SEC FORM 20IS (REVISED).Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Organization Name Substation Class Region 111 Paseo De Roxas Condominium Association Inc

Organization Name Substation Class Region 111 Paseo De Roxas Condominium Association Inc. Zapote CCU LUZON 20-12 Property Holdings, Inc. Sucat CCU LUZON 20-34 Property Holdings, Inc. Sucat CCU LUZON 21st Century Mouldings Corp. Quezon CCU LUZON 21st Century Steel Mill, Inc Dolores CCU LUZON 3-J Plasticworld & Manufacturing Corporation Duhat CCU LUZON 557 Feather Meal Corporation Concepcion CCU LUZON 6776 Ayala Avenue Condominium Corporation Sucat CCU LUZON A.D. Gothong Manufacturing Corporation Mandaue GIS CCU VISAYAS Abenson Inc. Zapote CCU LUZON ABS-CBN Corporation Araneta CCU LUZON AcBel Polytech Philippines, Inc. Calauan CCU LUZON Acesite (Phils.) Hotel Corporation Paco CCU LUZON ACI, Inc. (Cyberpark 2) Araneta CCU LUZON Adebe Realty Company, Inc. Zapote CCU LUZON Adriatico Consortium, Inc. Paco CCU LUZON Aeonprime Land Development Corp. (Block 45-Aeon Center) Sucat CCU LUZON Aeonprime Land Development Corporation Zapote CCU LUZON Agripacific Corporation Amadeo CCU LUZON Aichi Forge Philippines, Inc. Sta.Rosa CCU LUZON Aikawa Philippines Inc. Calauan CCU LUZON Air Liquide Philippines, Inc. Sucat CCU LUZON Air Liquide Pipeline Utilities Services, Inc. BIñan CCU LUZON Air Liquide Pipeline Utilities Services., Inc. Calung Calung CCU VISAYAS Ajinomoto Philippines Flavor Food Inc. Duhat CCU LUZON Alabang Commercial Corporation Zapote CCU LUZON ALASKA Milk Corporation Biñan CCU LUZON Albay Agro-Industrial Development Corporation Tiwi A DCU LUZON Ali Makati Hotel Property, Inc. Sucat CCU LUZON ALI-CII Development Corporation Zapote CCU LUZON Allegro MicroSystems Philippines,Inc. Sucat CCU LUZON AllHome Corp. (AllHome Libis) Dolores CCU LUZON Allied Packaging Corporation Duhat CCU LUZON Alpha Supreme Corp. Duhat CCU LUZON Alphaland Corporation (Alphaland Southgate Tower, Inc.) Zapote CCU LUZON Alphaland Makati Place, Inc. -

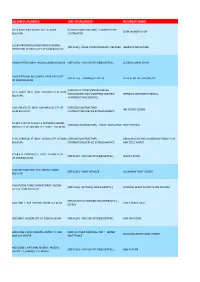

Business Address Line of Business Business Name

BUSINESS ADDRESS LINE OF BUSINESS BUSINESS NAME # 013 BRGY. POBLACION I CITY OF SJDM [SERVICES/CONTRACTORS] - LAUNDRY SHOP SJDM LAUNDRY SHOP BULACAN CONTRACTOR # 166A PROVINCIAL ROAD FARMVIEW BRGY. [RETAILER] - DRUG STORE/PHARMACY RETAILER GENERIKA DRUGSTORE TUNGKONG MANGGA CITY OF SJDM BULACAN # 1824 PARTIDA BRGY MUZON CSJDM BULACAN [RETAILER] - SARI-SARI STORE(ESSENTIAL) CLAIRE & AIRISH STORE # 260 NATIONAL ROAD BRGY. GAYA GAYA CITY [RETAILER] - TRADING (RETAILER) FIL-BEST METAL TRADING INC. OF SJDM BULACAN [LESSORS OF APARTMENT\BOARDING # 277 CARRIEDO ST. BRGY. MUZON CITY OF SJDM HSE\LODGING\INNS \SHOPPING CENTERS] - LERMENG APARTMENT RENTAL BULACAN APARTMENT (RESIDENTIAL) # 28 CORINTH ST. BRGY. SAN MANUEL CITY OF [SERVICES/CONTRACTORS] - INK STUDIO DESIGN SJDM BULACAN CONTRACTORS/SERVICE ESTABLISHMENTS # 3 BLK 1 LOT 34 PHASE F-1 FRANCISCO HOMES [SERVICES/CONTRACTORS] - PHOTO DEVELOPING PRINT STATION NARRA CITY OF SAN JOSE DEL MONTE BULACAN # 332 CARRIEDO ST. BRGY. MUZON CITY OF SJDM [SERVICES/CONTRACTORS] - GENDOR GLASS AND ALUMINUM FABRICATION BULACAN CONTRACTORS/SERVICE ESTABLISHMENTS AND STEEL WORKS # 358 STO. DOMINGO ST. BRGY. FATIMA I CITY [RETAILER] - SARI-SARI STORE(ESSENTIAL) CESAR`S STORE OF SJDM BULACAN # 40 IGAY ROAD BGY. STO. CRISTO, CSJDM [RETAILER] - PAINT RETAILER GJ LAGMAN PAINT CENTER BULACAN # 56 MUZON PUBLIC MARKET BRGY. MUZON [RETAILER] - RETAILER [ NON-ESSENTIAL ] CORAZON DEROY PLASTIC WARE TRADING CITY OF SJDM BULACAN [RESTAURANT\CARINDERIAS\EATERIES\ETC.] - # 64 ZONE 1, BGY. MUZON, CSJDM, BULACAN TINS`S SNACK HAUZ EATERY #001 BRGY. MUZON CITY OF SJDM BULACAN [RETAILER] - SARI-SARI STORE(ESSENTIAL) SARI SARI STORE #001 ZONE 1 BRGY, MUZON, DISTRICT 1, SAN [BANK & OTHER FINANCIAL INST.] - MONEY BOAQUIÑA REMITTANCE CENTER JOSE DEL MONTE REMITTANCE #001 ZONE 1 NATIONAL RD BRGY, MUZON, [RETAILER] - SARI-SARI STORE(ESSENTIAL) MBS-R STORE DISTRICT 1, SAN JOSE DEL MONTE #005 B1 L5 ST. -

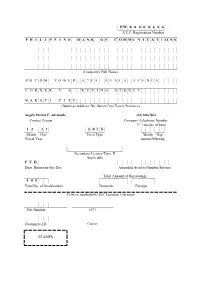

P W 0 0 0 0 0 6 8 6 S.E.C. Registration Number

P W 0 0 0 0 0 6 8 6 S.E.C. Registration Number P H I L I P P I N E B A N K O F C O M M U N I C A T I O N S (Company's Full Name) P B C O M T O W E R , 6 7 9 5 A Y A L A A V E N U E C O R N E R V . A . R U F I N O S T R E E T M A K A T I C I T Y (Business Address: No. Street City/ Town/ Province) Angelo Patrick F. Advincula (02) 830-7062 Contact Person Company Telephone Number 3rd Tuesday of June 1 2 3 1 2 0 I S Month Day Form Type Month Day Fiscal Year Annual Meeting Secondary License Type, If Applicable C F D Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 4 0 5 Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel Concerned File Number LCU Document I.D. Cashier STAMPS We are not asking you for a proxy and you are requested not to send us a proxy. GENERAL INFORMATION Date, Time and Place of Meeting of Security Holders Date : 4 June 2019, Tuesday Time : 10:00 a.m. Place : Manila Golf and Country Club, Harvard Road, Forbes Park, Makati City Mailing Address of the Bank The complete mailing address of the Philippine Bank of Communications (hereinafter, “PBCOM”, the “Bank” or the “Corporation”) is: PHILIPPINE BANK OF COMMUNICATIONS PBCOM Tower, 6795 Ayala Ave. -

Annual Report 2018

[ On[ Onthe the Cover Cover ] ] BountifulBountiful nature nature and and values values generatedgenerated therein therein are arerendered rendered as as beadsbeads of dew/waterof dew/water on ona petal. a petal. Also,Also, the the geometric geometric pattern pattern representsrepresents the the increasingly increasingly complex complex andand diverse diverse roles roles we weare areto play.to play. [ Inquiri[ Inquiries ]es ] TAISEITAISEI CORPO CORPORATIONRATION CSRCSR Promotion Promotion Section, Section, CorporateCorporate Communication Communication Departmen Department , t , CorporateCorporate Planning Planning Office Office E-maiE-mail : [email protected] : [email protected] URLp URL : http://www.taisei.co.jp/english/ : http://www.taisei.co.jp/english/ 1809.1800.T.S1808.15000.T.S 1809.1800.T.S1808.15000.T.S 005_0356501373008.indd005_0356501373008.indd 1-3 1-3 2018/09/192018/09/19 13:18:10 13:18:10 To Create a Vibrant Environment for All Members of Society The Taisei Group creates “safe, secure, and attractive spaces” and “high value” in harmony with the nature, and strives to build a global society filled with dreams and hopes for the next generation. The Taisei Group is rich inactive, diverse human resources working at various sites. At the site of (tentative name) Toranomon 2-10 Project of Tokyo Office, Hotel Okura Tokyo Building Reconstruction Project, we engage in the “Kensetsu Komachi” initiative, which is promoted by the Japan Federa- tion of Construction Contractors, for different activities intended to create a “comfortable workplace” through the synergy of both men and women working at the same workplace. In recognition of such efforts, we won the 3rd Kensetsu-komachi Empowerment Award of Excellence sponsored by the Japan Federation of Construction Contractors in 2017. -

Notice of Filing of Application/S for Alien Employment Permit/S (Aep/S)

PM-NCR-03.01-F.05 NOTICE OF FILING OF APPLICATION/S FOR ALIEN EMPLOYMENT PERMIT/S (AEP/S) Notice is hereby given that the following companies/Employers have filed with this Regional Office application/s for Alien Employment Permit/s: Name and Address of Company/Employ Name of Foreign Position National/Citizenship 1 24/7 BUSINESS PROCESSING INC. Huang, Yang Customer Service 5th - 7th Floor, 81 Newport BL, Newport City, Brgy. Representative (Chinese 183, Pasay , Metro Manila Chinese Accounts) 2 24/7 BUSINESS PROCESSING INC. Yang, Fan Mandarin Speaking Customer 9/F, Capella Bldg., L-3 & 4, B2, Filinvest Alabang, Service Representative Muntinlupa, Metro Manila Chinese 3 2SUCCESS INC. Le Minh Hoang, Customer Service 40/F, Philamlife Tower, 8767 Paseo De Roxas, Bel-Air, Representative Makati City, Metro Manila Vietnamese 4 2SUCCESS INC. Phan Thi Thu Hien, Customer Service 40/F, Philamlife Tower, 8767 Paseo De Roxas, Bel-Air, Representative Makati City, Metro Manila Vietnamese 5 3D ANALYZER INFORMATION Zhao, Zhenyu Customer Service TECHNOLOGIES INC. Representative - Mandarin 7-8/F Double Dragon Plaza, 255 EDSA Cor. Chinese Speaking Macapagal Blvd., Brgy. 076, Pasay City, Metro Manila If you have any information/objection to the above mentioned application/s, please communicate with the Regional Director thru Employment Promotion and Workers Welfare (EPWW) Division with Telephone No. 400-6011. ATTY. MARION S. SEVILLA ATTY. SARAH BUENA S. MIRASOL ASSISTANT REGIONAL DIRECTOR Page 1 of 255 PM-NCR-03.01-F.05 NOTICE OF FILING OF APPLICATION/S FOR ALIEN EMPLOYMENT PERMIT/S (AEP/S) Notice is hereby given that the following companies/Employers have filed with this Regional Office application/s for Alien Employment Permit/s: Name and Address of Company/Employ Name of Foreign Position National/Citizenship 6 3D ANALYZER INFORMATION Tian, Peilin Customer Service TECHNOLOGIES INC. -

Organization Name Substation Class Region 111 Paseo De Roxas Condominium Association Inc

Organization Name Substation Class Region 111 Paseo De Roxas Condominium Association Inc. Zapote CCU Luzon 20-12 Property Holdings, Inc. Muntinlupa CCU Luzon 20-34 Property Holdings, Inc. Muntinlupa CCU Luzon 21st Century Mouldings Corp. Quezon CCU Luzon 21st Century Steel Mill, Inc Taytay CCU Luzon 3-J Plasticworld & Manufacturing Corporation Duhat CCU Luzon 557 Feather Meal Corporation Concepcion CCU Luzon 6776 Ayala Avenue Condominium Corporation Muntinlupa CCU Luzon A.D. Gothong Manufacturing Corporation Mandaue CCU Visayas A1+ Multinational Packaging Inc. Quezon CCU Luzon Abenson Inc. Zapote CCU Luzon ABS-CBN Corporation Dona Imelda CCU Luzon Absolut Distillers, Inc. Calaca CCU Luzon AcBel Polytech Philippines, Inc. Calauan CCU Luzon Acesite (Phils.) Hotel Corporation Manila CCU Luzon ACI, Inc. (Cyberpark 2) Dona Imelda CCU Luzon ACI, INC. -Ali Mall 24-B Dona Imelda CCU Luzon ACI, INC. -Ali Mall 24-F Dona Imelda CCU Luzon Adebe Realty Company, Inc. Zapote CCU Luzon Adriatico Consortium, Inc. Manila CCU Luzon Aeonprime Land Development Corp. (Block 45-Aeon Center) Muntinlupa CCU Luzon Aeonprime Land Development Corporation Zapote CCU Luzon Agripacific Corporation Amadeo CCU Luzon Aichi Forge Philippines, Inc. Sta.Rosa CCU Luzon AIDA UY CUA Duhat CCU Luzon Aikawa Philippines Inc. Calauan CCU Luzon Air Liquide Philippines, Inc. Muntinlupa CCU Luzon AIR LIQUIDE PIPELINE UTILITIES SERVICES (ALPLUS) INC. Sta.Rosa CCU Luzon Air Liquide Pipeline Utilities Services, Inc. Biñan CCU Luzon Air Liquide Pipeline Utilities Services., Inc. Calung Calung CCU Visayas Ajinomoto Philippines Flavor Food Inc. Duhat CCU Luzon Alabang Commercial Corporation Zapote CCU Luzon Alabang Commercial Corporation (ATC Corp Center) Zapote CCU Luzon ALASKA Milk Corporation Biñan CCU Luzon Albay Agro-Industrial Development Corporation Daraga DCU Luzon Ali Makati Hotel Property, Inc. -

Notice of Filing of Application/S for Alien Employment Permit/S (Aep/S)

PM-NCR-03.01-F.05 NOTICE OF FILING OF APPLICATION/S FOR ALIEN EMPLOYMENT PERMIT/S (AEP/S) Notice is hereby given that the following companies/Employers have filed with this Regional Office application/s for Alien Employment Permit/s: Name and Address of Company/Employ Name of Foreign Position National/Citizenship 1 24/7 BUSINESS PROCESSING INC. Yang, Mengjiao Customer Service 5th - 7th Floor, 81 Newport BL, Newport City, Brgy. Representative (Chinese 183, Pasay City, Metro Manila Chinese Accounts) 2 24/7 BUSINESS PROCESSING INC. Cheng, Xianying Customer Service 5th - 7th Floor, 81 Newport BL, Newport City, Brgy. Representative (Chinese 183, Pasay City, Metro Manila Chinese Accounts) 3 24/7 BUSINESS PROCESSING INC. Zhang, Qian Customer Service 5th - 7th Floor, 81 Newport BL, Newport City, Brgy. Representative (Chinese 183, Pasay City, Metro Manila Chinese Accounts) 4 3D ANALYZER INFORMATION Wu, Zhinan Chinese Speaking Customer TECHNOLOGIES INC. Service Representative 7-8/F Double Dragon Plaza, 255 EDSA Cor. Chinese Macapagal Blvd., Brgy. 076, Pasay City, Metro Manila 5 3D ANALYZER INFORMATION Li, Wenyong Chinese Speaking Customer TECHNOLOGIES INC. Service Representative 7-8/F Double Dragon Plaza, 255 EDSA Cor. Chinese Macapagal Blvd., Brgy. 076, Pasay City, Metro Manila If you have any information/objection to the above mentioned application/s, please communicate with the Regional Director thru Employment Promotion and Workers Welfare (EPWW) Division with Telephone No. 400-6011. ATTY. SARAH BUENA S. MIRASOL ATTY. SARAH BUENA S. MIRASOL REGIONAL DIRECTOR Page 1 of 264 PM-NCR-03.01-F.05 NOTICE OF FILING OF APPLICATION/S FOR ALIEN EMPLOYMENT PERMIT/S (AEP/S) Notice is hereby given that the following companies/Employers have filed with this Regional Office application/s for Alien Employment Permit/s: Name and Address of Company/Employ Name of Foreign Position National/Citizenship 6 3D ANALYZER INFORMATION Pan, Da Chinese Speaking Customer TECHNOLOGIES INC. -

Philippine Bank of Communications (PBCOM) Reported a Consolidated Net Income of Php1.17B in 2020

BANKING TABLE OF CONTENTS IN THE NEW About the Cover 1 NORMAL PBCOM Through the Years 2 Our Vision, Mission and Values 3 Chairman’s Message 4 The President Speaks 6 ABOUT THE COVER Banking in the New Normal 10 With a health crisis threatening the world, 2020 was a Our Board of Directors 15 year of challenges for many. A lot of changes had to be Our Senior Management Team 24 made in order to deal with the COVID-19 pandemic. For financial institutions such as PBCOM, the challenge is to Our Business 32 continuously provide the necessary financial services to Our Branch and ATM Network 35 the public without compromising the health and safety of both our employees and the banking public. Sustainability Report 43 Corporate Governance 60 This annual report highlights the successes that PBCOM achieved in 2020 in meeting these challenges. Risk and Capital Management 75 Investments in digital capabilities, product Consumer Protection and Experience 93 enhancements, improvements in service delivery, and the implementation of operational changes, are only Financial Highlights 98 some of the major steps we undertook in order to deliver a superior banking experience in the new normal. 1 Our bank, PBCOM, has a very rich history marked by a legacy of strong relationships nurtured through trust and service. And our thrust to focus on you, our clients, is always the center of everything we do. In 2020, we continue our journey towards building a “digital-first” banking experience for our clients. We have formally launched PBCOMobile, the Bank’s all-mobile banking platform to enhance our other digital offerings. -

Bls with No Entries As of June 1, 2021 Actual Cargo Arrival Date of May 27-31, 2021

PORT OF MANILA - BLs with No Entries as of June 1, 2021 Actual Cargo Arrival Date of May 27-31, 2021 ACTUAL DATE ACTUAL DATE OF No. CONSIGNEE/NOTIFY PARTY CONSIGNEE ADDRESS REGNUM BL DESCRIPTION OF ARRIVAL DISCHARGED ADD 3M COMPOUND BARANGAY BAG MAKING MACHINE WSD 600C BAG SANTA ROSA II MARILAO MAKING MACHINE WSD 450A HS 8477800000 1 3M MF AND KW CORP 5/31/2021 5/31/2021 APL0055-21 ACLY007317 BULACAN 3019 PHILLIPINES TEL FAX 86 510 86321923 REG NO CS201909059 639175655436 FAX 639175655436 EMAIL ALFON SIA MFPACKAGING PH 10TH AND 11TH FLOORS THE FINANCE CENTRE 26TH CORNER 9TH 1X20 AND 1X40 CTNR 26 PACKAGES STC 2 3M PHILIPPINES INC AVENUE 5/30/2021 5/30/2021 APL0060-21 SIN210502677 OFFICE AND LABORATORY SUPPLIES HS BONIFACIO GLOBAL CITY TAGUIG CODE 960390 METRO MANILA 1634 PHILIPPINES 10TH AND 11TH FLOORS THE FINANCE CENTRE 26TH CORNER 9TH PART OF 1X40 CTNR 2 PACKAGES STC OFFICE 3 3M PHILIPPINES INC AVENUE 5/30/2021 5/30/2021 APL0060-21 SIN210586397 AND LABORATORY SUPPLIES HS CODE 391990 BONIFACIO GLOBAL CITY TAGUIG METRO MANILA 1634 PHILIPPINES 10TH AND 11TH FLOORS THE FINANCE CENTRE 26TH CORNER 9TH PART OF 1X40 CTNR 3 PACKAGES STC OFFICE 4 3M PHILIPPINES INC AVENUE 5/30/2021 5/30/2021 APL0060-21 SIN210546460 AND LABORATORY SUPPLIES HS CODE 391990 BONIFACIO GLOBAL CITY TAGUIG METRO MANILA 1634 PHILIPPINES 10TH AND 11TH FLOORS THE FINANCE CENTRE 26TH CORNER 9TH 4X40 CTNR 80 PACKAGES STC OFFICE AND 5 3M PHILIPPINES INC AVENUE 5/30/2021 5/30/2021 APL0060-21 SIN210546459 LABORATORY SUPPLIES HS CODE 630790 BONIFACIO GLOBAL CITY TAGUIG METRO -

MEDTECS INTERNATIONAL CORPORATION LIMITED (Incorporated in Bermuda)

MEDTECS INTERNATIONAL CORPORATION LIMITED (Incorporated in Bermuda) CORRIGENDUM TO ANNUAL REPORT 2017 The Board of Directors (the " Board ") of MEDTECS INTERNATIONAL CORPORATION LIMITED (the "Company ") refers to the Company’s annual report for the financial year ended 31 December 2017 (the “Annual Report 2017 ”) and wishes correct certain inadvertent typographical errors in the Annual Report 2017 to shareholders as set out below. All page references in this announcement are references to the Annual Report 2017. 1. With reference to page 13, the section on Principal Bankers should be amended to reflect the additions as indicated by the bold and underlined text below: “Principal Bankers Bank of SinoPac No. 260, Sec. 2 Beixin Rd., Xiandian Dist., New Taipe City 231, Taiwan Bank of Taiwan 2F-2, No. 66, Sachong Rd.m Nangang Dist., Taipei Taiwan Cathay United Bank - Manila Branch Unit 1, 15 th Floor, Tower 6789 No. 6789 Ayala Avenue, Makati City, 1226 Mega International Commercial Bank Co. 3rd Floor, Pacific Star Building Gil Puyat Avenue, Makati City, Philippines China Banking Corporation CBC Building 8745 Paseo de Roxas Makati City, Philippines Land Bank of Taiwan No. 323, Jingping Rd., Zhonghe Dist., New Taipei City 23577, Taiwan Chang Hwa Bank 3F., No.333, Sec. 1, Keelung Rd., Xinyi Dist., Taipei City 11012, Taiwan Taiwan Business Bank No. 552, Sec. 5, Zhongxiao E. Rd., Xinyi Dist., Taipei City 110, Taiwan ” 2. With reference to page 14, under the Profile of the Board of Directors, the profile of Mr Xia Junwei should be amended to reflect the additions as indicated by the bold and underlined text below and the deletions as indicated by the deleted text below: “Mr Xia Junwei was appointed as a Non-Executive and Non-Independent Director of the Company on 15 October 2015 and Deputy Non-Executive Chairman of the Board on 20 November 2015. -

National Capital Region

LIST OF LICENSED PRIVATE EMPLOYMENT AGENCIES FOR LOCAL EMPLOYMENT, THEIR AUTHORIZED BRANCH OFFICES AND RECRUITERS, BY REGION AS OF 29 MARCH 2021 NAME OF AGENCY EXPIRY DATE National Capital Region 1. 1D MANPOWER SERVICES 2/10/2023 605 ITC BUILDING, #337 SEN. GIL PUYAT AVENUE MAKATI CITY Contact JULITA A. PELANDE . 2. A. A. MAÑALAC MANPOWER SERVICES 3/14/2022 35 BUSTAMANTE STREET, TENAJEROS MALABON CITY Contact MARVIN P. MAÑALAC Tel. 285-0867 0. 3. A7 RECRUITMENT CORPORATION 6/25/2023 4TH FLOOR SM MAKATI CYBERONE BLDG., 373 SEN. GIL PUYAT BEL-AIR VILLAGE, MAKATI CITY Contact VICENTE C. NEPOMUCENO, JR. Tel. 88573700 0. 4. ACES CALL CENTER JOBS INC. 10/1/2021 U605, 6/F, BSA TWIN TOWERS, BANK DRIVE ORTIGAS CTR, BRGY WACK WACK, MANDALUYONG CITY Contact PHILIPS YU Tel. 5014772 Branch Address: Unit 303, The One Executive Office Bldg., #5 West Ave. corner Col. Martinez St., Brgy. Nayong Kanluran, Quezon City 0. 5. ADDFORCE HUMAN RESOURCES SOLUTIONS, INC. 9/26/2021 U 403, FSS BLDG. I, #20 SCT TUASON COR SCT CASTOR STS. BRGY LAGING HANDA, QUEZON CITY Contact GERALD SANVICTORES Tel. 370-0739 0. 6. ADMEREX CAREERS INC. 12/5/2021 14TH & 15TH FLRS THE PEAK TOWER, 107 LP LEVISTE ST., SALCEDO VILLAGE, MAKATI CITY Contact ROBERTO DIZON, JR. Tel. 824-4574 0. BABALA: Ang mga ahensyang ito ay walang pahintulot na magpadala ng anumang uri ng mangagawa o propesyonal sa ibang bansa. Page 1 of 35 NAME OF AGENCY EXPIRY DATE 7. AEVP MANPOWER SERVICES 5/21/2021 24-B ROBINA STREET, BARANGAY BUNGAD, S.F.D.M. -

PHASE I QUALIFIED CONTESTABLE CUSTOMERS (July 2021 Data)

QUALIFIED CONTESTABLE CUSTOMERS (July 2021 Data) PHASE I NAME LOCATION 1 20-12 PROPERTY HOLDINGS, INC. TAGUIG CITY 2 20-34 PROPERTY HOLDINGS, INC. TAGUIG CITY 3 21ST CENTURY STEEL MILL INC. TAYTAY, RIZAL 4 557 FEATHER MEAL CORPORATION CONCEPCION, TARLAC 5 6776 AYALA AVENUE CONDOMINIUM CORPORATION MAKATI CITY 6 7TH INFANTRY DIV. PHIL ARMY PALAYAN CITY, NUEVA ECIJA 7 A.D. GOTHONG MANUFACTURING CORPORATION MANDAUE CITY, CEBU 8 AAC PLANTSITE NEGROS OCCIDENTAL 9 ABENSON INC. PASAY CITY 10 ABS-CBN CORPORATION (200397770101) QUEZON CITY 11 ABS-CBN CORPORATION (200397910101) QUEZON CITY 12 ABSOLUT CHEMICALS LIAN, BATANGAS 13 ACCUPRINT INCORPORATED QUEZON CITY 14 ACESITE (PHILS.) HOTEL CORPORATION MANILA CITY 15 ACI, INC. (200160740101) QUEZON CITY 16 ADEBE REALTY COMPANY, INC. (100146610101) MAKATI CITY 17 ADEBE REALTY COMPANY, INC. (100146620101) MAKATI CITY 18 ADRIATICO CONSORTIUM, INC. MANILA CITY 19 AEGIS PEOPLE SUPPORT REALTY CORPORATION CEBU CITY 20 AFC FERTILIZER AND CHEMICALS, INC. CEBU CITY 21 AFP HNDF PHIL ARMY QUEZON CITY 22 AGRIPACIFIC CORPORATION TANZA, CAVITE 23 AICHI FORGE PHILIPPINES, INC. STA. ROSA, LAGUNA 24 AIKAWA PHILIPPINES INC. STO. TOMAS, BATANGAS 25 AIR LIQUIDE PHILIPPINES, INC. PASIG CITY 26 AIR LIQUIDE PIPELINE UTILITIES SERVICES, INC. (200150140101) CALAMBA, LAGUNA 27 AIR LIQUIDE PIPELINE UTILITIES SERVICES, INC. (9169094711) BALAMBAN CEBU AIR TRANSPORTATION OFFICE (ILOILO INTERNATIONAL 28 CABATUAN, ILOILO AIRPORT) 29 ALABANG COMMERCIAL CORPORATION (100000240101) MUNTINLUPA CITY 30 ALABANG COMMERCIAL CORPORATION (100072280101) MUNTINLUPA CITY 31 ALASKA MILK CORPORATION SAN PEDRO, LAGUNA 32 ALBAY-AGRO INDUSTRIAL DEVELOPMENT CORPORATION MALINAO 33 ALI MAKATI HOTEL PROPERTY, INC. MAKATI CITY 34 ALI-CII DEVELOPMENT CORPORATION PASAY CITY 35 ALLEGRO MICROSYSTEMS PHILIPPINES,INC.