Shawbrook Group

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Ritz London, 16Th November 2016 by Invitation Only Confidential – Not for Distribution

® The Ritz London, 16th November 2016 By Invitation Only The AI Finance Summit is the world’s first and only high-level conference exploring the impact of Artificial Intelligence on the financial services industry. The invitation-only event, brings together CxOs from the world’s leading banks, insurance companies, asset management organisations, brokers. The event takes place at London’s most prestigious address, The Ritz, on the 16th of November and features world-class speakers presenting exclusive case studies shedding light into how the 4th industrial revolution will affect specifically affect the financial services industry. DRAFT AGENDA 16tH November 2016, The Ritz London 08:30 Registration, Breakfast refreshments & Networking 09:15 A welcome unlike any other… and Chair’s Opening Remarks 09:20 State of Play opening keynote: the 4th industrial revolution in financial services Where are financial services currently at with artificial intelligence, what technologies in particular are being used, how quickly is it being adopted, and what areas are leading the adoption of new intelligent technologies? These are are some of the pivotal questions answered in the scene-setting opening keynote to the AI Finance Summit. 09:45 Introducing a new era of risk management in investment banking The use of artificial intelligence within the world of investment banking is a phenomenon which is going to propel the industry in more ways than one. This talk will discuss how the advent of AI technologies, focusing on machine learning and cognitive computing, will drastically enhance risk management processes and achieve levels of accuracy previously unseen in the industry 10:10 Customer Experience/ Relations Management through AI platforms AI is revolutionizing customer service across every industry, with financial services already a pioneer in adoption. -

Shawbrook Group Plc Annual Report & Accounts 2017

Shawbrook Group plc Annual Report & Accounts 2017 Proudly different Proudly different Word Contents Strategic report The Strategic report provides readers with a holistic picture of Shawbrook’s business model, strategy, 2017 performance and future prospects. 1 The difference in being different 2 Basis of preparation 4 Our business 6 Chairman’s statement 7 Chief Executive Officer’s statement 9 Our strategy 10 Our business model 12 Business review 24 Risk management report 42 Corporate social responsibility Corporate governance report In this section we set out our commitment to the highest standards of corporate governance in line with UK best practice, our approach to remuneration and Directors’ Responsibilities. 47 Corporate governance report 50 Board of Directors 76 Directors’ Remuneration Report 81 Directors’ report 85 Statement of Directors’ responsibilities 86 Independent Auditor’s report Financial statements The financial statements comprise of the statutory financial statements and notes to the accounts for 2017. 94 Consolidated statement of profit and loss and other comprehensive income 95 Consolidated and Company statement of financial position 96 Consolidated statement of changes in equity 97 Company statement of changes in equity 98 Consolidated and Company statement of cash flows 99 Notes to the financial statements 167 Glossary shawbrook.co.uk twitter.com/shawbrookbank twitter.com/shawbrookbroker linkedin.com/company/shawbrook-bank The difference in being different Shawbrook is a growing UK specialist bank. Our approach to lending and savings is founded on the simple and good old-fashioned quality of good sense. What sets us apart is the deep relationships we develop with our customers and business partners. -

List of PRA-Regulated Banks

LIST OF BANKS AS COMPILED BY THE BANK OF ENGLAND AS AT 2nd December 2019 (Amendments to the List of Banks since 31st October 2019 can be found below) Banks incorporated in the United Kingdom ABC International Bank Plc DB UK Bank Limited Access Bank UK Limited, The ADIB (UK) Ltd EFG Private Bank Limited Ahli United Bank (UK) PLC Europe Arab Bank plc AIB Group (UK) Plc Al Rayan Bank PLC FBN Bank (UK) Ltd Aldermore Bank Plc FCE Bank Plc Alliance Trust Savings Limited FCMB Bank (UK) Limited Allica Bank Ltd Alpha Bank London Limited Gatehouse Bank Plc Arbuthnot Latham & Co Limited Ghana International Bank Plc Atom Bank PLC Goldman Sachs International Bank Axis Bank UK Limited Guaranty Trust Bank (UK) Limited Gulf International Bank (UK) Limited Bank and Clients PLC Bank Leumi (UK) plc Habib Bank Zurich Plc Bank Mandiri (Europe) Limited Hampden & Co Plc Bank Of Baroda (UK) Limited Hampshire Trust Bank Plc Bank of Beirut (UK) Ltd Handelsbanken PLC Bank of Ceylon (UK) Ltd Havin Bank Ltd Bank of China (UK) Ltd HBL Bank UK Limited Bank of Ireland (UK) Plc HSBC Bank Plc Bank of London and The Middle East plc HSBC Private Bank (UK) Limited Bank of New York Mellon (International) Limited, The HSBC Trust Company (UK) Ltd Bank of Scotland plc HSBC UK Bank Plc Bank of the Philippine Islands (Europe) PLC Bank Saderat Plc ICBC (London) plc Bank Sepah International Plc ICBC Standard Bank Plc Barclays Bank Plc ICICI Bank UK Plc Barclays Bank UK PLC Investec Bank PLC BFC Bank Limited Itau BBA International PLC Bira Bank Limited BMCE Bank International plc J.P. -

Confirmed Presenters & Chairs Patrick Brusnahan, Editor, Private Banker

Confirmed Presenters & Chairs Patrick Brusnahan, Editor, Private Banker International David Durlacher, Chief Executive Officer, Julius Baer International Duncan MacIntyre, Chief Executive Officer UK, Lombard Odier Stéphane Monier, Group Managing Director & Chief Investment Officer, Lombard Odier Salman Haider, Managing Director, Head of Global Growth Markets, Barclays Private Bank Gregory Perdon, Co-Chief Investment Officer, Arbuthnot Latham & Co. Sharon Maguire, Chief Customer Officer, C.Hoare & Co. Samuel Brown, Strategy Director – Strategy, Sustainability & Innovation, Coutts & Co. Patrick Thomas, Investment Director, Canaccord Genuity Wealth Management Antonio Curia, Executive Director & Head of Economic Research Unit, Wimmer Financial LLP Guy Healey, Head of Private Banking, Brown Shipley James Longstaff, Head of Innovation & Delivery, Shawbrook Bank Damian Payiatakis, Head of Impact Investing, Barclays Private Bank Charles Radclyffe, Former Head of AI, Fidelity International Ravi Sidhoo, Managing Director – Private & Business Banking, Cynergy Bank Private Banking and Wealth Management 11 June 2020 Full Day Programme 08:00 – Registration and Welcome Refreshments 09:30 Welcoming Remarks 08:30 - 08:40 Patrick Brusnahan, Editor, Private Banker International SESSION ONE: Global Market Challenges & Opportunities 08:40 – QE Infinity: Are We Walking into Another Financial Crisis? 09:05 A brief step through time to determine historical context Analysing triggers and causes of concern which may cause doubts on the future of QE Sharing -

Annual Report & Accounts 2015

SHAWBROOK GROUP PLC Annual Report & Accounts for the year ended 31 December ReportAnnual 2015 ended for the year 31 & Accounts SHAWBROOK GROUP PLC ANNUAL REPORT & ACCOUNTS FOR THE YEAR ENDED 31 DECEMBER 2015 SHAWBROOK IS A SPECIALIST LENDING AND SAVINGS BUSINESS WITH A FOCUS ON POORLY- SERVED CUSTOMER SEGMENTS ACROSS THE SME AND CONSUMER MARKETS IN THE UK. WE USE OUR EXPERIENCE AND JUDGEMENT TO MAKE INDIVIDUAL DECISIONS THAT BALANCE RISK, RETURN AND CUSTOMER NEEDS. SHAWBROOK COMPLETED ITS SUCCESSFUL IPO AND LISTED ON THE LONDON STOCK EXCHANGE IN APRIL 2015 (LSE:SHAW) A FULL VERSION OF OUR ANNUAL REPORT AND PILLAR 3 REPORT ARE AVAILABLE ONLINE AT WWW.SHAWBROOK.CO.UK CONTENTS STRATEGIC REPORT 01 Highlights 02 At a glance 04 History and Background 08 Chairman’s Statement 10 Q&A with the CEO and Interim CEO/CFO 14 Market Overview 17 Our Strategy 18 KPIs 20 Business Model 24 Business Review 32 Risk Management Report 43 Corporate Social Responsibility CORPORATE GOVERNANCE 45 Corporate Governance Report 48 Board of Directors 67 Directors’ Remuneration Report 82 Statement of Directors’ Responsibilities 83 Directors’ Report FINANCIAL STATEMENTS 87 Independent Auditor’s Report 90 Consolidated Statement of Profit or Loss and Other Comprehensive Income 91 Consolidated and Company Statements of Financial Position 92 Consolidated Statement of Changes in Equity 93 Company Statement of Changes in Equity 94 Consolidated Statement of Cash Flows 95 Notes to the Financial Statements 131 Glossary STRATEGIC REPORT GOVERNANCE FINANCIALS HIGHLIGHTS A RECORD YEAR -

Proudly Different Proudly Different Word

Shawbrook Group plc Annual Report & Accounts 2017 Proudly different Proudly different Word Contents Strategic report The Strategic report provides readers with a holistic picture of Shawbrook’s business model, strategy, 2017 performance and future prospects. 1 The difference in being different 2 Basis of preparation 4 Our business 6 Chairman’s statement 7 Chief Executive Officer’s statement 9 Our strategy 10 Our business model 12 Business review 24 Risk management report 42 Corporate social responsibility Corporate governance report In this section we set out our commitment to the highest standards of corporate governance in line with UK best practice, our approach to remuneration and Directors’ Responsibilities. 47 Corporate governance report 50 Board of Directors 76 Directors’ Remuneration Report 81 Directors’ report 85 Statement of Directors’ responsibilities 86 Independent Auditor’s report Financial statements The financial statements comprise of the statutory financial statements and notes to the accounts for 2017. 94 Consolidated statement of profit and loss and other comprehensive income 95 Consolidated and Company statement of financial position 96 Consolidated statement of changes in equity 97 Company statement of changes in equity 98 Consolidated and Company statement of cash flows 99 Notes to the financial statements 167 Glossary shawbrook.co.uk twitter.com/shawbrookbank twitter.com/shawbrookbroker linkedin.com/company/shawbrook-bank The difference in being different Shawbrook is a growing UK specialist bank. Our approach to lending and savings is founded on the simple and good old-fashioned quality of good sense. What sets us apart is the deep relationships we develop with our customers and business partners. -

Shawbrook: Doing the Right Thing Chris Richold, MD – Specialist Asset & Sector Finance, Shares Shawbrook’S Proactive Approach CONTENTS

VOL 13 I NO 150 I JULY 2020 FOR THE UK EQUIPMENT LEASING AND ASSET FINANCE PROFESSIONAL Shawbrook: doing the right thing Chris Richold, MD – Specialist Asset & Sector Finance, shares Shawbrook’s proactive approach CONTENTS IN THIS ISSUE 10 Motor Finance News PUBLISHER LeasingWorld Ltd Oakhill House Uphampton Droitwich Spa Worcs. WR9 OJR, UK 24 Managing in the age of Covid 18 If you think training is expensive, try ignorance E: [email protected] www.leasingworld.co.uk Published by LeasingWorld Ltd NEWS REGULARS Company No: 5387699. ISSN 1749-3501 UK NEWS DATABANK Printed in England by Pensord, 4 Asset finance market falls by 60pct in May 2020 26 UK new business finance May 2020 Tram Road, Pontllanfraith, 4 Multiple lenders approved for loan schemes Blackwood NP12 2YA CITY CHATTER 5 British Business Bank appoints Interim CEO 28 Old Moore Looks Back No part of this publication may be 6 White Oak exceeds £30m in CBILS loans resold, reproduced or transmitted in 6 SMEs expect to borrow £48bn BACK IN THE OFFICE any form or by any means, electrical, 7 Close Brothers funds assets for state-of-the-art 29 Stop Press: Customer Service Excellence 2020 Awards mechanical, photocopying, recording composting facility or otherwise without the prior written EVENTS 9 Aldermore offers CBILS for invoice finance permission of the publisher. 30 Leasing Events Calendar 2020/21 LeasingWorld Ltd, Oakhill House, 9 SFS appoints Graham Leaney Uphampton, Droitwich Spa, Worcs WR9 0JR. MOVES MOTOR FINANCE NEWS 31 A roundup of who has moved where SUBSCRIPTIONS -

Best Buys Data Supplied By

54 1G M Saturday April 14 2018 | the times Money Best buys Data supplied by Savings Mortgages Personal loans Easy access (without introductory bonus) First-time buyer mortgages Fixed monthly repayment on £10,000 for 5 years Provider Contact Account Min AER Redmptn (without insurance) Provider Contact Initial Period Max Fee Charge Rep Amount per Total RCI Bank UK A rcibank.co.uk Freedom Savings £100 1.30% Rate LTV Until Provider Contact APR month repaid Shawbrook Bank shawbrook.co.uk Easy Access - Issue 11 £1,000 1.25% Monmouthshire BS 0845 888 8000 2.99% D for 2 years 95% £150 1st 2 yrs M&S Bank 0800 363400 2.8% £178.64 £10,718.40 Ford Money fordmoney.co.uk Flexible Saver £1 1.22% West Brom BS 0800 298 0008 3.39% F to 31.5.20 95% - To 31.5.20 Sainsbury's Bank 0800 169 8503 2.8% £178.64 £10,718.40 Kent Reliance kentreliance.co.uk Easy Access - Issue 25 £1,000 1.21% Melton Mowbray BS 01664 414141 2.79% D for 3 years 95% - 1st 3 yrs Yorkshire Bank 0800 707 6471 2.8% £178.64 £10,718.40 Virgin Money virginmoney.com Double Take E-Saver 5 £1 1.20% Yorkshire Bank 0800 202122 3.59% F to 30.6.21 95% - 1st 3 yrs John Lewis FS 0345 266 1380 2.9% £179.07 £10,744.20 Long-term fixed rates Yorkshire Bank 0800 202122 3.89% F to 30.6.23 95% - 1st 5 yrs Borrowing rates and availability of products are subject to individual credit ratings. -

UK & EU Unsupported Banks

UK & EU Unsupported Bank List EU Unsupported Banks (Bank and Credit Cards only) UK Unsupported Banks (Bank and Credit Cards only) ABANCA (Business) (Spain) - Bank AA credit card (UK) ABANCA (Spain) - Bank AA Savings (UK) - Bank ABN AMRO (Netherlands) - Bank Abbey National (UK) - Credit Card ABN Amro Business Credit Card (Netherlands) Adam & Company (UK) - Bank Activo Bank (Portugal) Airdrie Savings Bank (UK) ActivoBank (Espana) - Banco Aldermore Business Bank (UK) Allied Irish Bank (Business) (Ireland) - Bank Aldermore Savings (UK) - Bank Allied Irish Bank (Business) (Ireland) - Credit Card Alliance & Leicester (UK) - Bank Allied Irish Bank (Ireland) - Bank Alliance & Leicester (UK) - Credit Card Allied Irish Bank (Ireland) - Credit Card Alliance Trust Savings (UK) - Bank American Express (Card Account) (Espana) - Tarjeta de Allied Irish Business Bank (UK) - Bank Credito American Express Card Amazon Credit Card (UK) American Express Cards (France) - Bank American Express Business Cards (UK) American Express Cards (Switzerland) American Express Cards (global) (UK) - Credit Card American Express Cards (Switzerland) American Express Cards (UK) American Express Cards DUTCH (Netherlands) - Bank American Express Cards Mobile (UK) - Credit Card American Express cards(NL) (Netherlands) - Credit Card aqua card (UK) American Express Credit Cards (Spain) Arbuthnot Latham (Current Account) (UK) - Bank ASN Bank (Netherlands) - Bank Arbuthnot Lathum (UK) - Bank ASN Bank (Netherlands) - Credit Card ASDA - Credit Cards (UK) AXA Banque (France) Bank of -

Direction for Modification by Consent of 5.1 to 5.3 and 5.5 of the Capital Buffers Part of the PRA Rulebook

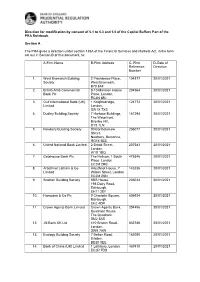

Direction for modification by consent of 5.1 to 5.3 and 5.5 of the Capital Buffers Part of the PRA Rulebook. Section A The PRA gives a direction under section 138A of the Financial Services and Markets Act, in the form set out in Section B of this document, to: A-Firm Name B-Firm Address C- Firm D-Date of Reference Direction Number 1. West Bromwich Building 2 Providence Place, 104877 20/01/2021 Society West Bromwich, B70 8AF 2. British Arab Commercial 8-10 Mansion House 204564 20/01/2021 Bank Plc Place, London, EC4N 8BJ 3. Gulf International Bank (UK) 1 Knightsbridge, 124772 20/01/2021 Limited London, SW1X 7XS 4. Dudley Building Society 7 Harbour Buildings, 161294 20/01/2021 The Waterfront, Brierley Hill, DY5 1LN 5. Newbury Building Society 90 Bartholomew 206077 20/01/2021 Street, Newbury, Berkshire, RG14 5EE 6. United National Bank Limited 2 Brook Street, 207381 20/01/2021 London, W1S 1BQ 7. Gatehouse Bank Plc The Helicon, 1 South 475346 20/01/2021 Place, London EC2M 2RB 8. Arbuthnot Latham & Co Arbuthnot House, 7 143336 20/01/2021 Limited Wilson Street, London EC2M 2SN 9. Scottish Building Society SBS House, 206034 20/01/2021 193 Dalry Road, Edinburgh, EH11 2EF 10. Hampden & Co Plc 9 Charlotte Square, 606934 20/01/2021 Edinburgh, EH2 4DR 11. Crown Agents Bank Limited Crown Agents Bank, 204456 20/01/2021 Quadrant House, The Quadrant, SM2 5AS 12. JN Bank UK Ltd 410 Brixton Road, 832786 20/01/2021 London, SW9 7AW 13. Ecology Building Society 7 Belton Road, 162090 20/01/2021 Silsden, BD20 0EE 14. -

Are You Getting Ready to Crawl out of Your Shell?

The Sunday Times April 29, 2018 17 MONEY Best Buys CURRENT ACCOUNTS FOREIGN MORTGAGES MONEY CREDIT INTEREST CURRENCY 2-YEAR FIXED RATES Provider Account name Account fee Interest rate 1 Balance Contact Lender Rate Scheme Deposit Fee Notes Contact MADE EASY These are the interbank TSB Classic Plus None 3% + £10 a month 2 £1-£1,500 0345 975 8758 Monmouthshire 1.34% Fixed for 2 years 35% £999 HR 0163 384 4351 INHERITANCE TAX rates at 5pm on Friday, Halifax Reward None £3 a month £1+ 0345 720 3040 which show where the HSBC 1.54% Fixed to 31.8.20 20% £999 LV 0800 494 999 Thousands of families Nationwide FlexDirect None 5% 3 £0.01-£2,500 0800 302 010 market is trading. Nationwide 1.89% Fixed for 2 years 10% £999 GLV 0800 302 010 have missed out on an They are not indicative inheritance tax break OVERDRAFTS * 3-YEAR FIXED RATES of the rate you will be intended to help people Provider Account name Account fee Interest rate 4 0% overdraft limit Contact able to get. Lender Rate Scheme Deposit Fee Notes Contact who pass on a family First Direct 1st Account £10 a month 5 15.9% £250 0800 242 424 HSBC 1.69% Fixed to 31.5.21 25% £999 LV 0800 494 999 home to their heirs, M&S Bank M&S Current Account None 15.9% £100 0345 900 0900 EURO Coventry 1.85% Fixed to 30.6.21 15% £999 LV 0800 121 8899 according to analysis by Post Office Money Standard Account None 14.9% £0 0345 266 8977 GBP>EUR Virgin Money 2.18% Fixed to 1.7.21 10% £995 LV 0345 605 0500 the insurer NFU Mutual. -

Market Intelligence

4th edition | july 2017 market intelligence A new year and a new economic beginning. Were you letting off introduction fireworks on 31st January or shedding a tear? Whatever your views, democracy seemed to be the real winner. Certainly our clients, who are a vibrant mix of international entities, seem happier and more confident given the closure and short term certainty this has provided. Yes, the transition period will be a difficult ride but recruitment wise the start of the year has begun in an encouraging manner. We have noticed 3 “hotspots” of activity, Credit Risk, Commercial Real Estate Finance and Trade & Commodity Finance respectively. As reported last quarter, the main concentration remains in the £50-80k basic salary level, so typically your Associate, Manager and AD levels. Turning to this quarters hot topic a big thank you as always for all your views and responses. We had a far higher number of responses than usual, apologies we can only publish a snapshot. In short summary while Mental Health issues are very real it appears that the Financial Services sector needs to do far more. Enjoy the piste – if you are heading to snowy peaks, and let’s hook up again at Easter (post bonus season)… when I’ll be wondering again… were you letting off fireworks or shedding a tear? These questions reflect our most common enquiries and quarterly survey so this regular feature is a chance to measure and share current market sentiment. Q1 Looking at the next quarter only, what Q2 ...and what is your outlook for the next is your personal outlook