Skin in the Game – the Producer Offset 10 Years on 2017 | Screen Australia 1 Lion

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

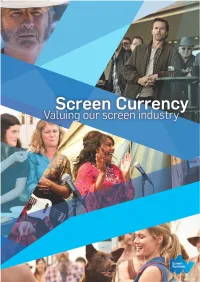

Screen Currency: Valuing Our Screen Industry

© Screen Australia 2016 The text in this report is released subject to a Creative Commons BY licence (Licence). This means, in summary, that you may reproduce, transmit and distribute the text, provided that you do not do so for commercial purposes, and provided that you attribute the text as extracted from Screen Australia’s Screen Currency: Valuing our screen industry. You must not alter, transform or build upon the text in this report. Your rights under the Licence are in addition to any fair dealing rights which you have under the Copyright Act 1968 (Cwlth). For further terms of the Licence, please see creativecommons.org/licenses/by-nc- nd/3.0/ All figures in Australian dollars. Cover: (clockwise) Wolf Creek 2, Jack Irish, The Sapphires, Red Dog and The Katering Show. Contents Introduction 4 The Dressmaker Economic value 5 Audience value 7 Cultural value 9 Screen Currency: Valuing our screen industry | Screen Australia 3 Introduction Screen Australia has engaged two companies – Deloitte Access Economics and Olsberg SPI – to comprehensively measure the economic and cultural value of the Australian screen sector. The studies quantify and articulate what Australian screen content contributes to the economy, and to Australian culture and society. Screen Currency comprises the key findings of the two studies. Miss4 Fisher’s Murder Mysteries Embrace Economic value: The financial benefits of having an Australian screen production industry The government supports the screen industry primarily because of the cultural benefits it delivers to Australian audiences and taxpayers. But the existence of a local industry also delivers significant economic benefits through the activity and employment it generates during the creation of Australian content. -

THOTKG Production Notes Final REVISED FINAL

SCREEN AUSTRALIA, LA CINEFACTURE and FILM4 Present In association with FILM VICTORIA ASIA FILM INVESTMENT GROUP and MEMENTO FILMS INTERNATIONAL A PORCHLIGHT FILMS and DAYBREAK PICTURES production true history of the Kelly Gang. GEORGE MACKAY ESSIE DAVIS NICHOLAS HOULT ORLANDO SCHWERDT THOMASIN MCKENZIE SEAN KEENAN EARL CAVE MARLON WILLIAMS LOUIS HEWISON with CHARLIE HUNNAM and RUSSELL CROWE Directed by JUSTIN KURZEL Produced by HAL VOGEL, LIZ WATTS JUSTN KURZEL, PAUL RANFORD Screenplay by SHAUN GRANT Based on the Novel by PETER CAREY Executive Producers DAVID AUKIN, VINCENT SHEEHAN, PETER CAREY, DANIEL BATTSEK, SUE BRUCE-SMITH, SAMLAVENDER, EMILIE GEORGES, NAIMA ABED, RAPHAËL PERCHET, BRAD FEINSTEIN, DAVID GROSS, SHAUN GRANT Director of Photography ARI WEGNER ACS Editor NICK FENTON Production Designer KAREN MURPHY Composer JED KURZEL Costume Designer ALICE BABIDGE Sound Designer FRANK LIPSON M.P.S.E. Hair and Make-up Designer KIRSTEN VEYSEY Casting Director NIKKI BARRETT CSA, CGA SHORT SYNOPSIS Inspired by Peter Carey’s Man Booker prize winning novel, Justin Kurzel’s TRUE HISTORY OF THE KELLY GANG shatters the mythology of the notorious icon to reveal the essence behind the Life of Ned KeLLy and force a country to stare back into the ashes of its brutal past. Spanning the younger years of Ned’s Life to the time Leading up to his death, the fiLm expLores the bLurred boundaries between what is bad and what is good, and the motivations for the demise of its hero. Youth and tragedy colLide in the KeLLy Gang, and at the beating heart of this tale is the fractured and powerful Love story between a mother and a son. -

What Killed Australian Cinema & Why Is the Bloody Corpse Still Moving?

What Killed Australian Cinema & Why is the Bloody Corpse Still Moving? A Thesis Submitted By Jacob Zvi for the Degree of Doctor of Philosophy at the Faculty of Health, Arts & Design, Swinburne University of Technology, Melbourne © Jacob Zvi 2019 Swinburne University of Technology All rights reserved. This thesis may not be reproduced in whole or in part, by photocopy or other means, without the permission of the author. II Abstract In 2004, annual Australian viewership of Australian cinema, regularly averaging below 5%, reached an all-time low of 1.3%. Considering Australia ranks among the top nations in both screens and cinema attendance per capita, and that Australians’ biggest cultural consumption is screen products and multi-media equipment, suggests that Australians love cinema, but refrain from watching their own. Why? During its golden period, 1970-1988, Australian cinema was operating under combined private and government investment, and responsible for critical and commercial successes. However, over the past thirty years, 1988-2018, due to the detrimental role of government film agencies played in binding Australian cinema to government funding, Australian films are perceived as under-developed, low budget, and depressing. Out of hundreds of films produced, and investment of billions of dollars, only a dozen managed to recoup their budget. The thesis demonstrates how ‘Australian national cinema’ discourse helped funding bodies consolidate their power. Australian filmmaking is defined by three ongoing and unresolved frictions: one external and two internal. Friction I debates Australian cinema vs. Australian audience, rejecting Australian cinema’s output, resulting in Frictions II and III, which respectively debate two industry questions: what content is produced? arthouse vs. -

The Water Diviner Reviewed by Garry Victor Hill the Water Diviner

1 The Water Diviner Reviewed by Garry Victor Hill The Water Diviner. Produced by Troy Lum, Andrew Mason and Keith Rodger. Directed by Russell Crowe. Screenplay by Andrew Anastasios and Andrew Knight. Based on the book by Sarah McGuire. Photography by Andrew Lesnie. Music by David Hirshfelder. Length: 111 minutes. A Hopscotch Feature. Warner Brothers/Universal distribution. Cinematic Release December 2014. Rated R for violence Rating ********* 90% Available on DVD. All images taken from the public domain using Google’s requirements. CAST Joshua Connor: Russell Crowe Ayshe: Olga Kurylenko Major Hasan: Yilmaz Erdoğan Sergeant Jemal: Cem Yilmaz Orhan: Dylan Georgiades Lieutenant Colonel Cyril Hughes: Jai Courtney Eliza Connor: Jaqueline McKenzie Arthur 2 Connor: Ryan Corr Henry Connor: Ben O’Toole Edward Connor: James Fraser Fatma: Megan Gale Captain James Brindley: Daniel Wylie Father Macintyre: Damon Herriman Omer: Steve Bastoni From the first scenes this emerges as a welcomingly different film. Lines of tired, pensive Turkish soldiers, clothed in motley, ragged uniforms, prepare to charge the enemy trenches. The stereotypical images of Middle Eastern soldiers, all glinting eyes as they cheerfully leap forward to kill, does not exist here: they are just weary and fearful men defending their homeland. When they do charge the trenches they are at first puzzled as the trenches are empty: then to their initial credulity they see the Allied ships sailing off. As they run up the rise the images of dirty, muddy trenches give way to a bright blue sea under a cloudless sky. Laughter and cheers replace their sadness. After living in a state of extaordinary tension and miserable expectations of death and more suffering, they find that life can also give exuberant joy. -

Australian Content on Broadcast, Radio and Streaming Services Submission 7

© Screen Australia 2016 The text in this report is rel eased subject to a Crea tive Commons BY licence {Licence). This means, in summar y, that you may reproduce, tra nsmit and distribute the text, provided that you do not do so for commercial purposes, and provided that you attribute the text as extracted from Screen Australia's Screen Currency: Valuing our screen industry. You must not alter, t ransform or build upon the text in this report. Your ri ghts under the Licence are in addition to any fa ir dealing ri ghts which you have under the Copyright Act 1968 (Cwlth) . For further terms of the Licence, pl ease see crea tivecommons.org/licenses/ by nc nd/3.0/ All figures in Australian dollars. Cover: {clockwise) Wolf Creek 2, Jack Irish, The Sapphires, Red Dag and The Katering Show. Australian Government • Contents Introduction 4 Economic value 5 Audience value 7 Cultural value 9 Screen Currency: Valuing our screen industry I Screen Australia 3 Introduction Screen Australia has engaged two companies - Deloitte Access Economics and Olsberg SPI - to comprehensively measure the economic and cultural value of the Australian screen sector. The studies quantify and articulate what Australian screen content contributes to the economy, and to Australian cu lture and society. Screen Currency comprises the key findings of the two studies. The government supports the screen industry primarily because of the cultural benefits it delivers to Australian audiences and taxpayers. But the existence of a local industry also delivers significant economic benefits through the activity and employment it generates during the creation of Australian content. -

First Winners of the 4Th Aacta Awards Announced in Sydney

Media Release – Strictly embargoed until 4:00pm Tuesday 27 January 2015 FIRST WINNERS OF THE 4TH AACTA AWARDS ANNOUNCED IN SYDNEY The 4th AACTA Awards Luncheon presented by Deluxe was today held at The Star Event Centre Sydney, celebrating screen craft excellence, and marking the first winners for the 4th AACTA Awards season. Twenty two awards were presented, recognising the talent and innovation of practitioners working across television, documentary, short fiction film, short animation and feature film. The remainder of 4th AACTA Awards will be presented at the 4th AACTA Awards Ceremony in Sydney on Thursday. Today’s event was hosted by writer/actor/producer/director Adam Zwar, whose AACTA and AFI awarded productions include Agony Aunts, Lowdown and Wilfred. Zwar, whose humour was in full force, was joined by outstanding presenters including AACTA President Geoffrey Rush, David Stratton, Damian Walshe-Howling, Alexandra Schepisi, Charlotte Best and Diana Glenn, to name a few. The talent pool was fierce this year with a number of productions bagging multiple nominations Including THE BROKEN SHORE, TENDER, UKRAINE IS NOT A BROTHEL and PREDESTINATION, all with five nominations. TELEVISION On the small screen the AACTA Award for Best Children’s Television Series went to Colin South and Keith Saggers for their show set in a tiny town called Whale Bay, home to a giant thong, ABC3’s THE FLAMIN’ THONGS. The AACTA Award for Best Direction in a Television Light Entertainment or Reality Series went to Beck Cole and Craig Anderson for Episode 3 of the ABC’s BLACK COMEDY, a ground breaking show, featuring an ensemble cast of Indigenous writers and performers. -

The Paul Hogan Story

Coming to HOGES THE PAUL HOGAN STORY From Seven and FremantleMedia Australia (FMA) comes HOGES: The Paul Hogan story. An almost accidental supernova of raw comedic talent exploding onto the entertainment scene; first Australia, then the world. The story of how a married-at-18 Sydney Harbour Bridge rigger with five kids entered a TV talent contest on a dare from his work-mates to become a household name and an Oscar-nominated superstar. Embraced by all Australians and soon known simply as “Hoges,” he is joined on his meteoric journey by lifelong friend, producer and sidekick John “Strop” Cornell. Together, they first make Australians laugh, then proud with one of the most successful tourism campaigns in history selling Aussie hospitality to the world. This, with the runaway success of Crocodile Dundee, the highest US-grossing foreign film ever in its day, cements Hogan’s legacy. HOGES explores the factors which shaped this success – and at what cost success might have come. It entwines the story of his amazing journey with that of his close family life, of his two great loves, the pain of divorce, his struggle with the intense scrutiny of life in the public eye, but also of his enduring friendship with Cornell and the rollercoaster ride of their careers. FMA’s Jo Porter and Seven’s Julie McGauran are Executive Producers, Kevin Carlin (Molly, Wentworth) is Co-Producer and Director, Brett Popplewell is Producer and the script is by Keith Thompson (The Sapphires) and Marieke Hardy (Packed To The Rafters, The Family Law). The Hoges Story PART ONE PART TWO Poolside at Granville baths, a young Paul Hogan cracks jokes and pashes While the success of Crocodile Dundee catapults Hoges onto the world Noelene, his childhood sweetheart. -

2015 Australians in Film Heath Ledger Scholarship Winner Announced Today in West Hollywood

PRESS RELEASE - EMBARGOED ***Under strict embargo until PST 9pm June 1 / AEST 2pm June 2 2015 *** 2015 AUSTRALIANS IN FILM HEATH LEDGER SCHOLARSHIP WINNER ANNOUNCED TODAY IN WEST HOLLYWOOD At the Sunset Marquis Hotel in Los Angeles this evening, Matt Levett was announced the winner of the prestigious 2015 HEATH LEDGER SCHOLARSHIP and Emilie Cocquerel and Lily Sullivan were named the runners up. For the high calibre judging panel, the choice was not an easy one to make. Emmy award winning casting director, Laray Mayfield (Fight Club, Gone Girl, House of Cards, The Social Network), who joined the panel for the first time this year said, ‘It was inspiring to be on a judging panel where every person was passionate and invested in the result. The decision was not easy as each of the applicants are talented and unique and we are sure they will have long and lovely careers. Ultimately our decision was to award the scholarship to Matt Levett. We are all excited about watching his talent and career continue to grow and we are also looking forward to seeing the work the runners up Emilie Cocquerel and Lily Sullivan will do .” Each year Heath’s father, Kim Ledger, contacts the winner of the scholarship to advise them that they have won. He said, “It is always such an exciting phone call to make because we know that the scholarship makes such an impact on a young performer’s career. For the seventh year, the scholarship has gone to a deserving recipient in Matt Levett. This is a wonderful initiative run by Australians in Film and we wish Matt every success.” Of his win, Levett said, "I am humbled to have received this incredible gift. -

The Water Diviner

presenta un film diretto e interpretato da Russell Crowe THE WATER DIVINER Con Russell Crowe, Olga Kurylenko, Yılmaz Erdoğan, Cem Yılmaz, Jai Courtney e Ryan Corr DALL’8 GENNAIO AL CINEMA Durata: 111 minuti I materiali sono scaricabili dall’ area stampa di www.eaglepictures.com Ufficio Stampa: [email protected] Stefania Collalto – tel. +39 0246762519 – mob. +39 339-4279472 Lisa Menga – tel. +39 02-46762529 – mob +39 347-5251051 Diletta Colombo – tel. +39 02-46762533 – mob. + 39 347-8169825 1 THE WATER DIVINER, film che segna il debutto alla regia di Russell Crowe, è un’avventura epica ambientata quattro anni dopo la terribile battaglia di Gallipoli in Turchia, durante la Prima Guerra Mondiale. Nel 1919, l’agricoltore australiano Joshua Connor (Russell Crowe) si reca proprio in Turchia sulle tracce dei tre figli dati per dispersi sul campo. Grazie alla propria determinazione, Joshua riesce a superare gli ostacoli della burocrazia militare, aiutato in questo prima dalla bellissima Ayshe (Olga Kurylenko), proprietaria dell’hotel in cui alloggia, poi da un ufficiale turco che ha combattuto contro i tre giovani. Connor si aggrappa alla speranza di ritrovare i figli vivi e con Hasan attraverserà il paese, dilaniato dal conflitto, per scoprire la verità. THE WATER DIVINER, struggente, romantica e toccante avventura epica, racconta l’amore oltre i confini del bene e del male. SINOSSI ESTESA 1919. La Grande Guerra è finita da un anno, ma le conseguenze bruciano ancora come ferite aperte in tutto il mondo. Nella campagna australiana del Mallee, l’agricoltore rabdomante JOSHUA CONNOR (Russell Crowe), vive accettando faticosamente la consapevolezza che tutto ciò che gli resta dei tre figli maschi, a quattro anni di distanza dalla battaglia di Gallipoli, è un pacchetto con un vecchio diario personale, alcune lettere e poche foto. -

Interview with Olga Kurylenko for the Daily Life's Sunday

SHE’S FRANK, SMART, FUNNY AND UNLUCKY IN LOVE. HERE BOND GIRL AND EX MODEL OLGA KURYLENKO OPENS UP TO JANE CORNWELL. lga Kurylenko’s people have booked a table for two in a cafe in Chelsea, in the heart of discrete, upper-crust west London. It will just be the two of us – no bodyguards, no PR girls flashing the five- minute sign, none of the media-minder obusiness often associated with celebrity interviews, especially ones with stunning, critically-acclaimed French-Ukrainian actresses on the cusp of A-list status. We’re meeting to talk about her role in Russell Crowe’s directorial debut, The Water Diviner, a drama about an Australian farmer, Joshua Connor (Crowe), who travels to Turkey in search of his three sons, missing after the 1915 Battle of Gallipoli. Kurylenko plays Ayshe, the mysterious woman who owns the Istanbul hotel in which Connor stays. There have been no press screenings, understanding so I haven’t seen the film. But the official trailer, with its swirling dust storms, swelling string music and exploding World War I battlefields underscores The Water Diviner’s wannabe blockbuster status. There’s a scene OLGA where Ayshe delivers linen to Connor’s room, her eyes big and sad under her headscarf. “There is nothing there but ghosts,” she says, a beguiling mix of beauty, strength and fragility. “Her husband has also disappeared in the war,” 35-year-old Kurylenko will tell me once she arrives (I have received a text saying she is running late). “But Ayshe refuses to marry her husband’s brother, as was the tradition in Turkey, because for her it is love or nothing. -

Australian Cinematographers Society V4.1 Now Releasedfirmware Cache Recording, Menu Updates & Much More!

australian cinematographer ISSUE #64 DECEMBER 2014 RRP $10.00 Quarterly Journal of the Australian Cinematographers Society www.cinematographer.org.au V4.1 Now ReleasedFirmware Cache recording, menu updates & much more! The future, ahead of schedule Discover the stunning versatility of the new F Series Shooting in HD and beyond is now available to many more content creators with the launch of a new range of 4K products from Sony, the first and only company in the world to offer a complete 4K workflow from camera to display. PMW-F5 PMW-F55 The result of close consultation with top cinematographers, the new PMW-F5 and PMW-F55 CineAlta cameras truly embody everything a passionate filmmaker would want in a camera. A flexible system approach with a variety of recording formats, plus wide exposure latitude that delivers superior super-sampled images rich in detail with higher contrast and clarity. And with the PVM-X300 monitor, Sony has not only expanded the 4K world to cinema applications but also for live production, business and industrial applications. Shoot, record, master and deliver in HD, 2K or 4K. The stunning new CineAlta range from Sony makes it all possible. PVM-X300X300 For more information, please email us at [email protected] pro.sony.com.au MESM/SO140803/AC www.millertripods.com There’s one thing Production Directors can agree on... ;OL*PULSPULZL[ZUL^Z[HUKHYKZMVY*PULÅ\PKOLHKZ • Quick & easy to operate ‘all-in-one location’ rear 0SS\TPUH[LKWHU[PS[KYHNJV\U[LYIHSHUJLJVU[YVSZ mounted controls HUKI\IISLSL]LS • Side loading camera platform, 150mm travel with >PKL7H`SVHKYHUNLRN SIZ Arri type camera plate 7HU[PS[Å\PKKYHNWVZP[PVUZ • Drag control with ultra-soft starts and smooth stops 7VZP[PVUZVMJV\U[LYIHSHUJL ,HZ`[VÄ[4P[JOLSSIHZLHKHW[VY[VZ\P[4P[JOLSS ÅH[IHZL[YPWVKZ Contact your nearest Miller dealer today. -

Law & Disorder

LAW & DISORDER RAKE LAW & DISORDER RAKE SERIES FOUR / 8 X ONE HOUR TV SERIES THURSDAY MAY 19 8.30PM STARRING RICHARD ROXBURGH WRITTEN BY PETER DUNCAN & ANDREW KNIGHT PRODUCED BY IAN COLLIE, PETER DUNCAN & RICHARD ROXBURGH ESSENTIAL MEDIA & BLOW BY BLOW MEDIA CONTACT Kristine Way / ABC TV Publicity T 02 8333 3844 M 0419 969 282 E [email protected] SERIES SYNOPSIS Last seen dangling from a balloon road leading straight to our dark drifting across the Sydney skyline, corridors of power. Cleaver Greene (Richard Roxburgh) Twisting and weaving the stories of crashes back to earth - literally and the ensemble of characters we’ve metaphorically, when he’s propelled grown to love over three stellar through a harbourside window into the seasons, Season 4 of Rake continues unwelcoming embrace of chaos past. the misadventures of dissolute Cleaver Fleeing certain revenge, Cleaver Greene and casts the fool’s gaze on all hightails it to a quiet country town, the levels of politics, the legal system, and reluctant member of a congregation our wider fears and obsessions. led by a stern, decent reverend and ALSO STARS Russell Dykstra, Danielle his flirtatious daughter. Before long Cormack, Matt Day, Adrienne Cleaver’s being chased back to Sin City. Pickering, Caroline Brazier, Kate Box, But Sydney has become a dark Keegan Joyce and Damien Garvey. place: terrorist threats and a loss of GUEST APPEARANCES from Miriam faith in authority have seen it take a Margolyes, Justine Clarke, Tasma turn towards the dystopian. When Walton, John Waters, Simon Burke, Cleaver finally emerges, he will be Rachael Blake, Rhys Muldoon, Louise accompanied by a Mistress of the Siversen and Sonia Todd.