Corporate Responsibility Practices in Engineering

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Civil Engineering & Construction Brochure

Distributed by: Civil Engineering & Construction Brochure INTRODUCTION Platipus® Anchors Limited are market leaders in the design, manufacture and supply of mechanical earth anchoring products in the UK. Founded in 1982 , we are renowned for providing some of the most innovative and cost effective anchoring solutions for the Civil Engineering and Construction industries. The percussion driven mechanical anchor is a unique, modern and versatile device that can be rapidly deployed in most displaceable ground conditions. It offers a lightweight corrosion resistant anchor that can be driven from ground level using conventional portable equipment. It creates minimal disturbance of the soil during installation, can be stressed to an exact holding capacity and made fully operational immediately.As a completely dry system it also has minimal environmental impact. ApplicationsHeavy Installation Retaining Walls Guyed Structures Slope Stabilisation Scaffolding Bridges Foundations Sheet Piling Landfill Capping Erosion Control Portable Buildings/ Gabion Support Structures Rock Retention General Security Buoyancy Control/ Marine Applications Pipelines Tunnel Linings Drainage Temporary Works 2 FEATURES & BENEFITS KEY BENEFITS OF THE PLATIPUS® EARTH ANCHORING SYSTEM • Simple and effective concept • Lightweight corrosion resistant products to suit a range of design life requirements • Fast and easy installation • Immediate quantifiable loads • Holding capacity up to 200kN • Ideal for temporary and permanent situations • Cost effective alternative to traditional -

8347 Interserve AR 2011 Introduction 4 Ifc-P1 Tp.Indd

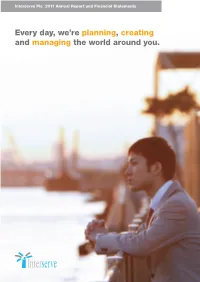

Interserve Plc 2011 Annual Report and Financial Statements Interserve Plc Every day, we’re planning, creating and managing the world around you. 2011 Annual Report and Financial2011 Statements INTERSERVE ANNUAL REPORT 2011 OVERVIEW HIGHLIGHTS Across the world, people wake to a new day. We help make it a great day. PROUD OF THE Every day people wake to put We help build and look after this their plans, dreams and goals world and we do this through the VALUE WE CREATE IN into action. lasting relationships our people have built with a range of partners PLANNING, CREATING, To make this happen they need the and clients worldwide to ensure we places around them – their schools, AND MANAGING THE create value for everyone involved. their workplace, hospitals, shops WORLD AROUND YOU and infrastructure – to function well, to support, inspire and add value to their lives. FINANCIAL HIGHLIGHTS HEADLINE EPS* PROFIT BEFORE TAX FULL-YEAR DIVIDEND 49.3p £ 67.1m 19.0p + 15% + 5% + 6% VIEW 2011 ANNUAL REPORT ONLINE: HTTP://AR2011.INTERSERVE.COM INTERSERVE ANNUAL REPORT 2011 OVERVIEW HIGHLIGHTS Across the world, people wake to a new day. We help make it a great day. PROUD OF THE Every day people wake to put We help build and look after this their plans, dreams and goals world and we do this through the VALUE WE CREATE IN into action. lasting relationships our people have built with a range of partners PLANNING, CREATING, To make this happen they need the and clients worldwide to ensure we places around them – their schools, AND MANAGING THE create value for everyone involved. -

Highways Agency Supplier Recognition Scheme 2011

Highways Agency Supplier Recognition Scheme 2014 Best Practice Report Introduction This report looks to highlight the key aspects of the winning and highly commended entries in each category. Background 2014 was the fourth year of the Highways Agency Supplier Recognition Scheme. The annual recognition scheme highlights the vital contribution made by the Agency’s suppliers who help it operate, maintain and improve England’s network of motorways and A roads. This year entries for the awards increased significantly – as 118 bid for the honour to receive public recognition from the Agency across seven categories. These included joint ventures, the extended supply chain and small and medium enterprises. 2014 Winners and Highly Commended The Highways Agency received 118 entries from 50 entrants which included single suppliers and joint ventures. The following winners and highly commended were chosen: Winners Highly Commended Building and Sustaining Capability Costain Carillion Civil Engineering Customer Experience Carillion Civil Engineering Mouchel (Designer) & Carillion (Delivery Costain Ltd Partner) Delivering Sustainable Value & Solutions Costain Group plc Interserve Construction Limited Sir Robert McAlpine & AW Jenkinson Managing Down Cost/Improving Value Carnell Group Carillion Civil Engineering WSP Skanska Balfour Beatty/Atkins Delivery Simulation Systems Limited Team Promoting Diversity & Inclusion EM Highway Service Limited & BAM/Morgan Sindall JV Recycling Lives Safety, Health & Wellbeing Carnell Group A-One+ Integrated -

NCE100-Gold-Book.Pdf

Gold Book The stories behind the most innovative, impactful and inspirational civil engineering practices Contents 6 Overview How the NCE100 Companies of the Year were chosen 8 8 Staff feedback analysis Staff feedback was key to 0% 100% NCE100 award winner choices 57% 11 NCE100 Very Satisfied Top10 The 10 best NCE100 companies in 2018 20 Trending 20 The top 20 up and coming civil engineering firms 22 Trending 20 winner FJD Consulting stood out 93% among the up and comers Satisfied 25 NCE100 winners The 15 greatest stories of 2017 56 NCE100 22 16 listing The NCE100 Companies of the Year 58 NCE100 Judges The 45 judges who assessed the NCE100 firms NCE100 GOLD BOOK 2018 3 EUROPE’S LEADING MULTI-DISCIPLINARY ENGINEERING, ENVIRONMENT & DESIGN CONSULTANCY WE BELIEVE IN THE POSITIVE POWER OF HUMAN CURIOSITY & THE POSSIBILITIES IN TECHNOLOGY, INNOVATION & DESIGN As Europe’s leading consultancy for future communities and cities, Sweco is delighted to be ranked by the NCE as the 6th civil engineering company in the UK and proud to be the recipient of its Low Carbon Leader Award. [email protected] | 0113 262 0000 | www.sweco.co.uk Foreword Welcome to the NCE100 Gold Book. Inside we are recognising some fantastic civil engineering businesses. The companies inside are the most innovative, impactful and inspirational companies operating in the infrastructure sector today. We know this because the NCE100 is the most rigorous and robustly-judged business recognition scheme in civil engineering. To achieve recognition here, firms have had to present their achievements to a panel of 45 judges representing the industry’s leading clients, owner/operators stakeholder groups and change bodies. -

Business Briefing

Business Briefing 05 June 2015 Business Briefing 05 June 2015 Tony Bickerstaff, Group Finance Director Agenda Meeting National Needs Andrew Wyllie Meeting the National Need for Energy John Pettigrew HS2: A Catalyst for Growth across Britain Simon Kirby BREAK Upgrading the highways infrastructure Graham Dalton Being a partner of choice Costain Business Briefing 05 June 2015 Andrew Wyllie CBE, Chief Executive Business Briefing 05 June 2015 Meeting the National Need for Energy John Pettigrew National Grid Executive Director, UK Change in Energy Landscape Electricity Market Reform A package of measures to………….. Incentivise low carbon investment - Contracts For Difference Manage emissions - Emissions Performance Standard - Carbon floor price support Security of supply - Capacity market Our 2015 Future Energy Scenarios Consumer Gone Green Power More More prosperity Prosperity Less Prosperity No Slow Progression Progression Less Ambition Green Ambition More ambition Changes in Generation landscape Currently New Applicants Plant Type Connected (MW) (MW) Coal / Biomass 20296 280 Hydro 3775 3029 Interconnector 4364 8205 Nuclear 9937 17737 Oil & AGT 800 0 Wind Offshore 4328 32791 Wind Onshore 2953 7144 Gas 28060 21044 Total 74513 90230 Key Investments Our major infrastructure projects (I/C’s in orange) NSN Link – UK / Norway North West Coast - Interconnector Nuclear connection HVDC Eastern Link - Inter connection with Scotland HVDC Western Link - King’s Lynn - Gas- Inter connection fired power station with Scotland connection North Wales - East Anglia -

VPS SPD Consultation Statement

Parking Standards Design and Good Practice Supplementary Planning Document Consultation Statement (Regulation 17 Statement) In the preparation of draft Supplementary Planning Guidance the Department for Communities and Local Government advises authorities to informally involve local communities and other stakeholders in the development of policies. Work on the Parking Standards Design and Good Practice document commenced in May 2007 by the forming of a Parking Standards Review Group. This group was led by officers of the Essex County Council Strategic Development section working with colleagues from both within Essex County Council and Essex local authorities. A list of those involved is included on page iii of the document. The development of the draft Parking Standards Design and Good Practice document has taken place over a 24-month period and comprised the following main activities: Residents Survey May- September 2007 (to complement a related existing survey undertaken in 2006) Group Site visits June – July 2007 Individual site visits, evening and weekends June – July 2007 Education meeting August 2007 Regular Review Group meetings May – April 2008 Review of other authority Parking Standards May – April 2008 SEA September 2008 – March 2009 Public Consultation March – April 2009 The scope and outcome of these activities are summarised below: 1. Residents Survey A survey was undertaken by Essex County Council term consultant’s Mouchel, to ascertain the opinions of local residents from housing developments that had recently been constructed -

Milton Keynes Council

Internal Audit Milton Keynes Council www.milton-keynes.gov.uk/internal-audit MOVING IN MOVING OUT Internal Audit – Final Report MKC INTERNAL AUDIT SERVICE MOVING IN MOVING OUT (EMPTY HOMES) EXECUTIVE SUMMARY AUDIT AREA An audit of Moving In Moving Out (Empty Homes) has been carried out in accordance with the annual audit plan. AUDIT OPINION Satisfactory - Controls are considered adequate with some areas of weakness that are not major risk areas. In addition the process may not be demonstrating Best Value for Money. AUDIT REPORT – E137/11 1 MAY 2011 MKC INTERNAL AUDIT SERVICE MOVING IN MOVING OUT (EMPTY HOMES) 1 AUDIT CONCLUSIONS 1.1 The empty homes process is generally operated very well. Staff, particularly management have a high level of focus and there is a passion to remove waste from the system at every opportunity using a continuous improvement approach. On the whole it is considered that the way that different parts of the Council, Mouchel, MITIE and Wheldons work together is to be commended. 1.2 The process as it appears today is far leaner than observed in previous audits reflecting the willingness to continually try different approaches to secure improvement. However there are some further smaller opportunities to squeeze out more waste and a more strategic rather than operational view point may assist with this. 1.3 A frustration which appears to be experienced by all contributors is the disturbance to the smooth flow created by the necessity to undertake asbestos surveys. The Council’s Asbestos Management Plan requires that every empty home must have an asbestos survey completed to comply with legislation. -

CSL Peer-Reviewed Publications 2015-2020

NOAA Chemical Sciences Laboratory 2015 – 2020 Peer-Reviewed Publications sorted by year of publication, then alphabetical by first author 2020 Akherati, A., Y. He, M. Coggon, A. Koss, A. Hodshire, K. Sekimoto, C. Warneke, J. de Gouw, L. Yee, J. Seinfeld, T. Onasch, S. Herndon, W. Knighton, C. Cappa, M. Kleeman, C. Lim, J. Kroll, J. Pierce, and S. Jathar, Oxygenated aromatic compounds are important precursors of secondary organic aerosol in biomass burning emissions, Environmental Science & Technology, 54(14), 8568-8579, doi:10.1021/acs.est.0c01345, 2020. Angevine, W.M., J.M. Edwards, M. Lothon, M.A. LeMone, and S. Osborne, Transition periods in the diurnally-varying atmospheric boundary layer over land, Boundary-Layer Meteorology, 177, 205-223, doi:10.1007/s10546-020-00515-y, 2020. Angevine, W.M., J. Olson, J. Gristey, I. Glenn, G. Feingold, and D. Turner, Scale awareness, resolved circulations, and practical limits in the MYNN-EDMF boundary layer and shallow cumulus scheme, Monthly Weather Review, 148(11), doi:10.1175/MWR-D-20-0066.1, 2020. Angevine, W.M., J. Peischl, A. Crawford, C. Loughner, I. Pollack, and C. Thompson, Errors in top-down estimates of emissions using a known source, Atmospheric Chemistry and Physics, 20, 11855-11868, doi:10.5194/acp-20-11855-2020, 2020. Archibald, A.T., J.L. Neu, Y. Elshorbany, O.R. Cooper, P.J. Young, H. Akiyoshi, R.A. Cox, M. Coyle, R. Derwent, M. Deushi, A. Finco, G.J. Frost, I.E. Galbally, G. Gerosa, C. Granier, P.T. Griffiths, R. Hossaini, L. Hu, P.Jöckel, B. Josse, M.Y. -

Responsive Repairs

Internal Audit Milton Keynes Council www.milton-keynes.gov.uk/internal-audit RESPONSIVE REPAIRS Internal Audit – Final Report MARCH 2012 MKC INTERNAL AUDIT SERVICE RESPONSIVE REPAIRS EXECUTIVE SUMMARY 1 AUDIT AREA An audit of Responsive Repairs has been carried out in accordance with the annual audit plan. This audit focussed on the work being carried out by Mitie. 2 AUDIT OPINION Good 3 AUDIT CONCLUSIONS 3.1 There has been significant improvement over the past few years in the way that the repairs service is managed. This conclusion is supported by the positive responses received from customer satisfaction surveys. 3.2 From first hand evidence obtained whilst working on site, having the end to end process on the same site, from receiving the customer’s call to the same operator conducting the satisfaction survey, is proving beneficial to all concerned. 3.3 The average cost of a repair, (calculated by dividing the total cost by the number of works orders issued) has increased by approximately 12% on the previous year. This can be explained by works to a property, carried out by Mitie’s operatives, being grouped together on the same works order therefore raising the cost of the individual works order and resulting in fewer works orders being issued. 3.4 There continue to be concerns accurately recording what constitutes a ‘first time fix’. As this is a key measure it is important that this is clarified. 4 THE FUTURE 4.1 All actions are in the Management Action Plan (Page 5). Detailed findings from the audit are reported within the Main Report in Section 7. -

Insights Into Facilities Management

Insights into ISSUE 15 • 2015 facilities management FMFacilities management market M&A update, Q2 2015 M&A activity eased off modestly in the second quarter of 2015, mainly as a result of lower activity among international buyers in the UK FM market. Important larger deals drove David Ascott Partner, Corporate Finance the value of M&A upwards during the period. Grant Thornton UK LLP M&A activity eases off; value increases After a relatively robust start to 2015, M&A activity in the UK’s FM market eased off somewhat “Whilst M&A activity in the second quarter, perhaps impacted at home by the focus on the general election and abroad in Q2 was steady the by concerns surrounding the Greek sovereign debt crisis. Overall the number of deals recorded July budget created in the sector fell by 13% from the 23 seen in Q1 to 20. While the second quarter total is also 17% down on the same period of 2014, the poor start to last year means that the first half of 2015 is unexpected ripples comfortably ahead of 2014 on run rate; it is also ahead of H1 2012, but some way behind the same in the market due to period in 2013. the potential impact As was underlined in the last bulletin, the M&A market in the FM sector is largely ticking of the increasing over on the back of consolidation activity at the smaller end of the scale, though the occasional larger deal has a significant impact on the market value. Although Q1 2015 saw no such deal, minimum wage. -

Following Its Announcement on 28 April 2015, Kier Group Plc ("Kier

KIER GROUP PLC Completion of the acquisition of Mouchel Following its announcement on 28 April 2015, Kier Group plc ("Kier"), the integrated property, residential, construction and services group, is pleased to announce that, on 8 June 2015, it completed the acquisition of the entire issued share capital of MRBL Limited (“Mouchel”). Mouchel is an international infrastructure and business services group. It provides advisory, design, project delivery and managed services to the highways and transportation, local government, property, emergency services, health, education and utilities markets in the United Kingdom, the Middle East and Australia. It is the leading provider of repair and maintenance services to the UK strategic road network. As stated at the time of the announcement of the acquisition, the Board believes that the rationale for the acquisition is compelling and aligned to Kier's “Vision 2020” strategy, representing an excellent opportunity to accelerate Kier's plans for growth in the infrastructure sector. Kier’s chief executive, Haydn Mursell, commented: “The successful acquisition of Mouchel now positions Kier as a sector leader in the growing UK highways maintenance and management market. In particular, the acquisition enables the Group to capitalise on £17 billion of investment in the strategic road network to be delivered through Highways England over the next five years, whilst also accelerating the delivery of Kier’s “Vision 2020” strategy.” - E N D S - For further information, please contact: J.P. Morgan Cazenove (Joint Financial Adviser, Joint Sponsor, Joint Bookrunner and Joint Broker to Kier) +44 (0) 20 7742 4000 Robert Constant Christopher Dickinson Laurene Danon Numis Securities (Joint Financial Adviser, Joint Sponsor, Joint Bookrunner and Joint Broker to Kier) +44 (0) 20 7260 1000 Heraclis Economides Christopher Wilkinson Richard Thomas Finsbury +44 (0)20 7251 3801 Kier Press Office +44 (0) 1767 355903 . -

Department for Work and Pensions

Department for Work and Pensions Ministers meetings with external organisations1 Period 13 May – 31 July 2010 Secretary of State for Work and Pensions Rt Hon Iain Duncan Smith MP Date of Name of External Purpose of Meeting Meeting Organisation June 2010 Independent Age; Age UK; Roundtable introduction to Carers UK; Joseph Rowntree a number of stakeholder Foundation; Counsel and Care; groups Church Action on Poverty; and Oxfam UK June 2010 National Association of Pension Introductory meeting Funds; Confederation of British Industry; Association of British Insurers; and Investment Management Association June 2010 Public and Commercial Introductory Meeting Services Union July 2010 Bristol Community Family Trust Reducing family breakdown July 2010 Thames Gateway London Tackling Worklessness Partnership Minister of State (Minister for Employment) Rt Hon Chris Grayling MP Date of Name of External Purpose of Meeting / Meeting Organisation subject of discussion June 2010 Tomorrow’s People Employment June 2010 Institute of Occupational Health Health and Safety & Safety June 2010 Confederation of British Pensions and the Industry European Union June 2010 Chambers of Commerce Budget June 2010 Chartered Institute of Budget Personnel and Development June 2010 Institute of Directors Budget June 2010 Federation of Small Businesses Budget June 2010 Citizens Advice Bureau Work Capability Assessment June 2010 Employment Related Services Work Programme Association; British Association for Supported Employment; Association of Learning Providers; Confederation