Philippine Bank of Communications (PBCOM) Reported a Consolidated Net Income of Php1.17B in 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Organization Name Substation Class Region 111 Paseo De Roxas Condominium Association Inc

Organization Name Substation Class Region 111 Paseo De Roxas Condominium Association Inc. Zapote CCU LUZON 20-12 Property Holdings, Inc. Sucat CCU LUZON 20-34 Property Holdings, Inc. Sucat CCU LUZON 21st Century Mouldings Corp. Quezon CCU LUZON 21st Century Steel Mill, Inc Dolores CCU LUZON 3-J Plasticworld & Manufacturing Corporation Duhat CCU LUZON 557 Feather Meal Corporation Concepcion CCU LUZON 6776 Ayala Avenue Condominium Corporation Sucat CCU LUZON A.D. Gothong Manufacturing Corporation Mandaue GIS CCU VISAYAS Abenson Inc. Zapote CCU LUZON ABS-CBN Corporation Araneta CCU LUZON AcBel Polytech Philippines, Inc. Calauan CCU LUZON Acesite (Phils.) Hotel Corporation Paco CCU LUZON ACI, Inc. (Cyberpark 2) Araneta CCU LUZON Adebe Realty Company, Inc. Zapote CCU LUZON Adriatico Consortium, Inc. Paco CCU LUZON Aeonprime Land Development Corp. (Block 45-Aeon Center) Sucat CCU LUZON Aeonprime Land Development Corporation Zapote CCU LUZON Agripacific Corporation Amadeo CCU LUZON Aichi Forge Philippines, Inc. Sta.Rosa CCU LUZON Aikawa Philippines Inc. Calauan CCU LUZON Air Liquide Philippines, Inc. Sucat CCU LUZON Air Liquide Pipeline Utilities Services, Inc. BIñan CCU LUZON Air Liquide Pipeline Utilities Services., Inc. Calung Calung CCU VISAYAS Ajinomoto Philippines Flavor Food Inc. Duhat CCU LUZON Alabang Commercial Corporation Zapote CCU LUZON ALASKA Milk Corporation Biñan CCU LUZON Albay Agro-Industrial Development Corporation Tiwi A DCU LUZON Ali Makati Hotel Property, Inc. Sucat CCU LUZON ALI-CII Development Corporation Zapote CCU LUZON Allegro MicroSystems Philippines,Inc. Sucat CCU LUZON AllHome Corp. (AllHome Libis) Dolores CCU LUZON Allied Packaging Corporation Duhat CCU LUZON Alpha Supreme Corp. Duhat CCU LUZON Alphaland Corporation (Alphaland Southgate Tower, Inc.) Zapote CCU LUZON Alphaland Makati Place, Inc. -

World Bank Document

Public Disclosure Authorized PH – RENEWABLE ENERGY DEVELOPMENT PROJECT Public Disclosure Authorized DOCUMENTATION OF THE PUBLIC CONSULTATION MEETING Public Disclosure Authorized May 16, 2013 Public Disclosure Authorized DOCUMENTATION OF THE PUBLIC CONSULTATION MEETING A. BASIC INFORMATION PROJECT NAME: Philippine Renewable Energy Development Project (PhRED) DATE and VENUE: May 16, 2013, 9:00- 12:00 am, Ascott Hotel, Makati City PARTICIPANTS (NUMBER AND AFFILIATION) 30 participants broken down as follows by groupings: (Private Commercial Bank (14), Consultants for Energy Development. Projects (2), Independent Power Providers (2), Dept of Energy (2), National Electrification Authority(3), LGUGC (3) and World Bank (4) B. OBJECTIVES OF THE CONSULTATION: To present the Environment and Social Safeguards Framework (ESSF) and seek suggestions for revisions. C. HIGHLIGHTS OF DISCUSSIONS 1. The PHRED concept and the need for it were presented to the body. The acceptability of this project was expressed by the participants specially the private bank representatives who expressed the need for it. The brown out all over Luzon the previous week helped the participants recognize the need for more stable power supply. 2. The draft ESSF was presented to the body. The participants accept the importance of safeguards operations for project sustainability. It was shared that both the national laws and the World Bank policies on safeguards must be respected. However, concerns were raised on cases of non-compliance. The private banks expressed apprehension that this will be made a condition prior to guarantee approval and/or loan release as well as a ground to withhold payment of guarantee claims. It was noted that non-compliance to safeguards may occur way after release of loans have been made and private banks will no longer have any hold on the borrower. -

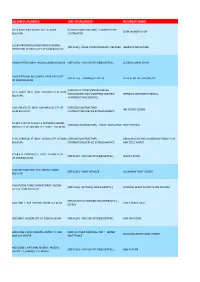

Business Address Line of Business Business Name

BUSINESS ADDRESS LINE OF BUSINESS BUSINESS NAME # 013 BRGY. POBLACION I CITY OF SJDM [SERVICES/CONTRACTORS] - LAUNDRY SHOP SJDM LAUNDRY SHOP BULACAN CONTRACTOR # 166A PROVINCIAL ROAD FARMVIEW BRGY. [RETAILER] - DRUG STORE/PHARMACY RETAILER GENERIKA DRUGSTORE TUNGKONG MANGGA CITY OF SJDM BULACAN # 1824 PARTIDA BRGY MUZON CSJDM BULACAN [RETAILER] - SARI-SARI STORE(ESSENTIAL) CLAIRE & AIRISH STORE # 260 NATIONAL ROAD BRGY. GAYA GAYA CITY [RETAILER] - TRADING (RETAILER) FIL-BEST METAL TRADING INC. OF SJDM BULACAN [LESSORS OF APARTMENT\BOARDING # 277 CARRIEDO ST. BRGY. MUZON CITY OF SJDM HSE\LODGING\INNS \SHOPPING CENTERS] - LERMENG APARTMENT RENTAL BULACAN APARTMENT (RESIDENTIAL) # 28 CORINTH ST. BRGY. SAN MANUEL CITY OF [SERVICES/CONTRACTORS] - INK STUDIO DESIGN SJDM BULACAN CONTRACTORS/SERVICE ESTABLISHMENTS # 3 BLK 1 LOT 34 PHASE F-1 FRANCISCO HOMES [SERVICES/CONTRACTORS] - PHOTO DEVELOPING PRINT STATION NARRA CITY OF SAN JOSE DEL MONTE BULACAN # 332 CARRIEDO ST. BRGY. MUZON CITY OF SJDM [SERVICES/CONTRACTORS] - GENDOR GLASS AND ALUMINUM FABRICATION BULACAN CONTRACTORS/SERVICE ESTABLISHMENTS AND STEEL WORKS # 358 STO. DOMINGO ST. BRGY. FATIMA I CITY [RETAILER] - SARI-SARI STORE(ESSENTIAL) CESAR`S STORE OF SJDM BULACAN # 40 IGAY ROAD BGY. STO. CRISTO, CSJDM [RETAILER] - PAINT RETAILER GJ LAGMAN PAINT CENTER BULACAN # 56 MUZON PUBLIC MARKET BRGY. MUZON [RETAILER] - RETAILER [ NON-ESSENTIAL ] CORAZON DEROY PLASTIC WARE TRADING CITY OF SJDM BULACAN [RESTAURANT\CARINDERIAS\EATERIES\ETC.] - # 64 ZONE 1, BGY. MUZON, CSJDM, BULACAN TINS`S SNACK HAUZ EATERY #001 BRGY. MUZON CITY OF SJDM BULACAN [RETAILER] - SARI-SARI STORE(ESSENTIAL) SARI SARI STORE #001 ZONE 1 BRGY, MUZON, DISTRICT 1, SAN [BANK & OTHER FINANCIAL INST.] - MONEY BOAQUIÑA REMITTANCE CENTER JOSE DEL MONTE REMITTANCE #001 ZONE 1 NATIONAL RD BRGY, MUZON, [RETAILER] - SARI-SARI STORE(ESSENTIAL) MBS-R STORE DISTRICT 1, SAN JOSE DEL MONTE #005 B1 L5 ST. -

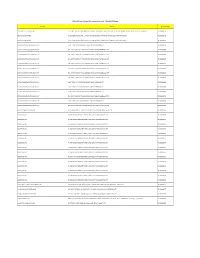

Top 100 Stockholders - Philippine H2O Ventures Corp

Top 100 Stockholders - Philippine H2O Ventures Corp. Count Stockholder # Stockholder Name Address Nationality TIN Number Of Shares Percentage 1 PCD Fil PCD Filipino N/A PH N/A 231,441,320.00 95.15 % 2 PCD Non-Fil PCD Non-Filipino N/A OA N-A 11,676,801.00 4.80 % 3 0000225748 YU KOK SEE 27 TIRAD PASS QUEZON CITY PH 106,272.00 0.04 % 4 0000225735 ASTURIAS, MARCIAL RONALD T. V.V. SOLIVEN COR. FELIX AVE. CAINTA RIZAL PH 7,200.00 0.00 % 5 0000225740 PASCUA, ROGELIO N. 29 DOLLAR MERALCO VILL. TAYTAY RIZAL PH 3,024.00 0.00 % 6 0000227991 MIGUEL DE CASTRO MARANA OR BITUIN DE CASTRO MARANA C/O AVON COSMETICS INC. ZAMBOANGA BRANCH CANELAR STREET,ZAMBOANGA CITY PH 241-338-761 3,000.00 0.00 % 7 0000225738 MORELOS, LILIAN GUISON 946 MA. CRISTINA SAMPALOC MANILA PH 2,160.00 0.00 % 8 1800300492 ERIC O. RECTO 5TH FLOOR PBCOM TOWER 6795, AYALA AVENUE, MAKATI CITY, METRO MANILA PH 108-730-891-000 1,000.00 0.00 % 9 0000225739 PANG, VICENTE LIM 1022 CORTADA STREET ERMITA, MANILA PH 432.00 0.00 % 10 0000240022 LIMGENCO, DONDI RON R. 886B MARQUITOS ST., SAMPALOC MANILA 1008 PHILIPPINES PH 302-242-112 111.00 0.00 % 11 1800300482 SHAREHOLDERS' ASSOCIATION OF THE PHILIPPINES, INC. UNIT 1003, 10TH FLOOR CITYLAND PASONG TAMO TOWER, 2210 DON CHINO ROCES AVE., MAPH 007-553-100 100.00 0.00 % 12 0000226005 AU, OWEN NATHANIEL S. AU ITF: LI MARCUS B9 L5 MT. TABOR ST., MT. VIEW SUBD., MANDALAGAN, BACOLOD CITY PH 197-550-637 75.00 0.00 % 13 0000225720 QUINTANA, DEXTER E. -

Modelo Direcciones

EMPRESAS ESPAÑOLAS ESTABLECIDAS EN: Filipinas Página 1 de 7 Directorio Empresas Españolas en Filipinas Actualización 30-may.-18 Empresa Española: ACERINOX SA SEDE LOCAL: ACERINOX (SEA) PTD LTD Dirección: 6795 Ayala Avenue Corner VA Rufino Street SECTOR DE ACTIVIDAD SEDE LOCAL Office 4010 40th Floor PBCom Tower - PRODUCTOS DE FUNDICIÓN Y SIDERÚRGICOS C.P. / Ciudad: 1226 Makati City Provincia: Metro Manila País: Filipinas Tel.: 6327899113 Fax: 6327899001 Email: Web: www.acerinox.com/es/ Empresa Española: AMADEUS IT GROUP SA SEDE LOCAL: AMADEUS MARKETING PHILIPPINES INC Dirección: Ayala Avenue SECTOR DE ACTIVIDAD SEDE LOCAL LKG Tower 6801 36th Floor - SERVICIOS TIC RELACIONADOS CON VIAJES Y TURISMO C.P. / Ciudad: 1227 Makati City Provincia: Metro Manila País: Filipinas Tel.: 6328577100 Fax: 6328577198 Email: Web: www.amadeus.com Empresa Española: BIOSYSTEMS SA SEDE LOCAL: BIOSYSTEMS REAGENTS & INSTRUMENTS INC Dirección: 74 Scout Dr Lazcano Brgy SECTOR DE ACTIVIDAD SEDE LOCAL Laging Handa - INSTRUMENTAL MÉDICO Y QUIRÚRGICO - MATERIAL FUNGIBLE C.P. / Ciudad: 1103 Quezon City Provincia: Metro Manila País: Filipinas Tel.: 6324127689 Fax: 6324756012 Email: Web: www.biosystems.ph/ Empresa Española: CALIDAD PASCUAL SA SEDE LOCAL: ABI PASCUAL FOODS Dirección: 6754 Ayala Avenue SECTOR DE ACTIVIDAD SEDE LOCAL Allied Bank Center 6th Floor - YOGURES C.P. / Ciudad: 1200 Makati City Provincia: Metro Manila País: Filipinas Tel.: 6328163421 Fax: 6328193463 Email: Web: creamydelightyogurt.ph Empresa Española: CENTUNION ESPAÑOLA DE COORDINACION TECNICA Y FINANCIERA SA SEDE LOCAL: CENTUNION PHILIPPINES INC Dirección: 199 Salcedo Street Legazpi Village SECTOR DE ACTIVIDAD SEDE LOCAL Fedman Suites Building Unit 704 7th Floor - SERVICIOS INTEGRADOS DE INGENIERIA DE INFRAESTRUCTURA CIVIL C.P. -

08 October 2015 the PHILIPPINE STOCK EXCHANGE, INC

08 October 2015 THE PHILIPPINE STOCK EXCHANGE, INC. Philippine Stock Exchange Plaza Ayala Triangle, Ayala Avenue Makati City Attention: Ms. Janet A. Encarnacion Head – Disclosure Department Dear Ms. Encarnacion: In connection with PSE Disclosure Rules, please find attached list of Top 100 Stockholders of East West Banking Corporation (EW) as of September 30, 2015. Thank you. Very truly yours, Stock Transfer Service Inc. EAST WEST BANKING CORPORATION List of Top 100 Stockholders As of 09/30/2015 Rank Sth. No. Name Citizenship Holdings Rank ------------------------------------------------------------------------------------------------------------------------ 1 0000000014 PCD NOMINEE CORPORATION (FILIPINO Filipino 487,027,283 32.47% 37/F ENTERPRISE CENTER AYALA AVENUE MAKATI CITY 2 0000000001 FILINVEST DEVELOPMENT CORPORATION Filipino 451,354,890 30.09% C/O EAST WEST BANKING CORPORATION 20/F PBCom Tower 6795 Ayala Ave. Makati City 3 0000000002 FILINVEST DEVELOPMENT CORPORATION FOREX Filipino 394,941,030 26.33% C/O EAST WEST BANKING CORPORATION 20/F PBCom Tower 6795 Ayala Ave. Makati City 4 0000000015 PCD NOMINEE CORPORATION (NON-FILIPINO) Foreign 162,083,230 10.81% 37/F ENTERPRISE CENTER AYALA AVENUE MAKATI CITY 5 0063181664 F. YAP SECURITIES INC Filipino 2,060,089 00.14% 17/F LEPANTO BLDG 8747 PASEO DE ROXAS MAKATI CITY 6 0000000030 ALFONSO S. TEH Filipino 450,000 00.03% #14 SCOUT MADRINAN ST., SOUTH TRIANGLE,QUEZON CITY 7 0000000049 PHILIPPINE AIR FORCE EDUCATIONAL FUND, INC. Filipino 390,000 00.03% 2/F SGV II BLDG.,#6758 AYALA AVE., MAKATI CITY 8 0000000042 WASHINGTON SYCIP American 322,000 00.02% 14/F SGV I BLDG., #6760 AYALA AVE., MAKATI CITY 9 0000000038 GERARDO SUSMERANO Filipino 320,000 00.02% 5/F THE PODIUM OF BEAUFORT 5TH AVE., COR. -

DOLE-NCR for Release AEP Transactions As of 7-16-2020 12.05Pm

DOLE-NCR For Release AEP Transactions as of 7-16-2020 12.05pm Company Address Transaction No. 3M SERVICE CENTER APAC, INC. 17TH, 18TH, 19TH FLOORS, BONIFACIO STOPOVER CORPORATE CENTER, 31ST STREET COR., 2ND AVENUE, BONIFACIO GLOBAL CITY, TAGUIG CITY TNCR20000756 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000178 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000283 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000536 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000554 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000569 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000607 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000617 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000632 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000633 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000638 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000680 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY -

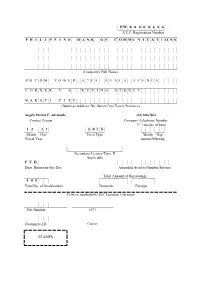

P W 0 0 0 0 0 6 8 6 S.E.C. Registration Number

P W 0 0 0 0 0 6 8 6 S.E.C. Registration Number P H I L I P P I N E B A N K O F C O M M U N I C A T I O N S (Company's Full Name) P B C O M T O W E R , 6 7 9 5 A Y A L A A V E N U E C O R N E R V . A . R U F I N O S T R E E T M A K A T I C I T Y (Business Address: No. Street City/ Town/ Province) Angelo Patrick F. Advincula (02) 830-7062 Contact Person Company Telephone Number 3rd Tuesday of June 1 2 3 1 2 0 I S Month Day Form Type Month Day Fiscal Year Annual Meeting Secondary License Type, If Applicable C F D Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 4 0 5 Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel Concerned File Number LCU Document I.D. Cashier STAMPS We are not asking you for a proxy and you are requested not to send us a proxy. GENERAL INFORMATION Date, Time and Place of Meeting of Security Holders Date : 4 June 2019, Tuesday Time : 10:00 a.m. Place : Manila Golf and Country Club, Harvard Road, Forbes Park, Makati City Mailing Address of the Bank The complete mailing address of the Philippine Bank of Communications (hereinafter, “PBCOM”, the “Bank” or the “Corporation”) is: PHILIPPINE BANK OF COMMUNICATIONS PBCOM Tower, 6795 Ayala Ave. -

2017 Integrated Annual Corporate Governance Report

Secutitieg aner Exchonge NIsvto Commission @\ SEC FORM _ I-ACGR INTEGRATED ANNUAT CORPORATE GOVERNANCE REPORT t. For the fiscal year ended: December 3 1. 20 1 7 2. SEC Identification Number: PW-686 3. BIR Tax Identification No.: 000-263-340 4. Exact name of issuer as specified in its charter: PHILIPPINE BANK 0F COMMUNICATIONS 5, Philippines (SEC Use Only) Province, Country or otherjurisdiction of Industrv Classification Code: incorporation or organization 7, 7226 Address ofprincipal office Postal Code 8, 830-7000 Issuer's telephone number, including area code 9. NA Former name, former address, and former fiscal year, if changed since last report. * SEC Form - I-ACGR Uodated 21,Dec2OI7 Page 3 of 80 INTEGRATED ANNUAL CORPORATE GOVERNANCE REPORT RECOMMENDED CG COMPLIANT ADDITIONAL INFORMATION EXPLANATION PRACTICE/POLICY / NON- COMPLIANT The Board’s Governance Responsibilities Principle 1: The company should be headed by a competent, working board to foster the long- term success of the corporation, and to sustain its competitiveness and profitability in a manner consistent with its corporate objectives and the long- term best interests of its shareholders and other stakeholders. Recommendation 1.1 1. Board is composed of directors Compliant • Eric O. Recto – Chairman of the Board & Director with collective working Mr. Recto, Filipino, 54 years old, was elected Director and Vice Chairman of the knowledge, experience or Board on July 26, 2011, appointed Co-Chairman of the Board on January 18, 2012 expertise that is relevant to the and Chairman of the Board on May 23, 2012. He is the Chairman and CEO of ISM company’s industry/sector. -

ANNUAL STATEMENT of PETROGEN INSURANCE CORPORATION SMC Head Office Complex, 40 San Miguel Ave., Mandaluyong City

COMPANY LOGO ANNUAL STATEMENT OF PETROGEN INSURANCE CORPORATION SMC Head Office Complex, 40 San Miguel Ave., Mandaluyong City Submitted to the INSURANCE COMMISSION Manila, Philippines For the Year Ended DECEMBER 31, 2020 NON-LIFE Submitted to the Philippine Insurance Commission Pursuant to the laws of the Republic of the Philippines. Denomination Amount Rate of USD 48.023 Exchange ANNUAL STATEMENT FOR THE YEAR ENDED: December 31, 2020 OF PETROGEN INSURANCE CORPORATION COMPANY PROFILE Certificate of Authority No… 2019/84-R Adminsitrative Order: Tax Account Number: 005-034-674-000 Date of Issue : January 01, 2019 Date of Issue : Date of Issue : September 10, 1996 Date of Original Issue…………………………….…….……. Incorporated on…………………….………………………………. August 23, 1996 Telephone no.: 8-886-3888 Commenced business on………………………………..…. January 02, 1997 Fax no.: 8-884-9163 Incorporated in the Philippines as: Domestic: ….................................. P SEC Certificate of Registration No.: A1996-04801 (please put a ✓ in the box) Domestically Incorporated …........ Registered Trade Name: Branch …...................................... Home Office address……………………………….…… SMC Head Office Complex, 40 San Miguel Ave., Mail address SMC Head Office Complex, 40 San Miguel Ave., Mandaluyong City Mandaluyong City Corporate Residence Certificate No……………………………………………...……CCC2016 00204536 Issued at Mandaluyong on 18-Jan-20 Website Email Address MEMBERS OF THE BOARD, OFFICERS AND EMPLOYEES TERM OF OFFICE AMOUNT POSITION NAME NATIONALITY # SHARES OWNED TO FROM Chairman Lubin B. Nepomuceno Present 12-Mar-2013 Filipino 1 1,000.00 Vice-Chairman Directors (Note 1) Member Emmanuel E. Eraña Present 25-Feb-2009 Filipino 1 1,000.00 Member Robert Coyiuto Jr. Present 07-Oct-2010 Filipino 1 1,000.00 Member Independent Director Carmen N. -

Annual Report 2018

[ On[ Onthe the Cover Cover ] ] BountifulBountiful nature nature and and values values generatedgenerated therein therein are arerendered rendered as as beadsbeads of dew/waterof dew/water on ona petal. a petal. Also,Also, the the geometric geometric pattern pattern representsrepresents the the increasingly increasingly complex complex andand diverse diverse roles roles we weare areto play.to play. [ Inquiri[ Inquiries ]es ] TAISEITAISEI CORPO CORPORATIONRATION CSRCSR Promotion Promotion Section, Section, CorporateCorporate Communication Communication Departmen Department , t , CorporateCorporate Planning Planning Office Office E-maiE-mail : [email protected] : [email protected] URLp URL : http://www.taisei.co.jp/english/ : http://www.taisei.co.jp/english/ 1809.1800.T.S1808.15000.T.S 1809.1800.T.S1808.15000.T.S 005_0356501373008.indd005_0356501373008.indd 1-3 1-3 2018/09/192018/09/19 13:18:10 13:18:10 To Create a Vibrant Environment for All Members of Society The Taisei Group creates “safe, secure, and attractive spaces” and “high value” in harmony with the nature, and strives to build a global society filled with dreams and hopes for the next generation. The Taisei Group is rich inactive, diverse human resources working at various sites. At the site of (tentative name) Toranomon 2-10 Project of Tokyo Office, Hotel Okura Tokyo Building Reconstruction Project, we engage in the “Kensetsu Komachi” initiative, which is promoted by the Japan Federa- tion of Construction Contractors, for different activities intended to create a “comfortable workplace” through the synergy of both men and women working at the same workplace. In recognition of such efforts, we won the 3rd Kensetsu-komachi Empowerment Award of Excellence sponsored by the Japan Federation of Construction Contractors in 2017. -

Masterlist of Private Schools Sy 2011-2012

Legend: P - Preschool E - Elementary S - Secondary MASTERLIST OF PRIVATE SCHOOLS SY 2011-2012 MANILA A D D R E S S LEVEL SCHOOL NAME SCHOOL HEAD POSITION TELEPHONE NO. No. / Street Barangay Municipality / City PES 1 4th Watch Maranatha Christian Academy 1700 Ibarra St., cor. Makiling St., Sampaloc 492 Manila Dr. Leticia S. Ferriol Directress 732-40-98 PES 2 Adamson University 900 San Marcelino St., Ermita 660 Manila Dr. Luvimi L. Casihan, Ph.D Principal 524-20-11 loc. 108 ES 3 Aguinaldo International School 1113-1117 San Marcelino St., cor. Gonzales St., Ermita Manila Dr. Jose Paulo A. Campus Administrator 521-27-10 loc 5414 PE 4 Aim Christian Learning Center 507 F.T. Dalupan St., Sampaloc Manila Mr. Frederick M. Dechavez Administrator 736-73-29 P 5 Angels Are We Learning Center 499 Altura St., Sta. Mesa Manila Ms. Eva Aquino Dizon Directress 715-87-38 / 780-34-08 P 6 Angels Home Learning Center 2790 Juan Luna St., Gagalangin, Tondo Manila Ms. Judith M. Gonzales Administrator 255-29-30 / 256-23-10 PE 7 Angels of Hope Academy, Inc. (Angels of Hope School of Knowledge) 2339 E. Rodriguez cor. Nava Sts, Balut, Tondo Manila Mr. Jose Pablo Principal PES 8 Arellano University (Juan Sumulong campus) 2600 Legarda St., Sampaloc 410 Manila Mrs. Victoria D. Triviño Principal 734-73-71 loc. 216 PE 9 Asuncion Learning Center 1018 Asuncion St., Tondo 1 Manila Mr. Herminio C. Sy Administrator 247-28-59 PE 10 Bethel Lutheran School 2308 Almeda St., Tondo 224 Manila Ms. Thelma I. Quilala Principal 254-14-86 / 255-92-62 P 11 Blaze Montessori 2310 Crisolita Street, San Andres Manila Ms.