 1Kozminski University, Jagiellonska 57/59, 03-301 Warsaw, Poland 2DCF Consulting Sp. z o.o., Kochanowskiego 24, 05-071 Sulejowek, Poland E-mails: [email protected] (corresponding author); [email protected] Received 02 October 2011; accepted 07 March 2012 Abstract. This article presents the concept of investor-expected rates of return on capital of listed companies and the use of these rates in the assessment of the extent to which the stock evaluation of a given entity is compatible with its intrinsic value. The article also features results of the research aimed at verification – with the use of the presented tool – of whether the market value of WSE-listed companies reflects their fundamental value. The calculations presented in the empirical part of the article show that at the beginning of 2011, market evaluation of the most of the analysed entities greatly exceeded their fundamental value. Keywords: DCF, EVA, valuation, capital markets, fundamental analysis, ROIC, intrinsic value. Reference to this paper should be made as follows: Mielcarz, P.; Roman, E. 2012. Using the idea of market-expected return rates on invested capital in the verifica- tion of conformity of market evaluation of stock-listed companies with their intrin- sic value, Business, Management and Education 10(1): 11–24. -

Poland Is Promoted to Developed Market Status by Ftse Russell

POLAND IS PROMOTED TO DEVELOPED MARKET STATUS BY FTSE RUSSELL As of 24 September 2018, Poland is classified as a Key issues Developed market by FTSE Russell. This promotion to the highest possible status in FTSE Russell's classifications is a • About FTSE Russell and FTSE significant achievement and a recognition of continuous Global Equity Index Series enhancements of the capital markets infrastructure and (GEIS) steady economic growth in Poland. Poland is now among the • International context eight largest economies in the European Union (EU) and 25 • For whom is Poland's promotion relevant? largest economies in the world. • Status of some Polish blue chips • Further implications ABOUT FTSE RUSSELL AND FTSE GLOBAL EQUITY INDEX SERIES (GEIS) FTSE Russell, a subsidiary of the London Stock Exchange Group, is a provider of stock market indices and associated data services, one of the largest in the world. FTSE Global Equity Index Series (GEIS) is a benchmark measuring the performance of global equity markets. According to FTSE Russell, FTSE GEIS looks at around 7,400 large-, mid- and small-cap stocks across 47 countries, with a total net market capitalization of USD 52 trillion, covering approximately 98 percent of the world’s investable market. FTSE Russell classifies markets using four categories: Developed, Advanced Emerging, Secondary Emerging and Frontier. Developed market status means that apart from market quality and size criteria being met, the country is considered as having high gross national income with developed market infrastructures. When determining a country's status, FTSE Russell measures, amongst other things, the market quality (regulatory framework, transactional landscape, derivatives market, etc.), adequateness of the market size, consistency and predictability, stability and market access (ease of investment and disinvestment). -

Klasa WIG20 KONTRAKTY TERMINOWE

DEPOZYTY ZABEZPIECZAJĄCE W DM PKO BP - STAN NA 2017-11-08 Klasa WIG20 KONTRAKTY TERMINOWE: Właściwy depozyt zabezpieczający w KDPW 7,20% Wstępny depozyt zabezpieczający w DM PKO BP 8,64% OPCJE, JEDNOSTKI INDEKSOWE: Parametr modyfikujący zmienność dla opcji 2,10% Klasa mWIG40 Właściwy depozyt zabezpieczający w KDPW 5,70% Wstępny depozyt zabezpieczający w DM PKO BP 6,84% Klasa EUR Właściwy depozyt zabezpieczający w KDPW 3,30% Wstępny depozyt zabezpieczający w DM PKO BP 3,96% Klasa USD Właściwy depozyt zabezpieczający w KDPW 5,20% Wstępny depozyt zabezpieczający w DM PKO BP 6,24% Klasa CHF Właściwy depozyt zabezpieczający w KDPW 4,80% Wstępny depozyt zabezpieczający w DM PKO BP 5,76% Klasa GBP Właściwy depozyt zabezpieczający w KDPW 3,90% Wstępny depozyt zabezpieczający w DM PKO BP 4,68% Klasa 1M WIBOR 1MW Właściwy depozyt zabezpieczający w KDPW 0,31% Wstępny depozyt zabezpieczający w DM PKO BP 0,37% Klasa 3M WIBOR 3MW Właściwy depozyt zabezpieczający w KDPW 0,49% Wstępny depozyt zabezpieczający w DM PKO BP 0,59% Klasa 6M WIBOR 6MW Właściwy depozyt zabezpieczający w KDPW 0,46% Wstępny depozyt zabezpieczający w DM PKO BP 0,55% Klasa OBLIGACJE STB Właściwy depozyt zabezpieczający w KDPW 1,00% Wstępny depozyt zabezpieczający w DM PKO BP 1,20% Klasa OBLIGACJE MTB Właściwy depozyt zabezpieczający w KDPW 2,00% Wstępny depozyt zabezpieczający w DM PKO BP 2,40% Klasa OBLIGACJE LTB Właściwy depozyt zabezpieczający w KDPW 2,60% Wstępny depozyt zabezpieczający w DM PKO BP 3,12% Klasa ASSECO POLAND ACP Właściwy depozyt zabezpieczający w KDPW 8,50% Wstępny -

Appendix D Updated.Xlsx

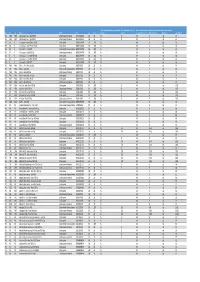

Block Threshold Minimum - Screen Tradeable LIS Pre-Trade Value - Block Only Strategy Threshold Minimum - Strategy Threshold Minimum - Basis Trade Threshold MIC PCC LCC Name ESMA ISIN Curr Lot Size Contracts Contracts Screen Tradeable Contracts Block Only Contracts Minimum Post-Trade LIS IFLO NWD NWA 21st Century Fox - Cash FLEX Fut Stock futures/forwards US90130A1016 USD 100 N/A 11 N/A 22 n/a 527 IFLO NWH NWA 21st Century Fox - Phys FLEX Fut Stock futures/forwards US90130A1016 USD 100 N/A 11 N/A 22 n/a 527 IFLO IIU III 3i Group plc - Amer Cash FLEX Opt Stock options GB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 168 IFLO IIQ III 3i Group plc - Amer Phys FLEX Opt Stock options GB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 168 IFLO 0U6 III 3i Group Plc - Cash DASF Stock dividend futures/forwardsGB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 60 IFLO IIY III 3i Group plc - Cash FLEX Fut Stock futures/forwards GB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 168 IFLO IIJ III 3i Group plc - Euro Cash FLEX Opt Stock options GB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 168 IFLO IIX III 3i Group plc - Euro Phys FLEX Opt Stock options GB00B1YW4409 GBP 1000 N/A 3 N/A 6 n/a 168 IFLO III III 3i Group Plc - STND OPT Stock options GB00B1YW4409 GBP 1000 250 3 500 6 n/a 168 IFLO PMR PMA 3M Co - Amer Phys Flex Opt Stock options US88579Y1010 USD 100 N/A 2 N/A 4 n/a 79 IFLO 3CP PMA 3M Co - Cash DASF Stock dividend futures/forwardsUS88579Y1010 USD 100 N/A 2 N/A 4 n/a 28 IFLO PMD PMA 3M Co - Cash FLEX Fut Stock futures/forwards US88579Y1010 USD 100 N/A 2 N/A 4 n/a 79 IFLO PML PMA 3M Co - Euro Cash Flex -

Investment Property in the Financial Statements of Capital Groups Listed on the Warsaw Stock Exchange

ISSN 2411-9571 (Print) European Journal of Economics January-April 2016 ISSN 2411-4073 (online) and Business Studies Volume 2, Issue 1 Investment Property in the Financial Statements of Capital Groups Listed on the Warsaw Stock Exchange Piotr Prewysz-Kwinto WSB University in Torun, Department of Finance and Accounting Poland, ppqq@poczta. onet. pl Grażyna Voss University of Technology and Life Sciences, Faculty of Management, Bydgoszcz, Poland, gvoss@wp. pl Abstract In recent years, investing in property has become very popular. It is related to a significant decrease in interest rates, which has resulted in a decrease in interest rates on bank deposits and risk-free securities. What is more, this kind of investment seems to be less risky than investing in shares or raw materials due to a steady increase in property prices in Poland in the recent years. Investment property owned by an entity conducting business activity must be properly presented in financial statements, which is next reflected in the evaluation of financial position. Recognition, measurement and presentation of investment property in financial statements have been comprehensively prescribed in International Accounting Standard 40 – Investment Property, which was released in December 2003. It was first applied to financial statements prepared for the reporting period starting after January 1, 2005. The standard was revised twice – first in 2008 and then in 2013. The aim of this paper is to describe the recognition, measurement and disclosure of investment property under polish and international accounting regulations as well as to analyze the presentation of such information in financial statements of the largest companies listed on the Warsaw Stock Exchange. -

CCC, Enea, Energa, Eurocash, JSW

Dziennik 17 maja 2019 r. Zapraszamy do uczestnictwa w konferencji WallStreet, która odbędzie się w dniach 31 maja-2 Indeksy GPW zmiana czerwca 2019 roku w Karpaczu. Będzie to unikalna okazja aby spotkać się z naszymi WIG otw. 56 583,4 0,0% analitykami technicznymi i spróbować sił w grze giełdowej, którą poprowadzą Przemysław WIG zam. 56 664,5 0,5% Smoliński i Paweł Małmyga. Zapraszamy także na wykład „Jak wygrać z rynkiem bez obrót (mln PLN) 944,5 28,8% nieprzespanych nocy?” Prelekcję poprowadzi Emil Łobodziński, odpowiedzialny w DM PKO BP WIG 20 otw. 2 174,1 -0,1% za doradztwo inwestycyjne i portfele modelowe. Więcej informacji znajduje się tutaj. WIG 20 zam. 2 188,4 0,9% FW20 otw. 2 172,0 -0,2% FW20 zam. 2 187,0 0,7% Komentarz dnia: mWIG40 otw. 3 937,5 0,1% Na wczorajszej sesji mocno spadły kursy największych spółek handlowych, zarówno mWIG40 zam. 3 918,5 -0,4% odzieżowych jak i żywnościowych. Takie zachowanie wynika z informacji, że sąd UE zdecydował o nieważności zakazu wprowadzenia podatku handlowego w Polsce wydanego przez Komisję Największe wzrosty kurs zmiana Europejską. Wyrok nie jest ostateczny. Oznacza on jednak, że o ile nie będzie odwołania, to od 1 Lotos 78,50 6,1% stycznia 2020 roku podatek ten zacznie obowiązywać. Jest to informacja negatywna dla dużych KGHM 96,82 4,2% sklepów. Z punktu widzenia wyników największych giełdowych spółek najmocniej dotknie to PKN Orlen 90,48 3,5% Jeronimo Martins oraz Dino. Finalnie oczekujemy, że w ich przypadku część kosztów nowego Ten Square Games 146,60 3,4% podatku zostanie przeniesiona na klientów. -

WOOD's Winter in Prague

emerging europe conference WOOD’s Winter in Prague Tuesday 5 December to Friday 8 December 2017 Please join us for our flagship event - now in its6th year - spanning 4 jam-packed days. We expect to host over 160 companies representing more than 15 countries. Click here ! For more information please contact Registration closes your WOOD sales representative: Tuesday: Energy, Industrials and Materials Warsaw +48 222 22 1530 Wednesday: TMT and Utilities on 10 November! Prague +420 222 096 453 Thursday: Consumer, Healthcare and Real Estate London +44 20 3530 7685 Friday: Diversified and Financials [email protected] Invited Companies by country Bolded confirmed Austria Iraq PGE PIK Lokman Hekim AT & S DNO PGNiG Polymetal International Migros Ticaret Atrium Genel Energy PKN Orlen Polyus Otokar BUWOG Kazakhstan PKO BP Raven Russia Pegasus Airlines DO&CO KMG EP PKP Cargo Rosneft Petkim Erste Group Bank Nostrum Oil & Gas Prime Car Management Rostelecom Reysas REIT Immofinanz Steppe Cement PZU Rusal Sabanci Holding OMV Lithuania Synthos Severstal Sisecam PORR Siauliu Bankas Tauron Sistema Tat Gida Raiffeisen International Poland Warsaw Stock Exchange Surgutneftegas TAV Strabag Agora Wirtualna Polska Tatneft Tekfen Holding Telekom Austria Alior Bank Work Service Tinkoff Bank Teknosa Uniqa Insurance Group Amica Romania TMK Torunlar REIC Vienna Insurance AmRest Banca Transilvania TransContainer Tofas Warimpex Asseco Poland Bucharest Stock Exchange VTB TSKB Croatia Bank Millennium Conpet X5 Tumosan Podravka Bank Pekao DIGI Yandex Turcas Petrol Czech -

Lista Spółek Uwzględnionych W Raporcie

Wynagrodzenia członków zarządów spółek notowanych na GPW w 2011 roku 1 Lista spółek uwzględnionych w raporcie 4fun Media SA Bioton SA ABC Data Spółka Akcyjna Bipromet SA ABM Solid SA BNP Paribas Bank Polska Spółka Akcyjna Action SA Boryszew SA AD. Drągowski S.A. BRE Bank SA Advadis SA Budimex SA Agora SA Budopol-Wrocław SA Alchemia SA Budvar Centrum SA Alma Market SA Bumech SA Alterco SA BZ WBK SA Amica Wronki SA Calatrava Capital SA Ampli SA CAM Media S.A. Amrest Holdings Se Capital Partners SA Anti S.A. Cash Flow SA Apator SA CD Projekt RED S.A. Aplisens S.A. Celtic Property Developments S.A. Arctic Paper S.A. Centrozap S.A. Arcus S.A. Centrum Klima S.A. Armatura Kraków SA Ceramika Nowa Gala SA Arteria SA Ciech SA Asseco BS SA City Interactive SA Asseco Poland SA Cognor SA Asseco South Eastern Europe SA Colian Spółka Akcyjna Atlanta Poland SA ComArch SA Atlantis SA Comp Safe Support SA ATM Grupa SA Complex SA ATM SA CP Energia SA Atrem SA Cyfrowy Polsat SA Awbud Spółka Akcyjna Dębica SA B3System SA Decora SA Bank BPH SA Delko SA Bank Handlowy SA DGA SA Bank Millennium SA Dom Development SA Bank Ochrony Środowiska SA Dom Maklerski IDM SA Bank Pekao SA Drewex SA Barlinek SA Drop SA Berling Spółka Akcyjna Drozapol-Profil SA Best SA eCard SA Sedlak & Sedlak 2012 Wynagrodzenia członków zarządów spółek notowanych na GPW w 2011 roku 2 ED Invest Spółka Akcyjna Getin Noble Bank SA Efekt SA Giełda Papierów Wartościowych w Echo Investment SA Warszawie Spółka Akcyjna Eko Export SA Giełda Praw Majątkowych Vindexus S.A. -

Stoxx® Europe Total Market Index

STOXX® EUROPE TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) NESTLE Food & Beverage Switzerland 3.41 ROCHE HLDG P Health Care Switzerland 2.55 NOVARTIS Health Care Switzerland 2.16 SAP Technology Germany 1.69 ASML HLDG Technology Netherlands 1.50 ASTRAZENECA Health Care Great Britain 1.43 LINDE Chemicals Germany 1.32 LVMH MOET HENNESSY Personal & Household Goods France 1.25 SANOFI Health Care France 1.15 NOVO NORDISK B Health Care Denmark 1.12 SIEMENS Industrial Goods & Services Germany 1.00 GLAXOSMITHKLINE Health Care Great Britain 0.95 TOTAL Oil & Gas France 0.92 ALLIANZ Insurance Germany 0.85 UNILEVER NV Personal & Household Goods Netherlands 0.80 HSBC Banks Great Britain 0.78 L'OREAL Personal & Household Goods France 0.77 BRITISH AMERICAN TOBACCO Personal & Household Goods Great Britain 0.76 AIR LIQUIDE Chemicals France 0.75 DIAGEO Food & Beverage Great Britain 0.75 IBERDROLA Utilities Spain 0.70 UNILEVER PLC Personal & Household Goods Great Britain 0.69 RECKITT BENCKISER GRP Personal & Household Goods Great Britain 0.68 RIO TINTO Basic Resources Great Britain 0.67 SCHNEIDER ELECTRIC Industrial Goods & Services France 0.66 ENEL Utilities Italy 0.66 BAYER Health Care Germany 0.64 BP Oil & Gas Great Britain 0.62 ADIDAS Personal & Household Goods Germany 0.59 BASF Chemicals Germany 0.57 DEUTSCHE TELEKOM Telecommunications Germany 0.55 ZURICH INSURANCE GROUP Insurance Switzerland 0.55 ROYAL DUTCH SHELL A Oil & Gas Great Britain 0.54 Kering Retail France 0.50 VINCI Construction & Materials France 0.48 ANHEUSER-BUSCH INBEV Food & Beverage Belgium 0.47 BHP GROUP PLC. -

The Mineral Industry of Poland in 2016

2016 Minerals Yearbook POLAND [ADVANCE RELEASE] U.S. Department of the Interior March 2021 U.S. Geological Survey The Mineral Industry of Poland By Lindsey Abdale In 2016, Poland’s economy was the 9th largest in Europe Other relevant laws and policy documents include the and the 23d largest in the world in terms of gross domestic Polish Energy Law of April 10, 1997; the Environmental product (GDP). Poland was estimated to be Europe’s Protection Law of April 27, 2001; the Act on Reserves second-ranked producer of coal, the third-ranked producer of Crude Oil, Petroleum Products and Natural Gas of of copper, and the fourth-ranked producer of cement. Poland February 16, 2007; the Energy Policy of Poland Until 2030 was the world’s second-ranked producer of rhenium, seventh- of November 10, 2009; and the Act on Tax on Extraction of ranked producer of feldspar (tied with the Republic of Korea Certain Minerals of March 2, 2012 (Rutkowska-Subocz, 2012; and Spain) and helium, eighth-ranked producer of peat and Library of Congress, 2013). silver, and ninth-ranked producer of selenium (not including the United States). Other commodities, such as lime, nitrogen Production (ammonia), salt, industrial sand and gravel, and sulfur were also In 2016, the production of bentonite increased by 120% produced in significant quantities (Central Statistical Office of to 1,000 metric tons (t); gold, by 30.9% to 3,539 kilograms; Poland, 2017, p. 755, 756; World Bank, The, 2017b; Anderson, synthetic gypsum, by 30.7% to 3,659,000 t; refractory quartzite, 2018; Apodaca, 2018; Bennett, 2018; Hamak, 2018; Polyak, by 17.5% to 64,500 t; and ferroalloys, by 15.3% to 90,699 t. -

Components of Comprehensive Income and Statement of Changes in Equity: an Analysis of Public Companies’ Reporting Practices in Poland and Germany Jacek Gad1

„Management and Business Administration. Central Europe” Vol. 23, No. 3/2015: p. 71–88, ISSN 2084-3356; e-ISSN 2300-858X Components of Comprehensive Income and Statement of Changes in Equity: An Analysis of Public Companies’ Reporting Practices in Poland and Germany Jacek Gad1 Primary submission: 24.06.14. Final acceptance: 27.04.15 Abstract Purpose: Identification of methods for presenting the components of other comprehensive income in the statement of changes in equity in the reporting practices of public companies in Poland and Germany. Methodology: A study of domestic and foreign literature was conducted with analysis of annual reports of public companies. The study followed the method of induction and to analyse the results, the structure similarity index was used. Results: The results of the study supported conclusions that the companies under study had not developed a uniform presentation of the components of comprehensive income in their statements of changes in equity. Five options of presenting the components of other comprehensive income in the statement of changes in equity were identified. Companies both from the WIG 30 and DAX indices most frequently presented the statement of changes in equity in option 1, which consisted of presenting the total comprehensive income item in a row and detailed items of equity in columns in which capital gains and losses were recognized. The differentiated forms of presenting the components of comprehensive income made it difficult to compare financial statements. Scope of research: The survey examined the annual reports of the largest Polish and German public companies respectively from the WIG 30 and DAX indices. -

PKN Orlen & Lotos

Tuesday, February 13, 2018 | special comment PKN Orlen & Lotos: Merger Rumors Revisited PKN Orlen (PKN PW) | Rating: sell | target price: PLN 82.84 | current price: PLN 95.04 Lotos (LTS PW) | Rating: reduce | target price: PLN 52.67 | current price: PLN 57.30 Analyst: Kamil Kliszcz +48 22 438 24 02 The PKN-Lotos merger rumors that have flared up share (at the current price level Lotos is trading about again over the recent days have so far not had much 18% above the 6-month swap ratio). Assuming all Lotos bearing on either stock as the market waits for any shareholders register to sell their shares to PKN in the concrete developments. Nevertheless, we thought it likely tender offer, the State's direct and indirect holdings would be worth exploring the possible scenarios and in the merged company would be 36.2%. If only the State outcomes of a merger between Poland's two largest sells its shares to PKN, its stake in the merged company state-controlled refiners. It is hard to say which type would be 39.5%, giving rise to a need to hold a tender of transaction would be best for whose minority offer to increase holdings to 66%. shareholders, but in terms of voting powers it is the minorities of PKN that can probably expect to be ■ A merger by absorption requires approval by a fourth- offered some form of an incentive, in the form of a fifths majority if the acquirer is Lotos or a 90% majority favorable swap ratio, to approve a potential stock-for- vote if the acquirer is PKN.