The Healthcare Diagnostics Value Game the Challenges of Delivering and Demonstrating Value in Under-Pressure Markets Realizing Value Series

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

"General Print Mint" For

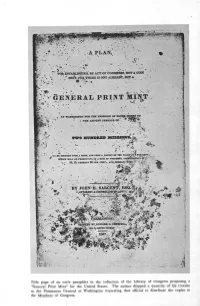

FOR ESTABLISIUWO, BY ACT OF CONOREBS,NOTA OWN 'MD4T, FOR THERE IS ONE ALREADY, BUT A W.3LUHOTON FOR THE EMISM9N OF PArkE MO r TO THE AMOUNT flRHAP& OF. - H TO 3Z SOUnDED UPON A ROCH, Afl UPON A CRfl)IT OF TLSYEAR$ATS !tVnYq: WHIOD WILL It PRODUCTIVIorARItOF PXOPEWET ILP -: - 10, 15, rztaa,. 20PZR CZRT., aflOflmflafl asx.t - E' -- :. BY EDWAn 0. OQflctLL, Title page of an early pamphlet in the collection of the Library of Congress proposing a "General Print Mint" for the United States.The author shipped a quantity of his treatise to the Postmaster General at Washington requesting that official to distribute the copies to the Members of Congress. HISTORY of the BUREAU of ENGRAVING and PRINTING 1862-1962 TREASURY DEPARTMENT Washington, D.C. For sale by the Superintendent of Documents, U.S. Government Printing Office Washington, D.C.20402.Price $7.00 CENTENNIAL HISTORY STAFF MICHAEL L. PLANT Office of the Controller ARTHUR BARON LOUISE S. BROWN Office of Office of Plant Currency and Stamp Manufacturing Facilities and Industrial Procurement JOHN J. DRISCOLL MICHAEL J. EVANS Internal Audit Staff Internal Audit Staff The Introduction, giving a brief history of the art of engraving and its application in American colonial and early Federal days, was prepared by Robert L. Miller of the Bureau's Designing Staff, Office of Engraving and Plate Manufacturing. II Foreword RE IDEA of publishing ahistory of the Bureau of Engraving and Printing to commemorate the centennialanniversary of its establishment was nurtured in the knowledge that a recitalof its accom- plishments was a story that well deserved the telling.It is not a subject that has been dealt with widely.Much of what has already appeared inprint concerning the Bureau is in the nature of guidebookmaterial or relates to its products, especially currency notes and stamps, ratherthan to the agency itself. -

2017 Palmares September 8-10, 2017 Newark, NJ

NOJEX 2017 Palmares September 8-10, 2017 Newark, NJ Grand and Large Gold: Best Exhibit in Show Hummel Post Coach “The Mail is Here” The 1903 Two Cent Washington Shield Issue Nicholas A. Lombardi and also U.S. Stamp Society Statue of Freedom Award, Sidney Scheider Memorial Award- Best Exhibit by North Jersey Federated Stamp Club Member, Best United States Sectional Award Reserve Grand and Large Gold: Second Best Exhibit in Show Postal History of Salem, Mass Domestic Mail through Sept.1883 (Act of 1863), Foreign Mail Up to U.P.U. Mark S. Schwartz Single Frame Grand and Large Gold Boston's "PAID in Grid" Cancels on the U.S. Imperforate Issues of 1847-56 Mark S. Schwartz Court of Honor Fighting the Fed in Philadelphia; Local poats, Independent Mails 1835-1868 Vernon R. Morris Along the Shantung Railway, China: German Postal Administration 1900-1966 Louis P. Pataki Boyd’s Local Post- New York City 1844-1911 Martin Richardson Multiframe Large Gold Alternative Ways Letters were Carried by Private Individuals and Companies from the Colonial Period to 1851 Clifford Alexander and also American Association of Philatelic Exhibitors Creativity Award, Postal History Society Medal Irish Coil Stamps 1922-1940 Robert M. Benninghoff and also American Philatelic Society Medal of Excellence, 1900-1940 Prominent Americans Series Roger S. Brody and also Auxiliary Marking Club Award, Errors, Freaks and Oddities Society Award Wei Hai Wei, China, 1896-1949 Sam G. Chiu The Era of the French Colonial Group Type; The French Pacific Colonies Edward J. J. Grabowski Major Croatian Postal Rates: 1941-1945 Henry Laessig and also American Philatelic Society Medal of Excellence, 1940-1980 The Private Post set the example for mail handling in the U.S. -

United States Columbian Exposition Issue of 1893

United States Columbian Exposition Issue of 1893 Bill Gustafson A set of mint Columbian Exposition stamps from my US mint collection -1- Columbian Exposition Issue The first commemorative stamps issued in the United States were printed for the World’s Colombian Exposition held in Chicago, Illinois from May 1 to October 30, 1893. This Exposition celebrated the 400th anniversary of the discovery of America by Christopher Columbus. There was some controversy over the initial printing of these stamps. Printing contracts required the printing companies to go out to bid. However, the Postmaster John Wanamaker executed a new contract with the American Banknote Company for the printing of the Colombian stamps without any competitive bidding process. This allowed the company to charge 17c per thousand stamps in contrast to the 7.45c per thousand rate charged for the 1890 definitive series. The Columbian issue was the last set of stamps to be printed by a private company for many years. During early 1894, the American Bank Note Company failed to secure a renewal of its stamp contract because the U.S. Bureau of Engraving and Printing submitted a lower bid. The Bureau then had a monopoly on US. Stamp production until 1944 when a private company produced the Overrun Countries series, which required special multicolor printing. Fifteen denominations of the series were placed on sale on Monday, January 2, 1893. They were available nationwide, not restricted to the Exposition. This was the largest number of stamps ever offered in a single series with the unprecedented inclusion of stamps with denominations of $1, $2, $3, $4 and $5. -

2014 Philatelic Palmares

CHICAGOPEX 2014 Palmares November 22, 2014 Grand - President's Award Jerzy Kupiec-Weglinski Air Mail in the Polish Territories (1914-1939) Reserve Grand - Felix Ganz Award Robert Puchala Cracow Issue 1919 Single Frame Grand Richard D. Bates, Jr. How Errors and Varieties Arose on Flat Press U.S. Stamps Overprinted CANAL ZONE COURT OF HONOR EXHIBITS Dr. James Mazepa Poland: 1918-1919 First and Second Warsaw Provisional Issues Jacek Kosmala Aerial Formations of the Gen. Haller "Blue" Army and the French Military Mission in Poland 1917-1923 Dr. James Mazepa The Poland Stamp of the U.S. Overrun Countries Series: 1943 MULTI-FRAME EXHIBITS Gold Richard Larkin Booklet Panes and Covers-United States and Possessions 1900-1945 Slawomir Chabros Correspondence of Polish Legions 1914-1917 Dr. Robert B. Pildes Artists' Drawings, Essays and Proofs and Associated Material of the 1948 Do'Ar Ivri Issue of Israel Marek Zbierski Polish Postal Rates May 1924 - September 1939 George Zelwinder "Groszy" Provisional Issues of Poland 1950-52 and Their Use Louis Fiset Mail Between USA and France 1939-1945 Gerald Menge General Gouvernement Protectorate Semi-Postal Issues Alfred F. Kugel Polish Forces in Exile During & Following World War II Robert Schlesinger The 1938 Presidential Issue-A Survey of Rates Robert Puchala Cracow Issue 1919 Ryszard Prange Basketball Report - I Love This Game Kathryn L. Johnson Senegal: French Colonial Africa 1914-1940 Alexander Kolchinsky The Mail of Leningrad Blockade Tom Brougham Canal Zone Overprints on Panama's 1909 ABNC Portrait Designs Jerzy Kupiec-Weglinski Air Mail in the Polish Territories (1914-1939) Kathryn J. -

N.S.S.S. Meets on the 2Nd and 4Th Saturday of Each Month at 10:00 Am in the Sparks Heritage Museum at Pyramid and Victorian Avenue

Nevada P.O. Box 2907 Sparks, Nevada 89432 N.S.S.S. meets on the 2nd and 4th Saturday of each month at 10:00 am in the Sparks Heritage Museum at Pyramid and Victorian Avenue Stamp Study Society N.S.S.S. POST BOY May 8, 2004 In my rush to publish the Post needed. Boy in a timely manner after We had a couple of visitors at the President: Stan Cronwall returning from my vacation, I made a last meeting. Jim May was there with 10000 Blue Spruce Dr., couple of errors. I would like to a UN collection he wanted to dispose Reno, NV 89511 correct them now. It is Duane of. Any takers? Xena (Hope that’s (775) 849-7850 Wilson, not Wayne that is in charge right), who inherited an old collection Vice President: Jim Ringer of producing the show cancellations. may be joining us soon. Maybe we 605 E. Huffaker Ln., The second error was not giving can encourage her. Reno, NV 89511 credit for the program from March. Stan Cronwell will be doing a (775) 853-3137 My apologies to Duane Wilson and commercial for Frank Fey’s place, the Secretary/Editor: Ed Davies. Liberty Belle. Can’t wait to see it. Is Nadiah Beekun 2560 Howard Dr. The program in March was given this going to be on TV Stan? Sparks, NV. 89434 by Ed Davies and was called Elections are coming up soon. (775) 355-1461 “Expanding Your Collection”. Ed Installation of the new officers will be Treasurer: continued the program in April. -

VOL. LXIV WASHINGTON 25, D. C, FRIDAY, OCTOBER 1, 1943 No

Published Tuesday and Friday, ex- For the information and guidance cept legal holidays, by direction of el officers and employees of the the Postmaster General postal bulletin Postal Service VOL. LXIV WASHINGTON 25, D. C, FRIDAY, OCTOBER 1, 1943 No. 18654 ORDER OF INSTRUCTIONS OF THE POSTMASTER GENERAL THIRD ASSISTANT POSTMASTER GENERAL COMMEMORATIVE STAMPS—OVERRUN COUNTRIES YUGOSLAVIA—ALBANIA—AUSTRIA—DENMARK POSTAL BULLETIN Frequency and Days of Issue Postmasters and employees of the Postal Service are advised that the remaining 5-cent postage stamps of the Overrun Countries Series, honoring Effective October 1, 1943, the POSTAL BULLETIN will be issued twice Yugoslavia, Albania, Austria, and Denmark, will be placed on sale at the a week, each Tuesday and Friday, in lieu of the present frequency, Monday, Washington, D. C, post office, as indicated herein. The central designs Wednesday, and Friday. portray the flags of the respective countries in natural colors, with the name Due to necessity for postmasters at fourth-class post offices to keep of the country appearing underneath the flag. current on the many changes affecting service at their offices a copy of each issue will be mailed to them direct. Country Colors of flag First-dap sale Yugoslavia Blue, white, and red Oct. 26,1943 Albania Red field with black emblem , Nov. 9,1943 CHRISTMAS MAIL FOR MEMBERS OF ARMED FORCES OVERSEAS Austria Red, white, and red Nov. 23,1943 Attention is directed to»the information in the POSTAL BULLETIN of June Denmark Red and white Dec. 7,1943 28, 1943, concerning Christmas mail for our armed forces overseas. -

Post Boy June 2016 Volume 49, Issue 6

Post Boy June 2016 Volume 49, Issue 6 MEETS THE 2ND & 4TH SATURDAY OF EACH MONTH AT 10:00 AM AT THE SILVERADA ESTATES CLUBHOUSE LOCATED AT 2301 ODDIE BLVD., RENO Officers: President and Editor Comments: President - John Walter [email protected] I'm still recovering from attending two large stamp shows in the past month. Vice President - Gary Atkinson First was WESTPEX which I attended from April 29 to May 1 in Burlingame, CA. [email protected] I attended the meeting of the Council of Northern California Philatelic Societies, Secretary - Howard Grenzebach of which we are a member. I'm a member of the United Postal Stationery [email protected] Society and attended their general meeting. Treasurer - Mike Potter [email protected] I just returned from the World Stamp Show 2016 in New York. This was my first international show and even with five days at the show did not see Directors: everything. I only attended one of the seven first day ceremonies. I did George Ray volunteer 6 hours at the front registration desk which gave me the opportunity Steve Foster to speak with people from both the U.S. and several overseas countries. Three [email protected] specialty association meetings were attended and a few other seminars. Paul Glass Wearing my NSSS shirt made me stand out and a few APS employees spoke [email protected] with me about the winter show in Reno. In particular, Jay Bigalke and I Nadiah Beekun [email protected] discussed an article for the American Philatelist about Reno or silver mining for Harvey Edwards an issue before the Reno show. -

USA ; Postal Markings ; Wierenga, T

Number Subject Author Title Date # Pages 3073 USA ; Postal Markings ; Wierenga, T. "New York/2" and "Printed Circular" Markings. 1980 2 pp. 10379 USA : Maritime Mail ; Canal Boat Mail ; Moore, Edward N. Canal Boat Mail. 23-Apr-05 1pp, ill 10466 USA : Postal History ; Griffiths, John O. Postal History Development in the Old North and Southwest Territories. 1990 13pp, ill 10059 USA : Precancels ; Washington Bureau ; Gunesch, Adolf U.S. Precancels. Washington Bureau Precancels. 1965, 1pp, ill 3319 USA : Registered Mail ; Norona, D. A First Year Registered Letter Return Receipt. 1935 1p. 2713 USA ; Brooks, K. L. Mark Hopkins, Teacher. 1940 1:00 PM 3447 USA ; Postal History ; Milgram, J. W. A Much-Traveled Cover. 1976 1p., ill. 2757 USA ; Specialized ; 1939 ; Varieties ; Printing Crafts Plate Varieties. (Scott 857) 1939 1:00 PM 10318 USA ; Specialized-1908 ; Schumacher, Paul Complex History Makes 519a Treasured Stamp. 3-Apr-93 1pp, ill 7998 USA ; 17th Century ; Postal History ; York, N. D. The 17th Century Posts. 1959 1p. 3436 USA ; Aerogrammes ; Varieties ; Errors ; Post, E. E. More Miscut Aerogrammes. 1974 3pp., ill. 10192 USA ; Air Mail - History ; Ragsdale, Capt. Carl V. The Saga of the NC-4. May-87 4pp, ill 194 USA ; Air Mail ; Singley, R. L. Trans-Pacific Airmail. 1964 17 pp. ill. 195 USA ; Air Mail ; Amick, G. Spectacular Failures of Airmail Pilot Boyle. 1986 3 pp. ill. 198 USA ; Air Mail ; Faries, B. On The Record. Robert H. Goddard. 1965 6 pp. ill. 422 USA ; Air MAil ; Silver, P. Knowledge and "Cheapies". (Flights from 1919 to 1924) 1981 3 pp. -

2017 4Th Quarter

The Philatelic Communicator Journal of the American Philatelic Society Writers Unit #30 -30- www.wu30.org Fourth Quarter 2017 Issue 198 In Paris, Passion Battles the Decline of Stamp Collecting The New York Times / By ELAINE SCIOLINO OCT. 18, 2017 Myself, a long time New York Times reader, did not Arrondissement (district) has long been the city’s see this article with my morning tea on October stamp district. There are reportedly about 30 stamp 18th. That story and its section was whisked out of shops that line the Rue Drouot near the Hôtel the house by my dear Drouot, one of the wife as she went to world’s oldest auction work. She does that all houses. the time. Gene Fricks There are also a few sent me a copy. That’s more shops in the the main reason I got to Passage des Panora- read it. The Times would mas in the Second be happy to allow me to Arrondissement as reprint that article but well as a few more the price would be a bit shops in the Eighth high for our small Arrondissement. group. I somewhat fear There used to be even using the photos many more dealers in they published. So I the Carré Marigny, an Parisinfo.com found a couple of simi- open air court that lar photos from Google was donated to the Images that might be city in 1860 to be used safe enough. IFSDA, for stamp dealers. It is the International Feder- still busy on weekends ation of Stamp Dealers but certainly not as Associations, reprinted much as even a few the article at their site decades ago. -

Totaloversikt Verdensdeler-Net.Indd

OVERSIKT OSLO FILATELIST- KLUBB BIBLIOTEK 27. Desember 2019 1 Denne siden er blank 2 INNHOLDSFORTEGNELSE: INNHOLDSFORTEGNELSE ............................................................................................. 3 NORGE ............................................................................................................................... 4 NORDEN: DANMARK ........................................................................................................................... 19 DANSK VEST INDIA ............................................................................................................ 26 FINLAND ............................................................................................................................. 26 FÆRØYENE ........................................................................................................................ 28 GRØNLAND ........................................................................................................................ 29 ISLAND ................................................................................................................................ 30 SVERIGE ............................................................................................................................. 31 ÅLAND ................................................................................................................................. 37 EUROPA ............................................................................................................................. -

The Philatelic Communicator Journal of the American Philatelic Society Writers Unit #30

The Philatelic Communicator Journal of the American Philatelic Society Writers Unit #30 -30- www.wu30.org Third Quarter 2018 Issue 201 Plea for Support of Literature Exhibits Bill DiPaolo Reviewing the palmares of this country’s two remaining Are they unmoved by recognition of their peers? Are they not philatelic literature competitions, CHICAGOPEX and interested in objective evaluation that could possibly improve StampShow, a couple things pop out. The first is that it is a future work? Do they feel their work not important enough? real accomplishment to win a large gold or Ask fellow collectors to name the top three gold medal at one of these events. They are not critical areas of APS. Almost certainly the seen as frequently as in philatelic exhibits. The library would be on that list and for many, it second is how few shorter articles are entered would be at number one. For philatelic au- in these competitions. Books, catalogs and thors, the library shelves provide a place for yearly runs of society journals predominate. the lasting, tangible legacy authors have left While some journal articles are submitted, they for our hobby, for our passion. Though a part tend to be overshadowed by their more volu- of APS, it would be a positive step if the minous cousins and, as a result, not often rec- APRL would take a more dynamic role in the ognized for their research contributions, inter- participation and promotion of literature ex- est generated for our hobby nor the quality of hibits. the presentation. The situation is not unlike the Writers Unit 30 and the Sarasota National problems once encountered by one frame phil- Bill DiPaolo, Stamp Exhibition are stepping up to try to atelic exhibits when forced to be evaluated Exhibit Chairman brighten the light on the literature aspect of next to multi-frame exhibits telling a larger our hobby by offering a venue exclusively for philatelic story. -

16Th NEW ZEALAND PHILATELIC LITERATURE EXHIBITION 2019

16th NEW ZEALAND PHILATELIC LITERATURE EXHIBITION 2019 Hosted by the Christchurch (NZ) Philatelic Society Inc 28 September, 2019 Philatelic Centre, Christchurch, New Zealand INTRODUCTION Following on from what was deemed to be a successful 15th New Zealand National Philatelic Literature Exhibition in 2017, the Christ- church (NZ) Philatelic Society (CPS) applied for and was granted authority from the New Zealand Philatelic Federation to host this 16th edition of our national specialist literature exhibition. Previous exhibitions had been mainly organised by the Central Districts Philatelic Trust. The CPS was founded in 1911 and has been an active society since that time. For many years it has seen both it’s library facility and it’s monthly newsletter “Captain Coqk” as key assets in providing a service for it’s members. To therefore be involved in the specialist literature exhibition is but a small extension of where our efforts are concentrated. The CPS is a shareholder in the ownership of the Philatelic Centre in Christchurch which gives us a significant permanent space for our extensive library which includes not only catalogues, monographs, and periodicals, but the research archives of a number of well known New Zealand philatelists. The CPS team that worked to organise this event was; The Judges group were: Paul van Herpt, Chairman Jeff Long, Chairman Murray Clark, Secretary Dr Ross Marshall Karen Jeffrey, Treasurer Alan Tunnicliffe Jeff Long, Jury Chairman John Campbell, Apprentice assisted by the Executive Murray Clark, Secretary committee of the CPS The team’s efforts were well supported by the considerable number of philatelic colleagues from around the world who so willingly submitted their entries which in many cases was at some cost to get to New Zealand.