Maritime Industries in Selangor – Manufacturing and Services 2012 Final

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

13. Regional Maritime Trends

13. REGIONAL MARITIME TRENDS 13.1 Singapore 13.1.1 Port Management Singapore Harbor Board had been responsible for the management of Port of Singapore until 1964. Port of Singapore Authority was established in April 1964 and it assumed complete responsibility for port construction and operation. In 1996, the former PSA was split into two, PSA corporation limited and MPA (Maritime and Port Authority of Singapore). The new PSA was established as a private entity responsible for port operation, although the government still holds its entire equity. On the other hand, MPA is in charge of the regulatory functions relative to the port including port planning, harbor master, ship registration, and port industry issues. Since May 1997, PSA comprises two main divisions, administrative division and strategic business division. The strategic business division is made up of three main groups, container terminal operation, storage and distribution, and overseas business. PSA established a subsidiary, PSA Marine, which takes care of tug and pilot services. Consequently, PSA now focuses on container terminal operation. PSA was privatized mainly because it would help streamline the government sector and facilitate PSA’s overseas business. Currently, PSA operates nine ports overseas including Dalien (China) and Aden (Yemen). PSA’s investment activity is now focused on overseas projects rather than domestic projects. PSA predicts that its overseas operation will become profitable in 2007. MPA and PSA are completely independent with no exchange of employees. Taking port development as an example, MPA prepares a development plan and PSA constructs and operates port facilities. The government continues to own the land and leases it out to the operator for a period of 20-30 years. -

ESCAP PPP Case Study #5

Public-Private Partnerships Case Study #5 Regulation in PPP projects: the case of Port Klang by Mathieu Verougstraete, Ferdinand Marterer and Clovis Eng (March 2015) The Malaysian government has improved the capacity and efficiency of its port infrastructure by involving the private sector. This case study reviews the develop- ment of the largest port in the country, Port Klang, and considers the role of the public partner when ports are privately operated. PRIVATE PORT OPERATORS THE CASE OF PORT KLANG To improve port efficiency, many governments Malaysia was one of the first countries to around the globe have introduced private introduce private port operators by the end of participation in port operations. Different the 1980s. Improving port efficiency was a models have been tested. The most common rising priority in order to reduce dependency one is the Landlord Port Model in which the on Singapore for external trade. Involving private partner leases a port terminal and private stevedores was seen as the best way is responsible for both the operation and to compete in the Strait of Malacca – one of related investments (e.g. wharf expansion, the world’s most crucial trade waterways with cranes and office buildings). However, the an annual throughput of 70,000 ships, for public authority remains in charge of common transhipment operations.3 facilities such as breakwaters, entrance The introduction of private operators began channels, utilities and road and rail access to ESCAP supports govern- 1 in 1986 with Port Klang, which is located the port. ments in Asia-Pacific in on the Malaysian west coast, about 40 km implementing measures While private operators could boost from Kuala Lumpur, the capital city. -

Unmanned Aerial Vehicle (UAV)

565 Int. J Sup. Chain. Mgt Vol. 8, No. 3, June 2019 Unmanned Aerial Vehicle (UAV) and ArcGIS for Shipping Container Counting Afiq Abdullah1, Jasmee Jaafar2, Khairul Nizam Tahar3, Wan Mazlina Wan Mohamed4 1,4Malaysian Institute of Transport (MITRANS), UniversitiTeknologi MARA, 40450 Shah Alam, Selangor, Malaysia. 2,3Centre of Studies for Surveying Science & Geomatics, Faculty of Architecture, Planning & Surveying UniversitiTeknologi MARA, 40450 Shah Alam, Selangor, Malaysia. [email protected] [email protected] [email protected] [email protected] Abstract— The current approach in counting shipping 1. Introduction containers at port terminal in Malaysia is done manually. This process will incur cost, time and labour Container terminal or depot is the place where the intensive. Furthermore, this technical issue has led to shipping container is being kept for storage, damage delay in container operation. This has made the inspection and fixing. Currently, the existing operational efficiency factor to be questioned. approach of shipping container counting is done Therefore, promoting an automated approached manually and the process is time consuming as well seems appealing. Previous studies demonstrate the capability of Unmanned Aerial Vehicle (UAV) images labor intensive. Validation process seems for automatic counting of cars and trees. In this study, impossible when the number of containers is large. combinations of aerial images captured using UAV Furthermore, during operation, manual counting and geo-processing software, ArcGIS, are promoted will involve human interventions and this will affect towards automated approach for counting shipping safety issues especially at busy terminals. containers. The overlapping UAV aerial images are It is reported that the efficiency of container post-processed using photogrammetric technique to terminal relates to technical efficiency [1]. -

An Overview and Examination of the Malaysian Service Sector

No. ID-27 OFFICE OF INDUSTRIES WORKING PAPER U.S. INTERNATIONAL TRADE COMMISSION An Overview and Examination of the Malaysian Service Sector Lisa Alejandro Jennifer Baumert Powell Samantha Brady Isaac Wohl November 2010 Office of Industries working papers are the result of the ongoing professional research of USITC Staff and are solely meant to represent the opinions and professional research of individual authors. These papers are not meant to represent in any way the views of the U.S. International Trade Commission or any of its individual Commissioners. Working papers are circulated to promote the active exchange of ideas between USITC Staff and recognized experts outside the USITC, and to promote professional development of Office staff by encouraging outside professional critique of staff research. ADDRESS CORRESPONDENCE TO: OFFICE OF INDUSTRIES U.S. INTERNATIONAL TRADE COMMISSION WASHINGTON, DC 20436 USA An Overview and Examination of the Malaysian Service Sector Lisa Alejandro, Jennifer Baumert Powell, Samantha Brady, and Isaac Wohl1 U.S. International Trade Commission ABSTRACT The service sector is a rapidly growing component of Malaysia’s economy. In 2008, the last year for which data are available, it expanded 7.2 percent to $96.9 billion and employed over half of the country’s workforce. Growth in the Malaysian service sector is largely a product of government policies that promote service industries, including tax benefits and investment, as well as specialization in niche service industries that cater to Islamic consumers. In April 2009, the government eliminated or eased ethnic-Malay equity requirements in 27 service industries in an effort to further increase service industries’ contribution to the Malaysian economy. -

PKA Chief: No Regrets Opening Can of Worms Malaysiakini.Com January 15 2011

PKA chief: No regrets opening can of worms Malaysiakini.com January 15 2011 Port Klang Authority (PKA) chairperson Lee Hwa Beng, whose term ends on Mar 31, has no regrets over his decision to initiate an investigation into the multi-billion Port Klang Free Zone (PKFZ) scandal that has riled up powerful politicians and companies. "Now I have become a black sheep to certain people in my party (MCA). There are also cases where some friends don't want to go out with me anymore. "There were also cases where people didn't want me to sit in their cars because they were scared of collateral damage," said Lee in an interview recently. His role in the scandal has made him a persona non grata within the party and has shut his door to MCA politics, Lee (left) said. However the former Subang Jaya assemblyperson called the task his religious duty. "I take it as a religious calling to serve my god. Then you don't care what people say, you don't care how you suffer. You just carry on with what you think is the right way." Lee's report card Lee was appointed on Apr 1, 2008 as PKA chairperson by then-transport minister and MCA president Ong Tee Keat, who later extended Lee's term twice. It is expected that with Ong's ouster as president by Chua Soi Lek last year, Lee as a staunch Ong supporter will be replaced by Chua's men when his term ends. Under Lee's leadership and Ong's backing, PKA took several bold moves to probe the multi-billion ringgit scandal including commissioning an independent audit report and seeking professional advice from external bodies, followed by civil suits against several individuals and companies to claim the losses. -

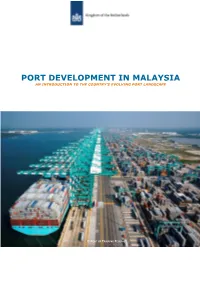

Port Development in Malaysia an Introduction to the Country’S Evolving Port Landscape

PORT DEVELOPMENT IN MALAYSIA AN INTRODUCTION TO THE COUNTRY’S EVOLVING PORT LANDSCAPE © PORT OF TANJUNG PELEPAS CONTENTS MARKET OPPORTUNITIES ............................................................................................ ii MARITIME GIANT MALAYSIA ........................................................................................ 2 GATEWAY TO SOUTHEAST ASIA ..................................................................................... 3 GLOBAL PORT ENVIRONMENT ........................................................................................ 4 PORTS OF MALAYSIA .................................................................................................... 5 MMC CORPORATION BERHAD ......................................................................................... 7 PORT POLICY ............................................................................................................... 7 PORT KLANG ................................................................................................................ 8 WESTPORTS ................................................................................................................ 9 NORTHPORT .............................................................................................................. 10 JOHOR PORT .............................................................................................................. 11 PORT OF TANJUNG PELEPAS ........................................................................................ 12 -

Management of Environmental Issues Related to Capital Dredging Works at Port Klang, Malaysia

MANAGEMENT OF ENVIRONMENTAL ISSUES RELATED TO CAPITAL DREDGING WORKS AT PORT KLANG, MALAYSIA Rajoo Addakann1 ABSTRACT Port Klang is Malaysia’s leading port with two main navigational entrances / exits. The Northern Pulau Angsa Approach is via the dredged North Channel, 153 meters wide with maintained declared depth of 11.3 meters below Chart Datum (m CD). The Southern approach lies adjacent to the North bound lane of the Malacca Straits Traffic Separation. The South Channel has a width of 365 meters with a maintained declared depth of 15.5 m below CD. Capital dredging work is proposed in order to upgrade the North access channel to the same width and a declared depth of 365 meters & 15.5 m below CD respectively as that of the Southern approach. The capital dredging volume involved is approximately 39 million cubic meters. The mainland bordering the port is the most developed region in the country. Mangrove forests cover the undeveloped coastal zones within and at areas bordering the port. Inter tidal mud flats and natural islands off the port provide protection and environmental buffer zones. The gazetted port area and its surroundings also include numerous fishing villages, cage fish farms, cockle breeding farms and artificial reefs to promote natural fish breeding. The port area is a multi user environment with significant natural buffer zones. Hence implementation of this major capital dredging project requiring relocation of very large quantities of dredged materials will cause multi-user conflicts, socio-economic impacts as well as concerns for environmental protection. Adequate studies, investigations and planning have been carried out to identify and address all issues on environmental impacts, environmental monitoring and mitigation measures to be adopted for the successful implementation of the project with minimal impact. -

The First Malaysian Port to Be Awarded Iso 37001:2016

FOR IMMEDIATE RELEASE NORTHPORT - THE FIRST MALAYSIAN PORT TO BE AWARDED ISO 37001:2016 PORT KLANG, 10 February 2021 – Northport (Malaysia) Bhd, (“Northport”), a member of MMC Group set another impressive milestone when it became the first port in Malaysia to attain the ISO 37001:2016 Anti-Bribery Management System (ABMS) certification from SIRIM QAS International Sdn Bhd (SIRIM QAS), the Malaysian certification body for ABMS. “ISO 37001:2016 certification is a testament of Northport’s continued commitment towards the highest level of integrity and ethical culture in our day to day business operations. We strongly believe that this certification will boost the confidence among our customers, business partners and other stakeholders towards Northport,” said Dato’ Azman Shah Mohd Yusof, Chief Executive Officer of Northport. SIRIM QAS’ Senior General Manager, Management Systems Certification Department, Haji Mohd Hamim Imam Mustain officially handed over the ISO certificate to Dato’ Azman during a simple ceremony at Northport on Wednesday, 10 February 2021. ISO 37001:2016 is an international standard that sets out requirements and provides guidance for establishing, implementing, maintaining, reviewing and improving anti- bribery management systems and processes, and reducing the risk of bribery in organisations. Since the takeover by MMC, Northport has embarked on a journey of transformation, founded upon a new set of core values namely Integrity, Customer Focus, Innovation, Teamwork and Excellence (InCITE). In the initial stage, efforts to promote the culture of integrity were initiated through Page 1 of 4 engagement sessions with employees to educate and instill the awareness on integrity related best practices, including the Whistleblowing Policy which gives the rights and responsibility to the employees and parties dealing with Northport to disclose any act of improper conducts within the organisation. -

Port Operations in Port Klang During the Implementation Period of the Movement Control Order (Mco) from 13 to 26 January 2021

MALAYSIAN PLASTICS MANUFACTURERS ASSOCIATION CIRCULAR NO. 14/2021 DATE: 15 JANUARY 2021 PORT OPERATIONS IN PORT KLANG DURING THE IMPLEMENTATION PERIOD OF THE MOVEMENT CONTROL ORDER (MCO) FROM 13 TO 26 JANUARY 2021 Reference is made to the CIRCULAR NO. 3/2021 FROM THE PORT KLANG AUTHORITIES dated 13 January 2021. Highlights of the Circular and Memorandum are as follows: 1. The port is categorised as essential services, the Northport & Westport operators and Port Klang Free Zone operating in Port Klang will operate as usual (24 hours per day) and will provide all service requirements for the port and logistics to meet the needs of the country during this critical period. 2. Since the port operations will run as usual, all activities unloading and movement of goods for cargo ships are allowed to run as usual and is not limited to essential items. 3. To ensure that the operation of the ports operated by Northport and Westport run smoothly and effectively, all containers and cargo unloaded from the ship must be removed from the port area immediately. Importers and exporters who are under the essential sectors and have obtained approval from the Ministry of International Trade and Industry (MITI) can receive containers and cargo from the port (refer to LAMPIRAN 1). 4. Commercial vehicle owners do not required to obtain a letter of approval from the Ministry of Transport (MOT), they just need to obtain a confirmation letter from their respective employers. There are no restrictions on commercial vehicles operating during this period of MCO. For this purpose, special routes will be provided at each Roadblocks (SJR) and commercial vehicle drivers are only required to submit an employer confirmation letter if requested by the authority. -

Malaysia's Invisible Ivory Channel

TRAFFIC MALAYSIA’S INVISIBLE IVORY REPORT CHANNEL An assessment of ivory seizures involving Malaysia from January 2003 - May 2014 SEPTEMBER 2016 Kanitha Krishnasamy TRAFFIC Report: Malaysia’s invisible ivory channel: An assessment of ivory seizures involving Malaysia from January 2003- May 2014 1 TRAFFIC REPORT TRAFFIC, the wild life trade monitoring net work, is the leading non-governmental organization working globally on trade in wild animals and plants in the context of both biodiversity conservation and sustainable development. TRAFFIC is a strategic alliance of WWF and IUCN. Reprod uction of material appearing in this report requires written permission from the publisher. The designations of geographical entities in this publication, and the presentation of the material, do not imply the expression of any opinion whatsoever on the part of TRAFFIC or its supporting organizations con cern ing the legal status of any country, territory, or area, or of its authorities, or concerning the delimitation of its frontiers or boundaries. The views of the authors expressed in this publication are those of the writers and do not necessarily reflect those of TRAFFIC, WWF or IUCN. Published by TRAFFIC. Southeast Asia Regional Office Unit 3-2, 1st Floor, Jalan SS23/11 Taman SEA, 47400 Petaling Jaya Selangor, Malaysia Telephone : (603) 7880 3940 Fax : (603) 7882 0171 Copyright of material published in this report is vested in TRAFFIC. © TRAFFIC 2016. ISBN no: 978-983-3393-52-7 UK Registered Charity No. 1076722. Suggested citation: Krishnasamy, K. (2016). Malaysia’s invisible ivory channel: An assessment of ivory seizures involving Malaysia from January 2003-May 2014. -

(MET) in Improving Maritime Sector in Malaysia

Open Journal of Business and Management, 2020, 8, 1193-1200 https://www.scirp.org/journal/ojbm ISSN Online: 2329-3292 ISSN Print: 2329-3284 Theories of Maritime Education and Training (MET) in Improving Maritime Sector in Malaysia Noorlee Boonadir1, Rosnah Ishak2, Hamidah Yusof2, Aida Fakhrul Lamakasauk3 1Maritime Management Section, Malaysian Institute of Marine Engineering Technology, Universiti Kuala Lumpur, Lumut, Malaysia 2Faculty of Management and Economy, Universiti Pendidikan Sultan Idris, Tanjung Malim, Malaysia 3Faculty of Modern Languages and Communication, Universiti Putra Malaysia, Seri Kembangan, Malaysia How to cite this paper: Boonadir, N., Abstract Ishak, R., Yusof, H., & Lamakasauk, A. F. (2020). Theories of Maritime Education The Ministry of Education (MOE) should focus on the provision of quality and Training (MET) in Improving Mari- academic programme as awareness to face the trends and challenges in the time Sector in Malaysia. Open Journal of era-globalization. Maritime education and Training (MET) is presently facing Business and Management, 8, 1193-1200. https://doi.org/10.4236/ojbm.2020.83076 many challenges thus to sustain a pool of qualified and competent profession is at a risk. The strong factors affect the implementation of maritime educa- Received: January 8, 2020 tion and training which may help the MET compete with other education Accepted: May 16, 2020 Published: May 19, 2020 fields in the educational institution. MET execution will be able to produce manpower that equip with the skills and knowledge with quality exposure ei- Copyright © 2020 by author(s) and ther for maritime education institution. Scientific Research Publishing Inc. This work is licensed under the Creative Keywords Commons Attribution International License (CC BY 4.0). -

Malaysian Container Seaport-Hinterland Connectivity: Status, Challenges and Strategies

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Elsevier - Publisher Connector The Asian Journal of Shipping and Logistics 32(3) (2016) 127-137 Contents lists available at Science Direct The Asian Journal of Shipping and Logistics Journal homepage: www.elsevier.com/locate/ajsl Malaysian Container Seaport-Hinterland Connectivity: Status, Challenges and Strategies Shu-Ling CHENa, Jagan JEEVANb, Stephen CAHOONc a Senior Lecturer, Australian Maritime College, University of Tasmania, Australia: Email: [email protected], (Corresponding Author) b PhD Candidate, Australian Maritime College, University of Tasmania, Australia: Email: [email protected] c Director, Sense-T, University of Tasmania, Australia: Email: [email protected] A R T I C L E I N F O A B S T R A C T Article history: This paper adopts a qualitative methodology to assess the Malaysian container seaport-hinterland Received 3 Feburary 2016 connectivity from the perspective of its physical properties. The findings reveal that although Received in revised form 30 August 2016 Malaysia’s major container seaports are connected to the hinterlands through road and rail Accepted 1 September 2016 transport, they are highly dependent on road. These seaports are also connected to inland freight facilities such as dry ports and ICDs, which are positioned as transit points to help connect Keywords: Malaysia exporters and importers in the hinterlands to seaports as well as facilitating regional and cross- Hinterland Connectivity border trades. This paper suggests that the quality of hinterland connectivity of Malaysian container Container Seaports seaports could be improved by implementing strategies which tackle the existing challenges Inland Facilities including overcoming an extremely imbalanced modal split, insufficient rail capacity and limited train services, increasing road congestion and the limitations of space restriction in some inland facilities.