How Does Family Control Influence a Firm's Acquisition and Divestiture

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Work in Progress (1999.03.07)

_________________________________________________________________ WORK IN PROGRESS by Cliff Holden ______________________________ Hazelridge School of Painting Pl. 92 Langas 31193 Sweden www.cliffholden.co.uk copyright © CLIFF HOLDEN 2011 2 for Lisa 3 4 Contents Foreword 7 1 My Need to Paint 9 2 The Borough Group 13 3 The Stockholm Exhibition 28 4 Marstrand Designers 40 5 Serigraphy and Design 47 6 Relating to Clients 57 7 Cultural Exchange 70 8 Bomberg's Legacy 85 9 My Approach to Painting 97 10 Teaching and Practice 109 Joseph's Questions 132 5 6 Foreword “This is the commencement of a recording made by Cliff Holden on December 12, 1992. It is my birthday and I am 73 years old. ” It is now seven years since I made the first of the recordings which have been transcribed and edited to make the text of this book. I was persuaded to make these recordings by my friend, the art historian, Joseph Darracott. We had been friends for over forty years and finally I accepted that the project which he was proposing might be feasible and would be worth attempting. And so, in talking about my life as a painter, I applied myself to the discipline of working from a list of questions which had been prepared by Joseph. During our initial discussions about the book Joseph misunderstood my idea, which was to engage in a live dialogue with the cut and thrust of question and answer. The task of responding to questions which had been typed up in advance became much more difficult to deal with because an exercise such as this lacked the kind of stimulus which a live dialogue would have given to it. -

Transcript of Interview with Sir Roger Gifford

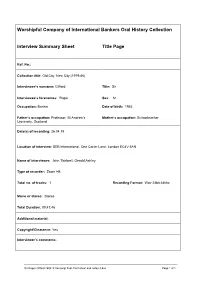

Worshipful Company of International Bankers Oral History Collection Interview Summary Sheet Title Page Ref. No.: Collection title: Old City, New City (1979-86) Interviewee’s surname: Gifford Title: Sir Interviewee’s forenames: Roger Sex: M Occupation: Banker Date of birth: 1955 Father’s occupation: Professor, St Andrew’s Mother’s occupation: Schoolteacher University, Scotland Date(s) of recording: 26.04.19 Location of interview: SEB International, One Carter Lane, London EC4V 5AN Name of interviewer: John Thirlwell, Gerald Ashley Type of recorder: Zoom H5 Total no. of tracks: 1 Recording Format: Wav 24bit 48khz Mono or stereo: Stereo Total Duration: 00:47:46 Additional material: Copyright/Clearance: Yes Interviewer’s comments: Sir Roger Gifford 260419 transcript final, front sheet and notes-3.doc Page 1 of 1 Introduction and biography #00:00:00# Graduate trainee at SG Warburg & Co Ltd; interviewed by #00:01:40# Siegmund Warburg #00:04:53# Banks’ graduate training schemes in the 1970’s i Move to Enskilda Securities (ES); ES’s ‘Big Bang’ structure; #00:06:38# relationship between ES and SEB and Wallenberg family Graduate training schemes in the 1970’s #00:10:15# Working in Enskilda Securities corporate finance #00:11:17# department Culture of the City – ‘the old school tie’; Americanisation of #00:12:38# the City - new capital, new structures Changes of business practice; conflicts of interest #00:19:32# Regulation by the Bank of England #00:21:26# Authorised banks and licensed deposit takers; funding and #00:23:07# growth of Enskilda Securities -

Annually Compounded Rate, 46–47 Annual Percentage Rate (APR

Index Note: Page numbers followed by n subprime mortgage crisis, 13, 168, Annually compounded rate, 46–47 indicate notes. 328–329, 355–356, 779–780 Annual percentage rate (APR), 35–38 transparency and, 861–862 Annuities, 28–33. See also Equivalent A Aggarwal, R., 307, 831n annual cost Aghion, P., 841n defined, 28 Aabar Investments, 853 AGL Resources Inc., 84 equivalent annual cash flow, Abandonment option, 254–256, 561–566 Agnblad, I., 856n 141–145 project life and, 564–565 Agrawal, D., 585n, 586n growing, 33–35 temporary, 565–566 AIG, 13, 355, 581 valuation of, 28–33 valuation of, 562–564 Airbus, 253, 567–569, 568n annual mortgage payments, 31–32 ABB, 856, 857 Aivasian, V., 462n annuities due, 31–32 Abnormal return, 318–319 Alcan, 793 future value, 32–33 Absolute priority, 451–452 Alcoa, 806 growing annuities, 33–35 Accelerated depreciation, 136–138, 139 Allayanis, G., 697 installment plan costing, 30 Accelerated underwritings, 377n Allen, Franklin, 163, 226n, 242, 329n, lottery winnings, 30–31 Accenture, 129 358, 409n, 410n, 412, 747–748, Anthony, R., 300n Accounting income, tax income 846n, 860n, 864, 869, 871n, 875n Antikarov, R. S., 572 versus, 137–138 Allen, J., 844 Antitrust law, mergers and, 805–806 Accounting rates of return, 711–713 Allen, L., 594 Aoki, M., 852n nature of, 711–712 Alliant, 834 AOL, 335, 793, 828 problems with, 712–713 Allied Crude Vegetable Oil Refining A&P, 681 Accounting standards, 705 Corporation, 780 Apex One, 793 Accounts payable, 134–135, 738, 740 Allman-Ward, M., 784 Apollo Management, 823 Accounts receivable, 134–135, Allocated overhead, in net present Apple Computer Inc., 369n, 555 733, 737–738, 757 value analysis, 131 Appropriation requests, 241–242 Accrued interest, 600 Alltel, 793 Aramark, 367 Acharya, V. -

Highlights May J U N E /J U

m is “Honoring Tradition, Celebrating Diversity, and Building a Jewish Future” da U form J Re on for I Un E h t r of hIghlIghts be m E Thursday, May 3 at 7:30 pm—PErspectIves on ISraEl. First of a series on Israel and its challenges from viewpoints across the political spectrum. a m This presentation is by Matthew Gabe, AIPAC East Bay Director. See Page 8. is Sunday, May 6 at 10:00 am—annUal MeetIng of thE CongrEgatIon. th El E This event will include election of new officers for the Beth El Board B and a review of the synagogue’s finances. See Page 6 for more details. on I gat Friday, May 11 at 6:15 pm (for appetizers)—CElebratIon of EducatIon honoring Beth El’s E B’nei Mitzvah class, Confirmation class and high school (Midrasha) graduates. Dinner at 6:30 pm with the Shabbat service at 7:30 pm. Join us in celebrating May our students as they lead us in prayer and share with us their insights and reflections. Congr Please sign up for dinner at: https://bethelyouthed.wufoo.com/forms/z7x2s9/ Sunday, May 20 at 10:15 am—MidraSha gradUatIon. Celebrate with the 15 high school students from eight different synagogues who will be graduating this year. For more details, see Page 17. Friday, June 1 at 8:00 pm--CommEmoratIon of thE 100th birthday of raoUl WallEnberg, as one of the Righteous Gentiles who saved a large number of Hungarian Jewish children, including our Emeritus Rabbi Raj, during the Holocaust. -

Statement of Terrence J. Collins

Statements in Support of Petition for Rulemaking Statement Exhibit (w/ Hyperlink) Statement of Terrence J. Collins ....................................................................................................... Exhibit A Statement of Miriam L. Diamond ..................................................................................................... Exhibit B Statement of David A. Eastmond ...................................................................................................... Exhibit C Statement of David Epel ................................................................................................................... Exhibit D Statement of Rolf Halden .................................................................................................................. Exhibit E Statement of Kim Harley ................................................................................................................... Exhibit F Statement of Julie Herbstman .......................................................................................................... Exhibit G Statement of Susan Kasper ............................................................................................................... Exhibit H Statement of Donald Lucas ................................................................................................................ Exhibit I Statement of Sharyle Patton .............................................................................................................. Exhibit J Statement -

Wallenberg Sphere and Samsung Group Hwa-Jin Kim University of Michigan Law School, [email protected]

University of Michigan Law School University of Michigan Law School Scholarship Repository Articles Faculty Scholarship 2014 Concentrated Ownership and Corporate Control: Wallenberg Sphere and Samsung Group Hwa-Jin Kim University of Michigan Law School, [email protected] Available at: https://repository.law.umich.edu/articles/1763 Follow this and additional works at: https://repository.law.umich.edu/articles Part of the Business Organizations Law Commons, Comparative and Foreign Law Commons, and the Law and Economics Commons Recommended Citation Kim, Hwa-Jin. "Concentrated Ownership and Corporate Control: Wallenberg Sphere and Samsung Group." J. Korean L. 14, no. 1 (2014): 39-59. This Article is brought to you for free and open access by the Faculty Scholarship at University of Michigan Law School Scholarship Repository. It has been accepted for inclusion in Articles by an authorized administrator of University of Michigan Law School Scholarship Repository. For more information, please contact [email protected]. Journal of Korean Law | Vol. 14, 39-59, December 2014 Concentrated Ownership and Corporate Control: Wallenberg Sphere and Samsung Group* Hwa-Jin Kim** Abstract Samsung Group’s success cannot be attributed to its corporate governance structure, at least thus far. The corporate governance of Samsung has been rather controversial. As the group faces the succession issue the corporate governance has become as crucial as their new products and services. Samsung has discovered a role model on the other side of the planet, Wallenberg Sphere in Sweden. Much effort has been made to learn about Wallenberg’s arrangements and key to its success. However, a fundamental difference between the institutions in Sweden and Korea has made the corporate structures of the two groups radically different. -

Raoul Wallenberg a Story of Courage and Resistance During the Holocaust

Raoul Wallenberg A Story of Courage and Resistance During the Holocaust “We’re fighting … and that’s the main thing” ymark w photo: Ewa Memorial stone in Gothenburg of Raoul Wallenberg by the artist Charlotte Gyllenhammar. The monument was unveiled in 2007. In 1944, Raoul Wallenberg saved and protected thousands of Jews in Budapest from abuse at the hands of the Nazis and members of the Hungarian Arrow Cross Party. People throughout the world know about his efforts. He is an honorary citizen of three countries. Monuments in his honour have been built in many cities. Schools, squares and buildings bear the Wallenberg name. The memory of his historical deeds lives on in books, music and film. raoul Wallenberg For Ching sear To: Timony and pho Tes e VaT pri To: “My brother Gustav was an errand boy at Raoul Wallenberg’s office. He got the job since my family had business contacts yad Vashem | pho Timony: Tes were attacking our house, a so-called Swedish Kate (now Wacz), 12 years old, and her brother “One night when the Arrow Cross soldiers seriously wounded but, as luck would have it, in Sweden. Mother, I and my brother all received I was taken care of andsafe received house, treatment I was struck in by a bullet. I was Esther Schlesinger, 7 years old. Gustav Kadelburger, 15 years old. under the protection of “We lived in a house the Swedish Embassy” protective passports.” the ghetto.” raoul wallenberg my mother, father and brothers lived. All the Jews were chased out into Danube River where they were murdered. -

Power Politics and the Empire of Economics: an Introduction

Power Politics and the Empire of Economics: An Introduction By: Andrew Gavin Marshall The President sat and listened to his closest adviser as they plotted a strategy to maintain Western domination of the world economy. The challenge was immense: divisions between industrial countries were growing as the poor nations of the world were becoming increasingly united in opposition to the Western world order. From Africa, across the Middle East, to Asia and Latin America, the poor (or ‘developing’) countries were calling for the establishment of a ‘New International Economic Order,’ one which would not simply serve the interests of the United States, Western Europe, and the other rich, industrial nations, but the world as a whole. It was on the 24th of May 1975 when President Gerald Ford was meeting with his Secretary of State and National Security Adviser, Henry Kissinger, easily the two most powerful political officials in the world at the time. Kissinger told the President: “The trick in the world now is to use economics to build a world political structure.”1 Ford and Kissinger agreed that the United States could not accept a new ‘economic order’ that would undermine American and Western power throughout the world. Uprisings, revolutions and liberation movements across Africa, Asia and beyond had largely thrown off the shackles of European colonial domination, establishing themselves as independent political nation-states with their own interests and objectives. Chief among those goals was for economic independence to follow political independence, to take control of their own resources and economies from the Europeans and Americans, to determine their own economic policies and help to redistribute global wealth along equal and just lines. -

The Swedish Wallenberg Family – Most Organized and Criminal Gang in the World | Wallenbergfraud 2013-06-06

The Swedish Wallenberg family – Most organized and criminal gang in the world | wallenbergfraud 2013-06-06 wallenbergfraud Home Kjell Stigsson Bornerheim (police officer/UN-soldier) – Assassin for the Swedish government Lukas Lundin – Ian Lundin – Lundin Oil/Petroleum – Criminals connected to Wallenberg Mafia family Swedish Criminal Bernadotte family – Weapon & Opium Business – Connected to Wallenberg Criminals ← Polis Ingrid Michel vägrar att lämna ut allmänna Madeleine Jerand – Patrick Aschenbach – Carl Grevelius – Search handlingar (förhör med poliser) Tingsrättsdomare Nils Hedström – Dokusåpa → Recent Posts The Swedish Wallenberg family – Most organized and Säg hej till Lars-Jonney criminal gang in the world Jonsson/Trafikpolisen Östergötl and Posted on March 27, 2012 Lars-Jonney Jonsson – Trafikpolisen Östergötland Trafikpolisen i Östergötland är och köper korv Poliser Ingeborg Karlsson och Daniel Fernström i Karlstad har inga pungkulor att gripa heroin-baron Fredrik Reinfeldt Poliser Ingeborg Karlsson och Daniel Fernström i Karlstad har inga pungkulor att gripa heroin-baron Fredrik Reinfeldt Archives March 2013 February 2013 January 2013 December 2012 November 2012 October 2012 September 2012 August 2012 July 2012 June 2012 May 2012 April 2012 March 2012 February 2012 January 2012 December 2011 November 2011 October 2011 September 2011 August 2011 July 2011 June 2011 May 2011 April 2011 March 2011 February 2011 September 2010 July 2008 Categories http://www.blogger.com/img/ The Swedish Wallenberg family has managed to fool the world to believe that Raoul blank.gif Wallenberg was saving lives during second world war. Raoul Wallenberg was only doing the Uncategorized http://wallenbergfraud.wordpress.com/2012/03/27/the-swedish-wallenberg-family-most-organized-and-criminal-gang-in-the-world/ 1 / 5 The Swedish Wallenberg family – Most organized and criminal gang in the world | wallenbergfraud 2013-06-06 same thing his brothers and sisters was and still are doing… killing and robbing poor people. -

Guide to Western Intelligence During the Holocaust

Series IV Volume 9 Eavesdropping on Hell: Historical Guide to Western Communications Intelligence and the Holocaust, 1939-1945 UNITED STATES CRYPTOLOGIC HISTORY Eavesdropping on Hell: Historical Guide to Western Communications Intelligence and the Holocaust, 1939-1945 Robert J. Hanyok CENTER FOR CRYPTOLOGIC HISTORY NATIONAL SECURITY AGENCY 2004 Table of Contents Page Table of Contents . .iii Preface and Acknowledgments . .1 A Note on Terminology . 5 Acknowledgments . 7 Chapter 1: Background . .11 The Context of European and Nazi Anti-Semitism . .11 Previous Histories and Articles . .14 Chapter 2: Overview of the Western Communications Intelligence System during World War II . 21 Step 1: Setting the Requirements, Priorities, and Division of Effort . .24 Step 2: Intercepting the Messages . .29 Step 3: Processing the Intercept . .36 Step 4: Disseminating the COMINT . .43 From Intercept to Decryption the Processing of a German Police Message . .51 Chapter 3: Sources of Cryptologic Records Relating to the Holocaust . .61 The National Archives and Records Administration . .61 The Public Record Office . .67 Miscellaneous Collections . .71 Chapter 4: Selected Topics from the Holocaust . .75 A. The General Course of the Holocaust and Allied COMINT . .76 B. Jewish Refugees, the Holocaust, and the Growing Strife in Palestine . .86 C. The Vichy Regime and the Jews . .89 D. The Destruction of Hungarys Jews, 1944 . .99 E. Japan and the Jews in the Far East . .97 F. Nazi Gold: National and Personal Assests Looted by Nazis and Placed in Swiss Banks, 1943 - 1945 . .104 Chapter 5: Some Observations about Western Communications Intelligence and the Holocaust . .. .121 What was Known from COMINT . .122 When the COMINT Agencies Knew . -

The Freeman 1996

THEFREEMAN IDEAS ON LIBERTY FEATURES 716 SimEconomics by Lawrence H. White Computer simulations that let you run a whole society misrepresent how real societies work. 719 Salvation Through the Internet? by Donald J. Boudreaux A communications network even more amazing than the Internet: the price system. 721 Home, Home on the Internet by Thomas Boustead Good fences make good markets. 726 Liberty and the Domain of Self-Interest by Steven Horwitz Does society work better or worse when self-interest is given freer reign? 731 The Social Function of Mr. Henry Ford by Spencer Heath The role ofthe business owner explained, in a 1937 letter to journalist Dorothy Thompson. 734 Red-Lining the Federal Government Budget by Richard H. Timberlake A different strategy for fiscal control. 739 Law Enforcement by Deceit?: Entrapment and Due Process by Jennifer Johnson Dubious investigative tactics threaten individual rights. 742 Why Not Slavery? by Bertel M Sparks Why shouldn't people be permitted to own people? 747 Ending Tax Socialism by James A. Dorn Progressive taxation is unfair and unsafe. 749 For Appearance's Sake by James D. Saltzman Private property versus "beautification" busybodies. 754 Our Most Precious Resource by Earl Zarbin Children are individuals-not the "resource" of either the parents or the state. 755 Externalities and the Environment by Andrea Santoriello and Walter Block Trash, trees, and trade. 757 Raoul Wallenberg, Great Angel of Rescue by Jim Powell The man who defied Hitler and Stalin, and saved almost 100,000 lives. COLUMNS Center NOTES from FEE-Sweatshops for the New World Order by Hans E Sennholz 724 IDEAS and CONSEQUENCES-The Electric Car Seduction by Lawrence W Reed 736 POTOMAC PRINCIPLES-Killing Enterprise by Doug Bandow 767 ECONOMICS on TRIAL-Single Policy Change-Double Economic Growth? by Mark Skousen DEPARTMENTS 714 Perspective-William Leggett, Dave Ross, J. -

A Great Home for Great Companies an Introduction to Patricia Industries Contents

A great home for great companies An introduction to Patricia Industries Contents 4 About us 6 Ownership & governance 8 Business model 10 Milestones 12 About our companies Aleris BraunAbility LABORIE Mölnlycke Health Care Permobil The Grand Group Vectura 3 Scandinavia Financial Investments 28 Our team 2 We build companies for the long term At Patricia Industries, we are building a group of companies with services, takes time. Therefore, we do not want to be limited by long-term growth potential. Our job is to be a committed owner a timeframe, and consequently, our ownership horizon is helping great companies realize their full potential. forever. Exits are not a part of our strategy – we plan to keep our companies indefinitely. That said, we also need to be relentless The Wallenberg sphere today centers around ten non-profit in managing near-term performance – the long-term consists of foundations – the Wallenberg Foundations – and two industrial many short-terms. holding companies – Investor AB and FAM – that hold significant ownership interest in some of Scandinavia’s largest and most Our companies are diverse and therefore face very different important blue chip corporations including ABB, AstraZeneca, challenges. Accordingly, our working model is based on treating Atlas Copco, Electrolux, Ericsson, Husqvarna, Saab AB, SAS, SEB, each company individually and independently. We base our SKF, Sobi, Stora Enso and Wärtsilä as well as US based Nasdaq. ownership philosophy on the Swedish model of corporate governance – which means that, as owners, we focus on Patricia Industries is responsible for the wholly-owned, private appointing the right board for each company.