The Case of Baseball Cards∗

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

April 2021 Auction Prices Realized

APRIL 2021 AUCTION PRICES REALIZED Lot # Name 1933-36 Zeenut PCL Joe DeMaggio (DiMaggio)(Batting) with Coupon PSA 5 EX 1 Final Price: Pass 1951 Bowman #305 Willie Mays PSA 8 NM/MT 2 Final Price: $209,225.46 1951 Bowman #1 Whitey Ford PSA 8 NM/MT 3 Final Price: $15,500.46 1951 Bowman Near Complete Set (318/324) All PSA 8 or Better #10 on PSA Set Registry 4 Final Price: $48,140.97 1952 Topps #333 Pee Wee Reese PSA 9 MINT 5 Final Price: $62,882.52 1952 Topps #311 Mickey Mantle PSA 2 GOOD 6 Final Price: $66,027.63 1953 Topps #82 Mickey Mantle PSA 7 NM 7 Final Price: $24,080.94 1954 Topps #128 Hank Aaron PSA 8 NM-MT 8 Final Price: $62,455.71 1959 Topps #514 Bob Gibson PSA 9 MINT 9 Final Price: $36,761.01 1969 Topps #260 Reggie Jackson PSA 9 MINT 10 Final Price: $66,027.63 1972 Topps #79 Red Sox Rookies Garman/Cooper/Fisk PSA 10 GEM MT 11 Final Price: $24,670.11 1968 Topps Baseball Full Unopened Wax Box Series 1 BBCE 12 Final Price: $96,732.12 1975 Topps Baseball Full Unopened Rack Box with Brett/Yount RCs and Many Stars Showing BBCE 13 Final Price: $104,882.10 1957 Topps #138 John Unitas PSA 8.5 NM-MT+ 14 Final Price: $38,273.91 1965 Topps #122 Joe Namath PSA 8 NM-MT 15 Final Price: $52,985.94 16 1981 Topps #216 Joe Montana PSA 10 GEM MINT Final Price: $70,418.73 2000 Bowman Chrome #236 Tom Brady PSA 10 GEM MINT 17 Final Price: $17,676.33 WITHDRAWN 18 Final Price: W/D 1986 Fleer #57 Michael Jordan PSA 10 GEM MINT 19 Final Price: $421,428.75 1980 Topps Bird / Erving / Johnson PSA 9 MINT 20 Final Price: $43,195.14 1986-87 Fleer #57 Michael Jordan -

LCCC Thematic List

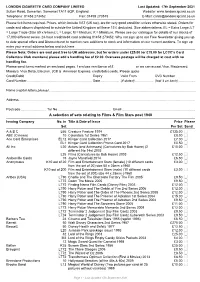

LONDON CIGARETTE CARD COMPANY LIMITED Last Updated: 17th September 2021 Sutton Road, Somerton, Somerset TA11 6QP, England. Website: www.londoncigcard.co.uk Telephone: 01458 273452 Fax: 01458 273515 E-Mail: [email protected] Please tick items required. Prices, which include VAT (UK tax), are for very good condition unless otherwise stated. Orders for cards and albums dispatched to outside the United Kingdom will have 15% deducted. Size abbreviations: EL = Extra Large; LT = Large Trade (Size 89 x 64mm); L = Large; M = Medium; K = Miniature. Please see our catalogue for details of our stocks of 17,000 different series. 24-hour credit/debit card ordering 01458 273452. Why not sign up to our Free Newsletter giving you up to date special offers and Discounts not to mention new additions to stock and information on our current auctions. To sign up enter your e-mail address below and tick here _____ Please Note: Orders are sent post free to UK addresses, but for orders under £25.00 (or £15.00 for LCCC's Card Collectors Club members) please add a handling fee of £2.00. Overseas postage will be charged at cost with no handling fee. Please send items marked on enclosed pages. I enclose remittance of £ or we can accept Visa, Mastercard, Maestro, Visa Delta, Electron, JCB & American Express, credit/debit cards. Please quote Credit/Debit Expiry Valid From CVC Number Card Number...................................................................... Date .................... (if stated).................... (last 3 on back) .................. Name -

THE LONDON CIGARETTE CARD COMPANY LIMITED Sutton Road, Somerton, Somerset TA11 6QP, England

THE LONDON CIGARETTE CARD COMPANY LIMITED Sutton Road, Somerton, Somerset TA11 6QP, England. Website: www.londoncigcard.co.uk Telephone: 01458 273452 Fax: 01458 273515 E-Mail: [email protected] POSTAL AUCTION ENDING 30TH APRIL 2016 CATALOGUE OF CIGARETTE & TRADE CARDS & OTHER CARTOPHILIC ITEMS TO BE SOLD BY POSTAL AUCTION Bids can be submitted by post, phone, fax, e-mail or through our website. Estimates include VAT. Successful bidders outside the European Community will have 15% (UK tax) deducted from prices realized. Abbreviations used: FCC = Finest Collectable Condition; VG = Very Good; G = Good; F = Fair; P = Poor; VP = Very Poor; O/W = Otherwise; EL = Extra Large; LT = Large Trade (89 x 64mm) L = Large; M = Medium; K = Miniature; Type Card = one card from a set; 27/50 = 27 cards out of a set of 50 etc; EST in end column = Estimated Value. See biding sheet for conditions of sale. Last date for receipt of bids Saturday 30th April. There are no additional charges to bidders for buyers premium etc. LOT ISSUER DESCRIPTION CONDITION EST 1 IMPEL/PACIFIC USA 2LT Sets Laffs, The College Years Saved by the Bell 1991-94……………………………………………… Mint £16 2 A & M WIX Set 250 Cinema Cavalcade 1st Series (mixed sizes as issued) 1939………….. Few creased, some F O/W G-VG £250 3 TYPHOO TEA Set 25 Common Objects Highly Magnified 1925…………………………………………………….. 1G O/W VG-FCC £40 4 WILLS 12/100 Soldiers of the World ‘Ld’ back thick card 1895…………………………………………………………… P-F £30 5 SKYBOX/RITTENHOUSE 2LT Sets Gargoyles Series 2, Conan Art of the Hyborian Age 1996-2004……………………………… Mint £21 6 PARKHURST Canada M79/100 Birds c1950………………………………………………………………………………. -

Dec Pages 79-84.Qxd 8/5/2019 12:45 PM Page 1

ASC080119_080_Dec Pages 79-84.qxd 8/5/2019 12:45 PM Page 1 All Star Cards To Order Call Toll Free Page 86 15074 Antioch Road Overland Park, KS 66221 www.allstarcardsinc.com (800) 932-3667 BOXING 1927-30 EXHIBITS: 1938 CHURCHMAN’S: 1951 TOPPS RINGSIDE: 1991 PLAYERS INTERNATIONAL Dempsey vs. Tunney “Long Count” ...... #26 Joe Louis PSA 8 ( Nice! ) Sale: $99.95 #33 Walter Cartier PSA 7 Sale: $39.95 (RINGLORDS): ....... SGC 60 Sale: $77.95 #26 Joe Louis PSA 7 $69.95 #38 Laurent Dauthuille PSA 6 $24.95 #10 Lennox Lewis RC PSA 9 $17.95 Dempsey vs. Tunney “Sparing” ..... 1939 AFRICAN TOBACCO: #10 Lennox Lewis RC PSA 8.5 $11.95 ....... SGC 60 Sale: $77.95 NEW! #26 John Henry Lewis PSA 4 $39.95 1991 AW SPORTS BOXING: #13 Ray Mercer RC PSA 10 Sale: $23.95 #147 Muhammad Ali Autographed (Black #14 Michael Moorer RC PSA 9 $14.95 1935 PATTREIOUEX: 1948 LEAF: ....... Sharpie) PSA/DNA “Authentic” $349.95 #31 Julio Cesar-Chavez PSA 10 $29.95 #56 Joe Louis RC PSA 5 $139.95 #3 Benny Leonard PSA 5 $29.95 #33 Hector “Macho” Camacho PSA 10 $33.95 #78 Johnny Coulon PSA 5 $23.95 1991 AW SPORTS BOXING: #33 Hector “Macho” Camacho PSA 9 $17.95 1937 ARDATH: 1950 DUTCH GUM: #147 Muhammad Ali Autographed (Black NEW! Joe Louis PSA 7 ( Tough! ) $99.95 ....... Sharpie) PSA/DNA “Authentic” $349.95 1992 CLASSIC W.C.A.: #D18 Floyd Patterson RC PSA $119.95 Muhammad Ali Autographed (with ..... 1938 CHURCHMAN’S: 1951 TOPPS RINGSIDE: 1991 PLAYERS INTERNATIONAL ...... -

July 2011 Prices Realized

HUGGINS & SCOTT JULY 28, 2011 PRICES REALIZED LOT# TITLE BIDS SALE PRICE 1 1968 Topps 3-D Near Set of (10/12) PSA Graded Cards with Perez & Stottlemyre 33 $16,450.00 2 1968 Topps 3-D Roberto Clemente PSA 5 25 $8,225.00 3 1968 Topps 3-D Ron Fairly (No Dugout) Variation PSA 7 8 $763.75 4 1968 Topps 3-D Jim Maloney (No Dugout) Variation PSA 6 3 $528.75 5 1968 Topps 3-D Willie Davis PSA 6 8 $381.88 6 1968 Topps 3-D Jim Lonborg PSA 8 24 $1,410.00 7 1968 Topps 3-D Jim Maloney PSA 8 12 $499.38 8 1968 Topps 3-D Tony Perez PSA 8 33 $3,525.00 9 1968 Topps 3-D Boog Powell PSA 8 30 $2,820.00 10 1968 Topps 3-D Ron Swoboda PSA 7 27 $1,997.50 11 1909-11 T206 Walter Johnson Portrait PSA EX 5 14 $1,410.00 12 (4) 1909-11 T206 White Border Ty Cobb Pose Variations-All PSA Graded 28 $3,818.75 13 (4) 1909-11 T206 Graded Hall of Famers & Stars with Lajoie & Mathewson 18 $940.00 14 (10) 1909-11 T206 White Border Graded Cards—All SGC 50-60 11 $528.75 15 (42) T205 Gold Borders & T206 White Borders with (17) Graded & (7) Hall of Famers/Southern Leaguers 21 $1,762.50 16 1912 T202 Hassan Triple Folders Egan/Mitchell PSA 7 4 $470.00 17 (37) 1919-21 W514 SGC Graded Collection with Ruth, Hornsby & Johnson--All Authentic 7 $1,292.50 18 (4) 1913 T200 Fatima Team Cards—All PSA or SGC 4 $558.13 19 (12) 1917 Collins-McCarthy SGC Graded Singles 12 $499.38 20 (7) 1934-36 Diamond Stars Semi-High Numbers—All SGC 60-80 6 $293.75 21 (18) 1934-36 Batter-Up High Numbers with (6) Hall of Famers—All SGC 60-80 12 $1,410.00 22 (5) 1940-1949 Play Ball, Bowman & Leaf Baseball Hall of -

Estate of Russel Dimartino Sports Cards and Sports Memorabilia Auction

09/29/21 06:52:05 Estate of Russel DiMartino Sports cards and Sports Memorabilia Auction Auction Opens: Tue, Jan 14 4:34pm CT Auction Closes: Fri, Feb 14 2:00pm CT Lot Title Lot Title 0001 Joe Namath New York Jets quarterback card 0029 1972 strikeout leaders Steve Carlton Phillies 0002 Walt Sweeney San Diego trading card Nolan Ryan Angels 0003 Joe Namath quarterback Jets trading card 0030 Trent Dilfer Tampa Bay buccaneers trading card 0004 Nolan Ryan Astro’s Trading Card 0031 1976 Dennis Eckersley Cleavland Indians trading card 0005 Brett Favre Atlanta Falcons Card 0032 Peyton Manning gold label trading card 0006 Nolan Ryan 1976 Angels trading card 0033 Michael Jordan NBA Legends Trading Card 0007 Phil Simms New York Giants trading card 0034 1985 Warren Moon Houston Oilers Trading card 0008 Dan Marino trading card 0035 Hank Aaron 1976 Milwaukee Brewers trading 0009 1976 Hank Aaron’s Brewers Trading Card card 0010 1998 playoff prestige Randy Moss trading card 0036 19 Chris Chandler Indianapolis Colts Trading 0011 1986 Jerry Rice San Francisco 49ers trading Cards card 0037 Nolan Ryan Mets Trading Card 0012 1998 Peyton Manning Rookie Colts 0038 John Unitas Colts 2000 Reprint 0013 Dave Winfield San Diego Padres trading card 0039 3 Mark McGwire Trading Cards 0014 Troy Aikman Dallas Cowboys 2000 Sno globe 0040 Steve DeLong defensive and San Diego trading Card chargers trading card 0015 Brett Favre Atlanta Falcons Pro Set platinum 0041 John Elway Denver Broncos game day card trading card 0042 Peyton Manning draft picks 1998 0016 Jose Canseco -

Message from the Owner of American Legends Launch Calendar For

Launch Calendar for January-March January, 2008 Message from the Owner of American Legends SPORTS CARDS AUThenTIcaTED & ENTERTAInmenT Dear Fellow Diamond Dealers, CollecTIbles JANUARY JANUARY Now that the holidays have passed, we need to come up with ways to get customers to walk • NHL Trilogy JANUARY • Yu-Gi-Oh! TCG Duelist through our doors again. Having just celebrated my 15th anniversary of owning a hobby shop, • NFL Sweet Spot • New Kevin Durant Signed Memorabilia Pack 6 & 7 — Jaden Yuki 3 & I realize how important this time is for retailers like us. Upper Deck has come up with a great program to help us • NHL SPx • LeBron James Jersey ROY Archives Box Jesse Anderson ® engage our customers in Baseball early on in the year and to keep that excitement going through the All-Star Game • NBA Fleer • All Star Vinyl: Peyton Manning • World of Warcraft TCG • NFA SP Authentic Magtheridon’s Lair Raid on into the playoffs. It’s called the Yankee Stadium Legacy Program and you have likely already heard about it. • NHL SP Game Used Deck As many of you know, Yankee fans are just a special breed. They really do live and die with their team from spring FEBRUARY ® • 2007/08 NHL Rookie Class Box Set • World of Warcraft TCG training to the last game of the season. The advantage for hobby shop owners is that they definitely spend a lot of Accessories FEBRUARY • Legends of Basketball Framed Piece money to support their love of all Yankee-related things. Imagine their excitement when they discover a 6500 card • 2007 MLB World Series Champions • MLB UD Series 1 Boston Red Sox Peterbilt Tractor set documenting every home game and major sports event hosted at Yankee Stadium! For these fans, this truly will • NBA SP Authentic FEBRUARY with Trailer • Yu-Gi-Oh! TCG Phantom be the collection of a lifetime. -

A Review of the Post-WWII Baseball Card Industry

A Review of the Post-WWII Baseball Card Industry Artie Zillante University of North Carolina Charlotte November 25th,2007 1Introduction If the attempt by The Upper Deck Company (Upper Deck) to purchase The Topps Company, Inc. (Topps) is successful, the baseball card industry will have come full circle in under 30 years. A legal ruling broke the Topps monopoly in the industry in 1981, but by 2007 the industry had experienced a boom and bust cycle1 that led to the entry and exit of a number of firms, numerous innovations, and changes in competitive practices. If successful, Upper Deck’s purchase of Topps will return the industry to a monopoly. The goal of this piece is to look at how secondary market forces have shaped primary market behavior in two ways. First, in the innovations produced as competition between manufacturers intensified. Second, in the change in how manufacturers competed. Traditional economic analysis assumes competition along one dimension, such as Cournot quantity competition or Bertrand price competition, with little consideration of whether or not the choice of competitive strategy changes. Thus, the focus will be on the suggested retail price (SRP) of cards as well as on the timing of product releases in the industry. Baseballcardshaveundergonedramaticchangesinthepasthalfcenturyastheindustryandthehobby have matured, but the last 20 years have provided a dramatic change in the types of products being produced. Prior to World War II, baseball cards were primarily used as premiums or advertising tools for tobacco and candy products. Information on the use of baseball cards as advertising tools in the tobacco and candy industries prior to World War II can be obtained from a number of different sources, including Kirk (1990) and most of the annual comprehensive baseball card price guides produced by Beckett publishing. -

Ingenious Inventions

Inventions Ingenious Prehistoric men and women In 1848, the Curtis brothers chewed on lumps of tree resin for pure made chewing gum from pure spruce enjoyment. For centuries the ancient tree resin. Later, adding paraffi n and Greeks chewed mastic gum derived from fl avoring to their already popular OST of us have enjoyed chewing the resin of the mastic tree. The word concoction, the brothers opened the gum at some point in our life. In M “mastic” in Greek means “to chew”. This fi rst major gum manufacturing plant, fact, people have enjoyed chewing gum- is the resin obtained from the bark of the Curtis Chewing Gum Factory. like substances in many lands and from the mastic tree, a shrub-like tree found very early times. The materials may mainly in Greece and Turkey. Grecian have been different – sometimes they women especially favored chewing were thickened resin and latex from Thomas Adams mastic gum to clean their teeth and certain kinds of trees, or various sweet sweeten their breath. grasses, leaves, grains and waxes. First fi nding relating to gum has been traced to 5000-year-old human settlements in Finland. In those distant times, many old cultures (Aztecs, Ancient Greeks and Egyptians) used several types of chewing gum as a mouth freshener and medicinal accessory. Thomas Adams was a photographer, he tried his hand at the gum business, boiling down chicle (natural gum collected from several species of Mesoamerican trees including M. zapota, M. chicle, M. staminodella, and M. bidentata) in his home. SCIENCE REPORTER, MARCH 2013 56 Ingenious Inventions Susan Montgomery Williams of Fresno, California established the Guinness World Record for the largest bubblegum bubble in 1996, blowing a bubble that measured 23 inches. -

The Auction List

Ephrata Lions Club Sports Card Show & Auction – 2:30 p.m., Saturday, October 23, 2021 Ephrata (PA) Recreation Center – Page 1 of 2 Lot Description Lot Description Lot Description Misc. Baseball, Basketball, Hockey 44 Matted New York Yankees 1958 Train Excursion Flyers 88 Auto. Navy Midshipmen Jersey Keenan Reynolds w/ COA-JSA 1 3 Mountain Dew Baseball Stand-ups 45 Babe Ruth and Mickey Mantle Handmade Wooden Plaques w/Career Stats 89 Auto. Steelers Jersey Joey Porter w/ COA-JSA 2 1970s Baltimore Oriole "The Bird" Stuffed Animal & Oriole Logo Mini BB Bat 46 Mickey Mantle Comic Book Graded CGC 9.4 90 Auto. Steelers Jersey Ernie Mills w/ COA-JSA 3 1960s Jim "Catfish" Hunter Signature Endorsed Padded Gun Case Autographed Baseball Items, Photos/Cards 91 Auto. NY Jets Jersey Don Maynard w/ COA-JSA 4 Ted Williams Box of Sears Shotgun Shells and '70s Ted's Root Beer Glass 47 Auto. 8x10 Photos (2) Johnny VanderMeer w/ Auto. Ticket 92 Auto. Warriors Jersey Rick Barry w/ COA-JSA 5 7 1962 Auravision 33 RPM Records w/ Maris, Koufax, Kaline et al. 48 Auto. Photo Willie Mays WS. "The Catch" w/ "Say Hey" Authentication Cert. 93 Auto. Yankees Jersey Bobby Shantz w/ COA-JSA 6 1990 Matchbox MLB Car Set w/ 26 Team Cars in Plastic Display Case 49 Auto. 8x10 Photo Don Newcombe (Deceased)*From Mr Mint/Alan Rosen 94 Auto. Phillies Jersey Rhys Hoskins w/ COA-Hunt Auction 7 1999 M. Jordan UD 19x19 Mobile Hanger w/4 Cards, 4 MJ Silhouettes 50 Auto. 8x10 Photo Al Gionfriddo (Deceased) Pittsburgh & Brooklyn *Mr Mint 95 Auto. -

Kit Young's Sale

KIT YOUNG’S SALE #21 Welcome to Kit Young’s Sale #21. Included in this sale are more fantastic sets MAKE US from The Barry Korngiebel Collection (and we have extended the “make us an AN OFFER II offer” option). Also included are outstanding new arrivals, 1/2 price GAI graded For a limited time you can make us an offer cards part II, baseball lot specials part II, a new set special section, Ted Williams on any set below (or any set on specials and much more. You can order by phone, fax, email, regular mail or www.kityoung.com). We will either accept online through Paypal, Google Checkout or credit cards. If you have any questions your offer or counter with a price more acceptable to both of us. or would like to email your order please email us at [email protected]. Our regular business hours are 8-6 Monday-Friday Pacific time. Toll Free 888-548-9686. 1948 BOWMAN FOOTBALL A 1962 TOPPS BASEBALL B COMPLETE SET VG-EX/EX COMPLETE SET EX-MT This 108 card set issued by Bowman consists of mostly Popular wood-grain border set loaded with stars and rookie cards as it was one of the very first football sets ever Hall of Famers. Overall grade is EX-MT (many better and issued. We’ll call this set VG-EX/EX overall with some better some less). Includes Koufax EX-MT, Clemente EX+/EX- (approx. 20 cards EX-MT) and a few worse. Most cards have MT, Mantle PSA 6 EX-MT, Maris EX/EX+, Berra PSA 6 some wear on the corners but still exhibit great eye appeal. -

Byron R. White Papers [Finding Aid]. Library of Congress. [PDF Rendered

Byron R. White Papers A Finding Aid to the Collection in the Library of Congress Manuscript Division, Library of Congress Washington, D.C. 2003 Revised 2012 April Contact information: http://hdl.loc.gov/loc.mss/mss.contact Additional search options available at: http://hdl.loc.gov/loc.mss/eadmss.ms003003 LC Online Catalog record: http://lccn.loc.gov/mm88077264 Prepared by Harry G. Heiss with the assistance of Kathleen Kelly and Robert Vietrogoski Revised and expanded by Harry G. Heiss with the assistance of Jennifer Bridges and John Monagle Collection Summary Title: Byron R. White Papers Span Dates: 1961-1993 ID No.: MSS77264 Creator: White, Byron R., 1917-2002 Size: 183,500 items ; 858 containers ; 361.4 linear feet Language: Collection material in English Location: Manuscript Division, Library of Congress, Washington, D.C. Summary: Associate justice of the United States Supreme Court, United States deputy attorney general, lawyer, naval intelligence officer, Rhodes scholar, and professional football player. Opinion files and related administrative records documenting cases heard during White's tenure on the Supreme Court, including material on cases involving the "Miranda law", abortion, child pornography, freedom of speech, homosexuality, racial bias, and liability of news organizations. Selected Search Terms The following terms have been used to index the description of this collection in the Library's online catalog. They are grouped by name of person or organization, by subject or location, and by occupation and listed alphabetically therein. People White, Byron R., 1917-2002. Organizations United States. Supreme Court. Subjects Abortion--United States. Child pornography--United States. Constitutional law--United States.