24January 2020 India Daily

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

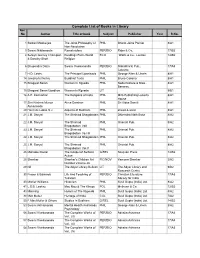

Complete List of Books in Library Acc No Author Title of Book Subject Publisher Year R.No

Complete List of Books in Library Acc No Author Title of book Subject Publisher Year R.No. 1 Satkari Mookerjee The Jaina Philosophy of PHIL Bharat Jaina Parisat 8/A1 Non-Absolutism 3 Swami Nikilananda Ramakrishna PER/BIO Rider & Co. 17/B2 4 Selwyn Gurney Champion Readings From World ECO `Watts & Co., London 14/B2 & Dorothy Short Religion 6 Bhupendra Datta Swami Vivekananda PER/BIO Nababharat Pub., 17/A3 Calcutta 7 H.D. Lewis The Principal Upanisads PHIL George Allen & Unwin 8/A1 14 Jawaherlal Nehru Buddhist Texts PHIL Bruno Cassirer 8/A1 15 Bhagwat Saran Women In Rgveda PHIL Nada Kishore & Bros., 8/A1 Benares. 15 Bhagwat Saran Upadhya Women in Rgveda LIT 9/B1 16 A.P. Karmarkar The Religions of India PHIL Mira Publishing Lonavla 8/A1 House 17 Shri Krishna Menon Atma-Darshan PHIL Sri Vidya Samiti 8/A1 Atmananda 20 Henri de Lubac S.J. Aspects of Budhism PHIL sheed & ward 8/A1 21 J.M. Sanyal The Shrimad Bhagabatam PHIL Dhirendra Nath Bose 8/A2 22 J.M. Sanyal The Shrimad PHIL Oriental Pub. 8/A2 Bhagabatam VolI 23 J.M. Sanyal The Shrimad PHIL Oriental Pub. 8/A2 Bhagabatam Vo.l III 24 J.M. Sanyal The Shrimad Bhagabatam PHIL Oriental Pub. 8/A2 25 J.M. Sanyal The Shrimad PHIL Oriental Pub. 8/A2 Bhagabatam Vol.V 26 Mahadev Desai The Gospel of Selfless G/REL Navijvan Press 14/B2 Action 28 Shankar Shankar's Children Art FIC/NOV Yamuna Shankar 2/A2 Number Volume 28 29 Nil The Adyar Library Bulletin LIT The Adyar Library and 9/B2 Research Centre 30 Fraser & Edwards Life And Teaching of PER/BIO Christian Literature 17/A3 Tukaram Society for India 40 Monier Williams Hinduism PHIL Susil Gupta (India) Ltd. -

2005 (Pdf, 4.7

2006 Global Citizenship Report Vital Responsible Ethical Global Governance Integrity Technology Product Innovative Reliable Operations Speed Agility Supply Expert Privacy Trustworthy Safety Collaborative Employee Citizenship Diversity Engaging Customer Relationship Accessible Social Meaningful Profitable Public Leadership Optimistic Forward Growth Inventive Essential Report About this report Table of contents GRI indicators* Scope 1. Introduction . 3 2.11-2.13, 2.15 This report describes HP’s HP’s global citizenship priorities . 3 3.19 global citizenship activities L e t t e r f ro m C EO M a r k H u rd . 4 1.1-1.2 worldwide. It charts HP’s progress in fiscal year 2005. H P p ro fi l e . 5 2.1-2.8, 3.7, EC1-EC2 Letter from Diana Bell . 7 1.1-1.2 Reporting year Global citizenship . 8 1.1, 3.6, 3.19 All data are for HP’s fiscal year 2005 (ending October 31, 2005), Economic value . 12 EC3, EC5, EC6, EC8, EC13 unless otherwise noted. 2. Governance and ethics . 15 Corporate governance . 15 3.1-3.2, 3.4, 3.6, 3.8 Currency and measurement All $ references in this document Business ethics . 16 3.7, HR10, SO2, SO7, PR9 are U.S. dollars, unless otherwise 3. Product environmental impacts . 18 3.19, EN14 noted. D e s i g n f o r E nvi ro n m e n t . 18 3.16-3.17, PR6 Measures used in the report are E n e rgy e f fi ci e n c y . 22 EN30 metric, except where stated. -

Lata S Singh

Lata S Singh https://www.facebook.com/latassingh © All Rights Reserved Information Acting age 22 - 30 years Nationality Indian Year of birth 1993 (27 years) Languages Hindi: native-language Height (cm) 166 German: basic Weight (in kg) 52 English: fluent Eye color black French: basic Hair color Black Dialects English: always Hair length Very long Brooklyn-English: only when Stature female required Place of residence Mumbai Minnesota-English: only when Cities I could work in Berlin, Paris, Cardiff, required Hamburg American: always Accents Indian: always American: always Instruments Harmonica: medium Sport Bycicle racing, Climb, Cricket, Fitness, Floor Exercise, Free Climbing, Frisbee, Hiking, Martial Arts, Mountain hiking, Yoga Dance Indian dance: professional Musical theatre: professional Freestyle dance: professional Folk dance: professional Expressionist dance: professional Bollywood dance: professional Improvisation dance: professional Experimental dance: professional Argentine tango: basic Contact Improvisation: professional Classic Indian dance: basic Profession Actor, Speaker, Young actor Singing Song: basic folk song: basic Vita Lata S Singh by www.castupload.com — As of: 2021-05-16 Page 1 of 4 Pitch Alto Other licenses Motorbike test certificate Professional background Actor* Originally from Delhi, India where I found my foundation in street theatre during college. Currently lives in Mumbai. Will travel. Since 2015, I've been made to jump existential hoops by incredible mentors and theatre directors from France, Poland, UK, Portugal, -

Jantar Mantar Strike Seeks a Sustainable Earth

STUDENT PAPER OF TIMES SCHOOL OF MEDIA GREATER NOiDA | MONDAY, OCTOBER 14, 2019 | VOL 3 , ISSUE 8 | PAGES 8 THE TIMESOF BENNETT Exploring a slice of Tibet in Delhi Trophy from the hunt Hip-hop: culture over trends The ISAC Walk 1.0 : Glimpses of Geeta Bisht, BU’s front desk executive, on Rapper’s take on today’s the photowalk to Majnu-ka-tilla winning the Super Model Hunt 2019 hip-hop industry | Page 5 | Page 4 | Page 6 BU hosts 1st inter-college sports fest, Expedite 2019 Silent walks to By ASHIMA CHOUDHARY were soul-stirring. As the the yum eateries. Even Zardicate came together was one to remember. took trophies, cash mon- Bennett University con- audience and athletes Mrs. Pratima was thrilled to mellow down the stress The crowd lit up the night ey and hampers home! fight harassment ducted its first-ever came together, the event to see the level of enthu- from the tournaments. with grooving students The stir caused by sports fest from 27th to electrified the atmosphere. siasm shown by students. The first night ended with and radium accessories. the fest was palpable as 29th of September. It Food stalls, to source In her words, “I expect- a bonfire, relaxing every- The DJ night lasted well Yashraj Saxena, former welcomed 400 students everyone’s energy, were ed it to be chaotic, but one, but it was the 28th, into the hours. Everyone head of the committee, from 16 universities from voiced his words, “We’ve the Delhi NCR region, been trying to host this Jaipur, Gwalior and a for the past two years. -

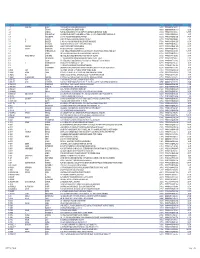

SR NO First Name Middle Name Last Name Address Pincode Folio

SR NO First Name Middle Name Last Name Address Pincode Folio Amount 1 A SPRAKASH REDDY 25 A D REGIMENT C/O 56 APO AMBALA CANTT 133001 0000IN30047642435822 22.50 2 A THYAGRAJ 19 JAYA CHEDANAGAR CHEMBUR MUMBAI 400089 0000000000VQA0017773 135.00 3 A SRINIVAS FLAT NO 305 BUILDING NO 30 VSNL STAFF QTRS OSHIWARA JOGESHWARI MUMBAI 400102 0000IN30047641828243 1,800.00 4 A PURUSHOTHAM C/O SREE KRISHNA MURTY & SON MEDICAL STORES 9 10 32 D S TEMPLE STREET WARANGAL AP 506002 0000IN30102220028476 90.00 5 A VASUNDHARA 29-19-70 II FLR DORNAKAL ROAD VIJAYAWADA 520002 0000000000VQA0034395 405.00 6 A H SRINIVAS H NO 2-220, NEAR S B H, MADHURANAGAR, KAKINADA, 533004 0000IN30226910944446 112.50 7 A R BASHEER D. NO. 10-24-1038 JUMMA MASJID ROAD, BUNDER MANGALORE 575001 0000000000VQA0032687 135.00 8 A NATARAJAN ANUGRAHA 9 SUBADRAL STREET TRIPLICANE CHENNAI 600005 0000000000VQA0042317 135.00 9 A GAYATHRI BHASKARAAN 48/B16 GIRIAPPA ROAD T NAGAR CHENNAI 600017 0000000000VQA0041978 135.00 10 A VATSALA BHASKARAN 48/B16 GIRIAPPA ROAD T NAGAR CHENNAI 600017 0000000000VQA0041977 135.00 11 A DHEENADAYALAN 14 AND 15 BALASUBRAMANI STREET GAJAVINAYAGA CITY, VENKATAPURAM CHENNAI, TAMILNADU 600053 0000IN30154914678295 1,350.00 12 A AYINAN NO 34 JEEVANANDAM STREET VINAYAKAPURAM AMBATTUR CHENNAI 600053 0000000000VQA0042517 135.00 13 A RAJASHANMUGA SUNDARAM NO 5 THELUNGU STREET ORATHANADU POST AND TK THANJAVUR 614625 0000IN30177414782892 180.00 14 A PALANICHAMY 1 / 28B ANNA COLONY KONAR CHATRAM MALLIYAMPATTU POST TRICHY 620102 0000IN30108022454737 112.50 15 A Vasanthi W/o G -

Recruiter's Handbook 2020

Recruiter’s Handbook 2020 VISION To create a state-of-the-art institution that sets new standards of world-class education in film, communication and creative arts. MISSION Benchmarking quality, inspiring innovation, encouraging creativity & moulding minds, by leading from the front in the field of film, media and entertainment education. ONE OF THE TEN BEST FILM SCHOOLS IN THE WORLD - THE HOLLYWOOD REPORTER Degree & Diploma 5.5 ACRE programmes CAMPUS acceredited by the TISS 1300+ 2200+ STUDENTS Media & Film industry Alumni campus SCHOOL OF EVENT MANAGEMENT Subhash Ghai Founder & Chairman, Whistling Woods International Chairman, Mukta Arts Limited Member, Executive Committee, Film & Television Producers Guild of India Member, United Producers Forum Education Evangelist Karamveer Chakra Awardee Chairman, MESC Subhash Ghai is a globally renowned filmmaker having directed 19 films over a four-decade career, with 14 of them being blockbusters. Recipient of many national and international awards, he has also been honoured by the United States Senate. He has been a former Chairman of the Entertainment Committee of Trade body CII and also a member of FICCI, NASSCOM and TIE Global & its alliances. He has been invited to address various forums and seminars on corporate governance and the growth of Media & Entertainment industry globally and in India. He is presently serving as the Chairman of Media and Entertainment Skills Council (MESC). Message from the Founder & Chairman My journey as a filmmaker in the Media & Entertainment (M&E) industry has been a long and cherished one. Over the years, the one factor that has grounded me and contributed to my success is the basic film education I received from the film institute I studied in, coupled with my strong desire to learn and re-learn from my days as part of the Indian film industry. -

Film Tourism in India – a Beginning Towards Unlocking Its Potential

Film tourism in India – a beginning towards unlocking its potential FICCI Shoot at Site 2019 13 March 2019 Film tourism is a growing phenomenon worldwide, fueled by both the growth of the entertainment industry and the increase in international travel. Film tourism sector has seen tremendous growth in the past few years. It represents a gateway to new and more intense ways of experiencing destinations. At the same time, it creates the potential for new communities by way of an exchange of insights, knowledge and experience among the tourists themselves. Films play a significant role in the promotion of tourism in various countries and different states of India. A film tourist is attracted by the first-hand experience of the location captured on the silver screen. Not only is film tourism an excellent vehicle for destination marketing, it also presents new product development opportunities, such as location tours, film museums, exhibitions and the theme of existing tourist attractions with a film connection. This report focusses on the concept of film tourism and the various initiatives taken by both the state and central government of India for boosting film induced tourism through their respective film production policies. Dilip Chenoy Secretary General - Federation of Indian Chamber of Commerce and Industry Foreword The significance of cinema in today’s times has gone beyond its intended purpose of mass entertainment. Cinema is a portal for people to escape from reality and into their world of fantasy. Cinema is a source of inspiration for some, a source of entertainment for some and a source of education for some. -

Song Catalogue February 2020 Artist Title 2 States Mast Magan 2 States Locha E Ulfat 2 Unlimited No Limit 2Pac Dear Mama 2Pac Changes 2Pac & Notorious B.I.G

Song Catalogue February 2020 Artist Title 2 States Mast Magan 2 States Locha_E_Ulfat 2 Unlimited No Limit 2Pac Dear Mama 2Pac Changes 2Pac & Notorious B.I.G. Runnin' (Trying To Live) 2Pac Feat. Dr. Dre California Love 3 Doors Down Kryptonite 3Oh!3 Feat. Katy Perry Starstrukk 3T Anything 4 Non Blondes What's Up 5 Seconds of Summer Youngblood 5 Seconds of Summer She's Kinda Hot 5 Seconds of Summer She Looks So Perfect 5 Seconds of Summer Hey Everybody 5 Seconds of Summer Good Girls 5 Seconds of Summer Girls Talk Boys 5 Seconds of Summer Don't Stop 5 Seconds of Summer Amnesia 5 Seconds of Summer (Feat. Julia Michaels) Lie to Me 5ive When The Lights Go Out 5ive We Will Rock You 5ive Let's Dance 5ive Keep On Movin' 5ive If Ya Getting Down 5ive Got The Feelin' 5ive Everybody Get Up 6LACK Feat. J Cole Pretty Little Fears 7Б Молодые ветра 10cc The Things We Do For Love 10cc Rubber Bullets 10cc I'm Not In Love 10cc I'm Mandy Fly Me 10cc Dreadlock Holiday 10cc Donna 30 Seconds To Mars The Kill 30 Seconds To Mars Rescue Me 30 Seconds To Mars Kings And Queens 30 Seconds To Mars From Yesterday 50 Cent Just A Lil Bit 50 Cent In Da Club 50 Cent Candy Shop 50 Cent Feat. Eminem & Adam Levine My Life 50 Cent Feat. Snoop Dogg and Young Jeezy Major Distribution 101 Dalmatians (Disney) Cruella De Vil 883 Nord Sud Ovest Est 911 A Little Bit More 1910 Fruitgum Company Simon Says 1927 If I Could "Weird Al" Yankovic Men In Brown "Weird Al" Yankovic Ebay "Weird Al" Yankovic Canadian Idiot A Bugs Life The Time Of Your Life A Chorus Line (Musical) What I Did For Love A Chorus Line (Musical) One A Chorus Line (Musical) Nothing A Goofy Movie After Today A Great Big World Feat. -

Magazine-1-4.Qxd (Page 2)

SUNDAY, OCTOBER 4, 2015 (PAGE-4) MOVIE-REVIEW PERSONALITY Comedy as a poor joke A teacher on a mission Saibal Chatterjee As completely meaningless as its silly title, Singh is Bliing is an Gopal Sharma NOBODY COMES HERE BUT THIS MADAM OFTEN COMES AND HAS attempted comedy that is funny for all the wrong reasons. It has no sto- Notwithstanding the innumerous hurdles and eco- ry, no screenplay and no logic. nomic constraints, a very humble and optimistic Gov- ENGAGED TWO FEMALE TEACHERS FOR OUR CHILDREN’S STUDY. SHE EVEN Co-produced by Akshay Kumar himself, the film is designed to give ernment teacher is moving ahead with her missionary the Bollywood star a standard range of things to do on the screen. On zeal to reform the children taking to rag- picking and TEACHES ON SUNDAYS. WE ARE PAYING NOTHING AND EVEN THE BOOKS, his part, with all his mannerisms intact, he plunges headlong into the begging and imparting them free education in a labour assignment. colony near Jammu Railway Station. NOTEBOOKS, PENS/ PENCILS, BAGS ETC ARE MANAGED BY THIS TEACHER. Unfortunately, Singh is Bliing is so utterly brainless that no matter While doing justice with her job and teaching chil- how enthusiastically Akshay strives to make it work with his brand of dren at a Govt Higher Secondary School in district Sam- buffoonery, he only hits his head against a shoddy wall of a script. ba (Sumb), this teacher (Lecturer) is also sparing time Singh is Bliing is Prabhudheva's first 'original' Hindi film, but it recy- for these children of ‘lesser God’ and trying hard to illu- cles all the cliched, lowbrow tropes he is known for. -

EROS INTERNATIONAL PLC (Translation of Registrant’S Name Into English)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 6-K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO SECTION 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934 For the month of June, 2016 001-36176 (Commission file number) EROS INTERNATIONAL PLC (Translation of registrant’s name into English) 550 County Avenue Secaucus, New Jersey 07094 (Address of principal executive office) ________________________________________ Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F. Form 20-F ☑ Form 40-F ☐ Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934. Yes ☐ No ☑ If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): Other Events This report on Form 6-K is being furnished to disclose the press release issued by the Registrant on June 28, 2016. The purpose of the press release, furnished as Exhibit 99.1, was to announce the Registrant’s results of operations for the fourth quarter and fiscal year ended March 31, 2016. The information in this Form 6-K and Exhibit 99.1 attached hereto shall not be deemed “filed” for purposes of Section 18 of the Securities Act of 1934. SIGNATURE Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized. -

Index to Volume 29 January to December 2019 Compiled by Patricia Coward

THE INTERNATIONAL FILM MAGAZINE Index to Volume 29 January to December 2019 Compiled by Patricia Coward How to use this Index The first number after a title refers to the issue month, and the second and subsequent numbers are the page references. Eg: 8:9, 32 (August, page 9 and page 32). THIS IS A SUPPLEMENT TO SIGHT & SOUND SUBJECT INDEX Film review titles are also Akbari, Mania 6:18 Anchors Away 12:44, 46 Korean Film Archive, Seoul 3:8 archives of television material Spielberg’s campaign for four- included and are indicated by Akerman, Chantal 11:47, 92(b) Ancient Law, The 1/2:44, 45; 6:32 Stanley Kubrick 12:32 collected by 11:19 week theatrical release 5:5 (r) after the reference; Akhavan, Desiree 3:95; 6:15 Andersen, Thom 4:81 Library and Archives Richard Billingham 4:44 BAFTA 4:11, to Sue (b) after reference indicates Akin, Fatih 4:19 Anderson, Gillian 12:17 Canada, Ottawa 4:80 Jef Cornelis’s Bruce-Smith 3:5 a book review; Akin, Levan 7:29 Anderson, Laurie 4:13 Library of Congress, Washington documentaries 8:12-3 Awful Truth, The (1937) 9:42, 46 Akingbade, Ayo 8:31 Anderson, Lindsay 9:6 1/2:14; 4:80; 6:81 Josephine Deckers’s Madeline’s Axiom 7:11 A Akinnuoye-Agbaje, Adewale 8:42 Anderson, Paul Thomas Museum of Modern Art (MoMA), Madeline 6:8-9, 66(r) Ayeh, Jaygann 8:22 Abbas, Hiam 1/2:47; 12:35 Akinola, Segun 10:44 1/2:24, 38; 4:25; 11:31, 34 New York 1/2:45; 6:81 Flaherty Seminar 2019, Ayer, David 10:31 Abbasi, Ali Akrami, Jamsheed 11:83 Anderson, Wes 1/2:24, 36; 5:7; 11:6 National Library of Scotland Hamilton 10:14-5 Ayoade, Richard -

HM 13 July Page 10.Qxd

www.himalayanmail.com 10 JAMMU ☯ TUESDAY ☯ JULY 13, 2021 ENTERTAINMENT The Himalayan Mail Anushka Shetty, Sonali Kulkarni and Kangana's best wishes for Ankita Lokhande as she more actresses who played onscreen kickstarts shooting for Pavitra Rishta 2 he shooting of the second season of TPavitra Rishta has mother to male stars older to them begun. Just yesterday, the ctresses who pictures and videos from the played onscreen sets of Pavitra Rishta 2 were Amother to male dropped by ALTBalaaji and stars older to them Zee5 and the cast and crew Well, we have seen many of the show were dropped on actresses of the entertain- social media. It went viral on ment industry speaking social media real quick. Sha- about being type casted and heer Sheikh has stepped into revealed how they are of- the shoes of Sushant Singh fered only roles of a Rajput's role of Manav. 'mother' after a certain age. Friends and colleagues of Well, in this gallery, we will Ankita Lokhande aka meet the actresses who Archana have been sending played mothers to male her best wishes for her new stars older to them. show. And joining them is Anushka Shetty noted Bollywood actress In the Baahubali fran- Kangana Ranaut. The chise, Anushka Shetty Queen actress worked with played the role of Prabhas' Ankita in Manikarnika: The mother, Devasena. At that Queen of Jhansi. The two ac- Ankita too thanked her tion. form. "Yes, I am aware that time Anushka was 36 and tresses grew close to each for the wishes. "Thanku Coming back to Pavitra Pavitra Rishta is getting a the Saaho star was 38.