Oil and Gas ESG Industry Report Card

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TEACHERS' RETIREMENT SYSTEM of the STATE of ILLINOIS 2815 West Washington Street I P.O

Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Performed as Special Assistant Auditors for the Auditor General, State of Illinois Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Table of Contents Schedule Page(s) System Officials 1 Management Assertion Letter 2 Compliance Report Summary 3 Independent Accountant’s Report on State Compliance, on Internal Control over Compliance, and on Supplementary Information for State Compliance Purposes 4 Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 8 Schedule of Findings Current Findings – State Compliance 10 Supplementary Information for State Compliance Purposes Fiscal Schedules and Analysis Schedule of Appropriations, Expenditures and Lapsed Balances 1 13 Comparative Schedules of Net Appropriations, Expenditures and Lapsed Balances 2 15 Comparative Schedule of Revenues and Expenses 3 17 Schedule of Administrative Expenses 4 18 Schedule of Changes in Property and Equipment 5 19 Schedule of Investment Portfolio 6 20 Schedule of Investment Manager and Custodian Fees 7 21 Analysis of Operations (Unaudited) Analysis of Operations (Functions and Planning) 30 Progress in Funding the System 34 Analysis of Significant Variations in Revenues and Expenses 36 Analysis of Significant Variations in Administrative Expenses 37 Analysis -

2021 Annual General Meeting and Proxy Statement 2020 Annual Report

2020 Annual Report and Proxyand Statement 2021 Annual General Meeting Meeting General Annual 2021 Transocean Ltd. • 2021 ANNUAL GENERAL MEETING AND PROXY STATEMENT • 2020 ANNUAL REPORT CONTENTS LETTER TO SHAREHOLDERS NOTICE OF 2021 ANNUAL GENERAL MEETING AND PROXY STATEMENT COMPENSATION REPORT 2020 ANNUAL REPORT TO SHAREHOLDERS ABOUT TRANSOCEAN LTD. Transocean is a leading international provider of offshore contract drilling services for oil and gas wells. The company specializes in technically demanding sectors of the global offshore drilling business with a particular focus on ultra-deepwater and harsh environment drilling services, and operates one of the most versatile offshore drilling fleets in the world. Transocean owns or has partial ownership interests in, and operates a fleet of 37 mobile offshore drilling units consisting of 27 ultra-deepwater floaters and 10 harsh environment floaters. In addition, Transocean is constructing two ultra-deepwater drillships. Our shares are traded on the New York Stock Exchange under the symbol RIG. OUR GLOBAL MARKET PRESENCE Ultra-Deepwater 27 Harsh Environment 10 The symbols in the map above represent the company’s global market presence as of the February 12, 2021 Fleet Status Report. ABOUT THE COVER The front cover features two of our crewmembers onboard the Deepwater Conqueror in the Gulf of Mexico and was taken prior to the COVID-19 pandemic. During the pandemic, our priorities remain keeping our employees, customers, contractors and their families healthy and safe, and delivering incident-free operations to our customers worldwide. FORWARD-LOOKING STATEMENTS Any statements included in this Proxy Statement and 2020 Annual Report that are not historical facts, including, without limitation, statements regarding future market trends and results of operations are forward-looking statements within the meaning of applicable securities law. -

Aker BP Acquires Licence Portfolio from Total

Aker BP acquires licence portfolio from Total Aker BP has entered into an agreement with Total E&P Norge to acquire its interests in a portfolio of 11 licences on the Norwegian Continental Shelf for a cash consideration of USD 205 million. The portfolio includes four discoveries with net recoverable resources of 83 million barrels oil equivalents ("mmboe"), based on estimates from the Norwegian Petroleum Directorate. Two of the discoveries, Trell and Trine, are located near the Aker BP-operated Alvheim field and are expected to be produced through the Alvheim FPSO. The Alve Nord discovery is located north of the Aker BP-operated Skarv field, and can be produced through the Skarv FPSO. The Rind discovery is part of the NOAKA area where the total recoverable resources are estimated to more than 500 mmboe, and where Aker BP is working towards a new area development. In addition to these discoveries, the transaction also provides the company with increased interest in exploration acreage near the Aker BP-operated Ula field. The transaction is subject to approval by Norwegian authorities. Karl Johnny Hersvik, CEO of Aker BP comments: “We see a huge value creation potential in maximizing production through our operated production hubs. This requires continuous development and optimisation of the existing reserves and resources, as well as adding new resources through exploration and acquisitions of existing discoveries. With this transaction, we get access to new tie-back opportunities in the Alvheim and Skarv areas, we strengthen our resource base in the NOAKA area, and we increase our interest in exploration acreage near the Ula field. -

Arctic Norwegian Value Creation Monthly Report July 2021

Arctic Norwegian Value Creation Monthly Report July 2021 FUND COMMENTS Arctic orwegianN Value Creation (Class B) increased by 3.0% in July. Since inception in August 2014, the fund has returned 139.5% compared to a return of 97,2% for the Norwegian OSEFX benchmark. The largest positive contributors to fund performance in July were Borregaard, Kongsberg and Schibsted. Borregaard reported good second quarter results with underlying profits up 23% year-over-year driven by high price realisations and contained costs within its BioSolutions segment. Moreover, Borregaard announced that it will invest NOK 144 million in two transactions to acquire 25% of Alginor, with a further intention to increase its ownership to 35%. Alginor is Norwegian marine biotech and biomaterials company based in Haugesund which is developing a biorefinery concept based on harvested kelp. The intention is to list Alginor on the stock exchange during the next few months. Kongsberg delivered another strong report with a 62% increase in operating profit year-over-year. Following four quarters of declining revenues, Kongsberg Maritime returned to growth while posting a book to bill ratio above one. Kongsberg’s defence segment reported strong profitability and revenue growth of 22%. Early in July, Kongsberg was awarded defence contracts for NOK 8.2 billion by Germany and Norway to deliver submarine combat systems and naval strike missiles. Schibsted reported a strong Q2 with year- on-year growth in sales and EBITDA of 18% and 49% respectively, clearly ahead of analyst estimates. Nordic Marketplaces and News Media showed particularly strong improvements. For the first quarter ever, Nordic Marketplaces reached more than NOK 1 bn in sales with an impressive EBITDA-margin of 47%, with Finn as the main contributor. -

Annual Report 2020 Contents

ANNUAL REPORT 2020 CONTENTS LETTER FROM THE CEO 4 BOARD OF DIRECTORS 44 KEY FIGURES 2020 8 EXECUTIVE MANAGEMENT TEAM 48 HIGHLIGHTS 2020 10 BOARD OF DIRECTORS’ REPORT 52 THE VALHALL AREA 16 REPORTING OF PAYMENTS TO GOVERNMETS 72 IVAR AASEN 20 BOD’S REPORT ON CORPORATE GOVERNANCE 74 THE SKARV AREA 24 FINANCIAL STATEMENTS WITH NOTES 88 THE ULA AREA 28 THE ALVHEIM AREA 32 JOHAN SVERDRUP 36 THE NOAKA AREA 40 COMPANY PROFILE Aker BP is an independent exploration and production Aker BP is headquartered at Fornebu outside Oslo and has company conducting exploration, development and produ- offices in Stavanger, Trondheim, Harstad and Sandnessjøen. ction activities on the Norwegian continental shelf (NCS). Aker BP ASA is owned by Aker ASA (40%), bp p.l.c. (30%) Measured in production, Aker BP is one of the largest and other shareholders (30%). independent oil and gas companies in Europe. Aker BP is the operator of Alvheim, Ivar Aasen, Skarv, Valhall, Hod, Ula The company is listed on the Oslo Stock Exchange with and Tambar, a partner in the Johan Sverdrup field and holds ticker “AKRBP”. a total of 135 licences, including non-operated licences. As of 2020, all the company’s assets and activities are based in Norway and within the Norwegian offshore tax regime. OUR ASSETS arstad AND OFFICES andnessen ar Trondei lei orne taaner ar asen oan erdrp operated inor laTaar alallod · ESG IN AKER BP SUSTAINABILITY REPORT 2020 Aker BP’s Sustainability report 2020 describes the ESG in Aker BP company’s management approach and performance to environment, social and governance. -

Empirical Inference of Related Trading Between Two Securities: Detecting Pairs Trading, Merger Arbitrage, and Strategy Rules*

Empirical inference of related trading between two securities: Detecting pairs trading, merger arbitrage, and strategy rules* Keith Godfrey The University of Western Australia Working paper: 5 September 2013 The traditional approach to studying pairs trading is to simulate profitability using ex-post historical prices. I study the actual trades reported anonymously in security pairs and build statistical inferences of related trading. The approach is based on the time differences between trades. It can distinguish intrinsically related securities from pseudo-random sets, find stocks involved in merger arbitrage in massive sets of paired index constituents, and infer dominant trading rules of mean reversion algorithms. Empirical inference of related trading can enable further studies into pairs trading, strategy rules, merger arbitrage, and insider trading. Keywords: Inferred trading, empirical inference, pairs trading, merger arbitrage. JEL Classification Codes: G00, G10, C10, C40, C60 The availability of intraday trading or “tick” data with time resolution of a millisecond or finer is opening many avenues of research into financial markets. Analysis of two or more streams of tick data concurrently is becoming increasingly important in the study of multiple-security trading including index tracking, pairs trading, merger arbitrage, and market-neutral strategies. One of the greatest challenges in empirical trading research is the anonymity of reported trades. Securities exchanges report the dates, times, prices, and volumes traded, without identifying the traders. In studies of a single security, this introduces uncertainty of whether each market order that caused a trade was the buy or sell order, and there are documented approaches of inference such as Lee and Ready (1991). -

To Arrive at the Total Scores, Each Company Is Marked out of 10 Across

BRITAIN’S MOST ADMIRED COMPANIES THE RESULTS 17th last year as it continues to do well in the growing LNG business, especially in Australia and Brazil. Veteran chief executive Frank Chapman is due to step down in the new year, and in October a row about overstated reserves hit the share price. Some pundits To arrive at the total scores, each company is reckon BG could become a take over target as a result. The biggest climber in the top 10 this year is marked out of 10 across nine criteria, such as quality Petrofac, up to fifth from 68th last year. The oilfield of management, value as a long-term investment, services group may not be as well known as some, but it is doing great business all the same. Its boss, Syrian- financial soundness and capacity to innovate. Here born Ayman Asfari, is one of the growing band of are the top 10 firms by these individual measures wealthy foreign entrepreneurs who choose to make London their operating base and home, to the benefit of both the Exchequer and the employment figures. In fourth place is Rolls-Royce, one of BMAC’s most Financial value as a long-term community and environmental soundness investment responsibility consistent high performers. Hardly a year goes past that it does not feature in the upper reaches of our table, 1= Rightmove 9.00 1 Diageo 8.61 1 Co-operative Bank 8.00 and it has topped its sector – aero and defence engi- 1= Rotork 9.00 2 Berkeley Group 8.40 2 BASF (UK & Ireland) 7.61 neering – for a decade. -

Preparing for Carbon Pricing: Case Studies from Company Experience

TECHNICAL NOTE 9 | JANUARY 2015 Preparing for Carbon Pricing Case Studies from Company Experience: Royal Dutch Shell, Rio Tinto, and Pacific Gas and Electric Company Acknowledgments and Methodology This Technical Note was prepared for the PMR Secretariat by Janet Peace, Tim Juliani, Anthony Mansell, and Jason Ye (Center for Climate and Energy Solutions—C2ES), with input and supervision from Pierre Guigon and Sarah Moyer (PMR Secretariat). The note comprises case studies with three companies: Royal Dutch Shell, Rio Tinto, and Pacific Gas and Electric Company (PG&E). All three have operated in jurisdictions where carbon emissions are regulated. This note captures their experiences and lessons learned preparing for and operating under policies that price carbon emissions. The following information sources were used during the research for these case studies: 1. Interviews conducted between February and October 2014 with current and former employees who had first-hand knowledge of these companies’ activities related to preparing for and operating under carbon pricing regulation. 2. Publicly available resources, including corporate sustainability reports, annual reports, and Carbon Disclosure Project responses. 3. Internal company review of the draft case studies. 4. C2ES’s history of engagement with corporations on carbon pricing policies. Early insights from this research were presented at a business-government dialogue co-hosted by the PMR, the International Finance Corporation, and the Business-PMR of the International Emissions Trading Association (IETA) in Cologne, Germany, in May 2014. Feedback from that event has also been incorporated into the final version. We would like to acknowledge experts at Royal Dutch Shell, Rio Tinto, and Pacific Gas and Electric Company (PG&E)—among whom Laurel Green, David Hone, Sue Lacey and Neil Marshman—for their collaboration and for sharing insights during the preparation of the report. -

Ellertsen Andre.Pdf (1.975Mb)

UIS BUSINESS SCHOOL MASTER’S THESIS STUDY PROGRAM: THESIS IS WRITTEN IN THE FOLLOWING SPECIALIZATION/SUBJECT: Business Administration – Master of Science Applied Finance IS THE ASSIGNMENT CONFIDENTIAL? The assignment is not confidential (NB! Use the red form for confidential theses) TITLE: Valuation of Aker BP ASA AUTHOR(S) SUPERVISOR: Bernt Arne Ødegaard Candidate number: Name: 3091 André Ellertsen 1 Executive summary The valuation will determine the fair value of Aker BP’s equity as of January 1st, 2020, using a fundamental approach. In addition, relative valuation will be included as a supplement. The valuation is done as of January 1st because of the ongoing COVID-19 pandemic, which has influenced multiple aspects of the global markets, like oil prices, demands and interest rates. The first part of this thesis consists of an introduction of the company and its surrounding environment. Further follows relevant theory of valuation, and an explanation for choice of method. Next a strategic analysis of the company’s internal and external environment is conducted to reveal the company’s level of competitiveness. Further in the thesis the company’s financial statements are presented and explained, and a risk analysis is conducted to uncover potential short-term or long-term payment failure. Next, Future cashflows are estimated based on findings from the strategic analysis and presented along with a justification. Based on the future cashflows, and estimated WACC, a fundamental valuation is done to estimate the value of Aker BP ASA. Lastly, the valuation is combined with a value estimated from a comparative valuation approach, and a brief conclusion is given. -

Maersk Drilling Fleet Status Report

Maersk Drilling Fleet Status Report 20 November 2020 Changes to Fleet Status Report Fleet Status Report, 20 November 2020 | p. 2 Commercial activity in Q3 2020: Maersk Integrator Awarded one-well contract with Aker BP in Norway in direct continuation of the rig’s current work scope with an estimated duration of 73 days. The contract is expected to commence in February 2021 and has a firm value of approximately USD 18.5m, excluding integrated services provided and a potential performance bonus.(1) Maersk Resilient Maersk Drilling has agreed with Serica Energy UK to defer the commencement of the drilling programme under the rig’s original contract to a window between March and July 2021.(1) Maersk Integrator Awarded one-well contract with Aker BP in Norway in direct continuation of the rig’s current work scope with an estimated duration of 85 days. The contract is expected to commence in April 2021 and has a firm value of approximately USD 21.6m, excluding integrated services provided and a potential performance bonus. Maersk Convincer Awarded extension with Brunei Shell Petroleum Company Sdn. Bhd. offshore Brunei Darussalam in direct continuation of the rig’s current work scope with an estimated duration of 602 days. The extension is expected to commence in May 2021 and has a firm value of approximately USD 47m, excluding a potential performance bonus. Maersk Resilient/ Maersk Drilling and Dana Petroleum Denmark B.V. have agreed to defer the previously announced one-well contract in the Danish sector of the North Sea which was originally expected to commence in May 2020. -

BP Plc Vs Royal Dutch Shell

FEBRUARY 2021 BP plc Vs Royal Dutch Shell 01872 229 000 www.atlanticmarkets.co.uk www.atlanticmarkets.co.uk BP Plc A Brief History BP is a British multinational oil and gas company headquartered in London. It is one of the world’s oil and gas supermajors. · 1908. The founding of the Anglo-Persian Oil Company, established as a subsidiary of Burmah Oil Company to take advantage of oil discoveries in Iran. · 1935. It became the Anglo-Iranian Oil Company · 1954. Adopted the name British Petroleum. · 1959. The company expanded beyond the Middle East to Alaska and it was one of the first companies to strike oil in the North Sea. · 1978. British Petroleum acquired majority control of Standard Oil of Ohio. Formerly majority state-owned. · 1979–1987. The British government privatised the company in stages between. · 1998. British Petroleum merged with Amoco, becoming BP Amoco plc, · 2000-2001. Acquired ARCO and Burmah Castrol, becoming BP plc. · 2003–2013. BP was a partner in the TNK-BP joint venture in Russia. Positioning BP is a “vertically integrated” company, meaning it’s involved in the whole supply chain – from discovering oil, producing it, refining it, shipping it, trading it and selling it at the petrol pump. BP has operations in nearly 80 countries worldwide and has around 18,700 service stations worldwide. Its largest division is BP America. In Russia, BP also own a 19.75% stake in Rosneft, the world’s largest publicly traded oil and gas company by hydrocarbon reserves and production. BP has a primary listing on the London Stock Exchange and is a constituent of the FTSE 100 Index. -

Global Proxy Voting Records

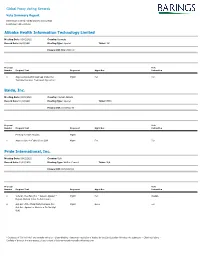

Global Proxy Voting Records Vote Summary Report Date range covered: 03/01/2021 to 03/31/2021 Location(s): All Locations Alibaba Health Information Technology Limited Meeting Date: 03/01/2021 Country: Bermuda Record Date: 02/23/2021 Meeting Type: Special Ticker: 241 Primary ISIN: BMG0171K1018 Proposal Vote Number Proposal Text Proponent Mgmt Rec Instruction 1 Approve Revised Annual Cap Under the Mgmt For For Technical Services Framework Agreement Baidu, Inc. Meeting Date: 03/01/2021 Country: Cayman Islands Record Date: 01/28/2021 Meeting Type: Special Ticker: BIDU Primary ISIN: US0567521085 Proposal Vote Number Proposal Text Proponent Mgmt Rec Instruction Meeting for ADR Holders Mgmt 1 Approve One-to-Eighty Stock Split Mgmt For For Pride International, Inc. Meeting Date: 03/01/2021 Country: USA Record Date: 12/01/2020 Meeting Type: Written Consent Ticker: N/A Primary ISIN: US74153QAJ13 Proposal Vote Number Proposal Text Proponent Mgmt Rec Instruction 1 Vote On The Plan (For = Accept, Against = Mgmt For Abstain Reject; Abstain Votes Do Not Count) 2 Opt Out of the Third-Party Releases (For = Mgmt None For Opt Out, Against or Abstain = Do Not Opt Out) * Instances of "Do Not Vote" are normally owing to: - Share-blocking - temporary restriction of trading by the Sub-Custodian following vote submission - Client restrictions - Conflicts of Interest. For any queries, please contact [email protected] Global Proxy Voting Records Vote Summary Report Date range covered: 03/01/2021 to 03/31/2021 Location(s): All Locations The