Working of Forest Divisions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Demp Kaimur (Bhabua)

DEMP KAIMUR (BHABUA) SL SUBJECT REMARKS NO. 1 2 3 1. DISTRICT BRIEF PROFILE DISTRICT POLITICAL MAP KEY STATISTICS BRIEF NOTES ON THE DISTRICT 2. POLLING STATIONS POLLING STATIONS LOCATIONS AND BREAK UP ACCORDING TO NO. OF PS AT PSL POLLING STATION OVERVIEW-ACCESSIBILITY POLLING STATION OVERVIEW-TELECOM CONNECTIVITY POLLING STATION OVERVIEW-BASIC MINIMUM FACILITIES POLLING STATION OVERVIEW-INFRASTRUCTURE VULNERABLES PS/ELECTIORS POLLING STATION LOCATION WISE ACCESSIBILITY & REACH DETAILS POLLING STATION WISE BASIC DETAISLS RPOFILING AND WORK TO BE DONE 3. MANPOWER PLAN CADRE WISE PERSONNEL AVAILABILITY FOR EACH CATEGORY VARIOUS TEAMS REQUIRED-EEM VARIOUS TEAMS REQUIRED-OTHERS POLLING PERSONNEL REQUIRED OTHER PERSONNEL REQUIRED PERSONNEL REQUIRED & AVAILABILITY 4. COMMUNICATION PLAN 5. POLLING STAFF WELFARE NODAL OFFICERS 6. BOOTH LIST 7. LIST OF SECTOR MAGISTRATE .! .! .! .! !. .! Assembly Constituency map State : BIHAR .! .! District : KAIMUR (BHABUA) AC Name : 205 - Bhabua 2 0 3 R a m g a r h MOHANIA R a m g a r h 9 .! ! 10 1 2 ! ! ! 5 12 ! ! 4 11 13 ! MANIHAR!I 7 RUP PUR 15 3 ! 14 ! ! 6 ! 8 73 16 ! ! ! RATWAR 19 76 ! 2 0 4 ! 18 .! 75 24 7774 17 ! M o h a n ii a (( S C )) ! ! ! 20 23 DUMRAITH ! ! 78 ! 83 66 21 !82 ! ! .! 32 67 DIHARA 22 ! ! 68 ! 30 80 ! 26 ! 31 79 ! ! ! ! 81 27 29 33 ! RUIYA 70 ! 25 ! 2 0 9 69 ! 2 0 9 KOHARI ! 28 KAITHI 86 ! K a r g a h a r 85 ! 87 72 K a r g a h a r ! ! 36 35 ! 71 60 ! ! ! 34 59 52 38 37 ! ! ! ! 53 KAIMUR (BHABUA) BHABUA (BL) 64 ! ! 40 84 88 62 55 MIRIA ! ! ! ! BAHUAN 54 ! 43 39 !89 124125 63 61 ! ! -

Block: Piro Class-6-8 Subject: Social Science Dist:-Bhojpur Provisional Merit List Block Teacher Niyojan-2019-20

BLOCK TEACHER NIYOJAN-2019-20 BLOCK: PIRO CLASS-6-8 SUBJECT: SOCIAL SCIENCE DIST:-BHOJPUR PROVISIONAL MERIT LIST 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 MATRIC INTER GRADUATION TRAINING FREE BTET/CT WEIG SUM OF AVG OF TAGE APPL.S. NAME OF SE D. FUL MARK ET TOTAL S.N. FATHER DOB ADDRESS CAT DIS. MARKS MARKS FULL MARKS FULL FULL PERCENT PERCEN OF REMARKS N. APPLICANT X FIGH L S MARKS MERIT OBTAI %GE OBTAIN MARK %GE OBTAINE MARK %GE MARK %GE AGE TAGE BTET/ T. MAR OBTAI % NED ED S D S S CTET KS NED MOHD ARANGI-01 NAZIA 1 1776 MONIR 18/4/1995 F USIA UR N N 457 500 91.4 434 600 72.3333 3330 4500 74 1675 2000 83.75 321.4833 80.37 62.66 2 82.371 MONIR ANSARI GHAZIPUR DAYASHAN PRAGYA KAILASHPUR 2 P/197 KAR 22/12/1996 F EWS N N 409 500 81.8 432 500 86.4 740 1000 74 762 1000 76.2 318.4 79.60 68 2 81.6 PANDEY I BUXAR PANDEY NEERAJ BHRIGUNA BIHIYA 3 976 KUMAR 02.01.1993 M UR N N 403 500 80.6 413 500 82.6 964 1500 64.2667 1064 1300 81.8462 309.3128 77.33 72.41 4 81.328 TH MISHRA BHOJPUR MISHRA SHREE DEVRADH, SUNITA 4 1785 DHAR 03.01.1986 F TIYAR, EWS N N 537 700 76.7143 683 900 75.8889 1179 1500 78.6 1054 1300 81.0769 312.2801 78.07 55.33 2 80.07 KUMARI DUBEY BHOJPUR VIPUL NAWAL GAUSGANJA 5 1770 KUMAR KISHOR 01.04.1979 M UR N N 711 900 79 693 900 77 1177 1500 78.4667 1834 2400 76.4167 310.8833 77.72 62.66 2 79.721 RA SINGH SINGH DHAMANIA, HIMANSHU RAMESHW 6 424 26/01/1996 M GARAHANI, EBC N N 419 500 83.8 350 500 70 722 1000 72.2 998 1300 76.7692 302.7692 75.69 70.67 4 79.692 SHEKHAR AR PRASAD BHOJPUR ROHAI, ASHWANI -

Bihar State Power Transmission Company Ltd., Patna (Department of Transmission) EXISTING GRIDS at DIFFERENT VOLTAGE LEVELS

As on: 25.03.2014 Bihar State Power Transmission Company Ltd., Patna (Department of Transmission) EXISTING GRIDS AT DIFFERENT VOLTAGE LEVELS SL. NAME OF GRID VOLTAGE CAPACITY VOLTAGE CAPACITY VOLTAGE CAPACITY DISTRICT BLOCK NO. SUBS. LEVEL (in MVA) LEVEL (in MVA) LEVEL (in MVA) (220/132)KV (132/33)KV (132/25)KV 1. Forbeshganj ------ ----- (132/33) KV 2x20 ----- ------ Araria Forbeshganj 2. Sonenagar ------ ----- (132/33) KV 1x50+1x10+2x20 (132/25)KV 1X20 + 1X21.6 Aurangabad Barun 3. Rafiganj ------ ----- (132/33) KV 2x20 ----- ------ Aurangabad Rafiganj 4. Aurangabad ------ ----- (132/33) KV 2X20 ----- ------ Aurangabad Aurangabad 5. Goh ------ ----- (132/33) KV 2x20 ----- ------ Aurangabad Goh 6. Begusarai (220/132)KV 2x100 (132/33) KV 2x50 ----- ------ Begusarai Barauni 7. Buxar ------ ----- (132/33) KV 2x20 ----- ------ Buxar Itarhi 8. Dumraon ------ ----- (132/33) KV 2x20 ----- ------ Buxar Dumraon 9. Sabour ------ ----- (132/33) KV 2X50 ----- ------ Bhagalpur Sabour 10. Sultanganj ------ ----- (132/33) KV 2X20 ----- ------ Bhagalpur Sultanganj 11. Kahalgaon ------ ----- (132/33) KV 2X20 + 1x50 ----- ------ Bhagalpur Kahalgaon 12. Naugachhia ------ ----- (132/33) KV 2X20 ----- ------ Bhagalpur Naugachhia 13. Ara ------ ----- (132/33) KV 1X20+ 1x50 ----- ------ Bhojpur Ara 14. Banka ------ ----- (132/33) KV 2X20 ----- ------ Banka Banka 15. Darbhanga (220/132)KV 2X100 (132/33) KV 1X50 + 1X20 ----- ------ Darbhanga Bahadurpur 16. Motihari ------ ----- (132/33) KV 2X20 ----- ------ East Champaran Motihari 17. Dhaka ------ ----- (132/33) KV 1X10+1x20 ----- ------ East Champaran Dhaka 18. Raxaul ------ ----- (132/33) KV 2X20 ----- ------ East Champaran Raxaul 19. Bodh Gaya (220/132) KV 3X150 (132/33) KV 2X50 ----- ------ Gaya Bodh Gaya 20. Chandauti ------ ----- (132/33) KV 2X50 (132/25) KV 2X13.35 Gaya Gaya 21. Belaganj ------ ----- (132/33) KV 2x20 ----- ------ Gaya Belaganj As on: 25.03.2014 22. -

Sr.No . Ward Name Father/Husband Adhar Bank Name Accountno

Sr.No Ward Name Father/Husband Adhar Bank name Accountno. present address . Mobile 1 1 rinku devi dablu sonkar Available union bank Available chillupar barhalganj Available 2 1 baby devi jaswant sonkar Available union bank Available chillupar barhalganj Available 3 1 surenddra sonkar ramdas Available oriental bank Available chillupar barhalganj Available 4 1 mannu devi nebulal sonkar Available oriental bank Available chillupar barhalganj Available 5 1 chinta devi rajesh sonkar Available purvanchal bank Available chillupar barhalganj Available 6 1 laliya gulab sonkar Available union bank Available chillupar barhalganj Available 7 1 viraju babulal Available union bank Available chillupar barhalganj Available 8 1 dileep kumar somkar babulal sonkar Available union bank Available chillupar barhalganj Available 9 1 patiya sonkar munib sonkar Available union bank Available chillupar barhalganj Available 10 1 radha devi amarnath Available indian overseas bank Available chillupar barhalganj Available 11 1 Anil Sonkar shiv prakash Sonkar Available punjab national bank Available tahsil chauraha Available 12 1 arun kumar maddhesia anmol prasad Available bank of baroda Available mahadeva muhalla Available 13 1 shakeel ahmad vakil ahmad ansari Available purvanchal bank Available kasab tola barhalganj Available 14 1 suresh chand varma ramashankar Available punjab national bank Available kasab tola barhalganj Available 15 1 geeta devi nandlal verma Available purvanchal bank Available purana gola muhalla Available 16 1 Leelawati Devi Sonkar Phoolchand -

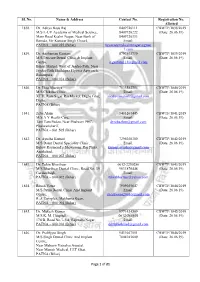

Cbwtf/1838/2019

Sl. No. Name & Address Contact No. Registration No. Allotted 1838. Dr. Aditya Basu Raj 8409726111 CBWTF/1838/2019 M/S L-UV Academy of Medical Science, 8409726222 (Date: 26.06.19) Main Road Keshri Nagar, Near Bank of 8409726333 Baroda, Vir Kunwar Singh Chowk, Email: PATNA – 800 025 (Bihar) luvacademykeshrinagar@gmai l.com 1839. Dr. Anshuman Gautam 8797503739 CBWTF/1839/2019 M/S Pericare Dental Clinic & Implant Email: (Date: 26.06.19) Centre, [email protected] Bihari Market, West of Jagdeo Path, Near Jagdeo Path Sheikhpra Flyover Approach, Rukanpura, PATNA – 800 014 (Bihar) 1840. Dr. Ekta Bhartiya 7033582754 CBWTF/1840/2019 M/S Chikitsa Clinic, Email: (Date: 26.06.19) XTTI, Ram Sagar Rai Market, Digha Ghat, [email protected] Digha, PATNA (Bihar) 1841. Zeba Alam 9431267445 CBWTF/1841/2019 M/S A Y Health Care, Email: (Date: 26.06.19) Tam Tam Padao, Near Phulwari PHC, [email protected] Phulwarisharif, PATNA – 801 505 (Bihar) 1842. Dr. Ayusha Kumari 7295038300 CBWTF/1842/2019 M/S Daant Dental Speciality Clinic, Email: (Date: 26.06.19) Below Raymond’s Showroom, Raj Plaza, [email protected] Anishabad, PATNA – 800 002 (Bihar) 1843. Dr. Tuhin Bharthuar 0612-2250286 CBWTF/1843/2019 M/S Bharthuar Dental Clinic, Road No. 39, 9631876448 (Date: 26.06.19) Gardanibagh, Email: PATNA – 800 002 (Bihar) [email protected] 1844. Ritesh Vatsa 7909055647 CBWTF/1844/2019 M/S Patna Dental Clinic And Implant Email: (Date: 26.06.19) Centre, [email protected] R. J. Complex, Makhania Kuan, PATNA – 800 004 (Bihar) 1845. Dr. Mukesh Kumar 9771424509 CBWTF/1845/2019 M/S K. -

Presentation for 2Nd CADWM Conference at Ahmedabad, Gujrat on 28Th May 2019 BIHAR DURGAWATI RESERVOIR CADWM PROJECT a CASE STUDY…………… 3 Introduction

Presentation for 2nd CADWM Conference at Ahmedabad, Gujrat on 28th May 2019 BIHAR DURGAWATI RESERVOIR CADWM PROJECT A CASE STUDY…………… 3 Introduction . The implications of a sustained growth of agricultural sector is huge for the economy of Bihar. Considering that about 88.7 percent of the state’s population resides in rural areas, agricultural sector holds the key for its overall growth. Located in the eastern part of India, Bihar has an area of 93.6 lakh hectares, accounting for nearly 3 percent of the country’s total geographical area. Overall about 56.55 percent of the land is under cultivation in Bihar . Bihar is endowed with rich ground and surface water resources. Along with the river Ganges, the tributaries of Gandak, Ghaghra, Burhi Gandak, Kosi, Mahananda, Karmanasa, Sone, Punpun, Phalgu, Sakri and Kiul contribute towards availability of water in Bihar for agricultural and non-agricultural purposes. Only around 57 percent of the cultivated area in the state is irrigated. The agricultural sector in the state is largely dependent on monsoons and the varying water resource endowments in the southern and northern parts of Bihar calls for a need to identify mechanisms to ensure adequate, timely and assured irrigation for cultivation. In the context of adoption of productivity enhancing inputs such as improved seeds, fertilizers and new methods of cultivation, irrigation plays an important role. State government has envisaged specific initiatives for better water management and creation of irrigation potential through measures such as:- • Restoration and extension of canals • Schemes for surface & groundwater irrigation • Command area development • Intra-state linking of rivers Annual Rainfall in Bihar (2001-2017) (in mms) 1600 1400 1200 1000 800 600 400 200 0 Irrigation at a Glance . -

DISTRICT : Vaishali

District District District District District Sl. No. Name of Husband's/Father,s AddressDate of Catego Full Marks Percent Choice-1 Choice-2 Choice-3 Choice-4 Choice-5 Candidate Name Birth ry Marks Obtained age (With Rank) (With Rank) (With Rank) (With Rank) (With Rank) DISTRICT : Vaishali 1 KIRAN KUMARIARVIND KUMAR kiran kumari c/o arvind 10-Dec-66 GEN 700 603 86.14 Muzaffarpur (1) Samastipur (1) Darbhanga (1) Vaishali (1) Champaran-E (1) kumar vill+po-parsara dis-muzaffarpur 2 SANDHYA SHRI JAY PRSHAK vill+po-mamudhpur,ps- 12-Jun-68 GEN 700 572 81.71 Saran (1) Siwan (1) Gopalganj (1) Vaishali (2) Patna (4) KUMARI UPADHIA mazi,dis-chapra (bihar)pin-841223 3 SUDHA KUMARISRI VIVEK RANJAN vill. + post. -top 10-Jan-86 MBC 700 570 81.43 Patna (5) Nalanda (5) Vaishali (3) Jahanabad (3) Bhojpur (1) SINHA thana - sahajapur, vaya - karaipasurai dist. patna - pin - 801304 4PREM LATA SHRI NAND LAL PD. village raj bigha, p.s. 10-Jan-79 MBC 700 566 80.86 Patna (7) Arwal (3) Jahanabad (4) Nalanda (6) Vaishali (4) KUMARI dhanarua p.o barni district patna pin code 804452 5 REENA SINHASRI DINESH SINGH dinesh singh, d/o- sita 31-Dec-76 BC 900 721 80.11 Siwan (2) Begusarai (3) Muzaffarpur (4) Samastipur (4) Vaishali (5) sharan singh, vill- ruiya, post- ruiya bangra, p.s.- jiradei, distt- siwan 6 CHANCHAL SRI JAMUNA SINGH w/o- sanjay kumar 14-Jan-73 BC 900 720 80 Vaishali (6) Jahanabad (7) Nalanda (8) Patna (9) Nawada (7) KUMARI sinha, vill- fatehpur, post- musadhi, p.s.- kray par sarai, distt- nalanda, pin- 801304 7 NEERU KUMARIKEDAR PANDEY vill-pusa sadpur 15-Jan-78 GEN 700 539 77 Muzaffarpur (8) Samastipur (6) Sitamarahi (1) Vaishali (7) Saran (5) po-sadpur dis-samastipur 8 MINTU KUMARISRI RAM PUJAN d/o- sri ram pujan singh, 01-Oct-71 GEN 500 385 77 Muzaffarpur (9) Vaishali (8) Saran (6) Samastipur (7) Darbhanga (3) SINGH vill+post- pratappur, via- gidadha, muzaffarpur 9 ARCHANA SHRI- BAKIL vill- ashiya chak , 15-Jun-79 BC 900 692 76.89 Patna (19) Vaishali (9) Saran (7) Bhojpur (4) Bhagalpur (24) KUMARI PRASAD SINGH. -

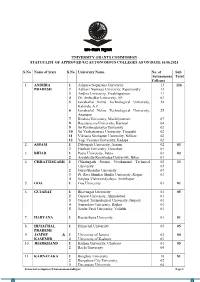

University Grants Commission Status List of Approved 832 Autonomous Colleges As on Date 16.06.2021

f FTele No. :-011-23222595 Kku&foKku foeqDr;s UNIVERSITY GRANTS COMMISSION STATUS LIST OF APPROVED 832 AUTONOMOUS COLLEGES AS ON DATE 16.06.2021 S.No Name of State S.No. University Name No. of Sub Autonomous Total Colleges 1. ANDHRA 1 Achraya Nagarjuna University 13 116 PRADESH 2 Adikavi Nannaya University, Rajamundry 13 3 Andhra University, Visakhapatnam 11 4 Dr. Ambedkar University, AP 01 5 Jawaharlal Nehru Technological University, 34 Kakinda, A.P. 6 Jawaharlal Nehru Technological University, 25 Anantpur 7 Krishna University, Machilipatnam 07 8 Rayalaseema University, Kurnool 04 9 Sri Krishnadevarya University 02 10 Sri Venkateswara University, Tirupathi 02 11 Vikrama Simhapuri University, Nellore 02 12 Yogi Vemana University, Kadapa 02 2. ASSAM 1 Dibrugarh University, Assam 02 03 2 Gauhati University, Guwahati 01 3. BIHAR 1 Patna University, Patna 01 02 2 Aryabhatta Knowledge University, Bihar 01 4. CHHATTISGARH 1 Chhatisgarh Swami Vivekanand Technical 02 13 University 03 2 Guru Ghasidas University 07 3 Pt. Ravi Shankar Shukla University, Raipur 01 4 Sarguja Vishwavidyalaya, Ambikapur 5. GOA 1 Goa University 01 01 6. GUJARAT 1 Bhavnagar University 01 05 2 Gujarat University, Ahmedabad 01 3 Gujarat Technological University, Gujarat 01 4 Saurashtra University, Rajkot 01 5 Sardar Patel University, Vallabh 01 7. HARYANA 1 Kurukshetra University 01 01 8. HIMACHAL 1 Himachal University 05 05 PRADESH 9. JAMMU & 1 University of Jammu 03 04 KASHMIR 2 University of Kashmir 01 10. JHARKHAND 1 Kolhan University, Chaibasa 01 05 2 Rachi University 04 11. KARNATAKA 1 Banglore University 18 81 2 Bengaluru City University, 02 3 Davangere University 04 Status List of Approved Autonomous Colleges Page 1 4 Gulbarga University 01 5 Karnataka State Law University, Huballi 01 6 Kuvempu University 02 7 Mangalore University 08 8 Mysore University 12 9 Rani Channamma University, Belgaum 04 10 Tumkur University, 01 11 Vijayanagara Srikrishnadevaraya University, 01 Bellari 12 Visvesvaraya Technological University 27 12. -

Block Teacher Niyojan-2019-20

BLOCK TEACHER NIYOJAN-2019-20 BLOCK: PIRO CLASS-1-5 (GEN) DIST:-BHOJPUR PROVISIONAL MERIT LIST ONLY NON-B.ED APPLICANTS 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 MATRIC INTER TRAINING FREE SUM OF AVG OF BTET/ WEIGT APPL.S. NAME OF SE D. FUL CTET AGE OF TOTAL TRAININ S.N. FATHER DOB ADDRESS CAT DIS. MARKS MARKS FULL MARKS FULL PERCENT PERCENT REMARKS N. APPLICANT X FIGH L MARK BTET/C MERIT G TYPE OBTAI %GE OBTAIN MAR %GE OBTAIN MARK %GE AGE AGE T. MAR S% TET NED ED KS ED S KS GALCHAUR ANKITA RAM AGYA DIPLOM 1 2060 24/11/1997 F KRISHNAGARH BC NN 456 500 91.2 435 500 87 1759 2300 76.4783 254.678 84.89 79.6 4 88.89275 RANI SINGH A BHOJPUR PALLAWE PRABODH DIPLOM 2 1461 05.03.1998 F PAWNA BHOJPUR UR NN 428 500 85.6 439 500 87.8 1840 2300 80 253.4 84.47 75.3 4 88.46667 E KUMAR A SHIV SANJAY KUMAR KUMAR DIPLOM 3 1447 10.01.1990 M NAGRA BALIYA UR NN 425 500 85 486 600 81 2896 3200 90.5 256.5 85.50 64.7 2 87.5 UPADHYA UPADHYA A Y Y BHANU JAWAHIR DARIYAPUR DIPLOM 4 1967 KUMAR 20/12/1996 M SC NN 418 500 83.6 417 500 83.4 779 950 82 249 83.00 71 4 87 RAM MUFFASIL ARA A RAM OMPRAKA JAMALPUR VIPUL SH BAZBHADUR DIPLOM 5 1220 SRIVASTA 07.12.1996 M UR NN 445 600 74.167 421 500 84.2 2874 3200 89.8125 248.179 82.73 71.3 4 86.72639 SRIVASTA ,SIDHRI, A VA VA AZAMGARH RAM RUWASPUR HIRALAL DIPLOM 6 1994 SURESH 11.09.1983 M BARHARA SC NN 418 600 69.667 462 600 77 1230 1500 82 228.667 76.22 90 10 86.22222 RAM A RAM BHOJPUR DEEPAK RAMASHR DIPLOM 7 P/8 14.07.1999 M AGASADA SIWAN BC NN 518 600 86.333 429 500 85.8 1557 1950 79.8462 251.979 83.99 65.3 2 85.99316 YADAV AY YADAV A ARUN SHIVAM DIPLOM 8 P/446 KUMAR 19/10/1996 M DERAWAN U.P. -

(70860) BIHAR (Pashchim Champaran) (BETIAH ) 8541946156

Volunteer Name with Reg No State (District) (Block) Mobile no ANURADHA MISHRA (70860) BIHAR (Pashchim Champaran) (BETIAH ) 8541946156 ABHISHEK KUMAR (69365) BIHAR (Pashchim Champaran) (NAUTA) 8757124405 PANKAJ KUMAR (69366) BIHAR (Pashchim Champaran) (RAMNAGAR) 9546123728 KAMESHWAR KUMAR (69367) BIHAR (Pashchim Champaran) (BERIA) 6200894193 AKHILESH KUMAR BIHAR (Pashchim Champaran) (MONAHA) 9973449545 GOPTA (69368) BIHAR (Pashchim RAUSHAN KUMAR (69369) 8863071757 Champaran) (NARKATIYAGANJ ) RAVI KUMAR PATEL (70856) BIHAR (Pashchim Champaran) (BAGHA 1) 9507470245 LOKESH KUMAR (69364) BIHAR (Pashchim Champaran) (BETIAH ) 8512022009 ANOOP HANSRAJ (70858) BIHAR (Pashchim Champaran) (MAINATAD) 7004523434 MANJU KUMARI (70859) BIHAR (Pashchim Champaran) (MAINATAD) 9162841370 LOKESH KUMAR (71645) BIHAR (Pashchim Champaran) (MONAHA) 7352355039 KAMLESH KUMAR BIHAR (Pashchim Champaran) (MADHUBANI) 7250137647 SINGH (71684) MD SHOAIB AKHTER (72150) BIHAR (Pashchim Champaran) (SIKTA) 8873361184 VIJAY KUMAR BIHAR (Pashchim Champaran) (MADHUBANI) 8969237540 KUSHWAHA (72148) JA (72147) BIHAR (Pashchim Champaran) (SIKTA) 7091880062 SHALU KUMARI (72146) BIHAR (Pashchim Champaran) (JOGAPATTI) 7634850501 AMISHA KUMARI (72151) BIHAR (Pashchim Champaran) (BERIA) 9631357767 SHIKHA GUPTA (70857) BIHAR (Pashchim Champaran) (PIPRASI) 8051457544 BIHAR (Pashchim SHIKHA KUMARI (68876) 9576221125 Champaran) (NARKATIYAGANJ ) MANISHA KUMARI (68594) BIHAR (Pashchim Champaran) (BAGHA 2) 6203884492 ANIL KUMAR (71644) BIHAR (Pashchim Champaran) (NAUTA) 9931348136 PREETI -

Consolidated Cdpos Fund Tranfer Status

CDPOs Master Account ‐ Fund Tranfer Status under Bal Kuposan Mukt Bihar Training S.No District NamProject Name Bank Name Branch Name Account No IFSC Code Amount 1 Araria Raniganj STATE BANK OF INDIA ARARIA 11432637209 SBIN0000009 103750 2 Araria Jokihaat STATE BANK OF INDIA ARARIA MAIN BRANCH 11432638859 SBIN0000009 81650 3 Araria Sikit STATE BANK OF INDIA ARARIA 11432637334 SBIN0000009 46550 4 Araria Farbisganj STATE BANK OF INDIA FARBISGANJ 11505794555 SBIN0000077 127800 5 Araria Palasi STATE BANK OF INDIA ARARIA 11432637628 SBIN0000009 67025 6 Araria Bhargama STATE BANK OF INDIA FORBESGANJ 11505794260 SBIN0000077 64750 7 Araria Araria STATE BANK OF INDIA SBI MAIN BRANCH ARARIA 31864124489 SBIN0000009 121625 8 Araria Kursakata STATE BANK OF INDIA ARARIA 11432637639 SBIN0000009 43625 9 Araria Narpatganj STATE BANK OF INDIA FORBISGANJ 11505794566 SBIN0000077 90100 10 Arwal Kurtha UNION BANK OF INDIA KURTHA BRANCH 364502010010058 UBIN0536458 39400 11 Arwal Kaler BANK OF INDIA Arwal 447720100000598 BKID0004477 47525 12 Arwal Arwal BANK OF INDIA ARWAL 447720100000197 BKID0004477 48825 13 Arwal Karpi BANK OF INDIA Arwal 447700100000194 BKID0004477 59875 14 Arwal Sonbhadra Banshi Suryapur BANK OF INDIA ARWAL 447720100000597 BKID0004477 26400 15 Aurangabad Aurangabad STATE BANK OF INDIA AURANGABAD 11113376102 SBIN0000013 78400 16 Aurangabad Goh STATE BANK OF INDIA GOH 11436538157 SBIN0012600 66375 17 Aurangabad Nabinager STATE BANK OF INDIA NABINAGAR 33466594125 SBIN0002980 83925 18 Aurangabad Kutumba STATE BANK OF INDIA AURANGABAD 11707648051 -

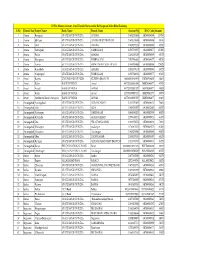

Cbs Sol Id Alpha Code Zone Name Region Name Bank

CBS_SOL ID ALPHA CODE ZONE NAME REGION NAME BANK NAME BRANCH NAME AREA DATE OF O STATE DISTRICT SUBDISTRICT_NAME CENTER_NAME ADDRESS 2774 PBBAHM AHMEDABAD ZONE AHMEDABAD ‐ I REGION BANK OF BARODA AHMEDABAD GEN METRO 36775 GUJARAT AHMEDABAD AHMEDABAD CITY AHMADABAD (M CORP.) NEHRU NAGAR SURENDRA MANGALDAS ROAD NEHRU NAGAR, , , AMBAWADI, 380015 GF, MILLENIUM PLAZA AKHABARNAGAR CIRCILE GF, MILLENIUM PLAZA AKHABARNAGAR, , , 5543 AKHABA AHMEDABAD ZONE AHMEDABAD ‐ I REGION BANK OF BARODA AKHABARNAGAR METRO 42089 GUJARAT AHMEDABAD AHMEDABAD CITY AHMADABAD (M CORP.) NAVA WADAJ, 380013 PANCHVATI MARG,AMBAWADI,AHMEDABAD‐6 PANCHVATI MARG,AMBAWADI,AHMEDABAD‐6, , , , 0320 AMBAWA AHMEDABAD ZONE AHMEDABAD ‐ I REGION BANK OF BARODA AMBAWADI METRO 23347 GUJARAT AHMEDABAD AHMEDABAD CITY AHMADABAD (M CORP.) 380006 2939 VEJALP AHMEDABAD ZONE AHMEDABAD ‐ I REGION BANK OF BARODA ANANDNAGAR METRO 38225 GUJARAT AHMEDABAD AHMEDABAD CITY AHMADABAD (M CORP.) ANAND NAGAR, 100 FT.ROAD, VEJALPUR ANAND NAGAR, 100 FT.ROAD, VEJALPUR, , , , 380051 ASHRAM ROAD,OPP.NATRAJ CINEMA,AHMEDABAD‐380009 ASHRAM ROAD,OPP.NATRAJ 0849 ASHRAM AHMEDABAD ZONE AHMEDABAD ‐ I REGION BANK OF BARODA ASHRAM ROAD METRO 27757 GUJARAT AHMEDABAD AHMEDABAD CITY AHMADABAD (M CORP.) CINEMA,AHMEDABAD‐380009, , , , 380009 IST FLOOR, RUDRA SQUARE BODAKDEV CROSS ROAD IST FLOOR, RUDRA SQUARE BODAKDEV, 4221 BODAKD AHMEDABAD ZONE AHMEDABAD ‐ I REGION BANK OF BARODA BODAKDEV METRO 41179 GUJARAT AHMEDABAD AHMEDABAD CITY AHMADABAD (M CORP.) AHMEDABAD, , , BODAKDEV, AHMEDABAD, 380015 2953 CHANDK AHMEDABAD ZONE