Taking Stock a Strategic Housing Market Assessment Part 5 - Size, Type and Tenure

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Lakes Andand Aleale

Edition 71 FREE Summer 2018 Westmorland CAMRA Branch Magazine LAKESLAKES ANDAND ALEALE Hawkshead’s brand new, state of the art £3 million Krones 40bbl turnkey brew kit see page 27. www.camrawestmorland.org Follow CAMRAWestmorland on Twitter @ lakes_and_ale Find us on Facebook CAMRA Westmorland Use new Hawkshead in Printers file please; destroy all others 2 EDITORIAL Welcome to the new summer edition of Lakes & Ale. There have been some significant changes to the ranks of Westmorland Branch Officers and we extend a warm welcome to all those who have generously volunteered to help continue the work of CAMRA in the area. We must also thank those officers who for various reasons have retired from their posts. They include Marilyn Molloy who for many years has been a stalwart of the Branch but who now, after some hospital operations, wishes to spend more well earned time with Mike. Also we say goodbye to Caroline Schwaller who has been a truly dedicated member of the Branch this last few years and also we learn that our Webmaster Dave Brown will need to leave post in the near future. They will be hard to replace. This is also a poignant moment for me as, after some ten very enjoyable years as Editor, I find that a combination of the increasing effects of Parkinson’s coupled with eyesight problems makes it more than time to call it a day. I am happy to see that we have an admirable replacement in Jodie Duxbury who has all the necessary technical skills to deal with Microsoft Publisher and no doubt she will have much support from our printer Howard Duff at Kent Valley. -

OSTA Tour of England and Scotland a Success

OSTA Tour of England and Scotland a Success By David Fallowfield Eleven US members of the Old Spanish Trail Association have now returned home after enjoying 10 days of touring in Cumbria and adjoining counties in England and Pictured at Carlisle Scotland from June 26 through Castle, the tour mem- July 5. The group was mainly bers were: L to R: Dr. based at B and B's in Penrith (six Don Rowland, Jean Rowland, Dennis nights) and for three nights in Ditmanson, Carole Dit- Scotland at Moffat and Dryburgh. manson, Joshua Hall, They were here at the invitation OSTA President Ashley of members of the local William Hall, Stuart Hall, Judy Workman Chapter of the Associa- Nickle, Jerry Nickle, Dr. Reba Grandrud and tion, who over eight years have at- Colin Benge. tended conferences in the USA and encouraged the members there to come to Britain. They came from California, Arizona, New Mexico group viewed the Workman grave- was Mary Workman of Brown and Nevada and included the Na- stones in the churchyard of St. Howe Farm, Melkinthorpe. The tional OSTA President, Brigadier Cuthbert’s church. Others in the Fallowfield coat of arms can be General Ashley Hall, who travelled group were Dr. Reba Wells Gran- seen in the east window of Clifton with his two grandsons Joshua drud accompanied by her son Co- Church, and David’s brother Alan, and Stuart. Also in the group was lin Benge from New Mexico, Jerry also of Penrith, was the last con- a descendant of the pioneering and Judy Nickle from Arizona, and stable of Clifton. -

Index to Gallery Geograph

INDEX TO GALLERY GEOGRAPH IMAGES These images are taken from the Geograph website under the Creative Commons Licence. They have all been incorporated into the appropriate township entry in the Images of (this township) entry on the Right-hand side. [1343 images as at 1st March 2019] IMAGES FROM HISTORIC PUBLICATIONS From W G Collingwood, The Lake Counties 1932; paintings by A Reginald Smith, Titles 01 Windermere above Skelwith 03 The Langdales from Loughrigg 02 Grasmere Church Bridge Tarn 04 Snow-capped Wetherlam 05 Winter, near Skelwith Bridge 06 Showery Weather, Coniston 07 In the Duddon Valley 08 The Honister Pass 09 Buttermere 10 Crummock-water 11 Derwentwater 12 Borrowdale 13 Old Cottage, Stonethwaite 14 Thirlmere, 15 Ullswater, 16 Mardale (Evening), Engravings Thomas Pennant Alston Moor 1801 Appleby Castle Naworth castle Pendragon castle Margaret Countess of Kirkby Lonsdale bridge Lanercost Priory Cumberland Anne Clifford's Column Images from Hutchinson's History of Cumberland 1794 Vol 1 Title page Lanercost Priory Lanercost Priory Bewcastle Cross Walton House, Walton Naworth Castle Warwick Hall Wetheral Cells Wetheral Priory Wetheral Church Giant's Cave Brougham Giant's Cave Interior Brougham Hall Penrith Castle Blencow Hall, Greystoke Dacre Castle Millom Castle Vol 2 Carlisle Castle Whitehaven Whitehaven St Nicholas Whitehaven St James Whitehaven Castle Cockermouth Bridge Keswick Pocklington's Island Castlerigg Stone Circle Grange in Borrowdale Bowder Stone Bassenthwaite lake Roman Altars, Maryport Aqua-tints and engravings from -

Trades. [ Westmorland

176 FAR TRADES. [ WESTMORLAND. FARMERs-continued. Wilkinson Mrs. Margaret,Henridding, Wilson Thomas, Fell house, Lupton, Watson Wm. John, Duckpool,Brough, Dalton, Carnforth Kirkby Lonsdale Kirkby Stephen Wilkinson R. Goose Howe,Hugill,Kndl Wilson Thomas, Fern cottage, Cas- Watters T. & J. Raisbeck, Tebay 8.0 Wilkinson Thos.Askew green, Wither- terton, Kirkby Lonsdale Watts Robert, Toddygill hall, Great slack, Grange-over-Sands S.O Wilson Thomas, Hugill, Kendal Musgrave, Penrith Wilkinson T. Gt. Strickland, Penrith Wilson Thomas Silk, Underfell, Bar- Waugh John, Water nook & Doe grn. Wilkinson W. Frost hall, Warcop 8.0 bon, KilOkby Lonsdale iMartindale, Penrith Wilkinson William, Howe lodge, Lyth, Wilson William,Durham bridge,Lyth, Waugh J. Winton hall,Kirkby Stephn Milnihorpe S.O Milnthorpe S.O Wear Benjamin, Tarn foot, Lough Wilkinson Wm. Oxenthwaite, Stain- Wil90nW.Ulpha,Grange-over-Snds.S.O rigg, Arn:bleside more South, Kirkby 8tephen Wilson William, Beech hill &; Kiln- Wear Fisher Mason, Greenbank,Deep Willan Bowness, 1Yhitestones, Asby, stone, Long Sleddale, Kenda! dale, Patterdale, Penrith Winderwath, Appleby Wilson William, jun. Bonfire haU. We'iT George, Elea Tarn house, Little Willan George, Drybeck, Killington, Underbarrow, Kendal Lngdale, Ambleside Kirkby Lonsdale Wilson William, Helsington, Kendal Wearmouth William,Eller hilI,Raven Willan J. Bow brow,Orton, Tebay S.O Wilson William, sen. Lower Gregg stonedale, Newbiggin S.O Willan J.Church ho.Bramptn..Appleby hall, Underbarrow, Kenda! Webster John Crayston, The Hall, Willan John, Beckfoot, Barbon, Kirk- Winder James, Greenside, Raven- Beetham, Milnthorpe S.O by Lonsdale stonedale, Ne"biggin S.O Weedall H. Low. Plumgarths, Kendal Willan John, Oddendale, Crosby, Winn Mrs. Ann, Beckfoot,' Barbon, Weightman J. -

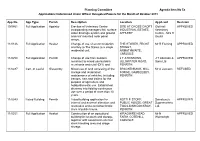

Applications Determined Under Officer Delegated Powers for the Month of October 2011

Planning Committee Agenda Item No 5a Applications Determined Under Officer Delegated Powers for the Month of October 2011 App No App Type Parish Description Location Applicant Decision 10/0861 Full Application Appleby Erection of Veterinary Centre SITE AT CROSS CROFT Old Hall APPROVED incorporating managers flat, surface INDUSTRIAL ESTATE, Veterinary water drainage system and ground APPLEBY Centre - Mrs H and roof mounted solar panel Gould arrays. 11/0146 Full Application Hesket Change of use of accommodation THE STORES, FRONT Mr R Fleming APPROVED ancillary to The Stores to a single STREET, residential unit. ARMATHWAITE, CARLISLE 11/0258 Full Application Penrith Change of use from builders J T ATKINSONS, J T Atkinson & APPROVED merchant to mixed use builders ULLSWATER ROAD, Sons Ltd merchants and retail (DIY) and PENRITH 11/0287 Cert. of Lawful Glassonby Mixed use of land consisting of the BRACKENBANK, MILL Mr A Jackson REFUSED storage and restoration/ FORGE, GAMBLESBY, maintenance of vehicles, including PENRITH tractors, cars and trailers for the purpose of agriculture and hobby/domestic use. Established driveway into field by continuous use over a period of more than 10 years. 11/0349 Listed Building Penrith Listed building application for BOTTLE STORE, Sainsbury's APPROVED internal and external alteration and PUBLIC HOUSE, GREAT Supermarkets restorative works to former bottle TWO LIONS DOCKRAY, Ltd. store of public house. PENRITH 11/0351 Full Application Hesket Construction of an agricultural WRAGMIRE HEAD Mr N APPROVED building for livestock and storage, FARM, COTEHILL, Wainwright together with associated external CARLISLE stock handling area and silage storage. 11/0363 Full Application Yanwath & Continuation of permanent 15 GLENDOWLIN Mr D Brookes APPROVED Eamont Bridge residential use for current resident LODGES, YANWATH, only. -

Westl\10HLAND

162 FAR .WESTl\10HLAND. [KELLY~ }l'A~MR'RS continuetL 13a.inbridg-B Jonn, Xnt:Jck, Rnvenstone- Beck Richal'd, Sandwath, -Ravenllklne- .!.tkinson Jobn, Ryclal, Ambleside dale, KiI'kby St~phen I dale, Kirkby Btephen ' i AtkinsOIl John, Sandpot. Mallerstan/;. Bainbridg'e Richard, Holme, Carnfotth Beck Thomas, Low Fairbanlr, NMMr Kirkby Stephen Bainbridge Thomas, Church Brougb, Staveley, Kendal Atki.nson J. Town head, Cliburn,Penrth Kirkby Stephen 'Becks John, Langdale, Tebay RB.~ Atkirtson John, Witherslack, Grange- Bainbridge Thomas, 0rc-sby Garrett, Bec;mith John, High Ewbanll', Stain- over-Sands R. S.O Kirkby Stephen ' more South, Kirkby Stepbell AJldnson John Thomas, Town head, Bainbridge William, ArcheI"' hill, Bell A. &, Wm. Reagin,SOOp H:S.D Milburn, Newbiggin R. S. 0 Langdale, Tebay R S. 0 Bell George, Dirk 'rigg, Mallent:mg, Atkinson Joseph, Barnskew, Reagill, Bainbridge William, Croft end~ ,Bramp- Kirkby 8tephen Shap RS.O ton, Appleby Bell Henry, Dummah hill, Stainmore Atk~nson J.Ghyll hd. Crosthwaite,Kndl Bainbridge Wm. 1 Garthshill, Raven- South, Kirkby Stephen- Atkimon.T. Waitby, Kirkby StephAn stonedale, Kirkby Stephen Bell Tsaac, Kirkby Thore, Poorith Atkinson Mrs: Margaret, Brunthwaite, Bainbridge William, Keisley, .Appleby Bell .lames, Drybeck, Appleby Old Hutton, Kendal Bainhridge Wm. Kelleth, Tebay RS.O Bell .lames, Outhgill, Kirk'bj Stepmn Atkinson Mark, Greyber. Maulds Me8- Bainbridge W. Waitby, Kirkby Stephn Bell .Tames, Reagill, Shap R.S.O b. burn, Shap R.S.O Ba.ines Mrs. Agnes & Son, Whasset, Bell John, G'rackent.horpe, Appleb:f ..Atkinson Mark, Murton, Appleby Beetham, Milnthorpe R.S.O Bell .In. Guest ford, Whinfell, K~dal . Atkinson M. -

Neighbourhood Development Plan: Penrith Town Council, August 2020

1 Penrith Draft Neighbourhood Development Plan – August 2020 2 Table of Contents Penrith Draft Neighbourhood Development Plan – August 2020 ........................... 2 ACKNOWLEDGEMENTS ................................................................................ 5 FOREWORD ................................................................................................ 6 Seeking Further Views ................................................................................. 7 1. INTRODUCTION AND BACKGROUND ........................................................ 9 2. PENRITH: A HISTORIC TOWN ................................................................ 11 3. KEY ISSUES FOR PENRITH TODAY .......................................................... 13 3.1 Sustainable Development ............................................................... 13 3.2 Housing ....................................................................................... 14 3.3 Greenspaces ................................................................................. 16 3.4 Culture and Leisure ....................................................................... 16 3.5 Wellbeing ..................................................................................... 17 3.6 Car Parking and Public Transport ..................................................... 19 3.7 Traffic Management ....................................................................... 21 3.8 Penrith Town Centre ...................................................................... 23 3.9 Employment -

Westmoreland in the Late Seventeenth Century by Colin Phillips

WESTMORLAND ABOUT 1670 BY COLIN PHILLIPS Topography and climate This volume prints four documents relating to the hearth tax in Westmorland1. It is important to set these documents in their geographical context. Westmorland, until 1974 was one of England’s ancient counties when it became part of Cumbria. The boundaries are shown on map 1.2 Celia Fiennes’s view in 1698 of ‘…Rich land in the bottoms, as one may call them considering the vast hills above them on all sides…’ was more positive than that of Daniel Defoe who, in 1724, considered Westmorland ‘A country eminent only for being the wildest, most barren and frightful of any that I have passed over in England, or even Wales it self. ’ It was a county of stark topographical contrasts, fringed by long and deep waters of the Lake District, bisected by mountains with high and wild fells. Communications were difficult: Helvellyn, Harter Fell, Shap Fell and the Langdale Fells prevented easy cross-county movement, although there were in the seventeenth century three routes identified with Kirkstone, Shap, and Grayrigg.3 Yet there were more fertile lowland areas and 1 TNA, Exchequer, lay subsidy rolls, E179/195/73, compiled for the Michaelmas 1670 collection, and including Kendal borough. The document was printed as extracts in W. Farrer, Records relating to the barony of Kendale, ed. J. F. Curwen (CWAAS, Record Series, 4 & 5 1923, 1924; reprinted 1998, 1999); and, without the exempt, in The later records relating to north Westmorland, ed. J. F. Curwen (CWAAS, Record Series, 8, 1932); WD/Ry, box 28, Ms R, pp.1-112, for Westmorland, dated 1674/5, and excluding Kendal borough and Kirkland (heavily edited in J. -

Cumbria Classified Roads

Cumbria Classified (A,B & C) Roads - Published January 2021 • The list has been prepared using the available information from records compiled by the County Council and is correct to the best of our knowledge. It does not, however, constitute a definitive statement as to the status of any particular highway. • This is not a comprehensive list of the entire highway network in Cumbria although the majority of streets are included for information purposes. • The extent of the highway maintainable at public expense is not available on the list and can only be determined through the search process. • The List of Streets is a live record and is constantly being amended and updated. We update and republish it every 3 months. • Like many rural authorities, where some highways have no name at all, we usually record our information using a road numbering reference system. Street descriptors will be added to the list during the updating process along with any other missing information. • The list does not contain Recorded Public Rights of Way as shown on Cumbria County Council’s 1976 Definitive Map, nor does it contain streets that are privately maintained. • The list is property of Cumbria County Council and is only available to the public for viewing purposes and must not be copied or distributed. A (Principal) Roads STREET NAME/DESCRIPTION LOCALITY DISTRICT ROAD NUMBER Bowness-on-Windermere to A590T via Winster BOWNESS-ON-WINDERMERE SOUTH LAKELAND A5074 A591 to A593 South of Ambleside AMBLESIDE SOUTH LAKELAND A5075 A593 at Torver to A5092 via -

Yanwath & Eamont Bridge Parish Council Business To

YANWATH & EAMONT BRIDGE PARISH COUNCIL BUSINESS TO BE TRANSACTED Virtual Parish Council Meeting 12th January 2021 1. Apologies 2. Register of Interest & Declaration of Acceptance completed 3. Parish Council Vacancies 4. Footway Yanwath to Eamont Bridge 5. Land at Glendowlin 6. Lease of Land Glendowlin 7. 2021 National Census 8. Great North Air Ambulance Donation 9. Drains & Flooding Yanwath 10. Support to Clifton Parish Council . Reduce Speed in the Community 11. CALC Training 12. Sewage Odour 13. Draft Housing Strategy 14. Parish Polls 15. Defibrillators Account 16. Plans Received- Lowther Holiday Park 17. Plans Details Submitted Yanwath Hall 18. Data Protection Account Paid 19. Highways England- Community Liaison Group 20. E Mail CALC – Website Compliance 21. E Mail CALC – Bus to Shap Medical Centre 22. E Mail CALC Early Years Engagement 23. Leaflet- Elan City- Radar Speed Sign 24. COVID Booklet 25. E Mail CALC Local Government -Ethical Public Safety Strategy 26. EALC Presentation Council-Jackie attended meeting & will give a short report 27. E Mail Cumbria County Council- Help at Christmas 28. E Mail CALC Parish Council – Carbon Footprint 29. Neighbourhood Plan 30. Came & Co Insurance 31. Leaflet Maximin Solution 32. CALC Newsletter 33. E Mail CAL:C - Community Leaders Pack 34. E Mai- £den District Council- Street Lighting Charge 35. Street Light at Eamont Bridge not working 36. E Mail CALC -Tier 2 37. Stagecoach Payment 38. E Mail- Rheged 39. E Mail Eden District Council-Recharge Footway Lighting 40. E Mail CALC -Legal Topic Note on Easement over Common Land 41. E Mail Cumbria County Council- Thank You 42. -

RSAP 6 Appendix 1 to RSAP 5

DOCUMENT REFERENCE RSAP 6 Copies of letters to consultees and to libraries and addressees lists This is Appendix 1 to Document RSAP 5 the Pre-submission Consultations Statement 2 APPENDIX 1 TO DOCUMENT RSAP 5 These are the October 2011 consultation letters and lists of addressees together with letters to district councils and libraries concerning public display copies of the Site Allocations Policies and Proposals Map. 3 LETTER 1 Environment Directorate Planning and Sustainability County Offices Kendal LA9 4RQ Tel: 01539 713425 Fax: 01539 713439 Email: [email protected] Date: 24 October 2011 Ref: RGE/P334-26 Dear Sir/Madam Cumbria Minerals and Waste Development Framework Site Allocations Policies and Proposals Map Repeated Regulation 27 Consultations In 2009 and 2010 we consulted you about the above policies and maps. They were subsequently submitted to the Secretary of State, examined by the Planning Inspectorate and formally adopted by the County Council in January 2011. At a very late stage in the process, there was a successful legal challenge in connection with a procedural matter and the documents were quashed by the High Court. It is, therefore, necessary for the consultations to be repeated before the documents can be resubmitted to the Secretary of State. The challenge was about the inclusion, without a further round of consultations, of an Area of Search for sand and gravel known as M12 Roosecote quarry extension in Site Allocations Policy 7. This Area of Search was intended as a possible replacement for the nearby Roose sand and gravel quarry near Barrow in Furness, which is a Preferred Area in the policy. -

Enclosure Awards

CUMBRIA RECORD OFFICE (KENDAL) INCLOSURE AWARDS Reference PLace (arranqed al-phabetically) Date Date of ^€ arara. ft/t4gffi.b* ^# 544r"rsr,l**ff Act. Ambl-eside, see Bird House Common Field Appleby, see Bongate etc wQR/r 6 Applethwaite (including 183 1 IB42 Troutbeck and Hugill)' WQR/I 3 Asby High Intake t-84 5 L849 wQR/r 2 Asby Low Intake 184 5 aB49 wQR/r 4 Asby Mask. (Asby Coatsforth, 1845 18 55 township) wQR/r 1 Asby Winderwath 186 5 1,87 4 Askham, see also Helton Cruse wQR/r s Askham High Fietd 1,845 1853 Bampton Sackwath, see Sackwath 183 6 IB46 WQR/I 7 Beetham L87.4 L82L WQR/I B Bird i{ouse Common Field, Ambleside 1336 1853 WQR/I 9 Bleatarn Common t-7 90 t79L wQR/r 10 Bolton 1808 1813 wQR/r 1r- Bongate and Burrells Moor 1-7 72 L774 Brad1eyfi.eld, see Underbarrow wQR/r L2 Brampton a77 0 1772 wDx 753 Brough Intack l-83 6 aB42 wD/Kilv 65 Brough Intack 183 5 L842 Brough, see also Lowgill Field BrougL:anr, see afso Cliburn Ling Reference Place (arranqed alohabeticallw) Date Date of of Act. Award. wD/K/322 Brougham Moor and Sandwath (copy) L77 6 Burrells Moor, see Bongate Burton in Kendal, see Dalton weR/r 1E i3 Capelrigg Intake, SLainmore 18 56 ]-857 wPR 89/23 Cartmel ].796 t_809 wQR/r 14 Casterton 78]-2 1B i_6 wQR/r 18 Church Brough Intake 1854 1855 WPC 30 Claife r7 94 L7 99 wQR/r ls Cliburn 18 06 182 0 wQR/r 16 Cliburn Ling (Brougham parish) 1835 L867 wQR/r L7 Clifton l8 t_1 t-815 wQR/r 21, Colby Mooi L8 51 1B 54 wQR/r 20 Colby Pasture wQR/r 24 Crook (Whitwe11 & Selsj-de, 18 23 7.829 Skelsmergh & Crook) wQR/t 22 Crosby Garrett 184