Acg Member Profile

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

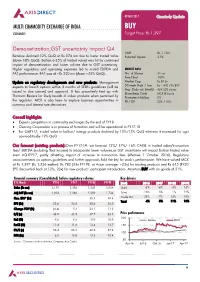

MULTI COMMODITY EXCHANGE of INDIA BUY EXCHANGES Target Price: Rs 1,397

09 MAY 2017 Quarterly Update MULTI COMMODITY EXCHANGE OF INDIA BUY EXCHANGES Target Price: Rs 1,397 Demonetization,GST uncertainty impact Q4 CMP : Rs 1,153 Revenue declined 12% QoQ at Rs 874 mn due to lower traded value Potential Upside : 21% (down 10% QoQ). Bullion (~35% of traded value) was hit by continued impact of demonetization and lower volume due to GST uncertainty. Higher regulatory and operating expenses led to muted EBITDA and MARKET DATA PAT performance. PAT was at ~Rs 220 mn (down ~35% QoQ). No. of Shares : 51 mn Free Float : 100% Update on regulatory developments and new products: Management Market Cap : Rs 59 bn expects to launch options within 3 months of SEBI’s guidelines (will be 52-week High / Low : Rs 1,420 / Rs 852 Avg. Daily vol. (6mth) : 429,628 shares issued in due course) and approval. It has proactively tied up with Bloomberg Code : MCX IB Equity Thomson Reuters for likely launch of index products when permitted by Promoters Holding : 0% the regulator. MCX is also keen to explore business opportunities in FII / DII : 23% / 36% currency and interest rate derivatives. Concall highlights ♦ Expects competition in commodity exchanges by the end of FY18 ♦ Clearing Corporation is in process of formation and will be operational in FY17-18 ♦ For Q4FY17, traded value in bullion/ energy products declined by 18%/13% QoQ whereas it increased for agri commoditiesby 19% QoQ Our forecast (existing products):Over FY17-19, we forecast 12%/ 17%/ 16% CAGR in traded value/transaction fees/ EBITDA (including float income) to incorporate lower volumes,as GST uncertainty will impact bullion traded value even inQ1FY17, partly offsetting impact of increase in transaction fees (effective 1 October 2016). -

Trading Services Price List

Trading Services Price List (On-Exchange and OTC) Effective 01st August 2016 Trading Services Price List Order book business All order and quote charges Order management charge Order Entry Non-persistent orders 1 1p All other orders Free Order and quote management surcharge 2 Each event High usage surcharge 5p High usage surcharge for qualifying order events in Exchange Traded Funds 2 1.25p (ETFs) or Exchange Traded Products (ETPs) Quote management charge (per side) Quote entry Securitised Derivatives 0.28p* All other securities Free * Monthly fee cap of £15,000. 2 Trading Services Price List Exchange charge 3 Equities Standard Value Traded Scheme 4 for Equities Charge First £2.5bn of orders executed 0.45bp* Next £2.5bn of orders executed 0.40bp* Next £5bn of orders executed 0.30bp* All subsequent value of orders executed 0.20bp* Liquidity Provider Scheme for FTSE 350 securities 5 Value of orders passively executed that qualify for the scheme Free Monthly fee for inclusion of each non-member firm as a Nominated Client £2,500 Value of all Nominated Client orders in FTSE 350 securities executed that do not qualify for the scheme 0.45bp* Aggressive executions qualifying under Liquidity Taker Scheme Packages 6 for Equities Package 1 - Monthly fee £40,000*** Value of orders executed 0.15bp** Package 2 - Monthly fee £4,000 Value of orders executed 0.28bp* Private Client Broker Order Book Trading Scheme 8 Value of orders executed in first 6 months from joining scheme Free Value of orders executed thereafter 0.10bp* Smaller Company Registered Market Maker 9 Value of orders executed 0.20bp* Hidden & non-displayed portion of Icebergs 10 Additional Charge Premium on the value executed of orders that are either hidden or the persistent non-displayed portion of an 0.25bp Iceberg * Subject to a minimum charge of 10p per order executed. -

Elixir Journal

50958 Garima saxena and Rajeshwari kakkar / Elixir Inter. Law 119 (2018) 50958-50966 Available online at www.elixirpublishers.com (Elixir International Journal) International Law Elixir Inter. Law 119 (2018) 50958-50966 Performance of Stock Markets in the Last Three Decades and its Analysis Garima saxena and Rajeshwari kakkar Amity University, Noida. ARTICLE INFO ABSTRACT Article history: Stock market refers to the market where companies stocks are traded with both listed Received: 6 April 2018; and unlisted securities. Indian stock market is also called Indian equity market. Indian Received in revised form: equity market was not organized before independence due to the agricultural conditions, 25 May 2018; undeveloped industries and hampering by foreign business enterprises. It is one of the Accepted: 5 June 2018; oldest markets in India and started in 18th century when east India Company started trading in loan securities. During post-independence the capital market became more Keywords organized and RBI was nationalized. As we analyze the performance of stock markets Regulatory framework, in the last three decades, it comes near enough to a perfectly aggressive marketplace Reforms undertaken, permitting the forces of demand and delivers an inexpensive degree of freedom to Commodity, perform in comparison to other markets in particular the commodity markets. list of Deposit structure, reforms undertaken seeing the early nineteen nineties include control over problem of Net worth, investors. capital, status quo of regulator, screen primarily based buying and selling and threat management. Latest projects include the t+2 rolling settlement and the NSDL was given the obligation to assemble and preserve an important registry of securities marketplace participants and experts. -

Today's Top Research Idea Market Snapshot Research Covered

12 May 2021 ASIAMONEY Brokers Poll 2020 (India) Today’s top research idea Godrej Consumer : New leadership offers scope for transformative change Upgrade to Buy We view Mr. Sudhir Sitapati’s appointment as MD and CEO of GCPL as a potentially transformative event in the fortunes of the company. Mr. Sitapati comes with impressive experience in heading HUVR’s F&R business and as part of the senior management team in the Detergents business, which Market snapshot have done very well under his tenure and where marketing campaigns in both segments have a high value impact. His appointment as MD and CEO for five Equities - India Close Chg .% CYTD.% years, as well has his relative young age (mid-40s), gives him adequate time to Sensex 49,162 -0.7 3.0 Nifty-50 14,851 -0.6 6.2 formulate and implement strategic changes. Nifty-M 100 24,972 0.8 19.8 The underpenetrated Household Insecticides (HI, ~70%/50% penetration in Equities-Global Close Chg .% CYTD.% urban/rural) and Hair Color (~30% penetration) categories could greatly S&P 500 4,152 -0.9 10.5 benefit from Mr. Sitapati’s past experience, where GCPL has struggled to Nasdaq 13,389 -0.1 3.9 boost penetration. FTSE 100 6,948 -2.5 7.5 DAX 15,120 -1.8 10.2 After more than a decade of being Neutral on the company (downgraded to Hang Seng 10,432 -2.1 -2.9 Neutral in Aug’10), a stand that has been vindicated particularly in the past Nikkei 225 28,609 -3.1 4.2 five years, we are upgrading the stock to Buy. -

Providing the Regulatory Framework for Fair, Efficient and Dynamic European Securities Markets

ABOUT CEPS Founded in 1983, the Centre for European Policy Studies is an independent policy research institute dedicated to producing sound policy research leading to constructive solutions to the challenges fac- Competition, ing Europe today. Funding is obtained from membership fees, contributions from official institutions (European Commission, other international and multilateral institutions, and national bodies), foun- dation grants, project research, conferences fees and publication sales. GOALS •To achieve high standards of academic excellence and maintain unqualified independence. Fragmentation •To provide a forum for discussion among all stakeholders in the European policy process. •To build collaborative networks of researchers, policy-makers and business across the whole of Europe. •To disseminate our findings and views through a regular flow of publications and public events. ASSETS AND ACHIEVEMENTS • Complete independence to set its own priorities and freedom from any outside influence. and Transparency • Authoritative research by an international staff with a demonstrated capability to analyse policy ques- tions and anticipate trends well before they become topics of general public discussion. • Formation of seven different research networks, comprising some 140 research institutes from throughout Europe and beyond, to complement and consolidate our research expertise and to great- Providing the Regulatory Framework ly extend our reach in a wide range of areas from agricultural and security policy to climate change, justice and home affairs and economic analysis. • An extensive network of external collaborators, including some 35 senior associates with extensive working experience in EU affairs. for Fair, Efficient and Dynamic PROGRAMME STRUCTURE CEPS is a place where creative and authoritative specialists reflect and comment on the problems and European Securities Markets opportunities facing Europe today. -

Lfs Broking Private Limited

LFS BROKING PRIVATE LIMITED (Member BSE, NSE, MCX & CDSL) A P P L IC A T IO N F O R A D D IT IO N A L S EG M E N T / EX C H A N G E F O R T R A D IN G A C C O U N T Client Code Client Name Branch/ AP Code Branch/ AP Name LFS BROKING PVT. LTD. CIN NO.: U67190PN2011PTC140719 Registered Office Address: Office No. 311/75, 3rd Floor, Shrinath Plaza, ‘B’ Wing, F.C. Road, Shivaji Nagar, Bhamburda, Pune - 411005. Correspondence Office Address: Unit No. 08, 2nd Floor, Prabhadevi Industrial Estate, 408 Veer Savarkar Marg, Prabhadevi, Mumbai - 400025. Tel: (91) 22-49228222 Fax: (91) 22-49228221 Website: www.lfsbroking.in Exchange Segment SEBI Registration No. Member Code Date of Registration BSE CASH/FO INZ 000101238 6628 February 20, 2017 NSE CASH/FO/CD INZ 000101238 90022 February 20, 2017 MCX COMMODITY INZ 000101238 56350 February 20, 2017 CDSL Depository Participant IN-DP-CDSL-363-2018 85400 April 05, 2018 IL & FS Securities Services Ltd. IL&FS House, Plot No.14, Raheja Vihar, Chandivali, Clearing Member for NSE (FO & CD) Segments: Andheri (E), Mumbai - 400072. Tel.: 022-42493000 www.ilfsdp.com SMC Comtrade Ltd. Clearing Member for MCX Commodity 11/6B, Shanti Chamber, Pusa Road, New Delhi ‐ 110005. Derivatives Segment: Tel.: 011-30111000 www.smcindiaonline.com Mr. Anand Tamhane Compliance Officer Details: Ph : 022-49228222 Ext: 225 Email id : [email protected] Mr. Saiyad Jiyajur Rahaman Director/CEO Details: Ph : 022-49228222 Ext. 220 Email id : [email protected] For any grievance / dispute please contact LFS BROKING PVT. -

A-Cover Title 1

Barclays Capital | Dividend swaps and dividend futures DIVIDEND SWAPS AND DIVIDEND FUTURES A guide to index and single stock dividend trading Colin Bennett Dividend swaps were created in the late 1990s to allow pure dividend exposure to be +44 (0)20 777 38332 traded. The 2008 creation of dividend futures gave a listed alternative to OTC dividend [email protected] swaps. In the past 10 years, the increased liquidity of dividend swaps and dividend Barclays Capital, London futures has given investors the opportunity to invest in dividends as a separate asset class. We examine the different opportunities and trading strategies that can be used to Fabrice Barbereau profit from dividends. +44 (0)20 313 48442 Dividend trading in practice: While trading dividends has the potential for significant returns, [email protected] investors need to be aware of how different maturities trade. We look at how dividends Barclays Capital, London behave in both benign and turbulent markets. Arnaud Joubert Dividend trading strategies: As dividend trading has developed into an asset class in its +44 (0)20 777 48344 own right, this has made it easier to profit from anomalies and has also led to the [email protected] development of new trading strategies. We shall examine the different ways an investor can Barclays Capital, London profit from trading dividends either on their own, or in combination with offsetting positions in the equity and interest rate market. Anshul Gupta +44 (0)20 313 48122 [email protected] Barclays Capital, -

Public Citizen

October 17, 2018 Office of the Comptroller of the Currency Legislative and Regulatory Activities Division 400 7th Street, S.W. Suite 3E-218, Mail Stop 9W-11 Washington, DC 20219 Board of Governors of the Federal Reserve System Ann E. Misback, Secretary 20th Street and Constitution Avenue, N.W. Washington, D.C. 20551 Federal Deposit Insurance Corporation Robert E. Feldman, Secretary Attention: Comments/Legal ESS 550 17th Street, N.W. Washington, D.C. 20429 Securities and Exchange Commission Secretary 100 F Street, N.E. Washington, DC 20549-1090 Commodity Futures Trading Commission Christopher Kirkpatrick, Secretary 1155 21st Street, N.W. Washington, DC 20581 Comptroller of the Currency Federal Reserve Board Commodity Futures Trading Commission Federal Deposit Insurance Corp Securities and Exchange Commission Proposed Revisions to Prohibitions and Restrictions on Proprietary Trading and Certain Interests in, and Relationships With, Hedge Funds and Private Equity Funds Dear officers, On behalf of more than 500,000 members and supporters of Public Citizen, we offer the following comments in response to the request by the five agencies regarding the rule titled “Proposed Revisions to Prohibitions and Restrictions on Proprietary Trading and Certain Interests in, and Relationships With, 1 Hedge Funds and Private Equity Funds.” 1 This proposal comes as a joint rulemaking from the Federal Reserve Board (Fed, Board), the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corp. (FDIC), the Commodity Futures Trading Commission (CFTC), and the Securities and Exchange Commission (SEC). Collectively, we will refer to these regulatory bodies as the “Agencies.” This proposal addresses Section 619 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, commonly known as the Volcker Rule. -

Staff Report on Algorithmic Trading in U.S. Capital Markets

Staff Report on Algorithmic Trading in U.S. Capital Markets As Required by Section 502 of the Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018 This is a report by the Staff of the U.S. Securities and Exchange Commission. The Commission has expressed no view regarding the analysis, findings, or conclusions contained herein. August 5, 2020 1 Table of Contents I. Introduction ................................................................................................................................................... 3 A. Congressional Mandate ......................................................................................................................... 3 B. Overview ..................................................................................................................................................... 4 C. Algorithmic Trading and Markets ..................................................................................................... 5 II. Overview of Equity Market Structure .................................................................................................. 7 A. Trading Centers ........................................................................................................................................ 9 B. Market Data ............................................................................................................................................. 19 III. Overview of Debt Market Structure ................................................................................................. -

Overview of Commodity Trading and Market in India

Volume 3 – Issue 6 Online ISSN: 2582-368X OVERVIEW OF COMMODITY TRADING AND MARKET IN INDIA Article Id: AL2021167 Seedari Ujwala Rani Assistant Professor, Department of Agricultural Economics, S.V. Agricultural College, Tirupati, ANGRAU, India Email: [email protected] he commodity markets began with the trading of agricultural products such as corn, cattle, wheat, and pigs in the 19th century. Chicago was the main hub for trading T due to its geographical location near the farm belt with railroad access. In India, commodity trading began with the set up of the Bombay Cotton Trade Association in 1875, which laid the foundation of futures trading in India. The nature of commodities exchanges is changing rapidly. Currently, the trend is in the direction of electronic trading, which is away from traditional trading, where traders meet face-to-face. A commodity market is a physical or virtual marketplace for buying, selling, and trading commodities. It is also called a futures market, futures exchange, organized market for the purchase and sale of enforceable contracts such as derivative products, agricultural products, and other raw materials. A farmer raising corn can sell a futures contract on his corn, which will not be harvested for several months, and gets a guarantee of the price he will be paid when he delivers. This protects the farmer from price drops and the buyer from price rises. Commodity exchange is a legal entity that determines and enforces rules produces for the trading standardized commodity contracts. From 2015, SEBI became a regulatory body for any updates and developments relating to the commodity derivatives market in India The Commodities Traded are Usually Classified Into Four Segments i. -

Multi Commodity Exchange (MCX)

Multi Commodity Exchange (MCX) CMP: | 1587 Target: | 2000 (26%) Target Period: 12 months BUY May 25, 2021 Market leadership, new products to drive earnings MCX reported a moderation in average daily turnover (ADTO) attributable to upfront margin requirement impacting volume. Operational performance remained healthy led by steady revenue and controlled opex. Volatility in other income and tax advantage in base year led to decline in earnings. Particulars ADTO in commodity futures on the exchange declined 13% to | 31823 crore Particulars Amount Update in Q4FY21, due to increase in regulatory requirement of upfront margin Market Capitalisation | 8091 crore partially offset by higher gold priced compared to last year. Markets share Equity Capital | 51 crore in commodity futures space has remained strong at 96.04% in FY21. Networth | 1418 crore Result Number of unique customers increased from 51.5 lakh in Q3FY21 to 60.2 lakh in Q4FY21 while authorised person count was at 52777. Face Value | 10 52 week high/low 1875/1112 Decline in ADTO (13% YoY) was partially offset by healthy realisation FII 36.2% keeping moderation in operational revenue at ~8% YoY to | 97 crore. Tight DII 41.2% control on cost led EBIDTA at | 44.2 crore, up 8.7% YoY, though sequentially declined 9.1%. Subsequently, EBITDA margin increased ~700 bps YoY to 445.6%. However, lower other income at | 11.5 crore in Q4FY21 (led by G- Key Highlights sec yield in narrow range) vs. | 29.7 crore in Q4FY20 and utilisation of MAT Growth in ADTO moderated 13% credit in last year led earnings decline to | 38.5 crore; down ~41% YoY. -

Enhancing Liquidity in Emerging Market Exchanges

ENHANCING LIQUIDITY IN EMERGING MARKET EXCHANGES ENHANCING LIQUIDITY IN EMERGING MARKET EXCHANGES OLIVER WYMAN | WORLD FEDERATION OF EXCHANGES 1 CONTENTS 1 2 THE IMPORTANCE OF EXECUTIVE SUMMARY GROWING LIQUIDITY page 2 page 5 3 PROMOTING THE DEVELOPMENT OF A DIVERSE INVESTOR BASE page 10 AUTHORS Daniela Peterhoff, Partner Siobhan Cleary Head of Market Infrastructure Practice Head of Research & Public Policy [email protected] [email protected] Paul Calvey, Partner Stefano Alderighi Market Infrastructure Practice Senior Economist-Researcher [email protected] [email protected] Quinton Goddard, Principal Market Infrastructure Practice [email protected] 4 5 INCREASING THE INVESTING IN THE POOL OF SECURITIES CREATION OF AN AND ASSOCIATED ENABLING MARKET FINANCIAL PRODUCTS ENVIRONMENT page 18 page 28 6 SUMMARY page 36 1 EXECUTIVE SUMMARY Trading venue liquidity is the fundamental enabler of the rapid and fair exchange of securities and derivatives contracts between capital market participants. Liquidity enables investors and issuers to meet their requirements in capital markets, be it an investment, financing, or hedging, as well as reducing investment costs and the cost of capital. Through this, liquidity has a lasting and positive impact on economies. While liquidity across many products remains high in developed markets, many emerging markets suffer from significantly low levels of trading venue liquidity, effectively placing a constraint on economic and market development. We believe that exchanges, regulators, and capital market participants can take action to grow liquidity, improve the efficiency of trading, and better service issuers and investors in their markets. The indirect benefits to emerging market economies could be significant.