Annual Report 1989.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1 Executive Summary Mauritius Is an Upper Middle-Income Island Nation

Executive Summary Mauritius is an upper middle-income island nation of 1.2 million people and one of the most competitive, stable, and successful economies in Africa, with a Gross Domestic Product (GDP) of USD 11.9 billion and per capita GDP of over USD 9,000. Mauritius’ small land area of only 2,040 square kilometers understates its importance to the Indian Ocean region as it controls an Exclusive Economic Zone of more than 2 million square kilometers, one of the largest in the world. Emerging from the British colonial period in 1968 with a monoculture economy based on sugar production, Mauritius has since successfully diversified its economy into manufacturing and services, with a vibrant export sector focused on textiles, apparel, and jewelry as well as a growing, modern, and well-regulated offshore financial sector. Recently, the government of Mauritius has focused its attention on opportunities in three areas: serving as a platform for investment into Africa, moving the country towards renewable sources of energy, and developing economic activity related to the country’s vast oceanic resources. Mauritius actively seeks investment and seeks to service investment in the region, having signed more than forty Double Taxation Avoidance Agreements and maintaining a legal and regulatory framework that keeps Mauritius highly-ranked on “ease of doing business” and good governance indices. 1. Openness To, and Restrictions Upon, Foreign Investment Attitude Toward FDI Mauritius actively seeks and prides itself on being open to foreign investment. According to the World Bank report “Investing Across Borders,” Mauritius has one of the world’s most open economies to foreign ownership and is one of the highest recipients of FDI per capita. -

R Basant Roi: Bank of Mauritius' New Headquarters

R Basant Roi: Bank of Mauritius’ new headquarters Address by Mr R Basant Roi, Governor of the Bank of Mauritius, at the inauguration of the New Headquarters Building of the Bank of Mauritius, Port Louis, 18 December 2006. * * * Dr. The Hon. Navinchandra Ramgoolam, Prime Minister of the Republic of Mauritius Honourable Ramakrishna Sithanen, Deputy Prime Minister, Minister of Finance and Economic Development His Lordship Mayor of Port Louis Hon. Judges Members of the Diplomatic Corps Fellow Bankers Ladies and Gentlemen Good Afternoon I am pleased to welcome you all to the inauguration of the New Headquarters Building of the Bank of Mauritius. I am privileged and honoured to perform this inaugural ceremony in your distinguished presence, Prime Minister, Sir – a ceremony that is similar to the one performed by the first Governor of the Bank, Mr. Aunauth Beejadhur, for the existing building in the presence of His Excellency, Sir John Shaw Rennie, Governor of Mauritius and late Sir Seewoosagur Ramgoolam, then Premier and Minister of Finance on 31st May 1967. One of the major constraints in the operation of the Bank when it was established way back in 1967 was insufficient office space. The offices of the Bank were located at various places in Port Louis. Security vault for notes and coins was located at the back of the Treasury building, Exchange Control at the entrance of the present Government Centre and Main Office at the Anglo Mauritius Building. In August 1968, a banking office was opened at the Treasury Building to accommodate the increasing volume of banking business. The existing Bank of Mauritius building at the corner of Sir William Newton St and Royal Road was designed by Messrs Victor Heal and Partners of London. -

Tax Relief Country: Italy Security: Intesa Sanpaolo S.P.A

Important Notice The Depository Trust Company B #: 15497-21 Date: August 24, 2021 To: All Participants Category: Tax Relief, Distributions From: International Services Attention: Operations, Reorg & Dividend Managers, Partners & Cashiers Tax Relief Country: Italy Security: Intesa Sanpaolo S.p.A. CUSIPs: 46115HAU1 Subject: Record Date: 9/2/2021 Payable Date: 9/17/2021 CA Web Instruction Deadline: 9/16/2021 8:00 PM (E.T.) Participants can use DTC’s Corporate Actions Web (CA Web) service to certify all or a portion of their position entitled to the applicable withholding tax rate. Participants are urged to consult TaxInfo before certifying their instructions over CA Web. Important: Prior to certifying tax withholding instructions, participants are urged to read, understand and comply with the information in the Legal Conditions category found on TaxInfo over the CA Web. ***Please read this Important Notice fully to ensure that the self-certification document is sent to the agent by the indicated deadline*** Questions regarding this Important Notice may be directed to Acupay at +1 212-422-1222. Important Legal Information: The Depository Trust Company (“DTC”) does not represent or warrant the accuracy, adequacy, timeliness, completeness or fitness for any particular purpose of the information contained in this communication, which is based in part on information obtained from third parties and not independently verified by DTC and which is provided as is. The information contained in this communication is not intended to be a substitute for obtaining tax advice from an appropriate professional advisor. In providing this communication, DTC shall not be liable for (1) any loss resulting directly or indirectly from mistakes, errors, omissions, interruptions, delays or defects in such communication, unless caused directly by gross negligence or willful misconduct on the part of DTC, and (2) any special, consequential, exemplary, incidental or punitive damages. -

ANNUAL REPORT MAUBANK Annual Report 2019 001 Table of Contents

ANNUAL REPORT MAUBANK Annual Report 2019 001 Table of Contents 004 Corporate information 007 Chairman Statement 008 Chief Executive Statement 012 Directors’ report 021 Corporate governance report 035 Statement of compliance 037 Statement of management’s responsibility for financial reporting 038 Report from the secretary 039 Independent auditor’s report 043 Statements of financial position 045 Statements of profit or loss and other comprehensive income 047 Statements of changes in equity 049 Cash flow statements for the year ended 050 Notes to the financial statements 154 Management discussion and analysis 173 Administrative information CORPORATE INFORMATION MAUBANK 004 Annual Report 2019 Corporate Information DIRECTORS: Non-Executive Directors Appointed on Resigned on Mr Burkutoola Mahmadally (Chairman) 29 March 2019 Mr Lalloo Said (Chairman) 20 January 2016 01 October 2018 Dr Paligadu Dharamraj (was appointed Acting Chairman on 06 June 2018) 07 March 2015 06 August 2019 Mr Nicolas Jean Marie Cyril 13 March 2015 Mr Putchay Vassoo Allymootoo 20 January 2016 05 September 2019 Mr Gokhool Ashvin Jain 23 February 2016 Mr Nilamber Anoop Kumar 22 March 2016 Mr Codabux Muhammad Javed 10 March 2017 Executive Directors Mr Mungar Premchand 23 November 2018 Mr Nagarajan Sridhar 24 September 2015 21 September 2018 MAUBANK Annual Report 2019 005 KEY MANAGEMENT TEAM: Position Mr Mungar Premchand Chief Executive Officer (As from 23 November 2018) Mr Nagarajan Sridhar (As from 24 September 2015 to 21 September 2018) Chief Executive Officer Mr Vydelingum -

State Bank of Mauritius (Sbm) Holdings Limited Analysis: Is Investors Cash Safe with Sbm?

STATE BANK OF MAURITIUS (SBM) HOLDINGS LIMITED ANALYSIS: IS INVESTORS CASH SAFE WITH SBM? January 2018 i List of Abbreviations: BOM – Bank of Mauritius CBK – Central bank of Kenya EOI – Expression of Interest KDIC – Kenya Deposit Insurance Corporation Kes – Kenya Shillings NAV – Net Assets Value SEMTRI - Stock Exchange of Mauritius Total Return Index SEM – Stock Exchange of Mauritius SBM – State bank of Mauritius ROE – Return on Equity USD – United States Dollar ii Table of Contents Executive Summary ........................................................ 1 Bank Overview.............................................................. 2 Ownership and Governance .............................................. 2 Corporate Governance .................................................... 3 SBM Stock Performance ................................................... 5 SBMH Acquisition of Fidelity Commercial Bank (Kenya) ............. 5 SBM Financial Performance ............................................... 6 SBM Holding Comparison with some selected Kenyan Banks ........ 9 SBM’s Binding Offer on Chase Bank ................................... 10 Chase Bank Acquisition Terms ......................................... 10 Fusion’s View on the terms of this deal .............................. 11 Fusion’s View on SBM Bank acquiring Chase Bank .................. 12 iii Executive Summary SBM Holdings ‘SBM’ was founded in 1973 by the Government of Mauritius and was listed in the Stock Exchange of Mauritius ‘SEM’ in 1995. The Bank is engaged in banking, non-banking -

Payment Systems in Mauritius

THE PAYMENT SYSTEM IN MAURITIUS Table of Contents OVERVIEW OF THE NATIONAL PAYMENT SYSTEM IN MAURITIUS .......................... 79 1. INSTITUTIONAL ASPECTS .............................................................................................. 80 1.1 General legal aspects ................................................................................................... 80 1.2 Role of financial intermediaries that provide payment services ............................ 80 1.2.1 Domestic banks ................................................................................................ 81 1.2.2 Offshore banks ................................................................................................. 81 1.2.3 Non-bank financial institutions authorised to transact deposit-taking business .................................................................................... 81 1.2.4 Savings banks ................................................................................................... 82 1.2.5 Housing corporation ........................................................................................ 82 1.2.6 Development bank............................................................................................. 82 1.2.7 Foreign exchange dealers ................................................................................ 82 1.2.8 Other financial institutions ............................................................................... 83 1.3 Role of the central bank ............................................................................................ -

Social Democracy in Mauritius

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Stellenbosch University SUNScholar Repository Development with Social Justice? Social Democracy in Mauritius Letuku Elias Phaahla 15814432 Thesis presented in partial fulfillment of the requirements for the degree of Master of Arts (International Studies) at Stellenbosch University Supervisor: Professor Janis van der Westhuizen March 2010 ii Declaration By submitting this thesis electronically, I declare that the entirety of the work contained therein is my own, original work, that I am the owner of the copyright thereof (unless to the extent explicitly otherwise stated) and that I have not previously in its entirety or in part submitted it for obtaining any qualification. Signature:……………………….. Date:…………………………….. iii To God be the glory My dearly beloved late sisters, Pabalelo and Kholofelo Phaahla The late Leah Maphankgane The late Letumile Saboshego I know you are looking down with utmost pride iv Abstract Since the advent of independence in 1968, Mauritius’ economic trajectory evolved from the one of a monocrop sugar economy, with the latter noticeably being the backbone of the country’s economy, to one that progressed into being the custodian of a dynamic and sophisticated garment-dominated manufacturing industry. Condemned with the misfortune of not being endowed with natural resources, relative to her mainland African counterparts, Mauritius, nonetheless, was able to break the shackles of limited economic options and one of being the ‘basket-case’ to gradually evolving into being the upper-middle-income country - thus depicting it to be one of the most encouraging economies within the developing world. -

International Directory of Deposit Insurers

A listing of addresses of deposit insurers, central banks and other entities involved in deposit insurance functions. Division of Insurance and Research Federal Deposit Insurance Corporation Washington, DC 20429 The FDIC thanks the countries listed for their cooperation, without which the directory would not have been possible. Please direct any comments or corrections to: Donna Vogel Division of Insurance and Research, FDIC by phone +1 202 898 8703 or by e-mail [email protected] FDIC INTERNATIONAL DIRECTORY OF DEPOSIT INSURERS ■ OCTOBER 2018 Table of Contents AFGHANISTAN ......................................................................................................................................6 ALBANIA ...............................................................................................................................................6 ALGERIA ................................................................................................................................................6 ARGENTINA ..........................................................................................................................................6 ARMENIA ..............................................................................................................................................7 AUSTRALIA ............................................................................................................................................7 AUSTRIA ................................................................................................................................................7 -

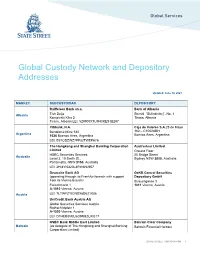

Global Custody Network and Depository Addresses

Global Custody Network and Depository Addresses Updated: June 30, 2021 MARKET SUBCUSTODIAN DEPOSITORY Raiffeisen Bank sh.a. Bank of Albania Albania Tish Daija Sheshi “Skënderbej”, No. 1 Kompleski Kika 2 Tirana, Albania Tirana, Albania LEI: 529900XTU9H3KES1B287 Citibank, N.A. Caja de Valores S.A.25 de Mayo Bartolome Mitre 530 362 – C1002ABH Argentina 1036 Buenos Aires, Argentina Buenos Aires, Argentina LEI: E57ODZWZ7FF32TWEFA76 The Hongkong and Shanghai Banking Corporation Austraclear Limited Limited Ground Floor HSBC Securities Services 20 Bridge Street Australia Level 3, 10 Smith St., Sydney NSW 2000, Australia Parramatta, NSW 2150, Australia LEI: 2HI3YI5320L3RW6NJ957 Deutsche Bank AG OeKB Central Securities (operating through its Frankfurt branch with support Depository GmbH from its Vienna branch) Strauchgasse 3 Fleischmarkt 1 1011 Vienna, Austria A-1010 Vienna, Austria Austria LEI: 7LTWFZYICNSX8D621K86 UniCredit Bank Austria AG Global Securities Services Austria Rothschildplatz 1 A-1020 Vienna, Austria LEI: D1HEB8VEU6D9M8ZUXG17 HSBC Bank Middle East Limited Bahrain Clear Company Bahrain (as delegate of The Hongkong and Shanghai Banking Bahrain Financial Harbour Corporation Limited) STATE STREET CORPORATION 1 GLOBAL CUSTODY NETWORK AND DEPOSITORY ADDRESSES MARKET SUBCUSTODIAN DEPOSITORY 1st Floor, Bldg. #2505 Harbour Gate (4th Floor) Road # 2832, Al Seef 428 Kingdom of Bahrain Manama, Kingdom of Bahrain LEI: 549300F99IL9YJDWH369 Standard Chartered Bank Bangladesh Bank Silver Tower, Level 7 Motijheel, Dhaka-1000 52 South Gulshan Commercial -

Mauritius RISK & COMPLIANCE REPORT DATE: May 2017

Mauritius RISK & COMPLIANCE REPORT DATE: May 2017 KNOWYOURCOUNTRY.COM Executive Summary - Mauritius Sanctions: None FAFT list of AML No Deficient Countries Not on EU White list equivalent jurisdictions Higher Risk Areas: Offshore Finance Centre Non - Compliance with FATF 40 + 9 Recommendations Medium Risk Areas: Corruption Index (Transparency International & W.G.I.) Failed States Index (Political Issues)(Average Score) Major Investment Areas: Agriculture - products: sugarcane, tea, corn, potatoes, bananas, pulses; cattle, goats; fish Industries: food processing (largely sugar milling), textiles, clothing, mining, chemicals, metal products, transport equipment, nonelectrical machinery, tourism Exports - commodities: clothing and textiles, sugar, cut flowers, molasses, fish Exports - partners: UK 18.7%, France 16.4%, US 10.4%, South Africa 9.7%, Spain 7.6%, Italy 7.1%, Madagascar 6.7% (2012) Imports - commodities: manufactured goods, capital equipment, foodstuffs, petroleum products, chemicals Imports - partners: India 23.7%, China 15.3%, France 8.9%, South Africa 6.3% (2012) Investment Restrictions: 1 Of the 33 economic sectors looked at in the World Bank report, 32 are fully open to foreign investment in Mauritius. The only exception is television broadcasting, where foreign capital participation in a company must be less than 20%. However, the World Bank report draws attention to the difficulties of investing in certain sectors in Mauritius such as electricity generation and distribution as well as port and airport management, due to -

Five Years of Steering a Central Bank in a Small, Open Island State and Keeping the Economy on an Even Keel

Rundheersing Bheenick: “Steaming on … in uncharted waters in storm-tossed seas” – five years of steering a central bank in a small, open island state and keeping the economy on an even keel Letter by Mr Rundheersing Bheenick, Governor of the Bank of Mauritius, to stakeholders, Bank of Mauritius, Port Louis, 4 February 2013. * * * On 28 December 2007, from my vantage point as newly-installed Governor, I issued my first Letter to Stakeholders to plug what I felt was a gap in our communication. I saw it as a vehicle to review developments in the economic and financial landscape and to give interested stakeholders a flavour of the Bank’s actions during the past year. It was the year of the Bank’s 40th Anniversary celebrations. Less auspiciously, it was also the year when the first tremors of an impending global financial crisis began to be felt in specialized corners of the financial market dealing with esoteric sub-prime mortgages originating in the US. 2. Five years on, the Letter to Stakeholders is well-embedded in the calendar of publications of the Bank, with its release much-awaited, not least by the local financial press. Five additional years in the life of the institution, five years at its helm as Governor, and five years of unending crisis, to boot ― surely all this requires us to pause awhile, look back over those tumultuous, challenging yet ultimately rewarding, years and take stock of the progress achieved. But, first, a brief assessment of 2012 and the perspective for 2013 may provide some context. 3. -

BTI 2020 Country Report Mauritius

BTI 2020 Country Report Mauritius This report is part of the Bertelsmann Stiftung’s Transformation Index (BTI) 2020. It covers the period from February 1, 2017 to January 31, 2019. The BTI assesses the transformation toward democracy and a market economy as well as the quality of governance in 137 countries. More on the BTI at https://www.bti-project.org. Please cite as follows: Bertelsmann Stiftung, BTI 2020 Country Report — Mauritius. Gütersloh: Bertelsmann Stiftung, 2020. This work is licensed under a Creative Commons Attribution 4.0 International License. Contact Bertelsmann Stiftung Carl-Bertelsmann-Strasse 256 33111 Gütersloh Germany Sabine Donner Phone +49 5241 81 81501 [email protected] Hauke Hartmann Phone +49 5241 81 81389 [email protected] Robert Schwarz Phone +49 5241 81 81402 [email protected] Sabine Steinkamp Phone +49 5241 81 81507 [email protected] BTI 2020 | Mauritius 3 Key Indicators Population M 1.3 HDI 0.796 GDP p.c., PPP $ 23709 Pop. growth1 % p.a. 0.1 HDI rank of 189 66 Gini Index 38.5 Life expectancy years 74.5 UN Education Index 0.730 Poverty3 % 3.0 Urban population % 40.8 Gender inequality2 0.369 Aid per capita $ 9.2 Sources (as of December 2019): The World Bank, World Development Indicators 2019 | UNDP, Human Development Report 2019. Footnotes: (1) Average annual growth rate. (2) Gender Inequality Index (GII). (3) Percentage of population living on less than $3.20 a day at 2011 international prices. Executive Summary Mauritius is not a transformation country in the classic sense.