Tax Treaty Policy Consultation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Memorable Dublin Houses

MEMORABLE DUBLIN HOUSES BY WIL MOT HAR RISON A HANDY AND DESCR IPTIVE GUI DE WITH TH IRTY - SEVEN I LLUSTRATIONS Printed and Pu blis hed by EC KI E C O 59 BOLT ON STR EET D UBLIN W . L , M CMI& C ON T E N T S . — — U . Trinit o e e RO TE I y C ll g Coll ege Green Dame Street — Cas e ee P ame ee — — tl Str t arli nt Str t Es sex Quay Exchange ee — o d d d — Str t L r E war Street Chris tchurch Place—Corn — ma e d e eet—Thom s — ’ rk t Bri g Str a Street Usher s Quay ’ sh e s Is — A u U r land rran Q ay pp. 1 to 20 OU — — . f o ree R TE II Gra t n St t Pitt Street William Street — Aun gi er ee o de e — o — Str t G l n Lan Y rk Street Digger; eet— Cu ffe ee — ' St. e h — Str Str t St p en s Green Harco urt Street 2 1 pp. to 4 8 O — UT I I I . Daws on ee K R E Str t Molesworth Street— ildar — e ee Lein ste1 ee —C a e — Str t Str t l r Street Merrio n Square~ — H ollee e e Denzille h ee — Str t S t Lower Mou nt Street e c ace— y ppe M ou n ee Me P r Pl U r t Str t rrion S quare — ppe Me on ee El P ce— o e U r rri Str t y la L w r Baggo t Street i w am S u ~ — F q are Lees on S ee Ch em tz illi tr t arl ont Plac e be — Porto llo H arbour Rathmines Road pp . -

M E R R I O N R O W D U B L I

MERRION ROW DUBLIN 2 Prime offices to let in Dublin’s most sought after location. 3 Description 2-4 Merrion Row offers occupiers a rare opportunity to locate in Dublin’s vibrant city centre. The building has been extensively refurbished throughout to provide stylish, high quality workspace over four floors, extending to a total NIA of 1,044.05 sq.m. (11,238 sq.ft.). Occupiers will benefit from the exceptional new open plan accommodation, completed to full third generation specification. A bright, contemporary reception with featured glass entrance sets the tone for the quality of finish delivered throughout. 4 5 Location Facebook Capita Google William Fry Accenture Bord Gáis Merrion Row, located in the Shire Pharmaceuticals Merrion Square hub of Dublin’s Business National Gallery ESB Headquarters Community, adjacent to of Ireland Government Natural History Buildings Government buildings and Museum National Library Trinity College The Merrion Hotel minutes from many well National Museum Fitzwilliam Square of Ireland established occupiers. Hudson Advisors Shelbourne Hotel Emirates The area is already home to many Intercom Aralez Pharmaceuticals leading occupiers across all sectors, Davy Stockbrokers including financial services, technology, MERRION Permanent TSB ROW media, insurance and banking. A sample AerCap of neighbouring occupiers includes The Conrad Hotel Hedgeserv Government Buildings, Shire Pharma, Grafton Street Stephen's Green St Stephen’s Green Intercom, AerCap, KPMG, PTSB, Emirates, Shopping Centre Maples & Calder The National Sky Aviation and Aralez Pharma. Department Concert Hall The Fitzwilliam Hotel The Gaiety Theatre of Foreign Affairs 2 – 4 Merrion Row benefits from Royal College Standard Life Ireland unrivalled access to public transport and Qualtrics Ireland of Surgeons of Ireland an excellent choice of amenities on the Indeed Sky Aviation doorstep, including St. -

The Building of the State the Buildingucd and the Royal College of Scienceof on Merrionthe Street

The Building of the State The BuildingUCD and the Royal College of Scienceof on Merrionthe Street. State UCD and the Royal College of Science on Merrion Street. The Building of the State Science and Engineering with Government on Merrion Street www.ucd.ie/merrionstreet Introduction Although the Government Buildings complex on Merrion Street is one of most important and most widely recognised buildings in Ireland, relatively few are aware of its role in the history of science and technology in the country. At the start of 2011, in preparation for the centenary of the opening of the building, UCD initiated a project seeking to research and record that role. As the work progressed, it became apparent that the story of science and engineering in the building from 1911 to 1989 mirrored in many ways the story of the country over that time, reflecting and supporting national priorities through world wars, the creation of an independent state and the development of a technology sector known and respected throughout the world. All those who worked or studied in the Royal College of Science for Ireland or UCD in Merrion Street – faculty and administrators, students and porters, technicians and librarians – played a part in this story. All those interviewed as part of this project recalled their days in the building with affection and pride. As chair of the committee that oversaw this project, and as a former Merrion Street student, I am delighted to present this publication as a record of UCD’s association with this great building. Professor Orla Feely University College Dublin Published by University College Dublin, 2011. -

Micheál Martin T.D. an Taoiseach Government Buildings Upper Merrion Street Dublin 2

Micheál Martin T.D. An Taoiseach Government Buildings Upper Merrion Street Dublin 2 1 September 2020 Re: Chambers Ireland Concerns regarding the EWSS and the co-ordination of the response to Covid-19 Dear Taoiseach, Chambers Ireland welcomes the early reconvening of the Dáil as there remain many policy areas which need the immediate attention of government. Since the Government’s July package was introduced circumstances for business have evolved and gaps have become apparent. Government needs to address the long-term nature of this pandemic with an appropriate suite of responses and the critical need to introduce a programme of structured interventions focused on regions which see restrictions reintroduced, and separately the sectors which are most acutely affected by the impact of Covid-19. Chamber Ireland Concerns: 1. There is a need for additional supports to help areas where restrictions have to be reintroduced to sustain businesses that are active in those areas, and then to support them upon reopening. 2. There are failings in the Employment Wage Subsidy Scheme which need to be addressed urgently. 3. It is critical that there is a co-ordinated, coherent, and clear programme of policy and communications from government, the absence of which is undermining the viability of businesses and the sustainability of our economy. Government Action Required: There needs to be: 1. Specific tailored packages for businesses that are operating in areas where restrictions are reintroduced, and, 2. A review of: www.chambers.ie _____________________________________________ ________________________________________________________________________________________________________________________ 11 St Stephens Green, Dublin 2, D02 FY84 T. +353 (0) 400 4300 E. [email protected] @chambersireland Chambers Ireland is a registered business name of The Chambers of Commerce of Ireland CLG Registered Office: 11 St Stephens Green, Dublin 2, D02 FY84 Registered in Dublin Reg. -

Guide to the National Museum of Ireland Archaeology

Guide to the National Museum of Ireland Archaeology i Guide to the National Museum of Ireland Archaeology ii 1 Contents Introduction 4 The Building and its Collections 5 The Exhibitions 8 Prehistoric Ireland 8 °° Ór – Ireland's Gold 15 The Treasury 21 Viking Ireland 31 Medieval Ireland 1150–1550 37 Ancient Egypt 43 Ceramics and Glass from Ancient Cyprus 2500 B.C. – A.D. 300 46 Kingship & Sacrifice 48 Guide to the National Museum of Ireland – Archaeology © National Museum of Ireland, Dublin, 2007 ISBN: 978-0-901777-58-4 Text: Eamonn P. Kelly. With thanks to Raghnall Ó Floinn, Mary Cahill, Andy Halpin, Maeve Sikora, Stephen Quirke and John Taylor Photography: Valerie Dowling, Noreen O'Callaghan and John Searle All rights reserved. No part of this publication may be copied, reproduced, stored in a retrieval system, broadcast or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without prior permission in writing from the publishers. 2 3 Introduction The Building and its Collections The National Museum of Ireland was founded under the Dublin Science and Art Museum Act of 1877. Previously, the museum’s collections had been divided between Leinster House, originally the headquarters of the Royal Dublin Society, and the Natural History Museum in Merrion Street, built as an extension to Leinster House in 1856–7. Under the Act, the government purchased the museum buildings and collections. To provide storage and display space for the Leinster House collections, the government quickly implemented plans to construct a new, custom-built museum on Kildare Street and on 29th August 1890, the new museum opened its doors to the public. -

Brexit: Analysis of Import Exposures in an EU Context

Brexit: Analysis of Import Exposures in an EU Context March 2018 `` Page | 1 Brexit: Analysis of Import Exposures in an EU Context Department of Finance March 2018 Department of Finance Government Buildings, Upper Merrion Street, Dublin 2, Ireland Website: www.finance.gov.ie Page | 2 Contents Executive Summary ................................................................................................................................. 4 1. Introduction ........................................................................................................................................ 5 2. Data and Methodology ....................................................................................................................... 7 3. Irish Goods Exposures to the UK ......................................................................................................... 9 4. EU-27 Goods Exposures to the UK .................................................................................................... 16 5. Conclusion ......................................................................................................................................... 27 6. References ........................................................................................................................................ 28 7. Annex: Services Trade Exposures ...................................................................................................... 29 8. Appendix .......................................................................................................................................... -

Press Information

Press Information A RICH HISTORY Press Information: Marketing The Merrion, Dublin Tel: ( 353 ) 1 603 0600 FAX: ( 353 ) 1 603 0700 EMAIL: [email protected] “The Merrion is one of the most significant restoration projects which has taken place in Dublin over recent years. The Georgian architecture lends itself perfectly to the needs of a hotel: the elegantly simple and dignified exterior of the houses give presence and a wonderful sense of arrival, to The Merrion. Mornington House has transitional interiors of great magnificence which provide an exciting backdrop for the activities of the hotel and its guests. These four important Listed houses have been sympathetically restored and brought back to life to be enjoyed by people from all over the world.” Peter MacCann, General Manager, The Merrion A PLACE IN HISTORY The Merrion is set in the heart of Georgian Dublin on Upper Merrion Street, opposite Government Buildings, the home of the Irish Government. The Main House of the hotel is comprised of four meticulously restored Grade I Listed Georgian townhouses and a specially commissioned contemporary Garden Wing is arranged around two private period gardens. The houses were built in the 1760’s by Lord Monck (Charles Stanley Monck) for wealthy Irish merchants and nobility. He lived in No. 22, which became known as Monck House. The most important of the four houses is, however, No. 24 Upper Merrion Street. This was leased to Garrett Wellesley, Earl of Mornington, in 1769, it has since been known as Mornington House. The house is remembered historically as being the birthplace of Arthur Wellesley, the 1st Duke of Wellington. -

An Taoiseach Enda Kenny Department of the Taoiseach, Government Buildings, Upper Merrion Street, Dublin 2 26Th June 2012

An Taoiseach Enda Kenny Department of the Taoiseach, Government Buildings, Upper Merrion Street, Dublin 2 26 th June 2012 Re: Constitutional Convention Dear Taoiseach, We welcome your Government’s decision to establish a Constitutional Convention. This could be a critical opportunity to update and strengthen Bunreacht na hÉireann, the most definitive statement of our country’s collective values. We note with regret that, to date, there has been no formal consultation with civil society about the form or content of the Constitutional Convention. We consider that a meaningful consultation with civil society groups should take place before the Government’s proposals are finalised. It is vital that the Government maximise public participation and engagement in the work of the convention. The list of issues already identified by your Government for review by the Convention is worthy of examination. However, the list is too restrictive and fails to take advantage of the initiative your Government has shown in establishing the Constitutional Convention and providing for a moment of such historical significance. Nor does it match the ambition of the Programme for Government commitment that "by the end of our term in government, Ireland will be recognised as a modern, fair, socially inclusive and equal society". In view of the economic uncertainty faced by Ireland, when the protection of economic and social rights has never been more important, it is disappointing that the Government has thus far failed to expressly commit to the examination of these issues by the Convention. Ireland’s international commitments under human rights law must be recognised in our domestic laws, including the commitment to protect economic, social and cultural rights, such as health, housing, and adequate income. -

The Merrion History Book History

The Merrion History Book history years ago Tak250E a waLk IN DubLIN’S GEORGIaN HISTORIc HEaRT, through Merrion Square and along towards St Stephen’s Green, and you could find yourself feeling as if you have stepped back in time. The elegant redbrick buildings, with their sash windows designed to let in exactly the right amount of light, and their sets of granite steps sweeping up to gleaming, smartly painted doors, whisper of the lives that once went on inside. Along the west side of Merrion Square and towards Upper Merrion Street, your route brings you past the grand civic buildings of the National Gallery, Natural History Museum, and Leinster House: seat of the Irish Government, and said to be so ideal in proportion and design that it became the model for the White House in Washington DC. Further up, pass the Palladian façade of Government Buildings, where for almost a century the future of Ireland has been considered and shaped; and opposite, in one of the most elegant collections of four perfect Georgian town houses, find the Merrion Hotel. Image Detail from: "A Book of Maps and References to the Estaes of The Right Honourable Richard Lord Viscount Fitzwilliam, 1792, by John Barker." • • List of Lord Fitzwilliam tenants: NAI - 2011/3/1p.22 Map Detail: "A Plan of Merrion Street with the intended New Streets, being part of the Estate of thethe Right merrion Hon. hotel Lord Viscont Fitzwilliam", 1764, by John Barker. • Jonathan Barker 1764, NAI/2011/2/2/10 history ONE OF THE LIVING IN finest Georgian Georgian cities IN THE WORLD MEDIEDublinvaL DubLIN waS a cITY OF wINDING, NaRROw streets, and houses overhanging shadowed lane- THE MERRION ExISTS THaNkS TO THE vISION OF OwNERS ways but, from the 1750s on, this was to change. -

Department of the Taoiseach, Government Buildings, Merrion Street Upper, Dublin 2, D02 R583, Ireland

Department of the Taoiseach, Government Buildings, Merrion Street Upper, Dublin 2, D02 R583, Ireland. 17 September 2020 RE: Occupied Territories Bill and Effective Steps Against Annexation An Taoiseach, Micheál Martin TD, I am writing to you in my capacity as General Director of Al-Haq, a Palestinian human rights organisations based in Ramallah, Palestine, and on behalf of Palestinian civil society, in reference to your newfound concerns regarding the legality and practicality of the Control of Economic Activity (Occupied Territories) Bill, voiced in Dáil Éireann.1 We in Palestine, and those who represent Palestinian civil society throughout the world, deeply regret this newfound position and the Bill’s exclusion from the recent Programme for Government, and wish to reassure you that there is no legal barrier to the full implementation of the Bill, as we previously communicated to you and members of your party in letters dated 5 June 2020.2 As we noted in these letters, Fianna Fáil has long been a leading voice in championing the rights of the Palestinian people, who have lived under 53 years of continuous occupation and domination, and are moreover subjected to an institutionalised regime of racial domination and oppression, amounting to the crime of apartheid.3 Indeed, we look toward Ireland, and its efforts in the pursuit of international peace, justice, and accountability as inspirational: the opposition of apartheid in South Africa;4 the introduction of the Nuclear Non-Proliferation Treaty;5 your unbroken commitment to peacekeeping, -

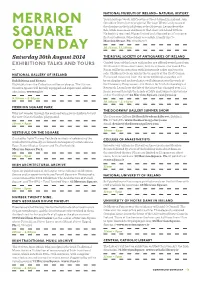

Merrion Square Open

NATIONAL MUSEUM OF IRELAND– NATURAL HISTORY Tour Heritage Week: All Creatures Great & Small in Ireland. Join MERRION Geraldine Breen for these special Heritage Week family tours of the displays in the Irish Room at the Museum. Learn about the fish, birds, mammals and insects that share our island with us. No booking required. Places limited and allocated on a first come, SQUARE first served basis. Wheelchair accessible. Family Age 7+ Merrion Street. Ph: 01 6486307 OPEN DAY 10.15am, 11.30am Saturday 30th August 2014 THE ROYAL SOCIETY OF ANTIQUARIES OF IRELAND Guided tours of the house and garden are offered every hour from EXHIBITIONS TALKS AND TOURS 10.30 until 3.30 on a first come, first serve basis. Our famed Tea — Room will be in operation with homemade cakes and teas for NATIONAL GALLERY OF IRELAND sale. Children (5+) can join in the tea party at the Craft Corner. Excavated treasures from the restored Georgian garden will Exhibitions and Events be on display and archaeologists will demonstrate the work of Highlights from the Collection will be on display. The Atrium the Discovery Programme - the Centre for Irish Archaeological Creative Spaces will be fully equipped and supervised. All free Research. Learn how the life of the house has changed over 221 admission. www.ngi.ie years, passed through the hands of MPs and judges to historians and archaeologists! 63 Merrion Square. [email protected] 9.30am – 5.30pm 10.30am – 3.30pm MERRION SQUARE PARK THE DOORWAY GALLERY SUMMER SHOW Why not wander through the park and bring your children to visit the new ‘Giant’s Garden’ playground. -

Department of the Taoiseach Customer Service Action Plan

Department of the Taoiseach Customer Service Action Plan APPENDIX C Customer Complaints Procedure What is a complaint? We define a complaint as an expression of dissatisfaction concerning the provision of a service or services by the Department, as laid out under the commitments in our Customer Charter. How to make a complaint? If you have a cause for complaint, it should be directed initially to the relevant section of the Department. Staff in that section will try to deal with the problem without delay or, if the complaint does not relate to a service provided by us, direct you to the appropriate body. If you do not know the name of the person in the section to contact, or if you are unsure which body you should make your complaint to, our Customer Service Officer will be happy to advise you; If the staff in the section cannot resolve your complaint, or you are unhappy with their response, you can ask for the matter to be reviewed by a senior member of staff from that section; If you are still unhappy with the response, you should make a formal complaint to the Customer Service Officer, who will investigate the complaint on your behalf; and You can make a complaint in person, by phone, in writing or by email (see contact details below). Department Address Department of the Taoiseach Government Buildings Upper Merrion Street D02 R583 Telephone Number (01) 619 4000 (Main Switchboard) 1890 227 227 (Lo-call) Department email address [email protected] [email protected] Quality Customer Service Officer (01) 619 4411 (Telephone) [email protected] Department of the Taoiseach Customer Service Action Plan What information should you provide? You will help to speed up the investigation of your complaint by providing the following details: Your name, address and email address; Exactly what you were dissatisfied with; The name of the official or section you dealt with; and A daytime telephone number.