The Demise of Toys 'R' Us Is a Warning

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Leadership Newsletter Winter 2020 / 2021

T���������, M���� ��� T����������������� Leadership Newsletter Winter 2020 / 2021 GTCR Firm Update Since the firm’s inception in 1980, GTCR has Technology, Media and Tele- partnered with management teams in more communications than 200 investments to build and transform growth businesses. Over the last twenty years alone, GTCR has invested over $16 billion in approximately 100 platform acquisitions, 30+ 95+ PLATFORMS ADD-ONS including more than 65 companies that have been sold for aggregate enterprise value of over $ $50 billion and another 14 companies that have 25B+ been taken public with aggregate enterprise value PURCHASE of more than $34 billion. In November 2020, PRICE we closed GTCR Fund XIII, the firm’s largest fund to date, with $7.5 billion of limited partner capital commitments. This fund follows GTCR Fund Acquisition Activity Since 2000 XII, which we raised in 2017, with $5.25 billion As of January 15, 2021* of limited partner capital commitments. GTCR currently has 25 active portfolio companies; ten of these companies are within the Technology, Media and Telecommunications (“TMT”) industry. Page 1 / Continues on next page Technology, Media and Telecommunications Group Update Since 2000, GTCR has completed over 30 new platform investments and over 95 add-on acquisitions within the TMT industry, for a total of over 125 transactions with a combined purchase price of over $25 billion. During just the past year, we have realized several of these investments, selling three businesses and completing the partial sale of two additional companies, for a combined enterprise value of over $9 billion. Our TMT franchise includes ten active portfolio companies and one management start-up, which together have completed nearly 30 add-on acquisitions under our ownership, representing approximately $3 billion of GTCR invested capital. -

Not Mitt Romney's Bain Capital: Boston Investment Firm Home To

Not Mitt Romney’s Bain Capital: Boston investment firm home to diverse political views - Business - The Boston Globe Interested in documentaries? Click here to view our latest free screening. TEXT SIZE MANAGE ACCOUNT LOG OUT NEWS BusinessMETRO MARKETS TECHNOLOGY ARTS BUSINESS BETABOSTON SPORTS OPINION Red Sox Live 3 8 POLITICS LIFESTYLE Final MAGAZINE INSIDERS AtTODAY'S Bain, PAPER a broad range of viewpoints is the new reality E-MAIL FACEBOOK TWITTER GOOGLE+ LINKEDIN 57 http://www.bostonglobe.com/...romney-bain-capital-boston-investment-firm-home-diverse-political-views/gAGQyqkSROIoVubvsCXJxM/story.html[5/23/2015 10:37:45 PM] Not Mitt Romney’s Bain Capital: Boston investment firm home to diverse political views - Business - The Boston Globe SUZANNE KREITER/GLOBE STAFF Former Governor Deval Patrick, a Democrat, is joining Bain Capital — an investment firm founded by his predecessor on Beacon Hill, Republican Mitt Romney. By Beth Healy and Matt Rocheleau GLOBE STAFF APRIL 16, 2015 There are two chestnuts that drive Bain Capital partners crazy: First, the notion that they are ruthless capitalists who enjoy firing people. Second, that they are all card-carrying Republicans. Fifteen long years since Mitt Romney left the Boston investment firm he founded, those old impressions still rankle. Enter Deval Patrick, former Massachusetts governor and a Democrat closely aligned with President Obama, named this week a Bain managing director who will focus on “social impact” investing. The newest Bain employee — and the public spirit implied by his new job — would seem to contradict the firm’s old image. But current and former partners, and close observers of the firm say Bain Capital is more of a big tent than many might think. -

The Retail Apocalypse - Fact Or Fiction?

The Retail Apocalypse - Fact or Fiction? May 10, 2019 Panel Introductions • Moderator: • Manuel Farach, Member, McGlinchey Stafford • Panelists: • Sarah Lemke, Vice President, Project Development, New England Development • Matt Epstein, Director, Goulston & Storrs, P.C. Agenda • Current State of Retail • Is It Really an Apocalypse? • Strategies for the New Future of Retail • Conclusion and Q&A Current State of Retail- Store Closures Abound ▪ Over 12,000 stores closed in 2018 ▪ Over 5,800 stores have already announced closures planned for 2019, including: ▪ Payless- 2,500 stores ▪ Gymboree- 805 stores ▪ Family Dollar- 390 stores ▪ Shopko- 371 stores ▪ Gap- 230 stores ▪ Sears- 70 stores ▪ Victoria’s Secret- 53 stores ▪ Abercrombie & Fitch- 40 stores ▪ Other retailers closing: Aerosoles, American Apparel, BCBG, Bon-Ton, Children’s Place, CVS, Dollar Tree, Foot Locker, Guess, JC Penney, Limited, Macy’s, Michael Kors, Toys R Us, Victoria’s Secret, Wet Seal © New England Development 4 Current State of Retail - Store Closures Abound © New England Development In 2018, over 145 million square feet of retail closed 5 Current State of Retail - Bankruptcies Continue © New England Development 6 What’s Causing Widespread Closures and Bankruptcies? ▪ Retailers facing massive debt from private equity financings ▪ E-Commerce and the “Amazon Effect” ▪ “Over-Retailing”/Saturation of the Market ▪ Changing Consumer Demands ▪ Inability to Adapt © New England Development 7 E-Commerce - Part of the Problem E-commerce continues to gain steam- growing 15% in 2018, -

Private Equity and Value Creation in Frontier Markets: the Need for an Operational Approach

WhatResearch a CAIA Member Review Should Know Investment Strategies CAIAInvestmentCAIA Member Member Strategies Contribution Contribution Private Equity and Value Creation in Frontier Markets: The Need for an Operational Approach Stephen J. Mezias Afzal Amijee Professor of Entrepreneurship and Family Enterprise Founder and CEO of Vimodi, a novel visual discussion with INSEAD, based at the Abu Dhabi campus application and Entrepreneur in Residence at INSEAD 42 Alternative Investment Analyst Review Private Equity and Value Creation in Frontier Markets Private Equity and Value Creation in Frontier Markets What a CAIA Member Should Know Investment Strategies 1. Introduction ership stakes, earning returns for themselves and the Nowhere else is the operational value creation approach LPs who invested with them. While this clarifies that more in demand than in the Middle East North Africa capturing premiums through ownership transactions is (MENA) region. Advocating and building operational a primary goal for GPs, it does not completely address capabilities requires active investment in business pro- the question of what GPs need to do to make the stakes cesses, human capital, and a long-term horizon. Devel- more valuable before selling the companies in question. oping the capabilities of managers to deliver value from There are many ways that the GPs can manage their in- operations will not only result in building capacity for vestments to increase value, ranging from bringing in great companies, but will also raise the bar for human functional expertise, e.g., sound financial management, talent and organizational capability in the region. In the to bringing in specific sector operational expertise, e.g., long term, direct support and nurturing of the new gen- superior logistics capabilities. -

Representative Financial Services M&A Transactions

Representative Financial Services M&A Transactions Asset Management • Hellman & Friedman. Representing Hellman & Friedman in connection with its acquisition of Allfunds Bank S.A., a Spanish bank that offers intermediation and investment services to commercial banks, private banking institutions, fund managers, insurance companies and fund supermarkets. • Ramius, LLC. Represented Ramius, LLC, in its sale of Ramius Alternative Solutions to AllianceBernstein. • Landmark Partners. Represented Landmark Partners in the $465 million sale to OM Asset Management, a privately owned asset management holding company. • State Street Bank and Trust Company. Represented State Street Bank and Trust Company in the acquisition of GE Asset Management (GEAM), a privately owned investment manager. • Mitsubishi UFJ Investor Services. Represented Mitsubishi UFJ Investors Services in its acquisition of UBS Global Asset Management’s Alternative Fund Services Business, a company that offers professional services for hedge funds, funds of hedge funds, private equity, and real estate structures. • Mitsubishi UFJ Fund Services Holdings Ltd. Represented Mitsubishi UFJ Fund Services Holdings Ltd., an asset administration company, in its acquisition of Meridian Fund Services Group. • Bain Capital. Represented the global credit affiliate of Bain Capital in its $1.6 billion acquisition of four portfolios of collateralized loan obligations (CLOs) from Regiment Capital. • Wellington Management Company. Represented Wellington Management Company, a privately owned investment manager, in its $85 million PIPE investment in ChinaCache International Holdings Ltd., a provider of content and application delivery services in the People’s Republic of China. • 3i Group. Represented 3i Group in its strategic transaction with Fraser Sullivan, a privately owned investment manager. • Special Committee of Cole Credit Property Trust II Inc. -

How Will Financial Services Private Equity Investments Fare in the Next Recession?

How Will Financial Services Private Equity Investments Fare in the Next Recession? Leading funds are shifting to balance-sheet-light and countercyclical investments. By Tim Cochrane, Justin Miller, Michael Cashman and Mike Smith Tim Cochrane, Justin Miller, Michael Cashman and Mike Smith are partners with Bain & Company’s Financial Services and Private Equity practices. They are based, respectively, in London, New York, Boston and London. Copyright © 2019 Bain & Company, Inc. All rights reserved. How Will Financial Services Private Equity Investments Fare in the Next Recession? At a Glance Financial services deals in private equity have grown on the back of strong returns, including a pooled multiple on invested capital of 2.2x in recent years, higher than all but healthcare and technology deals. With a recession increasingly likely during the next holding period, PE funds need to develop plans to weather any storm and potentially improve their competitive position during and after the downturn. Many leading funds are investing in balance-sheet-light assets enabled by technology and regulatory change. Diligences now should test target companies under stressful economic scenarios and lay out a detailed value-creation plan, including how to mobilize quickly after acquisition. Financial services deals by private equity funds have had a strong run over the past few years, with deal value increasing significantly in Europe and the US(see Figure 1). Returns have been strong as well. Global financial services deals realized a pooled multiple on invested capital of 2.2x from 2009 through 2015, higher than all but healthcare and technology deals (see Figure 2). -

Municipality

TheMunicipality Your Voice. Your Wisconsin. January | 2019 2019–2020 LEAGUE LEGISLATIVE AGENDA Split Party After the Retail Apocalypse, Preparing Wisconsin New Records Control is Good Small State Agency — Prepare for the Property Opportunity Zones Schedule Approved for Municipalities Big Statewide Impact Tax Meltdown for Investment for Municipalities 4 8 The Municipality12 | January 2019 20 24 1 Is there a company that insures only cities and villages? Oh yes, dear Why LWMMI, of course For 33 years, the League of Wisconsin Municipalities Insurance Program has responded to the coverage needs of local cities and villages, saving them substantial amounts of money in the process Protecting The Communities We Live In. 608.833.9595 | www.LWMMI.org A Mutual Company Owned by Member Cities and Villages. TheMunicipality The Municipality Official Monthly Publication of the League of Wisconsin Municipalities January | 2019 Volume 114, No. 1, January 2019 Editorial Offices 131 W. Wilson St., Suite 505, Madison, WI 53703 Feature Dial (608) 267-2380 In-State (800) 991-5502 Fax: (608) 267-0645 Small State e-mail: [email protected] Split Party Agency — Here’s to Did You Website: www.lwm-info.org Control is Good for Big Statewide You Know? The Municipality serves as the medium of Municipalities Impact exchange of ideas and information on municipal affairs for the officials of Wisconsin cities and villages. Nothing included herein is to 3 4 8 11 be construed as having the endorsement of the League unless so specifically stated. The Municipality (ISSN 0027-3597) is published monthly at $25 per year ($5.00 per copy, back After the Retail Preparing issues $5.00 each) by the League of Wisconsin Apocalypse, Wisconsin Municipalities, 131 W. -

Form 3 FORM 3 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

SEC Form 3 FORM 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 OMB APPROVAL INITIAL STATEMENT OF BENEFICIAL OWNERSHIP OF OMB Number: 3235-0104 Estimated average burden SECURITIES hours per response: 0.5 Filed pursuant to Section 16(a) of the Securities Exchange Act of 1934 or Section 30(h) of the Investment Company Act of 1940 1. Name and Address of Reporting Person* 2. Date of Event 3. Issuer Name and Ticker or Trading Symbol Requiring Statement EASTMAN KODAK CO [ EK ] Chen Herald Y (Month/Day/Year) 09/29/2009 (Last) (First) (Middle) 4. Relationship of Reporting Person(s) to Issuer 5. If Amendment, Date of Original Filed C/O KOHLBERG KRAVIS ROBERTS & (Check all applicable) (Month/Day/Year) CO. L.P. X Director 10% Owner Officer (give title Other (specify 2800 SAND HILL ROAD, SUITE 200 below) below) 6. Individual or Joint/Group Filing (Check Applicable Line) X Form filed by One Reporting Person (Street) MENLO Form filed by More than One CA 94025 Reporting Person PARK (City) (State) (Zip) Table I - Non-Derivative Securities Beneficially Owned 1. Title of Security (Instr. 4) 2. Amount of Securities 3. Ownership 4. Nature of Indirect Beneficial Ownership Beneficially Owned (Instr. 4) Form: Direct (D) (Instr. 5) or Indirect (I) (Instr. 5) Table II - Derivative Securities Beneficially Owned (e.g., puts, calls, warrants, options, convertible securities) 1. Title of Derivative Security (Instr. 4) 2. Date Exercisable and 3. Title and Amount of Securities 4. 5. 6. Nature of Indirect Expiration Date Underlying Derivative Security (Instr. 4) Conversion Ownership Beneficial Ownership (Month/Day/Year) or Exercise Form: (Instr. -

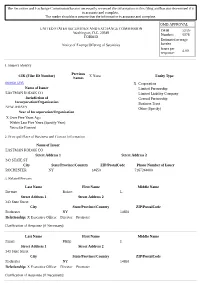

The Securities and Exchange Commission Has Not Necessarily Reviewed the Information in This Filing and Has Not Determined If It Is Accurate and Complete

The Securities and Exchange Commission has not necessarily reviewed the information in this filing and has not determined if it is accurate and complete. The reader should not assume that the information is accurate and complete. OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB 3235- Washington, D.C. 20549 Number: 0076 FORM D Estimated average Notice of Exempt Offering of Securities burden hours per 4.00 response: 1. Issuer's Identity Previous CIK (Filer ID Number) X None Entity Type Names 0000031235 X Corporation Name of Issuer Limited Partnership EASTMAN KODAK CO Limited Liability Company Jurisdiction of General Partnership Incorporation/Organization Business Trust NEW JERSEY Other (Specify) Year of Incorporation/Organization X Over Five Years Ago Within Last Five Years (Specify Year) Yet to Be Formed 2. Principal Place of Business and Contact Information Name of Issuer EASTMAN KODAK CO Street Address 1 Street Address 2 343 STATE ST City State/Province/Country ZIP/PostalCode Phone Number of Issuer ROCHESTER NY 14650 7167244000 3. Related Persons Last Name First Name Middle Name Berman Robert L. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Faraci Philip J. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Haag Joyce P. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Kruchten Brad W. -

The Retail Apocalypse - Debunking the Myth

Public Square | CNU Journal September 2019 The Congress for the New Urbanism Page 1 The Retail Apocalypse - Debunking the Myth Introduction – The “Retail Apocalypse” is a This article also touches on some emerging retail concept being actively promoted through media trends, including retrofitting vacant mall anchors headlines, and largely based on recent closures and leveraging the “Halo Effect” of Omni-channel among national chain stores across the nation. marketing to optimize retail sales. However, it is only a myth that can be easily debunked with real data. Increasing Number of Retail Establishments – The hypothetical Retail Apocalypse should be It is important to debunk the myth and change supported by a decline in the total retail the dialogue about the future of retail establishments – but nothing could be farther nationwide, in our downtowns, and all urban from the truth. In fact, the United States had over settings. By challenging mainstream media and 1 million retail establishments in 2018 – and more shifting the conversation, we hope to instill new than the prior year 2017. More specifically, the faith and encouragement for urban and town Bureau of Labor Statistics (BLS) reported planners, developers, downtown merchants, and 1,044,509 establishments for 2018, for a net gain of main street managers. +2,413 establishments since 2017 (1,042,096). The 2018 figure also represents a net gain of over This article explores real data and demonstrates +20,800 establishments since the trough in 2011. that the total number of retail establishments and aggregate retail sales are actually increasing; A timeline of total retail establishments since 2001 new chain stores and restaurant openings are is shown in chart below. -

COVERAGE LIST GEO Group, Inc

UNITED STATES: REIT/REOC cont’d. UNITED STATES: REIT/REOC cont’d. UNITED STATES: NON-TRADED REITS cont’d. COVERAGE LIST GEO Group, Inc. GEO Sabra Health Care REIT, Inc. SBRA KBS Strategic Opportunity REIT, Inc. Getty Realty Corp. GTY Saul Centers, Inc. BFS Landmark Apartment Trust, Inc. Gladstone Commercial Corporation GOOD Select Income REIT SIR Lightstone Value Plus Real Estate Investment Trust II, Inc. Gladstone Land Corporation LAND Senior Housing Properties Trust SNH Lightstone Value Plus Real Estate Investment Trust III, Inc. WINTER 2015/2016 • DEVELOPED & EMERGING MARKETS Global Healthcare REIT, Inc. GBCS Seritage Growth Properties SRG Lightstone Value Plus Real Estate Investment Trust, Inc. Global Net Lease, Inc. GNL Silver Bay Realty Trust Corp. SBY Moody National REIT I, Inc. Government Properties Income Trust GOV Simon Property Group, Inc. SPG Moody National REIT II, Inc. EUROPE | AFRICA | ASIA-PACIFIC | MIDDLE EAST | SOUTH AMERICA | NORTH AMERICA Gramercy Property Trust Inc. GPT SL Green Realty Corp. SLG MVP REIT, Inc. Gyrodyne, LLC GYRO SoTHERLY Hotels Inc. SOHO NetREIT, Inc. HCP, Inc. HCP Sovran Self Storage, Inc. SSS NorthStar Healthcare Income, Inc. UNITED KINGDOM cont’d. Healthcare Realty Trust Incorporated HR Spirit Realty Capital, Inc. SRC O’Donnell Strategic Industrial REIT, Inc. EUROPE Healthcare Trust of America, Inc. HTA St. Joe Company JOE Phillips Edison Grocery Center REIT I, Inc. GREECE: Athens Stock Exchange (ATH) AFI Development Plc AFRB Hersha Hospitality Trust HT STAG Industrial, Inc. STAG Phillips Edison Grocery Center REIT II, Inc. AUSTRIA: Vienna Stock Exchange (WBO) Babis Vovos International Construction S.A. VOVOS Alpha Pyrenees Trust Limited ALPH Highwoods Properties, Inc. -

LIFE at KKR We Are Investors

LIFE AT KKR We are investors. But we're more than that. IT'S IN OUR DNA We're collaborative team players who are curious communities. We often measure success over about the world around us. We're passionate about years, not quarters. We value integrity in all that we always learning more and pushing to be better. do, whether it's presenting numbers accurately or Here, we're never finished growing or discovering being open and honest with a portfolio company new ideas. executive. People want to do business with those they like and trust. It's a mantra instilled in all of us People want to do business from the top down. with those they like and trust As a firm we manage investments across multiple asset classes and as individuals we are encouraged to think creatively to solve problems, explore opportunities, take on new responsibilities and challenges, put our clients first and contribute to our LIFE AT KKR | 2 We are investors. But we're more than that. Culture & Work Environment For over 40 years, our At KKR, you'll find a team of curious, driven, dedicated and intelligent professionals who enjoy working together. We all work collaborative approach hard to create a friendly environment that encourages asking continues to drive our culture questions and reaching out to others. Teamwork Entrepreneurial Spirit Integrity No matter where you sit in the Some of our best ideas come from It's at the heart of everything we do organization, you have the full giving people the time to explore, from our internal interactions to resources, network, skills and research and have conversations.