Garden Reach Shipbuilders & Engineers Ltd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A (Technical Offer)

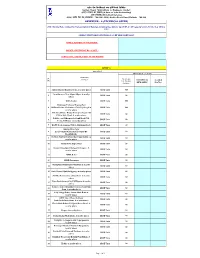

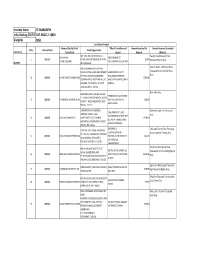

गार्डने रीच शिपबि쥍र्ड셍स ए赍र्ड इंजिननय셍स शऱशिटेर्ड Garden Reach Shipbuilders & Engineers Limited (भारत 셍रकार का उपक्रि) (A Govt. of India Undertaking) (रक्षा िंत्राऱय) (Ministry of Defence) 43/46, गार्डने रीच रोर्ड, कोऱकाता - 700 024 / 43/46, Garden Reach Road, Kolkata – 700 024 ANNEXURE - A (TECHNICAL OFFER) JOB : Biennial Rate Contract for Transportation of Materials including Gas Cylinder by 2.5 MT & 1 MT capacity vehicle for the Year 2018 & 2019 STORE/OT/PB/TRANSPORTATION/2.5 & 1 MT VEHICLE/ET-02065 NAME & ADDRESS OF THE BIDDER * BIDDER S REFERENCE NO. & DATE * CONTACT NO., FAX NO, E-MAIL OF THE BIDDER* GROUP A Appendix-I 1MT Vehicle ( A CAT) Destination Sl. (to & fro) No of Trips TECHNICAL Accepted No. For Two year (tentative) REMARKS* (Yes/No)* 1 Amtala/Bhasha/Bagirhat/Joka & nearby places GRSE Units 160 Taratala more/New Alipur/Alipur & nearby 2 GRSE Units 20 places 3 BOC (Linde) GRSE Units 100 Khidirpur/Panbazar/Hasting/Fort 4 William/Defence Ordanance Club/Taj Bengal & GRSE Units 100 nearby places Hide Road/Brace Bridge/Transport Depot/ All 5 GRSE Units 60 CFS in Hide Road & nearby places Poddar court/Dharmotala/Stand Road/C.R. 6 GRSE Units 50 AvenueDalhousie & nearby places 7 KOPT Dock premises NSD & Khidirpur Dock GRSE Units 40 Dunlop More/Agar 8 para/Sodepur/Kamarhati/Cossipur/BT GRSE Units 10 Road/Kharda Howrah Station/Shalimar/Das Nagar/Salkia & 9 GRSE Units 20 nearby places 10 Andul/Kona Expressway GRSE Units 20 Domjur/Jangalpur/Dhulagarh/Alampur & 11 GRSE Units 20 nearby places 12 GRSE Belur GRSE Units 20 13 GRSE Baranagar -

Name and Addresses of Routine Immunization Centers in KMC Area

Name and Addresses of Routine Immunization Centers in KMC Area Conducted on every Wednesday from 9 am to 1 pm Borough-1 Borough Organization Srl No Ward No Centre Name Zone / Project No Name 1 1 1 Shyama Club, 22/H/3, Hagen Chatterjee Road, KMC CUDP 2 1 1 WHU-1, 1B, G. C. Road , Kol-2 KMC CUDP Paschim Banga Samaj Seva Samiti ,35/2, B.T. Paschim Banga 3 1 1 NGO Road, Kol-2 Samaj Seba Samiti North Subarban Hospital,82, Cossipur Road, Kol- 4 1 1 DFWB Govt. of W.B. 2 5 2 1 6 PALLY CLUB, 15/B , K.C. Sett Lane, Kol-30 KMUHO Zone-II WHU - 2, 126, K. C. GHOSH ROAD, 6 2 1 KMC CUDP KOL - 50 7 3 1 Friend Circle, 21No. Bustee, Kol - 37 KMC CUDP Belgachia Basti Sudha Committee Club,1/2, J.K. 8 3 1 KMUHO Zone-II Ghosh Road,Lal Maidan, Kol-37 Netaji Sporting Club, 15/H/2/1, Dum Dum Road, 9 4 1 KMUHO Zone-II Kol-30,(Near Mother Diary). 10 4 1 Camelia Building, 26/59, Dum Dum Road, Kol-2, ICDS Belgachia Friends Association Cosmos Club, 89/1 Belgachia 11 5 1 ICDS Belgachia Road.Kol-37 Indira Matri O Shishu Kalyan Hospital, 12 5 1 Govt.Hospital Govt. of W.B. 35/B, Raja Manindra Road, Kol - 37 W.H.U. - 6, 10, B.T. Road, Kol-2 , Paikpara (at 13 6 1 KMC CUDP Borough Cold Chain Point) Gun & Cell Factory Hospital, Kossipur, Kol-2 Gun & Shell 14 6 1 CGO (Ordanance Factory Hospital) Ph # 25572350 Factory Hospital Gangadhar Sporting Club, P-37, Stand Bank 15 6 1 ICDS Bagbazar Road, Kol - 2 Radha Madhab Sporting Club, 8/1, Radha 16 8 1 Madhab Goswami Lane, Kol-3.Near Central KMUHO Zone-II Medical Store, Bagbazar Kumartully Seva Samity, 519A, Rabindra Sarani, Kumartully Seva 17 8 1 NGO kol-3 Samity Nagarik Sammelani,3/D/1, Raja Naba Krishna 18 9 1 KMUHO Zone-II Street, kol-5 Borough-2 1 11 2 160,Arobindu Sarani ,Kol-6 KMC CUDP 2 15 2 Ward Health Unit - 15. -

West Bengal Minorities' Development and Finance Corporation

West Bengal Minorities' Development & Finance Corporation • (A Statutory Corporation of Govt. of West Bengal) Memo No: 194 -MDC/VT-13-14 Date: 12th January,2021 ~: WBMDFC-.$1~ '5ll\JMt~. fly,: rn:f¥« C~IO:BI WEIT !-til~N,\S / <Pl©C.§iM~ - National Institute of Fashion Teechnology (NIFT). Kolkata C1J ~ ~~ WBMDFC ~ "'-!rnf@'-!> NIFT Kolkata-el ~ ~ QaR~ C~~ ~ "'-!IC<PFI ;qsrnc~··( ~ ~ri ')~M '9!11Jll~1, ~o~') - ~~M '9!11Jll'ffi, ~o~') ~ )O.oo C~ ~.oo ~'i:f ~~ ~1'1i:lR:,@-~ ~ ~'3m'i:f ~ "'-1-!Ci:ll~ ~ ~ I ~1'1i::1R,© .El'?l'~<J' .El<f~ ~ i6ll--ll~ ~ WBMDFC website (www.wbmdfc.org) 01~1 ~~~~1.,Ji:lR:,@~~~C<PR~TA&DA~~~~ I ~1.S1i:1f;©::4J'i:f~Rtii?l~~~'3 ~<Pf~~~~) "'-!HC\!>~g 1. ~ (17'/')o/')~) ~ s:i1fGf¥c;qs'G ~9RT'i:l" ~"'-l"i~l~ s:i1fGr¥c¥G "'-11..:ic<:1..:i) 2. ISrJJ s:i1fGf¥c;qs'G 3. ~ ~ f% ffi / '5JTl:ffif ffi 4. ~ <Pf9f 9ff51t9ffi, ~ ~ 5. "'-!r.!i.91~"'1-~ ~~~-~'i:f~GITT% ~ ~ ;::;,r-=ror--·,o I. ''II / 111. "I I / I -, '\ ····· o WEST BENGAL MINORITIES DEVELOPMENT & ~-~-~ - (7003597117) FINANCE CORPORATION (WBMDFC) "AMBER"DD- (NIFT) 27 /e, SECTOR 1, SALT LAKE CITY, KOLKATA 700 '1fibll<:15'/ '51"~~~'3 ~R~ 064 (WBMDFC) -18001202130 West Bengal Minorities' Development & Finance Corporation • (A Statutory Corporation of Govt. of West Bengal) 1 Memo no: 194-MDC/VT-13-14 Date: 12 h January, 2021 Notice Subject: Counselling/ Interview for Skill Training at National Institute of Fashion Technology (NIFT). Kolkata sponsored by WBMDFC Candidates applied for Skill Training course at National Institute of Fashion Technology (NIFT), Kolkata , sponsored by WBMDFC are hereby requested to attend Interview for selection from 19th January, 2021 to 22nd January, 2021 from 10.00 am to 2.p.m. -

Hungry Bengal: War, Famine, Riots, and the End of Empire 1939-1946

Hungry Bengal: War, Famine, Riots, and the End of Empire 1939-1946 By Janam Mukherjee A dissertation submitted in partial fulfillment of the requirement for the degree of Doctor of Philosophy (Anthropology and History) In the University of Michigan 2011 Doctoral Committee: Professor Barbara D. Metcalf, Chair Emeritus Professor David W. Cohen Associate Professor Stuart Kirsch Associate Professor Christi Merrill 1 "Unknown to me the wounds of the famine of 1943, the barbarities of war, the horror of the communal riots of 1946 were impinging on my style and engraving themselves on it, till there came a time when whatever I did, whether it was chiseling a piece of wood, or burning metal with acid to create a gaping hole, or cutting and tearing with no premeditated design, it would throw up innumerable wounds, bodying forth a single theme - the figures of the deprived, the destitute and the abandoned converging on us from all directions. The first chalk marks of famine that had passed from the fingers to engrave themselves on the heart persist indelibly." 2 Somnath Hore 1 Somnath Hore. "The Holocaust." Sculpture. Indian Writing, October 3, 2006. Web (http://indianwriting.blogsome.com/2006/10/03/somnath-hore/) accessed 04/19/2011. 2 Quoted in N. Sarkar, p. 32 © Janam S. Mukherjee 2011 To my father ii Acknowledgements I would like to thank first and foremost my father, Dr. Kalinath Mukherjee, without whom this work would not have been written. This project began, in fact, as a collaborative effort, which is how it also comes to conclusion. His always gentle, thoughtful and brilliant spirit has been guiding this work since his death in May of 2002 - and this is still our work. -

Garden Reach Shipbuilders & Engineers

Garden Reach Shipbuilders & Engineers Ltd (A Government of India Undertaking) (Ministry of Defence) 1.1 Particulars of organization, functions and duties [Section 4(1) (b) (i)] Name and address of the organization, genesis, inception, formation of the department i) Name & Address of the Organization : Garden Reach Shipbuilders & Engineers Ltd 43/46, Garden Reach Road, Kolkata – 700 024. ii) Head of the Organization: Rear Admiral V.K. Saxena, IN (Retd.) iii) Origin/ genesis/inception of the Company: The company came into being in 1884 as a small factory on the Eastern Bank of the river Hooghly. In 1926, the amalgamation of workshops of River Steam Navigation Company (RSNC) and British India Steam Navigation Company (BISN) was finally effected and managed as a partnership concern. Garden Reach Workshop was incorporated as a Company under the Indian Companies Act of 1913 with effect from 26 February 1934. The company was taken over by the Government of India on 01 April 1960. iv) The Administrative Ministry for GRSE: Ministry of Defence, Department of Defence Production, Government of India, New Delhi. GRSE has Eight production units and Three Regional Offices- at Delhi, Mumbai and Visakhapatnam. The contact details are given below: UNIT ADDRESS CONTACT NUMBERS GRSE-MAIN UNIT 43/46, GARDEN REACH EPABX 2469-8100 TO 8114 ROAD, KOLKATA-700024 FAX 033-2469 8150 (WEST BENGAL) GRSE-FOJ UNIT P-70, KARL MARX SARANI, EPABX 2439 1081/ 1091/ KOLKATA-700043 1092/ 2262/ (WEST BENGAL) 2265/3245/3246 FAX 033-2439 2416 GRSE-CENTRAL 61, GARDEN REACH EPABX -

Ward No: 080 ULB Name :KOLKATA MC ULB CODE: 79

BPL LIST-KOLKATA MUNICIPAL CORPORATION Ward No: 080 ULB Name :KOLKATA MC ULB CODE: 79 Member Sl Address Name of Family Head Son/Daughter/Wife of BPL ID Year No Male Female Total 1 SICK LINE NA G. C. D. SICK LINE A. BIBI MUSTAFA KHAN 2 1 3 1 2 77 GARDEN REACH ROAD KOL-43 A. CHINNA RAO LATE A. KALIDAS 2 2 4 2 3 HOOGLY JUTE MIL 77 GARDEN REACH RD. KOL 43 A. DADRINARAYAN RAO LT. KALIDAS RAO 3 4 7 3 4 NA 116/13/14 T. ROAD A. GOCHAIT NA 3 1 4 4 5 NA 120/21/22 T. ROAD A. K. PANDEY NA 2 2 4 6 6 BHUT GHAT NA 2. N. M. ROAD ASHIA KHATOON LATE MD ALAUDDIN 2 1 3 7 7 4 NO. INDIRA PALLY (BR NA HIDE ROAD A. MOLLA CHAMED MOLLA 4 1 5 8 8 NA 94/1/2 T. ROAD A. N. SARKAR A. N. SARKAR 2 2 4 9 9 HW NO86 TARATALLA ROAD, KOLKATA-88 AAJAR ALI JOYNAL MUNSHI 3 2 5 11 10 HUT NO-126 TARATALLA ROAD, KOLKATA-88 AANSAR LASKAR MUSSA LASKAR 3 1 4 13 11 C.P.T. QTR. NIMAK MOHAL RD. NIMAK MOHAL ROAD, KOL 43 AARTI HALDER LATE KALIPADA HALDER 4 2 6 14 12 1NO PALLY HUT NO 165 TARATALLA ROAD, KOLKATA-88 AASMOTH LASKAR CHANNAT LASKAR 3 4 7 15 13 C. P. T. COLONY JHUPRI TARATALA 1 NO. GATE ABBAD HOSSEIN NA 2 5 7 17 14 C. P. T. COLONY NA TARATALA 1 NO. -

We Have Two Containment Zones As on 04.05.20 for Darjeeling District: 1. Ward No 47, Siliguri Municipal Corporation. 2.Shantinik

We have two Containment Zones as on 04.05.20 for Darjeeling District: 1. Ward No 47, Siliguri Municipal Corporation. 2.Shantiniketan Housing Complex, Shusrat Nagar, Matigara Block. List of Containment Zones in Hooghly District as on 08.05.2020 * Containment Zone of Serampore Sub-Division Containment zone 1 Ramsita Lane, (labour quarters of line no 9 of Indian Jutemill) of ward no 12 of Serampore municipality under Serampore P.S. Containment zone 2 Burning ghat of Ballavpur Smasankali, Thakurbati Street of ward no 17 of Serampore Municipality under Serampore P.S. Containment zone 3 Bhatrisangha , Neheru nagar colony of ward no 18 of Serampore municipality under Serampore P.S. Containment zone 4 Naya bustee of ward no 29 of Serampore municipality under Serampore P.S. Containment zone 5 Bari masjid Lane of ward no 1of Rishra municipality under Serampore P.S. Containment zone 6 Gokhana housing complex beside R.K Road of ward no 2 of Rishra municipality under Serampore P.S. Containment zone 7 Goalapara Road (G.T. Road to 4no Rail gate) of ward no 2 of Rishra municipality Serampore P.S. Containment zone 8 Jodhan Singh Road of ward no 3 of Rishra municipality under Serampore P.S Containment zone 9 Bhutnath Pal lane (15 house holds) of Bangur park ward no 11 of Rishra municipality (Rishra P.S.) Containment zone 10 Simla Satghara Road, Pravasnagar of ward no 18 of Rishra municipality, (SS Road extension to Entry point of Pravasnagar of Serampore 29 no ward) under Serampore P.S. Containment zone 11 Himnagar of Ward no 11 of Dankuni municipality under Dankuni P.S. -

Indian Water Works Association 47Th IWWA Annual Conven On, Kolkata

ENTI NV ON O 2 0 C 1 L 5 A , K U Indian Water Works O N L N K A A h T t A 7 Association 4 47th Annual Convention Kolkata 30th, 31st Jan & 1st Feb, 2015 Theme: ‘Sustainable Technology Soluons for Water Management’ Venue: Science City J.B.S Haldane Avenue Kolkata ‐ 700046, (West Bengal) Convention Hosted By IWWA Kolkata Centre INDIAN WATER WORKS ASSOCIATION 47th IWWA ANNUAL CONVENTION, KOLKATA Date : 30th, 31st January & 1st February, 2015 Venue : Science City, J.B.S Haldane Avenue, Kolkata ‐ 700046, West Bengal APPEAL Dear sir, The Indian Water Works Associaon (IWWA) is a voluntary body of professionals concerned and connected with water supply for rural, urban, industrial, agricultural uses and disposal of wastewater. IWWA focuses basically on the enre 'Water Cycle' encompassing the environmental, social, instuonal and financial issues in the area of water supply, wastewater treatment & disposal. IWWA was founded in the year 1968 with headquarters at Mumbai having 32 centers across the country with more than 9000 members from all professions around the world. The Kolkata Centre of IWWA in associaon with Public Health Engineering Department, Govt. of West Bengal along with others is organizing The 47th IWWA Convenon in Kolkata from 30th January to 1st February, 2015 at Science City, J.B.S Haldane Avenue, Kolkata ‐ 700046, West Bengal under the Theme 'Sustainable Technology Soluons for Water Management'. The professionals from all over the country and abroad will parcipate and present their technical papers in the three days convenon. The organizing commiee would like to showcase the Kolkata convenon in a very meaningful manner and make it a grand success and a memorable event to be cherished for a long me. -

Kolkata Merit List

NATIONAL MEANS‐CUM ‐MERIT SCHOLARSHIP EXAMINATION,2019 PAGE NO.1/16 GOVT. OF WEST BENGAL DIRECTORATE OF SCHOOL EDUCATION SCHOOL DISTRICT AND NAME WISE MERIT LIST OF SELECTED CANDIDATES CLASS‐VIII ADDRESS NAME OF ADDRESS OF QUOTA UDISE NAME OF OF SCHOOL DISABILITY MAT SAT SLNO ROLL NO. THE THE GENDER CASTE TOTAL DISTRICT CODE THE SCHOOL THE DISTRICT STATUS MARKS MARKS CANDIDATE CANDIDATE SCHOOL 21/1HN ROAD,ULTADANGA,MANICKTALA WEST 1 123194304099 ABHIJIT RAJBANSHI KOLKATA 19170101634 SARADA PRASAD INST KOLKATA M SC None 29 33 62 KOLKATA 700067 BENGAL AJ‐65/9, KHUDIRAM PALLY , TALPUKUR SURSUNA HIGH SCHOOL WEST 2 123194304056 ABHIJIT SAHA KOLKATA 19170112916 KOLKATA M GENERAL None 44 55 99 ROAD,SARSUNA,SARSUNA KOLKATA 700061 (H.S.) BENGAL ABID HUSSAIN 227 BANSDRONI,BANSDRONI,BANSDRONI WEST 3 123194304205 KOLKATA 19170110323 NAKTALA HIGH SCHOOL KOLKATA M GENERAL None 62 69 131 PIYADA SOUTH TWENTY FOUR PARGANAS 700070 BENGAL ANANDA PALLY PURBA PUTIARY,PURBA GANGAPURI SIKSHA WEST 4 123194304075 ADARSHA HALDAR KOLKATA 19170111712 KOLKATA M GENERAL None 47 47 94 PUTIARY,REGENT PARK KOLKATA 700070 SADAN BENGAL G‐26 ADRIJA BARISHA VIVEKANANDA WEST 5 123194304126 ANANDANAGAR,THAKURPUKUR,THAKURPUK KOLKATA 19170112705 KOLKATA F GENERAL None 60 66 126 CHAKRABORTY GIRLS H.S. BENGAL UR KOLKATA 700063 11/39 NEW CIT ALL INDIA WOMEN C.B. WEST 6 123194304068 ADRIJA JASH BUILDING,BELEGHATA,BELEGHATA KOLKATA KOLKATA 19170103612 KOLKATA F GENERAL None 42 43 85 BIDYAPITH BENGAL 700010 NARENDRAPUR,SONARPUR,SONARPUR BINODINI GIRLS HIGH WEST 7 123194304154 AISHI JANA KOLKATA 19170109522 KOLKATA F GENERAL None 58 45 103 SOUTH TWENTY FOUR PARGANAS 700150 SCHOOL BENGAL 262, DUTTABAD ROAD, SECTOR‐II SALT LAKE CITY,BIDHANNAGAR CC BLOCK,BISHANNAGAR WEST 8 123194304040 AKASH BISWAS KOLKATA 19170101634 SARADA PRASAD INST KOLKATA M SC None 30 48 78 SOUTH NORTH TWENTY FOUR PARGANAS BENGAL 700064 16/5/H/2/2 BIPLABI BARIN GHOSH MURARI PUKUR GOVT. -

16‐06‐20 13 5 Seals Garden Lane Cossipore 700002 1 1

Affected Zone DAYS SINCE Date of reporting of REPORTING Sl No. Address Ward Borough Local area the case 13 5 SEALS GARDEN LANE The premises itself 1 1 1 Cossipore 16‐06‐20 COSSIPORE 700002 14 The affected flat/the 59 Kalicharan Ghosh Rd standalone house 2 kolkata ‐ 700050 West 2 1 Sinthi Bengal India 16‐06‐20 14 The premises itself 21/123 RAJA MANINDRA 3 31 Paikpara ROAD BELGACHIA 700037 16‐06‐20 14 14A BIRPARA LANE The premises itself 4 kolkata ‐ 700030 West 31 Belgachia 16‐06 ‐20 BBlIdiengal India 14 The flat itself A4 6 R D B RD Kolkata ‐ 5 41 Paikpara 700002 West Bengal India 16‐06‐20 14 110/1A COSSIPORE Road The premises itself 6 Kolkata ‐ 700002 West 6 1 Chitpur 16‐06‐20 Bengal India 14 Adjacent common passage of affected hut 14 3 GALIFF STREET 7 7 1 Bagbazar including toilet and BAGHBAZAR 700003 water source of the 16‐06‐20 slum 14 Adjacent common passage of affected hut 14 3 GALIFF STREET 8 7 1 Bagbazar including toilet and BAGHBAZAR 700003 water source of the 16‐06‐20 slum 14 Affected Zone DAYS SINCE Date of reporting of REPORTING Sl No. Address Ward Borough Local area the case 1 RAMKRISHNA LANE The premises itself 9 Kolkata ‐ 700003 West 7 1 Girish Mancha 16‐06‐20 Bengal India 14 The premises itself 4/2/1B KRISHNA RAM BOSE 10 STREET SHYAMPUKUR 10 2 Shyampukur KOLKATA 700004 16‐06‐20 14 T/1D Guru Charan Lane The premises itself 11 Kolkata ‐ 700004 West 10 2 Hatibagan 16‐06‐20 Bengal India 14 Adjacent common 47 1 SHYAMBAZAR STREET passage of affected hut 12 Kolk at a ‐ 700004 W est 10 2 Shyampu kur iilditiltdncluding toilet and -

Consulting Projects Details-2D

Institute Name IIT KHARAGPUR India Ranking 2017 IDIR17-ENGG-2-18630 Discipline ENGG Consultancy Projects Name of faculty (Chief Title of Consultancy of Amount received (in Amount received (in words) S.No. Financial Year Client Organization PARAMETER Consultant) project Rupees) [Rupees] SOFTLORE SOLUTION-SCIENCE & Twenty Two Thousand Four RAJLAKSHMI DEVELOPMENT OF 1 2015-16 TECHNOLOGY ENTREPRENEURS PARK, 22456 GUHA(T0109,RM) PSYCHOMETRIC ALGORITHMS Hundred Fifty Six Only 2D.FPPP IIT KHARAGPUR Twenty Seven Lakh Sixty Three WATER & SANITATION SUPPORT ORGANISATION (WSSO)-DEPARTMENT RIVER WATER QUALITY Thousand Nine Hundred Thirty OF PUBLIC HEALTH ENGINEERING, EVALUATION FOR RIVER Only 2 2015-16 JAYANTA BHATTACHARYYA(87019,MI), ABHIJIT MUKHERJEE(10018,GG) 2763930 GOVERNMENT OF WEST BENGAL, N.S. BASED PIPED WATER SUPPLY BUILDING, 7TH FLOOR, 1, K. S. ROY SCHEME ROAD, KOLKATA - 700 001 One Lakh Only SRIKRISHNA COLD STORAGE-VILL & P. PROBLEMS OF CULTIVATION O. - NONAKURI BAZAR (KAKTIA BAZAR), 3 2015-16 PROSHANTA GUHA(04016,AG) AND PRESERVATION OF 100000 DISTRICT - PURBA MEDINIPUR, WEST BETEL LEAVES BENGAL - 721172 SUPERINTENDING ENGINEER,- Seventeen Lakh Ten Thousand EVALUATION OF FLOOD WESTERN CIRCLE-II, I&W MANAGEMENT SCHEME FOR Only 4 2015-16 RAJIB MAITY(08039,CE) DIRECTORATE, DIST, PASCHIM 1710000 KELIAGHAI - KAPALESWARI - MEDINIPUR, GOVERNMENT OF WEST BAGHAI RIVER BASIN BENGAL, PIN-721101 WIDENING & Two Lakh Twenty Four Thousand ORIENTAL STRUCTURAL ENGINEERS STRENGTHENING OF PVT. LTD.-21, COMMERCIAL COMPLEX, Seven Hundred Twenty Only 5 2015-16 -

Grse an Iso 9001:2015 Company

GRSE AN ISO 9001:2015 COMPANY “Uttar Pradesh Defence Expo-2018” (UPDEX-2018) Chandra Shekhar Azad University of Agriculture & Technology Kanpur, U.P. FLOW • Company Profile • Product Profile • Integrated Shipbuilding Facility • Business Opportunities • Shipbuilding Projects • Vendor Development • Registration Procedure & Contact Details GRSE AT A GLANCE Founded in 1884. Taken over by Govt of India in 1960 Pioneer Shipbuilder –Built First Indigenous Warship, INS AJAY in 1961 1st Warship Export of Country- CGS Barracuda to Mauritius in 2014 Profit Making & Dividend paying PSU for last 24 years Mini Ratna Category 1 Company. 2800 Employees Best Performing Defense Shipyard for Four Consecutive Years (from 2010-11 to 2013-14) COMPANY PROFILE 4 COMPANY PROFILE SHIPBUILDING DIVISION ENGINEERING DIVISION ENGINE DIVISION - MAIN WORKS, KOLKATA - PORTABLE BRIDGE UNIT, KOLKATA - DIESEL ENGINE PLANT (RANCHI) - FITTING OUT UNIT, KOLKATA - DECK MACHINERY UNIT, KOLKATA - RAJA BAGAN DOCKYARD, KOLKATA 5 # THE SEVENTH UNIT IN KOLKATA IS A TECHNICAL TRAINING CENTRE IN PURSUIT OF EXCELLENCE & QUALITY IN SHIPBUILDING TECHNICAL TRAINING CENTRE TOOK OVER “DEVELOPMENT WORKSHOP” OF INDIAN STATISTICAL INSTITUTE (ISI) CONVERTED TO TECHNICAL TRAINING CENTER WEF FROM 1995 CERTIFIED AS ISO 9001:1994 & ISO 9001:2000 CONDUCTS TRAINING FOR FOLLOWING TRADES : . TRADE APPRENTICES . ELECTRICIAN, FITTER, MACHINIST, PIPE FITTER & WELDER . GRADUATE/ DIPLOMA ENGINEER APPRENTICESHIP . TRAINEE MARINE ENGINEER 6 IN PURSUIT OF EXCELLENCE & QUALITY IN SHIPBUILDING SHIPBUILDING